Cyber-Physical Systems Market Report Scope & Overview:

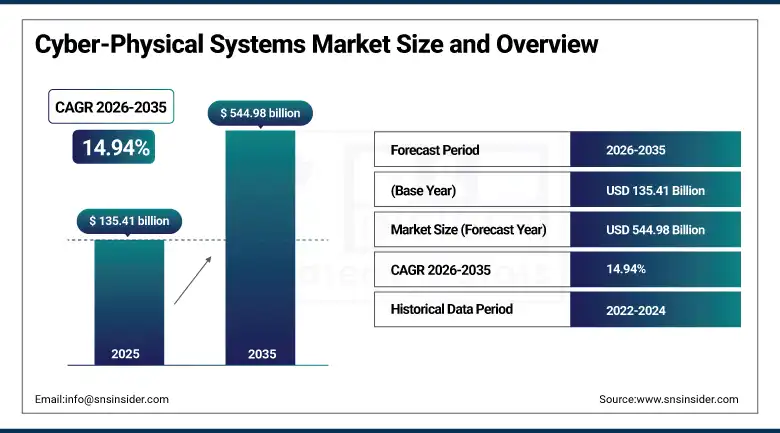

The cyber-physical systems market was valued at USD 135.41 billion in 2025 and is expected to reach USD 544.98 billion by 2035, growing at a CAGR of 14.94% from 2026–2035.

The cyber-physical systems (cps) market represents one of the most foundational technology categories enabling the Fourth Industrial Revolution, as the systematic integration of computational algorithms, network connectivity, and physical world sensing and actuation is transforming how manufacturing plants, transportation networks, healthcare systems, power grids, and urban infrastructure are designed, operated, monitored, and optimized. cyber-physical systems unite the digital and physical worlds through embedded sensors that continuously measure physical system states, computational algorithms that process sensor data in real time, network connectivity enabling distributed system coordination, and actuators that translate computational decisions into physical world actions, creating a closed-loop system of unprecedented intelligence and responsiveness that enables automation, optimization, and autonomous operation at scales and speeds impossible through purely human supervision. The market encompasses the full CPS technology ecosystem including embedded security systems protecting connected physical devices, industrial control system security for manufacturing and utility infrastructure, robotic systems with integrated sensing and computational autonomy, and IoT security frameworks protecting the billions of connected devices that form the sensing layer of CPS deployments across smart factories, connected vehicles, intelligent buildings, and smart city infrastructure.

where the competitive advantages of real-time operational intelligence, predictive maintenance, remote monitoring, and AI-optimized control create compelling economic cases for CPS investment that progressive cost reduction in sensor, connectivity, and edge computing technology is making commercially accessible across progressively smaller and more cost-sensitive application environments. The National Science Foundation's recognition of CPS as one of the top 12 economically disruptive technologies by 2025 confirms institutional validation of the market's structural importance.

Market Size and Forecast

- Market Size in 2026E: USD 155.64 Billion

- Market Size by 2035: USD 544.98 Billion

- CAGR (2026-2035): 14.94%

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information On Cyber-Physical Systems Market - Request Free Sample Report

Cyber-Physical Systems Market Trends

- Accelerating integration of AI and ML in CPS enables edge AI inference at device level, reducing cloud dependency and supporting millisecond-level response for industrial automation, autonomous vehicles, and medical systems.

- Growing 5G deployment in CPS provides ultra-low latency, massive device connectivity, and network slicing for reliable industrial communication beyond WiFi and 4G capabilities.

- Rising adoption of digital twins enables real-time virtual modelling of physical systems for predictive maintenance, simulation, and operational optimization.

- Expanding autonomous vehicle CPS integrates vehicle-to-infrastructure communication for traffic optimization, collision avoidance, and real-time hazard sharing.

- Increasing healthcare CPS applications support continuous patient monitoring, robotic surgery, and AI-driven real-time control of medical devices.

The U.S. Cyber-Physical Systems Market Size Outlook

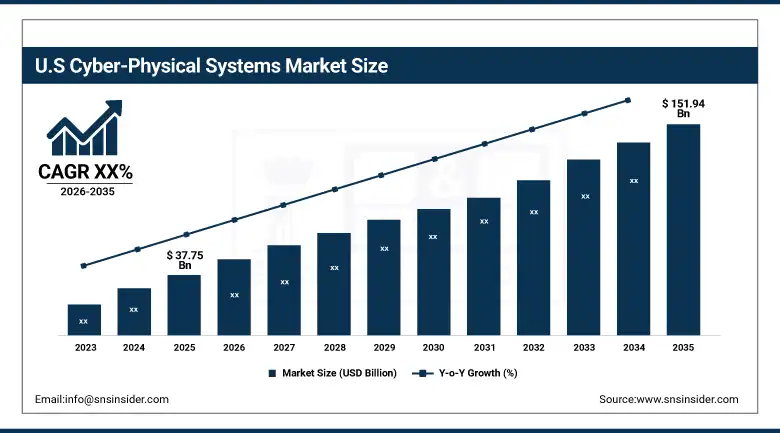

The U.S. Cyber-Physical Systems Market was valued at approximately USD 37.75 billion in 2025 and is expected to reach approximately USD 151.94 billion by 2035, driven by industrial automation investment, CHIPS Act semiconductor manufacturing, and autonomous vehicle technology development.

The United States dominates the global cyber-physical systems market through its position as the world's most advanced industrial automation economy, the headquarters of leading CPS technology companies including Siemens, Honeywell, Rockwell Automation, and General Electric, and the largest autonomous vehicle technology development ecosystem anchored by Tesla, Waymo, Cruise, and hundreds of CPS-dependent startup companies. U.S. federal investment in CPS through NSF's Cyber-Physical Systems research programme, DARPA's autonomous systems programmes, and the Advanced Manufacturing National Program Office sustains the research frontier that drives commercial CPS technology development. The CHIPS Act's domestic semiconductor manufacturing investment is creating new CPS-intensive chip fabrication facilities that require sophisticated automated material handling, precision process control, and real-time quality monitoring systems that represent premium CPS deployments.

The National Science Foundation's classification of CPS as one of the top 12 economically disruptive technologies by 2025, combined with its foundational role in enabling smart homes, IoT, connected healthcare, and autonomous vehicles, confirms that CPS is not a single technology category but an enabling infrastructure for an extraordinary range of technology megatrends simultaneously accelerating market demand.

Cyber-Physical Systems Market Segment Analysis

- By Security Type, ICS Security dominated with the largest market share in 2025 through extensive industrial control system security investments across manufacturing, energy, and utility CPS deployments; IoT Security is the fastest-growing segment driven by rapid expansion of connected devices across smart homes, healthcare, transportation, and industrial IoT ecosystems.

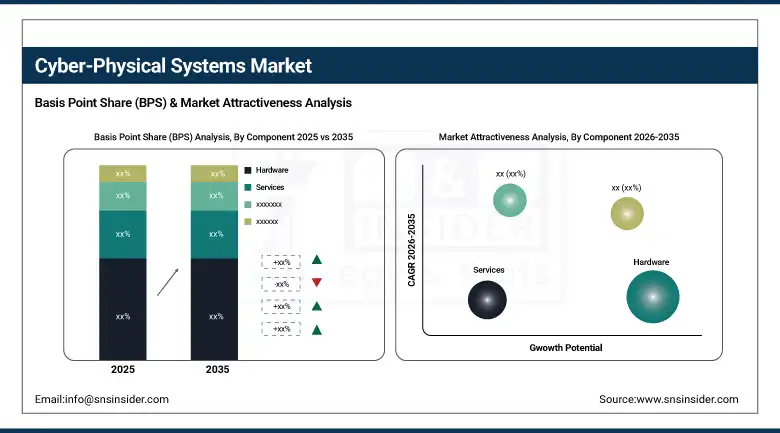

- By Component, Hardware dominated with approximately 49% of revenues in 2025 due to the essential role of sensors, actuators, and embedded systems in CPS infrastructure; Services is the fastest-growing component through rising demand for consulting, system integration, cybersecurity, and managed services for complex CPS deployments.

- By Application, Manufacturing and Industrial Automation dominated as the largest and most mature application segment through widespread smart factory, robotics, and industrial IoT adoption; Transportation and Automotive is projected to grow at the highest CAGR through increasing investments in autonomous vehicles and smart transportation infrastructure.

By Security Type, ICS security dominates the cyber-physical systems market, iot security is expected to grow fastest

ICS Security held the largest market share in 2025 due to strong demand for protecting industrial control systems across manufacturing, energy, and utility infrastructure, where operational continuity and safety are critical. Enterprises continue to invest heavily in securing SCADA, PLCs, and other OT systems against rising cyber threats and ransomware attacks targeting critical infrastructure.

IoT Security is expected to grow at the fastest pace through 2035, driven by the rapid expansion of connected devices across smart homes, healthcare, transportation, and industrial IoT environments. Increasing device interconnectivity is pushing demand for advanced security solutions such as AI-based threat detection, encryption, and zero-trust frameworks to protect highly distributed CPS networks.

By Component, hardware dominates the cyber-physical systems market, services is expected grows fastest

Hardware retained the dominant component position with approximately 49% of the cyber-physical systems market in 2025, reflecting the foundational necessity of physical hardware including sensors, actuators, embedded processors, communication modules, and power systems that constitute the physical enabling layer of every CPS deployment. The extraordinary diversity of CPS hardware requirements across different application environments, from miniaturized medical implant sensors through industrial vibration sensors for rotating machinery predictive maintenance to automotive radar and LiDAR systems for autonomous vehicle perception, creates a large and heterogeneous hardware market encompassing the full range of semiconductor, electromechanical, and connectivity component categories. Semiconductor advances in microcontroller, sensor, and RF component miniaturization and power efficiency are progressively reducing CPS hardware cost per function, expanding the commercial viability of CPS deployment across progressively cost-sensitive application environments.

Services is the fastest-growing CPS component at the highest CAGR through 2035, driven by the increasing complexity of CPS deployments that requires expert consulting, system integration, cybersecurity, and ongoing managed services that most end-user organizations cannot provide in-house at the depth and currency of expertise required for optimal CPS performance, security, and reliability. CPS system integration service requirements are particularly demanding because of the multi-vendor hardware ecosystem, real-time software requirements, safety certification obligations, and cybersecurity hardening that must be coordinated across the full system architecture.

By Application, manufacturing dominates the cyber-physical systems market, transportation is expected grows fastest

Manufacturing and Industrial Automation retained the dominant application position in the cyber-physical systems market, reflecting decades of smart manufacturing investment through programmable logic controllers, distributed control systems, SCADA systems, and industrial robotics that collectively constitute the world's most mature and extensively deployed CPS infrastructure. The industry 4.0 digital transformation programme is accelerating the upgrade of legacy manufacturing CPS infrastructure with next-generation networked sensors, edge AI, digital twin systems, and cloud-connected manufacturing execution systems that create comprehensive cyber-physical integration across the entire production process from raw material intake through finished goods shipping. Manufacturing CPS deployments in automotive, aerospace, semiconductor, pharmaceutical, and food processing industries represent the highest-value and most extensively validated CPS application category.

Transportation and Automotive is projected to grow at the fastest application CAGR through 2035, driven by the autonomous vehicle technology development that represents the most technically ambitious and commercially consequential CPS deployment in history, where the integration of radar, LiDAR, camera, ultrasound, and GPS sensors with AI decision-making algorithms and vehicle actuation systems enables safe, reliable vehicle navigation without human driver supervision. Beyond autonomous vehicles, smart transportation infrastructure CPS including intelligent traffic management, connected intersection systems, dynamic toll pricing, and railway positive train control are being deployed across developed and emerging market urban centers as governments invest in reducing traffic congestion, improving road safety, and enabling more efficient public transportation networks.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

82% |

|

Europe |

Germany |

32% |

|

Asia Pacific |

China |

46% |

|

Middle East & Africa |

UAE |

27% |

|

Latin America |

Brazil |

43% |

North America Cyber-Physical Systems Market Insights

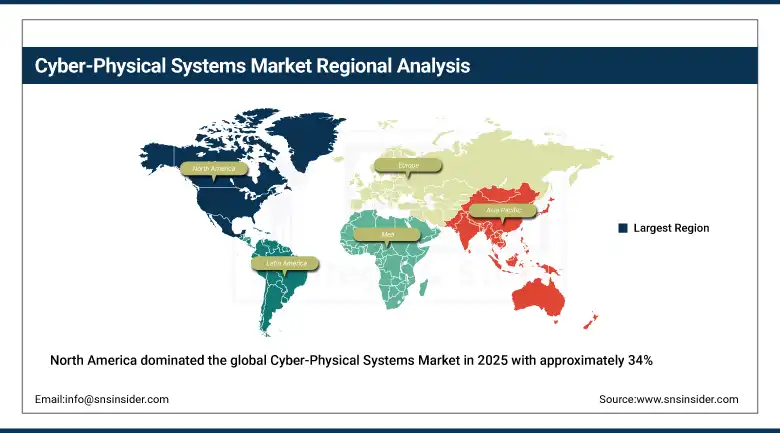

North America dominated the global Cyber-Physical Systems Market in 2025 with approximately 34% of revenues, led by the United States at approximately 82% of North American revenues. U.S. market leadership is driven by the world's most advanced industrial automation ecosystem, the headquarters of leading CPS technology companies, NSF's CPS research programme, and the most active autonomous vehicle technology development environment globally. The CHIPS Act's semiconductor manufacturing investment is creating new premium CPS demand in domestic chip fabrication facilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Cyber-Physical Systems Market Insights

Asia Pacific is the fastest-growing regional CPS market, driven by China's extraordinary industrial automation investment under the Made in China 2025 initiative creating the world's largest smart manufacturing CPS deployment programme, Japan's advanced robotics and automotive manufacturing industries, South Korea's semiconductor and electronics manufacturing automation, and India's rapidly expanding industrial sector adopting CPS for productivity and quality improvement. The region's 5G infrastructure deployment provides the connectivity foundation that accelerates CPS deployment across smart cities, industrial automation, and transportation applications.

Europe Cyber-Physical Systems Market Insights

Europe is a technically sophisticated CPS market anchored by Germany's world-leading manufacturing automation and automotive technology industries, combined with the UK's aerospace and financial technology CPS investment, France's transportation infrastructure CPS, and the Nordic countries' smart grid and wind energy CPS deployment. Siemens' Xcelerator digital enterprise platform and Bosch's industrial IoT ecosystem represent European-headquartered CPS technology platforms that serve global markets from their European development centers.

Latin America and MEA Cyber-Physical Systems Market Insights

Latin America and MEA are growing CPS markets driven by industrial sector modernization and smart infrastructure investment. Brazil leads Latin American CPS adoption through its automotive manufacturing, agribusiness automation, and energy sector CPS deployments. MEA investment is driven by UAE and Saudi Arabia's smart city programmes including NEOM and Dubai's autonomous transportation investment, combined with the region's energy sector CPS investment in smart oil field and renewable energy monitoring applications.

Market Dynamics

Growth Drivers: Industry 4.0 smart manufacturing imperative and autonomous vehicle technology development creating the largest parallel CPS demand waves in the market's history

The primary structural growth drivers for the cyber-physical systems market are the global Industry 4.0 transformation of manufacturing that is systematically deploying CPS infrastructure across production facilities worldwide as the primary mechanism for achieving the operational efficiency, quality improvement, and predictive maintenance capability that competitive manufacturing requires, combined with the autonomous vehicle technology development that represents the most ambitious and highest-value CPS deployment project in history, where the successful commercialization of truly self-driving vehicles would create CPS deployment at billion-unit scale across the global vehicle fleet.

The NSF's recognition of CPS as one of the top 12 economically disruptive technologies by 2025 and its foundational enabling role for smart homes, IoT, connected healthcare, and connected vehicles confirms that CPS is not simply one technology market but the enabling infrastructure layer for an extraordinary range of 21st century technology transformation programmes.

Restraints: Cybersecurity vulnerability of connected physical systems with severe consequence risk, complex safety certification requirements for safety-critical CPS, and interoperability challenges across heterogeneous CPS component ecosystems

A significant restraint on the cyber-physical systems market is the fundamental cybersecurity vulnerability of connected physical systems where successful cyber-attacks can trigger catastrophic physical consequences including industrial accidents, vehicle crashes, power outages, and medical device failures that dwarf the financial consequences of conventional data breach events. The complexity of safety certification for safety-critical CPS applications including autonomous vehicles, medical devices, aircraft avionics, and nuclear plant control systems creates development timelines and certification costs that significantly extend commercialization pathways and require regulatory expertise that many CPS developers lack. Interoperability challenges across the fragmented CPS hardware and software ecosystem, where proprietary protocols, vendor-specific APIs, and incompatible data formats create integration barriers that add cost and complexity to multi-vendor CPS system deployments, limit the full commercial potential of connected CPS infrastructure.

Opportunities: Autonomous vehicle CPS commercial deployment, healthcare CPS for remote patient monitoring, and smart city infrastructure CPS integration

The autonomous vehicle commercial deployment represents the single most transformative market development opportunity in the CPS ecosystem, where the successful certification and scaling of self-driving vehicle systems would create a multi-trillion-dollar CPS deployment demand across the global vehicle fleet that would dwarf all other CPS application markets combined. Healthcare CPS for continuous remote patient monitoring, smart prosthetics, robotic surgical systems, and AI-powered drug delivery represents a premium, high-growth market where CPS capability directly improves patient outcomes and healthcare system efficiency in ways that command premium pricing from healthcare systems and reimbursement frameworks. Smart city infrastructure CPS integration, connecting transportation, energy, water, waste, and public safety systems within unified real-time monitoring and management platforms, represents the most ambitious and potentially most commercially significant municipal technology investment programme of the 21st century.

Recent Developments:

-

2025: Siemens advanced its Xcelerator digital enterprise platform with enhanced AI and digital twin capabilities for industrial CPS deployments, enabling manufacturers to create comprehensive virtual replicas of production systems for optimization and predictive maintenance without physical system intervention.

-

2025: Honeywell expanded its industrial CPS portfolio with new connected sensor solutions and process control systems for energy and utility applications, integrating AI-powered anomaly detection that identifies process control deviations before they develop into production or safety incidents.

-

2025: NVIDIA advanced its DRIVE platform for autonomous vehicle CPS, with new hardware and software solutions enabling automotive OEMs to deploy increasingly capable autonomous driving features while managing the computational complexity of multi-sensor fusion at the real-time speeds that safe autonomous operation requires.

-

2025: Rockwell Automation expanded its FactoryTalk Analytics platform with enhanced edge AI capabilities for manufacturing CPS, enabling real-time quality inspection, predictive maintenance, and production optimization through AI-powered sensor data analysis at the machine level.

-

2025: Bosch continued expanding its connected mobility and industrial IoT CPS ecosystem, with new vehicle-to-everything communication modules and industrial sensor networks providing the connectivity infrastructure for next-generation automotive and smart factory CPS deployments.

Cyber-Physical Systems Market Key Players are:

-

Siemens AG

-

Honeywell International Inc.

-

Rockwell Automation Inc.

-

General Electric Company (GE Digital)

-

ABB Ltd.

-

Cisco Systems Inc.

-

IBM Corporation

-

Microsoft Corporation

-

Robert Bosch GmbH

-

NVIDIA Corporation

-

Intel Corporation

-

Schneider Electric SE

-

Emerson Electric Co.

-

Texas Instruments Inc.

-

Qualcomm Technologies Inc.

-

National Instruments Corporation (NI)

-

Yokogawa Electric Corporation

-

Mitsubishi Electric Corporation

-

Hitachi Ltd.

-

PTC Inc.

Cyber-Physical Systems Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 135.41 Billion |

| Market Size by 2035 | USD 544.98 Billion |

| CAGR | CAGR of 14.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Security Type (Embedded Security, ICS Security, Robotic Security, IoT Security) • By Component (Hardware, Software, Services) • By Application (Manufacturing and Industrial Automation, Transportation and Automotive, Healthcare, Energy and Utilities, Aerospace and Defense, Consumer Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens AG, Honeywell International Inc., Rockwell Automation Inc., General Electric Company (GE Digital), ABB Ltd., Cisco Systems Inc., IBM Corporation, Microsoft Corporation, Robert Bosch GmbH, NVIDIA Corporation, Intel Corporation, Schneider Electric SE, Emerson Electric Co., Texas Instruments Inc., Qualcomm Technologies Inc., National Instruments Corporation (NI), Yokogawa Electric Corporation, Mitsubishi Electric Corporation, Hitachi Ltd., PTC Inc. |

Frequently Asked Questions

North America dominated with approximately 34% of revenues in 2025, led by the United States at approximately 82%

Transportation and Automotive is projected to grow at the fastest application CAGR through 2035, driven by autonomous vehicle technology

Hardware dominated with approximately 49% of revenues in 2025 through the foundational necessity of physical sensors, actuators, embedded processors, communication modules

The global Industry 4.0 transformation of manufacturing systematically deploying CPS infrastructure across production facilities worldwide.

The Cyber-Physical Systems Market was valued at USD 135.41 billion in 2025.

The Cyber-Physical Systems Market is expected to grow at a CAGR of 14.94% from 2026 to 2035.

Get in Touch