Data Center Chip Market Report Scope & Overview:

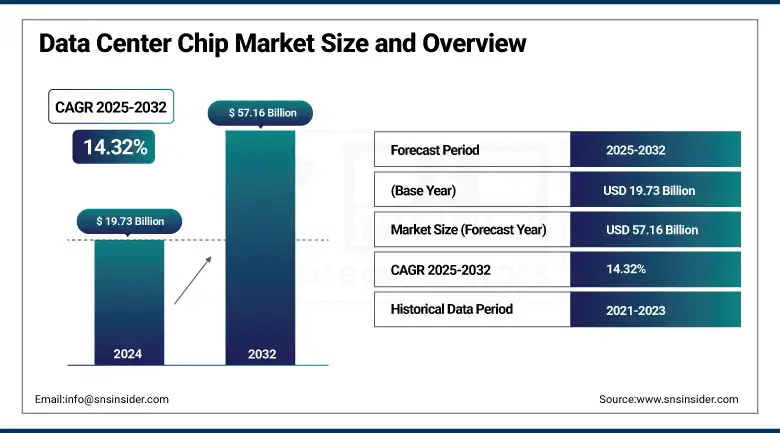

Data Center Chip Market was valued at USD 19.73 billion in 2024 and is expected to reach USD 57.16 billion by 2032, growing at a CAGR of 14.32% from 2025-2032.

The Data Center Chip Market is expanding fast due to skyrocketing demand for cloud computing, artificial intelligence, big data analytics, and edge computing. Rising data traffic, leading-edge chip technologies, and growth in hyperscale data centers drive further market growth, enabling digital transformation and high-performance computing demands globally.

To Get more information On Data Center Chip Market - Request Free Sample Report

In May 2024, AMD announced that 156 of the Top500 supercomputers are powered by its technology, marking a 29% year-over-year increase in high-performance computing (HPC) deployments.

Meanwhile, startup Crusoe secured $11.6 billion in funding to expand a major data center in Abilene, Texas, for OpenAI. This expansion will increase the facility from two to eight buildings, each housing up to 50,000 Nvidia Blackwell chips. The total investment for the project now stands at $15 billion, marking it as OpenAI's largest data center to date.

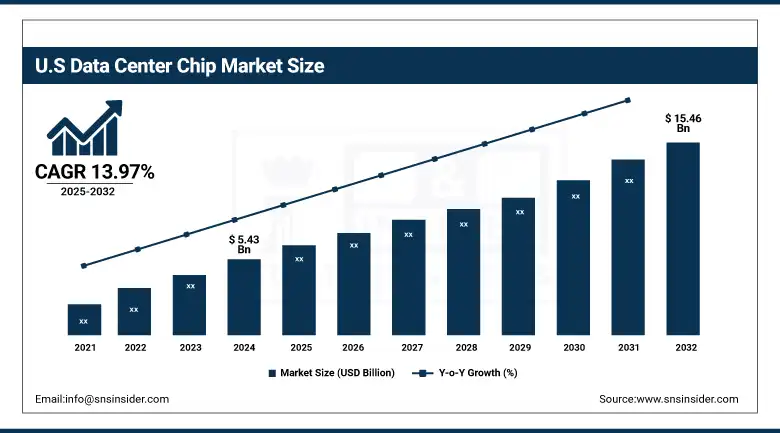

U.S. Data Center Chip Market was valued at USD 5.43 billion in 2024 and is expected to reach USD 15.46 billion by 2032, growing at a CAGR of 13.97% from 2025-2032.

The growth of the U.S. Data Center Chip Market is fueled by increasing cloud adoption, AI development, rising data processing requirements, and hyperscale data center expansion, driving up demand for energy-efficient, high-performance chips to support digital infrastructure.

Data centers in the U.S. consumed approximately 4.4% of the nation’s electricity in 2023, according to the U.S. Department of Energy. To support the accelerating demands of AI, the Department has identified 16 federal sites, including major national laboratories like Los Alamos and Oak Ridge, as potential locations for new data centers dedicated to AI development.

Data Center Chip Market Dynamics

Drivers

-

Growing cloud and AI workload demand drives high-performance chip adoption in hyperscale data centers worldwide.

The exponential expansion of cloud computing and AI use cases has fueled much greater demand for high-performance data center chips. Hyperscale operators and enterprises are making large-scale chip investments to accommodate more sophisticated workloads, ranging from machine learning algorithms to big data workloads. This need is driving chipmakers to innovate more rapidly, specifically in GPU, FPGA, and ASIC design. Furthermore, the growth of AI-based automation and real-time computing across industries such as healthcare, finance, and manufacturing is also enhancing the market growth path for energy-efficient, high-performance chips designed for next-generation cloud infrastructure.

Nvidia has announced a major strategic shift by opening its AI server platform to support chips from other manufacturers, including CPUs and AI accelerators. This move introduces NVLink Fusion, a new system allowing integration of third-party processors with Nvidia's technology.

Amazon Web Services (AWS) announced the development of a supercomputer named "Ultracluster" and a new server called "Ultraserver," both powered by its own AI chips, Trainium. The Ultracluster, to be located in the U.S., will be one of the largest in the world for training AI models and will be used by the AI startup Anthropic.

Restraints

-

Supply chain disruptions and semiconductor shortages postpone production schedules and affect the availability of chips in key data center markets.

Global semiconductor supply chains are still susceptible to geopolitical tensions, raw material shortages, and logistics disruptions that impact chip making cycles. The aftereffects of the COVID-19 pandemic, together with global trade restrictions, have revealed data center chip sourcing vulnerability. Data center constructors, as a result, experience procurement delays, increased costs, and reduced availability of critical components. These bottlenecks have a direct impact on deployment schedules and present strategic risks to hyperscalers and cloud service providers that count on uninterrupted chip supply in order to ensure uptime and performance.

Opportunities

-

Accelerated digital transformation in emerging markets drives demand for localised data centers with tailored chip architectures.

Emerging regions are experiencing growth in digital services, which is creating demand for localised data center infrastructure. This shift presents opportunities for chip companies to provide personalized, value-priced, and locality-optimized solutions. Governments' investments in digital public infrastructure and increasing adoption of the cloud by SMEs create demand for chips that are customized to address various climatic, regulatory, and power efficiency needs. Local collaboration and modular chip architectures can allow vendors to unlock untapped growth in previously underserved markets by global data center networks.

Brazil's clean energy infrastructure, with nearly 90% of electricity derived from renewable sources, positions it as an attractive destination for AI data centers. Meanwhile, China has invested approximately USD 6.1 billion in its "Eastern Data, Western Computing" project, aiming to build computing data centers in western regions to support eastern economic hubs. The initiative includes constructing eight major data center hubs, attracting over 200 billion yuan in total investment.

Challenges

-

Pursuing cybersecurity and data integrity using powerful chips creates new points of vulnerability in dynamic multi-tenant environments.

Adding more powerful chips to cloud and edge data centers adds increased risks of data leakage, side-channel attacks, and hardware-level exploits. With increasingly specialized and connected chips, protecting each layer of the architecture becomes a bigger challenge. Multi-tenant data centers have special problems in segregating workloads and keeping chip-level breaches out. The intricacy of secure firmware updates and trusted computing paths makes system design even more difficult. Enhancing hardware security while preserving performance is a critical, continuing challenge for both chipmakers and data center operators.

Data Center Chip Market Segment Analysis

By End-use

The IT & Telecom segment dominated the Data Center Chip Market with the highest revenue share of about 32% in 2024 due to massive investments in digital infrastructure, cloud-based services, and 5G deployments. Telecom operators and IT giants rely heavily on high-performance chips to power data-intensive applications, virtualization, and large-scale data storage. The rising demand for real-time processing and network optimization has made chips an essential backbone for IT and telecom operations, particularly as edge computing and AI integration continue expanding across this sector.

The Healthcare segment is expected to grow at the fastest CAGR of about 16.10% from 2025 to 2032, driven by the rapid adoption of AI-enabled diagnostics, telemedicine, and electronic health records. Healthcare providers are investing in powerful data center infrastructure to manage growing volumes of patient data, predictive analytics, and personalized medicine. Additionally, the integration of wearable health technologies and genomics research is generating vast data sets, necessitating high-efficiency chips that can handle sensitive, complex workloads in secure and regulated environments.

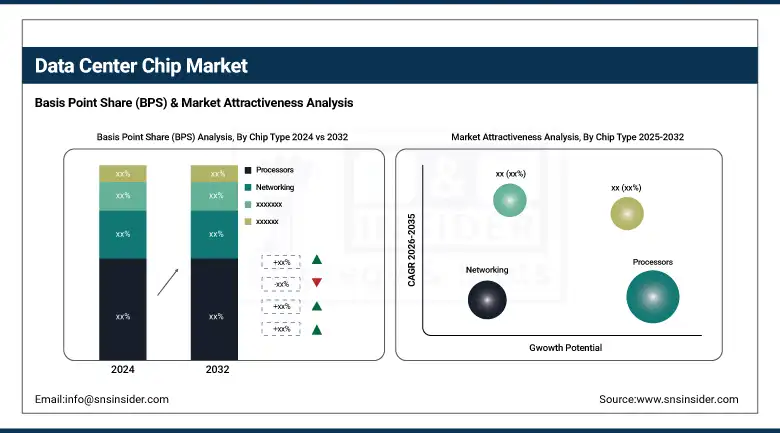

By Chip Type

The Processors segment dominated the Data Center Chip Market with the highest revenue share of about 48% in 2024 due to its central role in managing computational loads across servers. Processors are the foundational elements for executing applications, virtual machines, and cloud-based operations in modern data centers. Continuous innovation in CPU and GPU architecture to support AI, machine learning, and multitasking has further cemented their dominance. Major data center operators prioritize advanced processors to maximize performance, scalability, and energy efficiency in high-demand digital environments.

The Networking segment is expected to grow at the fastest CAGR of about 17.56% from 2025 to 2032, fueled by the increasing need for ultra-low latency and high-bandwidth communication within data centers. As AI, IoT, and edge computing gain prominence, networking chips that support fast data transfer, packet processing, and congestion management have become crucial. The proliferation of software-defined networking (SDN) and high-speed interconnects is also accelerating demand.

By Application

The Artificial Intelligence (AI) segment dominated the Data Center Chip Market with the highest revenue share of about 41% in 2024, owing to the escalating use of AI algorithms across industries. AI workloads require specialized chips such as GPUs, TPUs, and custom ASICs that offer massive parallel processing capabilities. Sectors like finance, healthcare, and e-commerce are deploying AI at scale for tasks like image recognition, fraud detection, and recommendation systems, driving up chip demand.

The Cloud Computing segment is expected to grow at the fastest CAGR of about 15.51% from 2025 to 2032, driven by widespread digital transformation and enterprise migration to cloud platforms. Cloud service providers are scaling their infrastructure and requiring high-performance, cost-efficient chips to manage dynamic workloads across public, private, and hybrid environments. Increased use of SaaS, PaaS, and containerized applications necessitates robust chip solutions for scalability, load balancing, and data security.

By Data Center Type

The Large Data Centers segment dominated the Data Center Chip Market with a revenue share of approximately 61% in 2024 and is expected to register the fastest CAGR of 15.05% from 2025 to 2032. This leadership is primarily due to the growing scale of operations by hyperscalers, cloud service providers, and multinational enterprises that centralize massive computational workloads. These centers require high-density, power-efficient chips capable of handling multi-tenant, AI-driven, and data-intensive processes. The rapid adoption of cloud platforms, big data analytics, and machine learning models continues to drive demand for advanced chip architectures, making large data centers the key growth engine.

Data Center Chip Market Regional Outlook

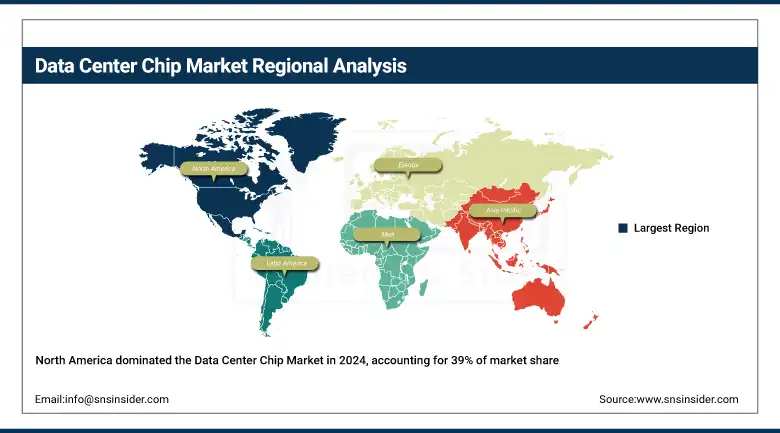

North America dominated the Data Center Chip Market with the highest revenue share of about 39% in 2024 due to its well-established data center infrastructure, high adoption of cloud services, and strong presence of leading tech giants such as Intel, AMD, and NVIDIA. The region also benefits from significant investments in AI, big data, and edge computing, which continue to drive demand for advanced data center chip solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. dominates the Data Center Chip Market due to advanced cloud infrastructure, tech giants' presence, and heavy investments in AI and hyperscale data centers.

Asia Pacific is expected to grow at the fastest CAGR of about 22.30% from 2025 to 2032 owing to rapid digital transformation, increasing data traffic, and rising investments in hyperscale data centers across countries like China, India, and Southeast Asia. Government support for digital infrastructure and the expanding footprint of global cloud providers are accelerating regional demand for high-performance and energy-efficient data center chips.

China is dominating the Data Center Chip Market in Asia Pacific due to massive data center expansion, strong government support, and leading domestic semiconductor manufacturing capabilities.

Europe is witnessing steady growth in the Data Center Chip Market, driven by increasing cloud adoption, rising demand for energy-efficient data centers, and digital transformation across industries. Germany leads the region, supported by strong infrastructure and industrial digitization initiatives.

Germany is dominating the Data Center Chip Market in Europe due to its advanced IT infrastructure, strong industrial base, and significant investments in digital transformation initiatives.

The Middle East & Africa and Latin America are emerging markets in the Data Center Chip trend, driven by growing internet penetration, increasing cloud adoption, and investments in digital infrastructure, with countries like UAE, Saudi Arabia, and Brazil showing notable momentum.

Key Players

Advanced Micro Devices, Inc., Alibaba, Arm Holdings, Broadcom Inc., Google, Huawei Technologies Co., Ltd., IBM Corporation, Intel Corporation, Marvell, Micron Technology, Inc., NVIDIA Corporation, Qualcomm, SAMSUNG, STMicroelectronics, Texas Instruments Incorporated

Recent Developments:

-

In 2025, Intel launched Xeon 6 processors with P-cores, offering enhanced AI acceleration, media processing, and networking capabilities, foundational for next-generation network infrastructure.

-

In 2025, Marvell demonstrated its first 2nm silicon IP for next-generation AI and cloud infrastructure, built on TSMC’s 2nm process, enhancing performance and efficiency.

-

In 2024, Broadcom delivered the Sian2 DSP, a 200G/lane PAM-4 DSP PHY, enabling 800G and 1.6T optical transceivers for next-generation AI clusters.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 19.73 Billion |

| Market Size by 2032 | USD 57.16 Billion |

| CAGR | CAGR of 14.32% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chip Type (Processors, Memory, Networking, Others) • By Data Center Type (Small and Medium-Sized Data Centers, Large Data Centers) • By Application (Artificial Intelligence (AI), Cloud Computing, Big Data Analytics) • By End-use (IT, Telecom, Healthcare, BFSI, Retail & E-commerce, Entertainment & Media, Energy, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Advanced Micro Devices, Inc., Alibaba, Arm Holdings, Broadcom Inc., Google, Huawei Technologies Co., Ltd., IBM Corporation, Intel Corporation, Marvell, Micron Technology, Inc., NVIDIA Corporation, Qualcomm, SAMSUNG, STMicroelectronics, Texas Instruments Incorporated |

Frequently Asked Questions

Ans: North America dominated the Data Center Chip Market in 2024 with a revenue share of approximately 39%, led by the U.S. market.

Ans: The Processors segment dominated in 2024 with a 48% share, remaining the primary revenue contributor due to its central computing role.

Ans: Surging cloud computing and AI workload demand is the major driver accelerating adoption of high-performance chips in hyperscale data centers.

Ans: The global Data Center Chip Market was valued at USD 19.73 billion in 2024.

Ans: The Data Center Chip Market is projected to grow at a CAGR of 14.32% from 2025 to 2032.

Get in Touch