Coworking Spaces Market Report Scope & Overview:

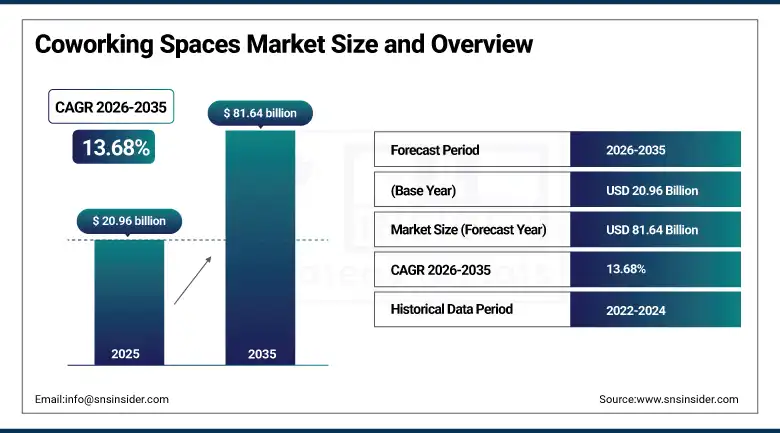

The Coworking Spaces market was valued at USD 20.96 Billion in 2025 and is expected to reach USD 81.64 Billion by 2035, growing at a CAGR of 13.68% from 2026–2035.

The global coworking spaces market is undergoing a structural transformation that has fundamentally repositioned flexible workspace from a niche offering serving freelancers and early-stage startups into a mainstream commercial real estate category that Fortune 500 corporations, financial institutions, technology companies, and professional services firms are actively incorporating into their property strategies as a permanent and growing component of their total office footprint. The convergence of post-pandemic hybrid work model normalization, the progressive recognition by corporate real estate executives that fixed long-term office leases represent an inflexible capital commitment in an environment of structural work pattern uncertainty, and the maturation of coworking space operators’ enterprise service capabilities to deliver the security, reliability, compliance, and customization standards that large organizations require has catalysed the market’s evolution from a disruptive niche to an established real estate sector.

The January 2025 acquisition of Industrious by CBRE Group, creating a new Building Operations & Experience business segment within the world’s largest commercial real estate services firm, represents the most definitive institutional validation of coworking’s permanent place in the commercial property ecosystem, signaling that major real estate capital allocators view flexible workspace not as a temporary accommodation for post-pandemic disruption but as a structurally growing product category warranting integration into mainstream real estate portfolio management at the highest institutional level.

Market Size and Forecast

-

Market Size in 2026E: USD 23.83 Billion

-

Market Size by 2035: USD 81.64 Billion

-

CAGR: 13.68% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Coworking Spaces Market - Request Free Sample Report

Coworking Spaces Market Trends

-

Progressive corporate enterprise adoption of coworking and managed flexible workspace solutions as a permanent component of hybrid work real estate strategies, with Fortune 500 companies and large professional services firms signing multi-location, multi-year enterprise agreements with coworking operators that provide distributed workspace access for their employee populations across city networks and international markets without the capital commitment, administrative burden, and inflexibility of equivalent traditional leased office footprints.

-

Rapid expansion of technology integration within coworking space operations, including AI-powered space reservation and utilisation optimization systems, IoT-enabled environmental controls that adjust lighting, temperature, and air quality to occupancy and individual preference data, biometric access control, and digital community platforms that enhance member networking, collaboration, and space management experiences across both physical and virtual coworking interactions.

-

Growing development of industry-specific coworking formats including life sciences and laboratory coworking spaces that provide wet lab infrastructure and scientific equipment on flexible terms, legal and compliance professional coworking environments with secure meeting facilities and client confidentiality infrastructure, creative industry coworking hubs with production equipment and content creation facilities, and healthcare professional coworking spaces with examination room access, creating premium specialist workspace sub-segments within the broader flexible workspace market.

-

Accelerating expansion of coworking operators into tier-2 and tier-3 cities across Asia Pacific, Latin America, Eastern Europe, and Africa driven by the combination of urbanization growth creating professional worker populations in secondary cities, rising entrepreneurship and startup activity in emerging technology hubs beyond primary metropolitan centers, and remote work adoption allowing knowledge workers to relocate from expensive primary cities while maintaining professional workspace access.

-

Rising adoption of wellness-oriented coworking design that prioritizes biophilic design elements, natural light maximization, acoustic management, ergonomic furniture specifications, outdoor workspace areas, fitness facilities, and mental health support amenities as coworking operators compete for premium member segments who priorities workspace environment quality as a meaningful component of their overall productivity, wellbeing, and professional identity.

The U.S. Coworking Spaces Market Outlook

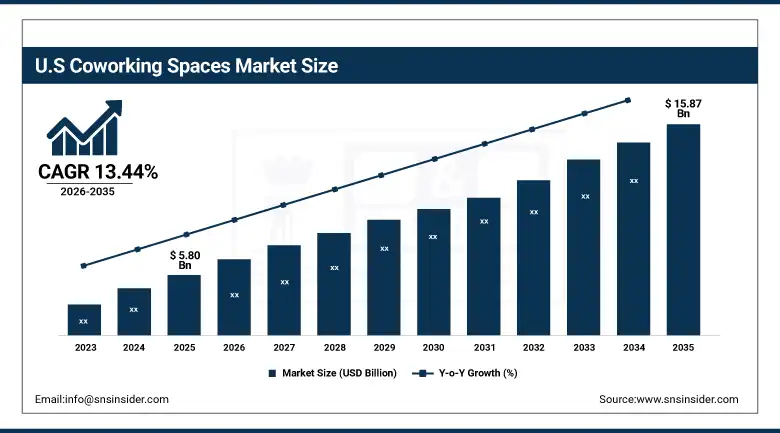

The U.S. coworking spaces market was valued at approximately USD 5.80 Billion in 2025 and is expected to reach approximately USD 15.87 Billion by 2035, growing at a CAGR of 13.44%.

The United States coworking market is defined by the coexistence of national network operators with thousands of locations including IWG’s Regus, Spaces, and HQ brands alongside specialist premium operators including Industrious, The Wing, and Serendipity Labs, technology company-specific facilities, and thousands of independent local coworking spaces that serve distinct community and geographic niches that national operators do not efficiently serve. The technology sector in San Francisco, New York, Austin, Seattle, and Boston represents the largest single driver of U.S. coworking demand, as the concentration of high-growth startups, venture capital-backed companies, and established technology enterprises whose distributed workforce models create demand for flexible workspace that can scale with headcount variability and geographic expansion without the lead times and capital commitments of conventional office leasing generates the highest per-square-meter coworking revenue in the global market.

The commercial real estate industry’s structural oversupply problem in major U.S. cities, where office vacancy rates in many downtown markets exceed 20%, is creating a paradoxical opportunity for coworking operators who can partner with building owners to convert underutilised traditional office floors into managed flexible workspace products, accessing premium locations at economics that would have been unavailable during the pre-pandemic tight commercial real estate market and simultaneously providing building owners with a revenue-generating alternative to leaving vacant space idle while the traditional office market finds its new equilibrium.

Coworking Spaces Market Segment Analysis

-

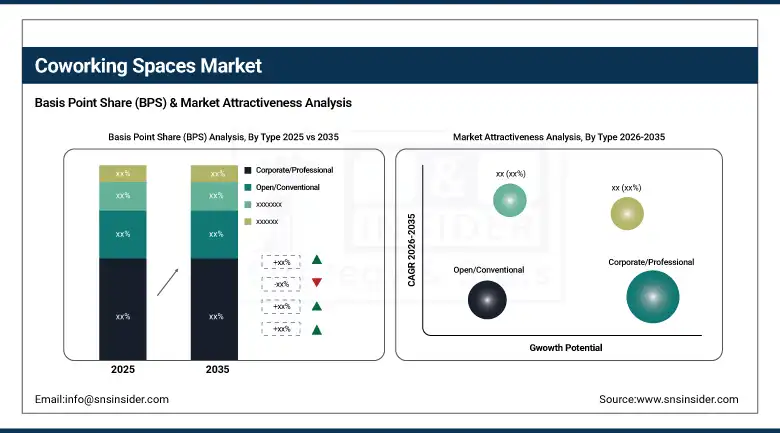

By Type, Corporate/Professional segment led the Coworking Spaces Market with approximately 27.60% revenue share in 2025; Conventional/Open coworking is the fastest-growing segment at a CAGR of approximately 14.1%.

-

By Nature, Managed segment led the Coworking Spaces Market with approximately 24.40% revenue share in 2025; Hybrid segment is the fastest-growing nature segment at a CAGR of approximately 14.30%.

-

By Application, SMEs led the Coworking Spaces Market with approximately 29.50% revenue share in 2025; Freelancers is the fastest-growing application segment at a CAGR of approximately 14.66%

By Type, Corporate/Professional type dominates, Conventional grows fastest

Corporate/Professional coworking retained the leading type position with approximately 27.60% of the Coworking Spaces Market in 2025, a dominance rooted in its comprehensive service proposition that goes substantially beyond physical workspace to deliver the professional infrastructure, support services, and community environment that modern knowledge workers and business teams require to operate effectively in a shared space setting. The corporate coworking format’s competitive strength lies in its ability to deliver a comprehensive professional environment that includes private offices and enclosed meeting rooms alongside shared open work areas, high-specification telecommunications and IT infrastructure, reception and business support services, and access to a curated community of fellow professionals and potential collaborators, creating a workspace experience that compares favorably with the self-managed traditional office for most categories of professional work.

Conventional or Open coworking is the fastest-growing type segment at a CAGR of approximately 14.1% through 2035, driven primarily by its expansion across tier-2 and tier-3 cities in Asia Pacific, Latin America, and Eastern Europe where it serves as the primary market entry format for coworking operators seeking to establish flexible workspace presence in markets where the professional user base and price sensitivity profile favors cost-effective open-plan shared environments over premium corporate coworking configurations.

By Nature, SMEs dominate applications, Freelancers grow fastest

SMEs retained the leading application position with approximately 29.50% of the Coworking Spaces Market in 2025, reflecting the structural alignment between the small and medium enterprise’s need for professional office infrastructure, the financial constraints that make long-term commercial leasing disproportionately burdensome relative to SME revenue scales, and the coworking model’s ability to provide the complete professional office experience on month-to-month terms that match SME cash flow management preferences and growth trajectory flexibility requirements. The SME sector’s coworking demand is particularly concentrated in professional services, technology, creative, and consulting sectors where client-facing professionalism and collaborative team working environments matter commercially, making the investment in shared professional workspace a direct business development and operational productivity investment rather than simply an overhead expenditure.

Freelancers is the fastest-growing application segment at a CAGR of approximately 14.66% through 2035, propelled by the extraordinary expansion of the global independent professional workforce driven by platform economy growth, corporate workforce restructuring that has converted many formerly employed positions into contracted independent roles, and the progressive cultural normalization of freelance career paths across professional disciplines from software development and design through legal, financial, and marketing consulting. The World Bank and Statista projections of the global freelance workforce reaching 540 million by 2027 define an application segment that is growing faster than the overall coworking market and converting to coworking use at increasing rates as the professional and wellbeing limitations of sustained home working drive freelancers who can afford coworking membership toward shared professional workspace alternatives that provide social connection, professional community, and separation between work and personal life that home offices cannot replicate.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Coworking Spaces Market Insights

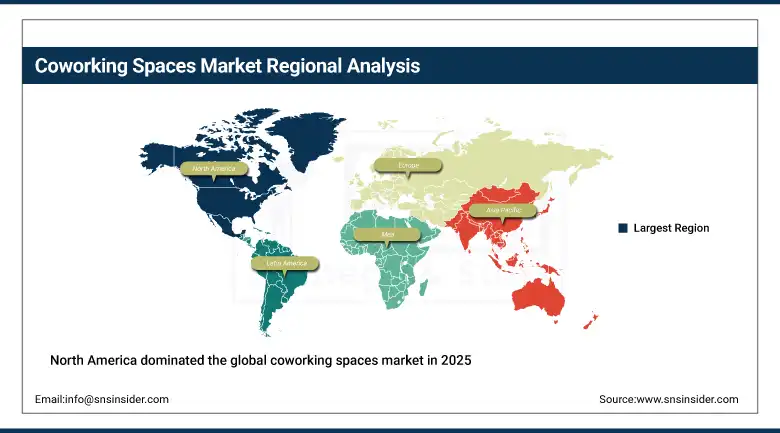

North America dominated the global coworking spaces market in 2025, with the United States accounting for approximately 87.4% of North American revenues, driven by the world’s most advanced hybrid work corporate adoption, the highest concentration of technology sector coworking demand, and the mature flexible workspace operator ecosystem anchored by IWG’s extensive multi-brand network, the post-acquisition CBRE Industrious platform, WeWork’s restructured operations, and dozens of regional premium operators serving distinct market segments across major metropolitan areas. The U.S. market benefits from the structural transformation of corporate real estate strategy that has made flexible workspace a board-level consideration for many large companies, with chief people officers and chief financial officers jointly advocating for flexible workspace allocation as an enabler of talent acquisition, workforce flexibility, and cost management objectives that fixed long-term leases cannot simultaneously serve. Canada contributes approximately 12.6% of North American coworking revenues through a technology and professional services sector in Toronto, Vancouver, and Montreal that mirrors U.S. hybrid work adoption trends and a growing French-Canadian entrepreneurship ecosystem in Quebec that is creating coworking demand in markets where the bilingual professional environment creates specific workspace community preferences.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Coworking Spaces Market Insights

Europe is the world’s second-largest coworking market, characterised by a sophisticated and diverse flexible workspace landscape that ranges from IWG’s pan-European network of corporate business centers through WeWork’s premium urban locations to a rich ecosystem of independent and specialist coworking operators who serve the region’s diverse professional communities, creative industries, technology hubs, and social enterprise sectors with workspace products that reflect European professional culture’s emphasis on work-life quality, sustainable design, and community belonging. Germany accounts for approximately 22.3% of European coworking revenues as the region’s largest national market, driven by a strong Mittelstand entrepreneurship culture, a rapidly growing technology startup ecosystem in Berlin, Munich, Hamburg, and Frankfurt, and the progressive adoption of flexible workspace by German corporate enterprises whose traditionally conservative office culture is adapting to the workforce expectations of younger professional demographics who priorities flexible work arrangements as a significant employment consideration. The European coworking market is also being shaped by the growth of pan-European regulatory and sustainability standards that are creating demand for certified sustainable coworking environments, as operators invest in green building certifications, carbon neutral operations, and circular economy design principles that align with the values of the environmentally conscious professional demographics that represent the premium coworking membership market across the region.

Asia Pacific Coworking Spaces Market Insights

Asia Pacific is the fastest-growing regional coworking market at a CAGR of approximately 14.66%, driven by a convergence of urbanization growth creating professional populations in cities across China, India, Indonesia, Vietnam, and the Philippines that are demanding professional workspace infrastructure faster than traditional commercial real estate supply can provide, a thriving startup and entrepreneurship ecosystem that generates intense coworking demand in innovation hubs including Bangalore, Shenzhen, Singapore, Jakarta, and Ho Chi Minh City, and the progressive adoption of hybrid work models by multinational corporations operating across the region whose Asia Pacific workforce management strategies increasingly incorporate flexible workspace as a core tool for distributed team collaboration. China accounts for approximately 61.7% of Asia Pacific coworking revenues and represents the most dynamic coworking market in the world by expansion rate and new location development velocity, with domestic operators including Ucommune, SOHO 3Q, and Kr Space building extensive national coworking networks alongside international brands including WeWork and IWG’s Regus brand that are competing for the premium corporate and startup segments of China’s extraordinarily large and rapidly evolving flexible workspace demand.

Latin America and MEA Coworking Spaces Market Insights

Latin America and the Middle East and Africa are fast-developing coworking markets where urbanization growth, entrepreneurship ecosystem development, and the adoption of hybrid work models by multinational corporations are creating the conditions for substantial coworking market expansion across professional populations that were previously served almost exclusively by traditional leased office formats. Brazil accounts for approximately 44.2% of Latin American coworking revenues through the combination of São Paulo’s status as Latin America’s primary financial and technology hub generating dense coworking demand across a large professional population, a growing startup ecosystem in Rio de Janeiro, Curitiba, and Belo Horizonte, and IWG’s recent expansion of Regus coworking suites into shopping mall locations across major Brazilian cities that is extending flexible workspace accessibility to professionals in non-traditional commercial districts. Saudi Arabia leads Middle East and Africa coworking revenues at approximately 38.4% of the regional total, driven by Vision 2030’s entrepreneurship development agenda creating institutional support for coworking infrastructure as a component of startup ecosystem building, high purchasing power enabling premium coworking membership adoption, and the progressive normalization of flexible professional work arrangements among the Kingdom’s young urban workforce whose career expectations increasingly include workspace flexibility as a standard professional benefit.

Market Dynamics

Growth Drivers: Hybrid work model normalization driving corporate enterprise flexible workspace adoption, global freelance workforce expansion increasing independent professional coworking demand, and technology integration improving coworking space operational efficiency and member experience

The primary structural growth drivers for the Coworking Spaces Market are the irreversible normalization of hybrid work across corporate organizations globally that has structurally reduced the fixed office space required per employee while simultaneously increasing demand for flexible professional workspace that corporate employees can access on an as-needed basis across distributed locations, combined with the extraordinary expansion of the global independent professional and freelance workforce that is creating a growing population of knowledge workers whose workspace needs are precisely served by the monthly-subscription, plug-and-play, community-embedded coworking model. The corporate real estate industry’s post-pandemic rethinking of office portfolio strategy, increasingly guided by total occupancy cost optimization frameworks that weight flexibility and scalability alongside cost-per-seat metrics, is driving enterprise real estate decisions toward flexible workspace allocations that can be adjusted quarterly rather than locked into five to ten year traditional lease commitments, creating a structural demand shift that benefits coworking operators whose enterprise service capabilities have matured to meet corporate security, compliance, and customization requirements.

Restraints: Commercial real estate availability and cost constraints in premium urban locations, data security and privacy concerns limiting enterprise adoption, and market saturation risk in major metropolitan primary markets

A meaningful restraint on the Coworking Spaces Market is the commercial real estate availability and cost structure in the premium urban locations where coworking demand is highest, as the combination of elevated base rental costs, fit-out capital requirements, and the revenue uncertainty of month-to-month membership models creates challenging unit economics for coworking operators seeking to establish and maintain financially viable locations in city center districts where the highest concentration of professional workers and corporate demand is located. Data security and privacy concerns represent a persistent barrier to deeper enterprise coworking adoption, as IT and information security executives at large corporations and regulated financial institutions are concerned about the shared network infrastructure, open physical environments, and multi-tenant building access control characteristics of standard coworking locations that create information security risk exposure inappropriate for functions handling sensitive client data, proprietary intellectual property, or regulatory-sensitive information.

Opportunities: Managed workspace enterprise agreement growth, tier-2 and tier-3 city expansion across emerging markets, and specialist industry-specific coworking format development

The enterprise managed workspace opportunity represents the single largest untapped commercial growth vector in the coworking market, as the progressive shift of large corporate real estate strategies toward outcome-based flexible workspace procurement is creating demand for operator-managed private workspace solutions delivered within shared building infrastructure that provide enterprise-grade security, customization, and service quality at flexible commercial terms, a product category that the most operationally sophisticated coworking operators are positioned to deliver but whose penetration of the total global enterprise office footprint remains a small fraction of its addressable potential. Life sciences and laboratory coworking represents a particularly high-value specialist format opportunity, as the June 2025 IWG and Smart Labs partnership to deliver fully managed laboratory coworking environments demonstrates commercial validation of a model that addresses the extraordinary capital and operational cost barriers that prevent early-stage biotech companies and independent researchers from accessing wet lab infrastructure on economically viable terms.

Recent Developments:

-

2025: CBRE Group completed its acquisition of Industrious National Management Company, creating a new Building Operations & Experience business segment that positions CBRE as both the world’s largest commercial real estate services firm and a major operator of flexible workspace solutions, signaling the permanent integration of coworking into mainstream institutional commercial real estate strategy.

-

2025: IWG plc expanded its coworking presence in Latin America through the launch of Regus coworking suites in shopping mall locations across Belo Horizonte, Florianopolis, and Rio de Janeiro, extending flexible workspace accessibility to professional populations in non-traditional commercial districts and high-traffic retail environments that increase workspace visibility and spontaneous membership conversion.

-

2025: IWG and SmartLabs announced a 10-year global partnership to deliver fully managed laboratory coworking environments in emerging and established life sciences hubs, addressing the demand from biotech startups and independent researchers for flexible access to wet lab infrastructure that individual organizations cannot afford to establish and manage independently.

-

2024: WeWork launched its Coworking Partner Network, an affiliate programme of third-party workspace locations that broadens its North American member workspace access options without requiring direct capital investment in new locations, expanding the effective geographic coverage of WeWork membership for enterprise and individual members seeking workspace access across markets where WeWork does not operate its own facilities.

-

2024: Industrious expanded its coworking space portfolio with AI-driven personalization features, IoT environmental connectivity, and biophilic nature-focused design elements that enhance member wellbeing, engagement, and workspace experience quality in response to growing enterprise client demand for premium managed workspace environments that support employee health and productivity objectives.

Coworking Spaces Market Key Players

-

IWG plc (Regus, Spaces, HQ, Signature)

-

WeWork

-

Industrious (CBRE)

-

Impact Hub

-

Awfis Space Solutions

-

Ucommune

-

The Executive Centre

-

Servcorp

-

Mindspace

-

Knotel (Newmark)

-

Serendipity Labs

-

Kr Space

-

SOHO 3Q

-

CommonGrounds

-

Techspace

-

Green Desk

-

Convene

-

The Hive

-

Workbar

-

Smartworks

Coworking Spaces Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.96 Billion |

| Market Size by 2035 | USD 81.64 Billion |

| CAGR | CAGR of 13.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Corporate/Professional, Open/Conventional, Industry-Specific, Others) • By Nature (Managed, Independent, Hybrid) • By Application (SMEs, Large Enterprises, Freelancers, Others) • By Industry Vertical (BFSI, Information Technology, Healthcare, Legal & Consulting, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IWG plc (Regus, Spaces, HQ, Signature), WeWork, Industrious (CBRE), Impact Hub, Awfis Space Solutions, Ucommune, The Executive Centre, Servcorp, Mindspace, Knotel (Newmark), Serendipity Labs, Kr Space, SOHO 3Q, CommonGrounds, Techspace, Green Desk, Convene, The Hive, Workbar, and Smartworks. |

Frequently Asked Questions

Ans: North America dominated the Coworking Spaces Market in 2025, with the United States as the leading national market within the region.

Ans: SMEs dominated with approximately 29.50% revenue share in 2025.

Ans: The irreversible normalization of hybrid work models across corporate enterprises globally driving structural demand for flexible workspace alternatives to fixed long-term office leases, combined with the extraordinary expansion of the global freelance and independent professional workforce and the maturation of coworking operator enterprise service capabilities to meet corporate security, compliance, and customization requirements.

Ans: The Coworking Spaces Market was valued at USD 20.96 Billion in 2025.

Ans: The Coworking Spaces Market is expected to grow at a CAGR of 13.68% from 2026 to 2035.

Get in Touch