Data Center Infrastructure Management Market Report Scope & Overview:

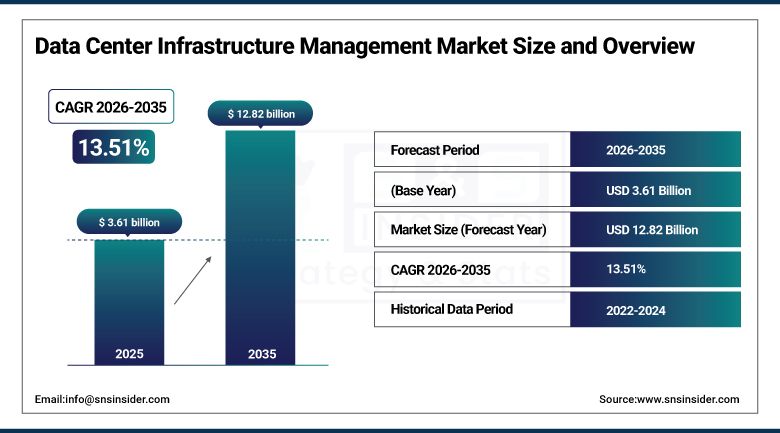

The Data Center Infrastructure Management Market size was USD 3.61 Billion in 2025 and is expected to reach USD 12.82 Billion by 2035, growing at a CAGR of 13.51% from 2026–2035.

The Data Center Infrastructure Management (DCIM) Market is witnessing healthy growth due to an increase in the need to optimize the operations of the data center, enhance energy efficiency, and maintain compliance among other factors. The data center infrastructure management market is being influenced by the fast-growing presence of hyperscale, colocation, enterprise, and edge data centers. The growth of the DCIM Market has been fueled by the growing usage of the technology in North America and Europe due to strict sustainability laws, power consumption issues, and visibility requirements in distributed facilities. The presence of the hyperscale data centers is expected to contribute significantly to investment in the infrastructure management and power, cooling, and capacity planning advancements in the coming years.

Hyperscale data center demand is accelerating as AI training workloads require massive, scalable compute and cooling infrastructure. Companies like Schneider Electric and Vertiv are developing AI-powered DCIM platforms that enable real-time energy optimization across multi-site environments. Sustainability pressures are also reshaping DCIM procurement as organizations seek solutions that support net-zero carbon commitments. Edge data centers are creating new demand for remote DCIM monitoring tools in markets where on-site IT staff are limited. These combined forces are transforming DCIM from a single-site operational tool into a multi-cloud, multi-facility enterprise infrastructure management platform.

Market Size and Forecast

-

Market Size in 2026E: USD 4.10 Billion

-

Market Size by 2035: USD 12.82 Billion

-

CAGR: 13.51% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Data Center Infrastructure Management Market - Request Free Sample Report

Data Center Infrastructure Management Market Trends

-

AI-powered DCIM platforms are enabling predictive maintenance, anomaly detection, and automated workload rebalancing.

-

Cloud-based DCIM deployment is gaining share as remote monitoring and multi-site management requirements grow.

-

Data center sustainability metrics are becoming core DCIM features as organizations pursue carbon reduction goals.

-

Edge data center proliferation is creating fresh demand for lightweight, remotely managed DCIM tools.

-

Digital twin simulation of data center environments is emerging as an advanced DCIM planning capability.

-

Integration of DCIM with IT service management platforms is enabling unified infrastructure visibility across IT and OT.

The U.S. Data Center Infrastructure Management Market Outlook

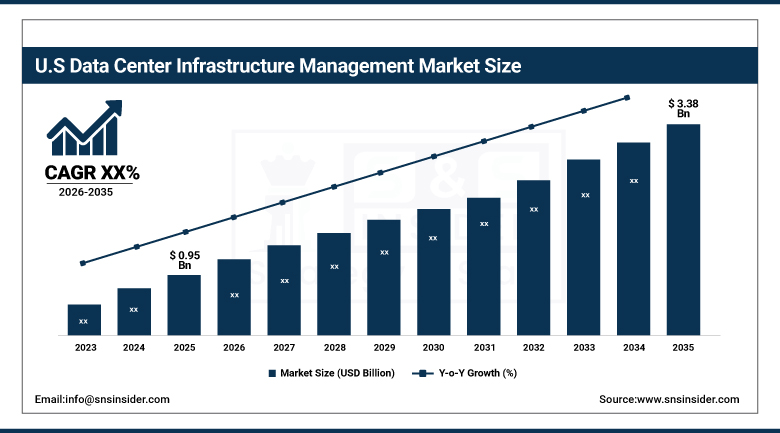

The U.S. data center infrastructure management market is estimated at approximately USD 0.95 Billion in 2025. It is expected to reach approximately USD 3.38 Billion by 2035.

The U.S. market is characterized by the fast development of hyperscale and edge data centers, AI-driven automation, and energy efficiency regulations. Cloud computing and sustainability programs become drivers of market growth as well. AI-integrated DCIM software and real-time monitoring tools help to optimize the performance of data centers. Major DCIM providers – Schneider Electric, Vertiv, IBM, and Cisco – drive domestic innovations and implementation. Investments into the construction of more data centers to run AI and cloud applications create additional demand for DCIM solutions.

In October 2024, DigitalBridge acquired Yondr Group, which develops and operates data centers. This step was made by the company to benefit from the AI boom. Yondr Group will remain an independent entity in the portfolio of DigitalBridge. The company has ongoing developments in Virginia, the UK, Malaysia, Japan, Germany, and India and contracted capacity equal to 878 MW. In October 2024, Blackstone entered into an agreement to acquire AirTrunk, which is an Australian data center operator, for $16 billion. This acquisition helped the company to position itself as one of the world's top digital infrastructure investors. These major acquisitions demonstrate the intensifying race for controlling the capacity of AI-capable data centers worldwide.

Data Center Infrastructure Management Market Segment Analysis

-

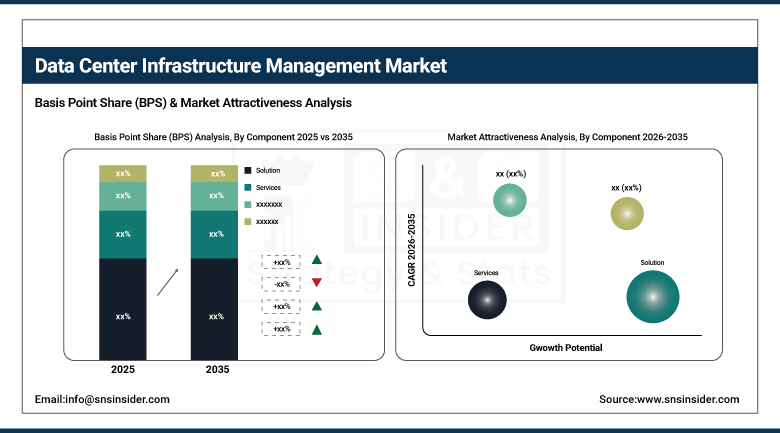

By Component, the solution segment dominated the data center infrastructure management market with approximately 68% share in 2025. The services segment is anticipated to witness the fastest CAGR during the forecast period.

-

By Deployment, the on-premises segment dominated the data center infrastructure management market with approximately 55% share in 2025. The cloud segment is estimated to grow at a considerable CAGR over the forecast period.

-

By Application, the asset management segment dominated the data center infrastructure management market with approximately 30% share in 2025. The BI & analytics segment is anticipated to witness significant CAGR growth.

-

By Vertical, the IT & ITeS segment dominated the data center infrastructure management market in 2025. The government & public sector segment is anticipated to register considerable CAGR throughout the forecast period.

By Component, solutions dominate, services grow fastest

The solution segment accounted for approximately 68% of revenue in 2025, driven by growing demand for centralized DCIM platforms that provide visibility across hybrid and multi-cloud infrastructure. Full DCIM solutions give operators a unified view across on-premise and cloud environments through centralized dashboards. This cross-environment perspective helps organizations distribute workloads efficiently, monitor resource utilization, and prevent over-commitment. The evolving hybrid and multi-cloud strategies continue introducing infrastructure management complexity that well-designed DCIM solutions address directly. As AI-driven data center complexity keeps growing, this segment should maintain its leadership position.

The services segment is anticipated to witness the fastest CAGR during the forecast period. With increasing data center complexity, many organizations are choosing managed services covering installation, monitoring, and maintenance of DCIM platforms. Managed service providers specialize in increasing the efficiency of data centers, enabling companies to concentrate on their primary business activities. Professional services including consulting, implementation, and training are also growing as organizations seek expert guidance for DCIM deployment. As data center operational complexity keeps increasing, demand for specialized services should keep accelerating.

By Deployment, on-premises dominates, cloud grows fastest

The on-premise segment held the leading market position in 2025, making up around 55% of revenue share. The advantage of using On-Premise implementation is that the firms get to tailor the DCIM software based on their individual requirements when it comes to defining performance level, integration with other software, and customization according to the company's procedures. Industries that have strict data sovereignty regulations such as BFSI, healthcare, and government favor On-Premise implementation due to its security and compliance aspects. Regulated firms require full control over access to their monitoring framework.

The cloud segment is estimated to grow at a considerable CAGR over the forecast period. The increasing prevalence of cloud-based services is driving the cloud deployment segment across the DCIM market. As enterprises move workloads to public, private, and hybrid clouds for scalability, flexibility, and cost-efficiency, they need cloud-based monitoring tools that follow those workloads. Cloud DCIM solutions are also solving legacy system integration challenges and reducing upfront capital expenditure for smaller operators. As cloud data center adoption keeps expanding, cloud-based DCIM should keep growing rapidly.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

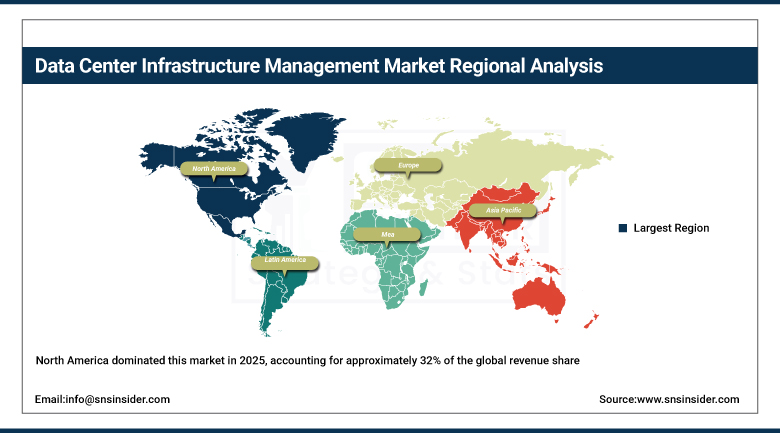

North America Data Center Infrastructure Management Market Insights

North America dominated this market in 2025, accounting for approximately 32% of the global revenue share. Growing need for scalable data centers across verticals including healthcare, finance, e-commerce, telecommunications, and entertainment drives regional leadership. Organizations are generating and processing more data than ever, creating consistent demand for advanced DCIM solutions to manage it effectively. The presence of major DCIM vendors and hyperscale cloud providers headquartered in the region further reinforces this leadership.

The United States accounts for approximately 82.5% of North American revenue. Hyperscale data center expansion, AI workload growth, and stringent energy efficiency regulations all keep fueling domestic DCIM adoption. This combination of demand and vendor presence keeps North America firmly in the lead.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Data Center Infrastructure Management Market Insights

Europe represents a meaningful DCIM market, supported by strong energy efficiency regulation and growing data sovereignty requirements. Germany leads the regional market, backed by strong industrial IT and financial services data center investment. France and the UK contribute meaningful demand through their own expanding cloud data center ecosystems and green building mandates.

Germany accounts for approximately 24.6% of European revenue. EU data sovereignty requirements and energy efficiency directives continue pushing organizations toward advanced DCIM monitoring and reporting. This regulatory environment should keep supporting steady European market growth.

Asia Pacific Data Center Infrastructure Management Market Insights

Asia Pacific is expected to register the fastest CAGR through the forecast period. Expansion of DCIM based on government initiatives and investments in digital infrastructure across Asia Pacific countries drives this growth. As governments pursue smart cities and digital connectivity, they are building and upgrading data centers that require advanced DCIM solutions. China, India, and Japan are all expanding data center capacity through both private investment and government programs.

China accounts for approximately 40.6% of Asia Pacific revenue. Rapid hyperscale data center construction and growing cloud adoption both keep expanding the regional DCIM addressable market. As smart city and digital economy investment keeps growing, this growth trajectory should continue strengthening.

MEA & Latin America Data Center Infrastructure Management Market Insights

The UAE leads MEA revenue, growing smart city infrastructure investment and expanding cloud data center capacity both support DCIM demand. Saudi Arabia is also expanding its data center infrastructure through Vision 2030 digital economy initiatives.

Brazil leads Latin American revenue, expanding cloud adoption and growing digital banking infrastructure both drive regional DCIM demand. Mexico and Argentina contribute secondary demand through their own expanding data center sectors.

Market Dynamics

Growth Drivers: Sustainability and cost optimization driving DCIM adoption

The constant attention to sustainability and energy efficiency forms another major market driver. Data centers are considered one of the largest consumers of electricity in the world; thus, organizations try to utilize DCIM solutions to optimize their power usage and adhere to various regulations regarding the environment. Moreover, improvements in the field of AI-enabled monitoring and analytics provide additional possibilities to enhance energy management. Government initiatives that encourage green data centers and use of renewable energy sources are another factor contributing to this process.

With increasing attempts to reduce the carbon footprint of companies and move to more sustainable workloads, such trend will continue to grow. Thus, the combination of regulatory requirements and cost savings creates an extremely strong market driver. Since AI-based loads are constantly growing in terms of energy consumption, DCIM is becoming more and more necessary.

Restraints: High implementation costs and legacy system integration complexity

DCIM implementation requires substantial investment in terms of software, hardware, and people training, making it difficult for SMEs. The integration of DCIM with existing IT infrastructure may lead to problems such as disruption of operations and delays in deployment periods. Most companies fail to integrate DCIM with multi-vendor environments due to interoperability problems.

Cost issues and integration problems are key barriers to adoption of DCIM technology. Insufficient internal expertise will definitely increase chances of failing in the implementation process. While cloud-based DCIM addresses some of these issues, integration problem continues to be a major restraint in the DCIM industry.

Opportunities: AI and IoT integration enhancing automation and real-time monitoring

The increased adoption of AI and IoT in DCIM solutions is making way for innovative capabilities in data center management. The use of AI-based analytics reduces downtime by means of predictive maintenance and increases operational efficiency within facilities. IoT sensors that provide real-time data on power usage, temperature, and network performance aid operations in making better operational decisions. It is particularly helpful in hyperscale and edge data centers.

The application of AI-based DCIM solutions can help organizations in resource management, automation, and security. The scaling of data centers together with the adoption of AI and IoT would drive growth in the forecast period. Early adopters adopting AI-based capabilities in their DCIM solutions would enjoy an operational advantage.

Recent Developments:

-

2024: DigitalBridge announced the acquisition of Yondr Group in October 2024, a data center developer and operator, to capitalize on AI infrastructure demand with contracted capacity of 878 MW globally.

-

2024: Blackstone agreed to acquire Australian data center operator AirTrunk for USD 16 billion in October 2024, positioning itself as a leading global digital infrastructure investor.

-

2024: Vantage Data Centers broke ground in October 2024 on its second Cyberjaya campus (KUL2) in Malaysia, a 35-acre facility delivering 256 MW of IT capacity to support cloud and AI growth.

Data Center Infrastructure Management Market Key Players are:

-

Schneider Electric

-

Vertiv

-

Eaton Corporation

-

Siemens

-

IBM Corporation

-

Cisco Systems, Inc.

-

Huawei Technologies

-

Nlyte Software

-

Sunbird Software

-

ABB

-

Panduit

-

FNT Software

-

Device42

-

Modius

-

Rackwise

-

Legrand SA

-

CommScope

-

Emerson Electric

-

Delta Electronics

-

Raritan Inc.

Data Center Infrastructure Management Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.61 Billion |

| Market Size by 2035 | USD 12.82 Billion |

| CAGR | CAGR of 13.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solution, Services) • By Deployment (On-premises, Cloud) • By Application (Asset Management, Capacity Planning, Power Monitoring, Environmental Monitoring, BI & Analytics, Others) • By Vertical (BFSI, Government & Public Sector, IT & ITeS, Manufacturing, Healthcare & Life Sciences, Telecommunications, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Schneider Electric, Vertiv, Eaton Corporation, Siemens, IBM Corporation, Cisco Systems, Inc., Huawei Technologies, Nlyte Software, Sunbird Software, ABB, Panduit, FNT Software, Device42, Modius, Rackwise, Legrand SA, CommScope, Emerson Electric, Delta Electronics, and Raritan Inc. |

Frequently Asked Questions

The Data Center Infrastructure Management Market is expected to grow at a CAGR of 13.51% from 2026 to 2035.

The Solution segment dominated with approximately 68% share in 2025.

Growing focus on sustainability, energy efficiency, and AI-driven data center automation are the primary growth factors.

The Data Center Infrastructure Management Market was valued at USD 3.61 Billion in 2025.

North America dominated the Data Center Infrastructure Management Market with approximately 32% revenue share in 2025.

Get in Touch