Cyber Crisis Management Market Report Scope & Overview:

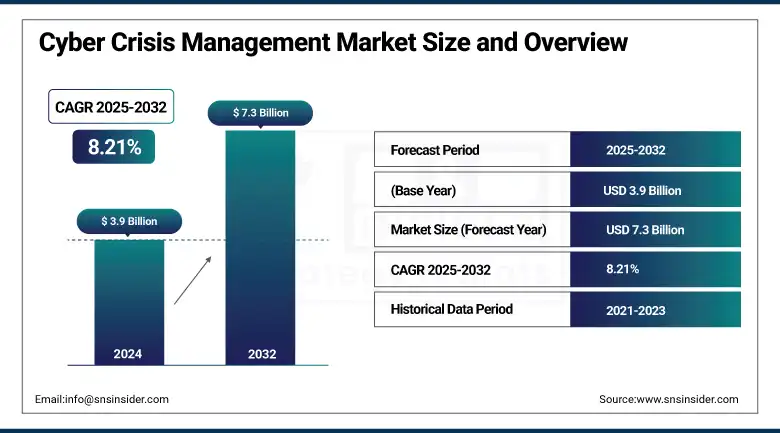

The cyber crisis management market size was valued at USD 3.9 billion in 2024 and is expected to reach USD 7.3 billion by 2032, growing at a CAGR of 8.21% during 2025-2032.

The cyber crisis management market growth is driven by the rise in the number of cyberattacks in every industry globally. Due to increased risk and regulatory pressure, organizations are moving quickly to embrace advanced technology and services to bolster their cybersecurity backbone. The increased attention on security is also a response to safeguarding sensitive information, ensuring business continuity, and enhancing stakeholder confidence amid a shifting digital landscape. Artificial intelligence and machine learning have become a key driver of growth due to the increasing efficiency in cyber crisis management systems through rapid threat detection and automated incident responses. Also, the increased use of cloud-based platforms offers centralized and scalable solutions to manage security operations. There is also increased demand for industry-focused cybersecurity solutions, especially in verticals with high stakes and high-profile attacks such as healthcare, finance, and critical infrastructure.

To Get more information On Cyber Crisis Management Market - Request Free Sample Report

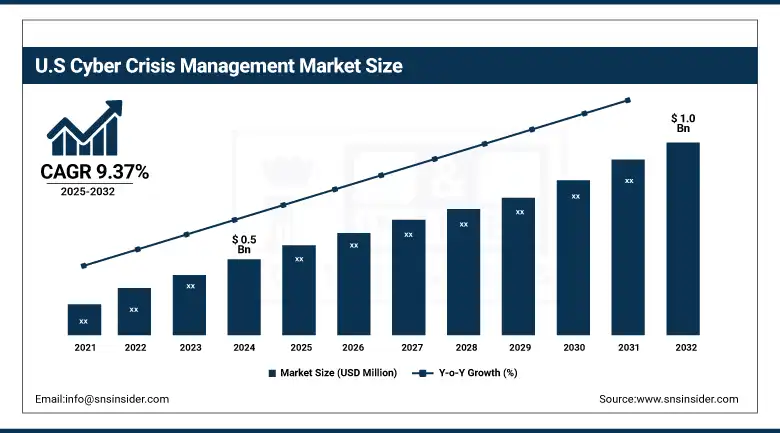

The U.S. cyber crisis management market is witnessing substantial growth, fueled by the rising frequency and complexity of cyber threats. Valued at approximately USD 0.5 billion in 2024, the market is expected to grow to around USD 1.0 billion by 2032, with a compound annual growth rate of 9.37% over 2024-2032. The increase in ransomware attacks, rigorous data protection regulations, and the growing prevalence of digital technologies in various industries contribute to the market growth. With the rise of ever-changing cyber threats, companies are now prioritizing investments towards futuristic cyber crisis management solutions to protect mission-critical data, maintain business continuity & build robust customer trust.

Cyber Crisis Management Market Dynamics:

Drivers:

-

Rising Cyberattacks Increase the Need for Advanced Cyber Crisis Management Solutions to Reduce Financial and Operational Damage

Rising occurrences of cyber-related attacks, such as ransomware and data breaches, are immensely responsible for driving the demand for effective cyber crisis management solutions. With cyber threats ever-evolving, organizations are realizing the need to identify, respond to, and recover from an attack as quickly as possible. Information cyber incidents, including data breaches, can inflict massive financial, reputational, and operational losses, leading companies to purchase a crisis management system. From the increased threat of cyberattacks, it has become a business imperative for organizations across the board to ensure their capabilities for rapid response and recovery, thereby minimizing the impact on business operations and brand equity.

For instance, in 2024, the U.K.'s Met Office and five other government agencies collectively thwarted 15 million cyberattacks, averaging around 40,000 threats daily.

Restraints:

-

High Implementation Costs Limit Adoption, Particularly for Smaller Businesses, Leaving Them Vulnerable to Cyber Threats.

One of the major restraints in the adoption of cyber crisis management solutions is the high cost involved in their implementation. Advanced security technologies need huge upfront capital to invest in technologies, such as IT incident response, threat detection software, disaster recovery tools, and others, and they need continuous maintenance and upgrading. The cost associated with this typically discourages smaller businesses or even larger businesses with limited cybersecurity budgets from deploying full solutions. Though the demand for these systems has soared following a rising wave of cyber threats, cost remains a significant barrier. Moreover, the financial burden is exacerbated by the time it takes to tailor these systems to meet the specific needs of an organization.

According to a study, approximately 47% of small businesses with fewer than 50 employees lack a dedicated cybersecurity budget, and 58% allocate less than USD 5,000 annually to cybersecurity measures.

Opportunities:

-

AI and ML Enhance Real-Time Threat Detection and Response, Improving the Efficiency of Cyber Crisis Management

Artificial Intelligence and Machine Learning Market is one of the most lucrative and growing fields for the cyber crisis management market. These technologies improve detection and response time to these information technology threats and increase the ease of incident response to these events. All the data related to computer networks, software vulnerability, potential security breaches, and other, can be analyzed by this type of technology, which helps in quicker decision making and minimizing the human error factor than the traditional way of analysis. As the data from cyberattacks and cyber threats is massive and complex, the use of automation will help organisations react proactively with higher precision to the growing number of cyber threats and security attacks. This is an area where AI-based security needs are increasing, and also enabling greater development.

For instance, implementing AI in cybersecurity has led to a 95% reduction in false positives, streamlining alert management, and enabling quicker responses to actual threats.

Challenges:

-

Global Shortage of Cybersecurity Professionals Limits Organizations' Ability to Deploy and Manage Effective Crisis Management Systems

However, due to the cybersecurity talent shortage, it is one of the biggest challenges in deploying and operationalizing cyber crisis management solutions. As organizations need more skilled professionals, by 2023, the global shortage of cybersecurity specialists climb to 3.4 million.

There is a shortage of these people, which has resulted in the inability of organizations to effectively capitalize on their cyber crisis management systems as the technologies require trained people to manage and operate them. The absence of professional specialists further hinders the creation of customized alternatives and raises the risk of flaws in cybersecurity approaches that hinder the protection of sensitive data and the maintenance of operational resilience once evolving cyber threats appear.

Cyber Crisis Management Market Segmentation Analysis:

By Type

The on-premise segment dominated the market and accounted for 69% of the cyber crisis management market share, as large enterprises and government agencies were keen to adopt this type of deployment, has witnessed high demand among end-users that need maximum control, compliance, and low-latency response. Such type of organizations often work in tightly regulated environments where data sovereignty and an internal threat posture are paramount. On-premise solutions enable greater customization, projects ensure better integration with legacy systems, and usage is more suitable for complex IT infrastructures.

The cloud-based segment is anticipated to grow at the fastest CAGR during the forecast period, owing to the increasing remote work culture, the need for scalable security, and the cost-effective adoption models. Businesses are migrating to cloud-native security platforms that deliver real-time threat telemetry and automated remediation with minimal on-prem deployment. With their flexibility, rapid updates, and centralised control, cloud-based solutions fit perfectly into modern IT environments.

In 2024, Australia has committed USD1.3 billion over the next decade to develop a top-secret cloud infrastructure in collaboration with Amazon Web Services. This initiative aims to enhance intelligence sharing, improve cybersecurity resilience, and support military operations.

By Application

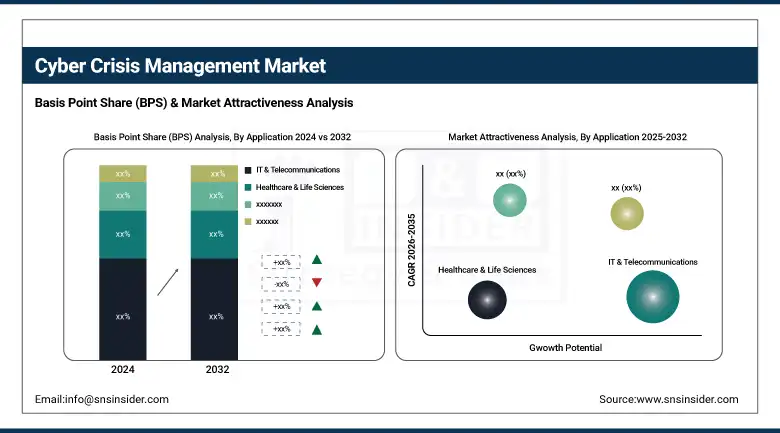

In 2024, the IT & telecommunications segment dominated the market and accounted for 29% of revenue share, since IT & telecommunications is highly vulnerable to cyberattacks as it is one of the most critical parts of digital infrastructure. Telecom providers and IT firms have become critical for the modern economy, but frequent data breaches, network disruptions, and DDoS attacks have caused these firms to adopt robust crisis response strategies. 5G networks, cloud computing, and IoT ecosystems deepen the risk environment, and firms are spending billions on offensive programs. As a result, the IT & telecom segment remains the leading segment during the forecast period.

By Vertical

The government & financial institutions segment dominated the cyber crisis management market and accounted for a significant revenue share in 2024, as the need for parry national security and financial data are quite a crucial business activity. The sectors are also under continuous Mongolian Ark cyber threats, fraud, and data breaches by state-supported cyber pirates. Consequently, they pour a great deal of resources into proactive cybersecurity frameworks, crisis response protocols, and regulatory compliance.

The healthcare & life sciences segment is expected to grow rapidly at a CAGR during 2025-2032, due to the soaring number of ransomware attacks on hospitals, clinics, and research centres. The digitization of patient records, the expansion of telemedicine, and the advent of medical devices powered by the internet of things have increased the attack surface. Furthermore, the nature of medical data itself and rigorous frameworks such as HIPAA necessitate healthcare leaders to implement strong and effective cyber crisis management.

Regional Analysis:

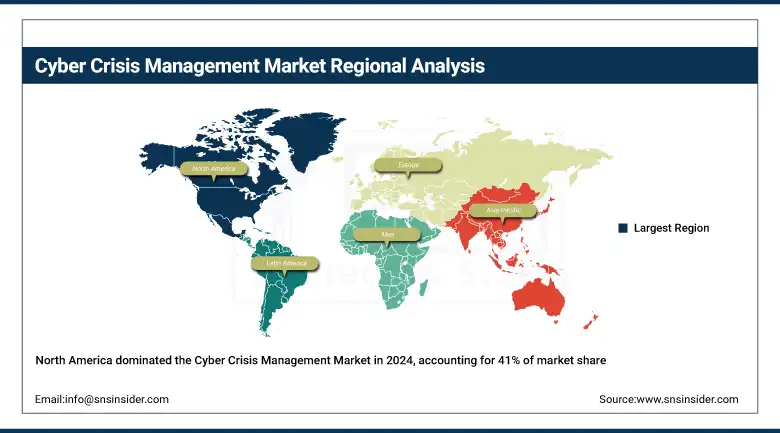

In 2024, North America dominated the market and accounted for 41% of revenue share, owing to advanced digital infrastructure, high internet penetration, and an increasing number of sophisticated cyberattacks against critical infrastructure sectors such as finance, health care, and government. With the heavy presence of leading cybersecurity firms and regulators, organizations have no option but to adopt an overall cyber crisis management approach framework, such as CCPA, and HIPAA, among others.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is expected to register the fastest CAGR during 2025-2032 due to the high digital transformation, rising cloud adoption, and increase in mobile and IoT dependence in this region. Across all sectors, cyberattacks are rising manyfold in countries, such as China, India, and Japan, especially in finance, health, and manufacturing. A. An unequal investment landscape. The relatively low level of cyber preparedness in some emerging economies has intensified the investments in robust cyber crisis management solutions.

Singapore is investing USD 38.5 million in the Cybersecurity Talent, Innovation, and Growth (Cyber TIG) Plan over the next three years to develop its cybersecurity workforce and promote innovation in the sector.

In the Asia Pacific region, China dominated the market due to the size of the digital ecosystem, the volume of data growth, and the rising frequency of cyber threats against critical infrastructure, government, and financial institutions, another driving factor is the stringent cybersecurity laws in the country including the Cybersecurity Law of China and the Data Security Law, the enterprises here have started to spend heavily on crisis response systems as well.

The cyber crisis management market in Europe is fueled by the compliance needs of strict general data protection regulations brought on by recent cyberattacks on critical infrastructure and the digitally fragile pace of change ongoing in many enterprises today. Organizations across verticals are adopting compliance-centred, AI-driven cybersecurity solutions, which would keep growing steady until 2032.

Germany dominated the market in Europe, owing to its stronghold in crypto, the presence of major manufacturers, stringent defense mandates, and spending on new technology arrival expectations in the field of cybersecurity, advanced new-age technologies based in space.

In 2024, together with more than 60 technology companies such as Lenovo, ZTE Dawning Information Industry, Qi-Anxin rolled out a large language model specifically for cybersecurity. The model seeks to proactively identify and assess cyber threats, enhancing real-time responsiveness within sectors.

Key Players:

The major cyber crisis management market companies are IBM, Cisco, Palo Alto Networks, Accenture, FireEye, CrowdStrike, BAE Systems, Deloitte, Kroll, Booz Allen Hamilton, and others.

Recent Developments:

-

In October 2024, Palo Alto Networks launched enhanced capabilities in its Operational Technology Security solution, including AI-powered, risk-based virtual patching. These upgrades aim to protect remote OT operations and critical assets in industrial environments.

-

In October 2024, Booz Allen participated in Singapore International Cyber Week, discussing cybersecurity best practices and challenges. The event focused on building trust and security in the evolving digital landscape.

-

In July 2024, CrowdStrike announced new safety measures to prevent IT outages caused by faulty software updates. The company will enhance testing and use a staggered deployment strategy to reduce risk. CEO George Kurtz will testify before the US Congress on a major IT outage incident.

|

Report Attributes |

Details |

|

Market Size in 2024 |

US$ 3.9 Billion |

|

Market Size by 2032 |

US$ 7.32 Billion |

|

CAGR |

CAGR of 8.21 % From 2024 to 2032 |

|

Base Year |

2024 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2021-2023 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Type (Cloud-Based, On-Premise) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

|

Company Profiles |

IBM, Cisco, Palo Alto Networks, Accenture, FireEye, CrowdStrike, BAE Systems, Deloitte, Kroll, Booz Allen Hamilton and others in report |

Frequently Asked Questions

The global shortage of cybersecurity professionals limits organizations' ability to deploy and manage effective crisis management systems.

Rising cyberattacks increase the need for advanced cyber crisis management solutions to reduce financial and operational damage.

Asia-Pacific is expected to register the fastest CAGR during the forecast period.

The CAGR of the Cyber Crisis Management Market during the forecast period is 8.21% from 2025-2032.

The cyber crisis management market size was valued at USD 3.9 billion in 2024 and is expected to reach USD 7.3 billion by 2032

Get in Touch