Data Center Market Report Scope & Overview:

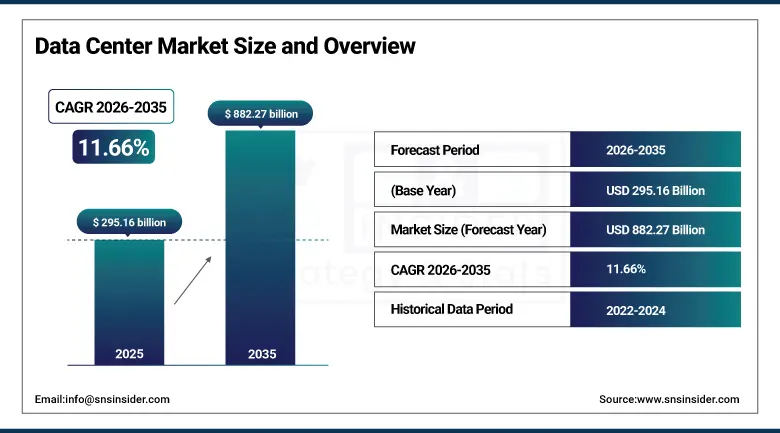

The Data Center Market was valued at USD 295.16 billion in 2025 and is expected to reach USD 882.27 billion by 2035, growing at a CAGR of 11.66% from 2026–2035.

Data centres represent the physical and organizational infrastructure of the digital economy, providing the computing, storage, networking, power, and cooling resources that enable every digital service, application, and communication system that individuals, enterprises, and governments depend upon in the modern world. The market encompasses an extraordinary spectrum of facility types from the hyperscale campus data centres operated by Amazon Web Services, Microsoft Azure, Google Cloud, and Meta whose individual facilities encompass hundreds of thousands of servers consuming hundreds of megawatts of power through the enterprise data centres that organizations operate to host their own IT infrastructure rather than consuming cloud services, through the colocation facilities that provide neutral interconnection hubs where multiple enterprises can house their private IT equipment in a shared facility with superior power redundancy, physical security, and network connectivity than most individual organizations can economically provide in-house, to the edge data centres that extend compute capabilities to locations close to end users and data sources where network latency constraints and data sovereignty requirements make centralized processing impractical.

The International Energy Agency's 2025 report estimating that data centres consumed approximately 415 terawatt-hours of electricity globally in 2024, representing approximately 1.5% of global electricity demand, and projecting this figure to grow to 1,000 terawatt-hours by 2030 driven primarily by AI workload electricity intensity, confirms the extraordinary scale of infrastructure investment and power capacity expansion that the data centre market's growth trajectory requires across the 2026 to 2035 forecast period.

Market Size and Forecast

- Market Size in 2026E: USD 329.55 Billion

- Market Size by 2035: USD 882.27 Billion

- CAGR: 11.66% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information on Data Center Market - Request Free Sample Report

Data Center Market Trends

- Rapid expansion of AI-optimized GPU cluster data centers is driving large-scale investments in high-density computing infrastructure.

- Growing adoption of direct liquid cooling and immersion cooling technologies is supporting advanced AI and high-performance computing workloads.

- Rising enterprise demand for hybrid cloud architectures is increasing investment in colocation data center facilities.

- Data center operators are increasingly focusing on renewable energy, energy efficiency, and sustainability initiatives to meet ESG and regulatory goals.

- Expanding deployment of edge data centers is supporting real-time AI inference, 5G, IoT, and low-latency applications.

The U.S. Data Center Market Outlook

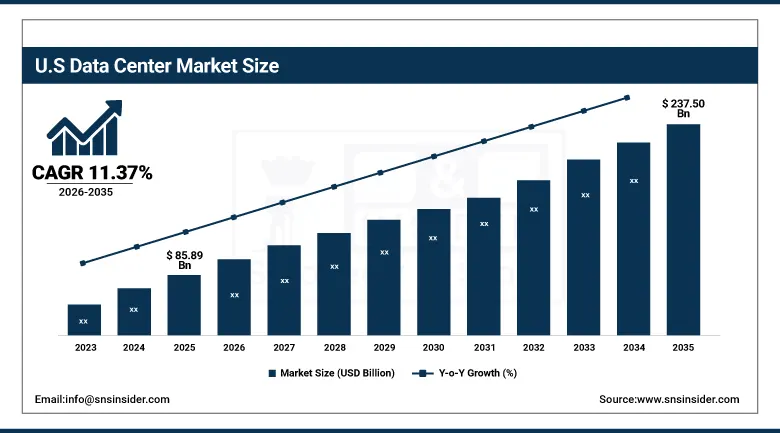

The U.S. Data Center Market was valued at approximately USD 85.89 billion in 2025 and is expected to reach approximately USD 237.50 billion by 2035, growing at a CAGR of 11.37%, driven by the concentration of hyperscale cloud provider headquarters and data centre campuses. The world's largest AI computing infrastructure investment programme, and the extraordinary electricity and real estate infrastructure investment that sustained hyperscale capacity expansion requires across the primary U.S. data centre markets of Northern Virginia, Phoenix, Dallas, Chicago, and the Pacific Northwest.

The United States commands the largest national data centre market globally through the extraordinary concentration of hyperscale cloud infrastructure in the primary U.S. colocation and hyperscale market clusters, where Northern Virginia's Loudoun County alone hosts more data centre capacity than any other geography globally and whose continued expansion is driving unprecedented power grid investment requests that are reshaping regional electricity infrastructure planning horizons. The AI computing investment wave has created a U.S. data centre capital expenditure cycle of historically unprecedented scale, where Microsoft, Google, Amazon, Meta, and Oracle collectively announced over USD 300 billion in combined U.S. data centre investment commitments in 2025, representing a capacity expansion programme that will reshape the U.S. data centre landscape and the associated power and construction industries that serve it over the following decade.

The U.S. executive orders directing federal agencies to accelerate AI infrastructure permitting, combined with state-level data centre incentive programmes including tax abatements and expedited grid connection processes that over 40 U.S. states have implemented to attract hyperscale investment, are creating a policy environment that sustains the United States' competitive position as the world's primary hyperscale data centre deployment location despite growing international competition from Ireland, Singapore, and emerging data centre markets.

Data Center Market Segment Analysis

- By Type, hyperscale data centers dominated with approximately 46.5% share in 2025 through the rapid expansion of cloud services, AI, and big data analytics demanding massive computing capacity and scalability from the largest cloud provider investments. Colocation data centers are the fastest-growing at a CAGR of 12.3% fueled by enterprise preference for cost-effective, flexible, and secure shared infrastructure that reduces capital expenditure.

- By Component, servers led the market with approximately 38.6% share in 2025 as high-performance computing, AI workloads, and virtualization drive demand for efficient and powerful server systems across industries. Networking equipment is the fastest-growing at a CAGR of 11.4% driven by the bandwidth requirements of AI GPU cluster interconnects and the shift toward software-defined networking in hyperscale deployments.

- By Deployment, cloud dominated with approximately 52.2% share in 2025 reflecting the sustained enterprise migration of workloads from on-premise infrastructure to public cloud services. Hybrid is the fastest-growing at a CAGR of 13.1% as organizations balance the scalability of cloud with data sovereignty, performance, and compliance requirements that retain specific workloads in private or colocation infrastructure.

- By End User, IT & telecom dominated with approximately 41.8% in 2025 through growing data traffic, 5G network expansion, and cloud adoption by technology and telecommunications providers. Healthcare is the fastest-growing end user at a CAGR of 12.6% driven by electronic health record expansion, medical imaging AI, genomics data processing, and regulatory requirements for secure clinical data management.

By Type, hyperscale dominates, colocation is expected to grow fastest

Hyperscale data centers retained the dominant type position with approximately 46.5% of the data center market in 2025, reflecting the extraordinary capital investment concentration among the five largest hyperscale cloud providers whose facility portfolios now span hundreds of data centres across dozens of countries, each individual campus representing billions of dollars of server, networking, power, and real estate investment whose scale creates unit economics unavailable to smaller operators. The AI training workload's requirements for clusters of thousands or tens of thousands of GPU servers that must be interconnected with extremely high-bandwidth, low-latency networks within a single facility or tightly interconnected campus complex has fundamentally aligned with the hyperscale operators' ability to construct purpose-built AI computing facilities at scales that no other operator category can match, sustaining the hyperscale segment's market share dominance even as colocation and edge data centre growth rates exceed it.

Colocation data centers are the fastest-growing type at a CAGR of 12.3% through 2035, driven by the enterprise hybrid cloud strategy's requirement for interconnection infrastructure that provides physical proximity to multiple cloud on-ramps from a neutral facility where private equipment can be housed alongside direct cloud peering connections that minimize the latency and bandwidth cost of data transfer between private and cloud environments. The colocation market's growth is further supported by the data sovereignty regulations in European, Asian, and emerging market jurisdictions that require certain data categories to remain within national territory on infrastructure under the customer's direct control, creating a compliance-driven colocation demand from multinational enterprises who cannot satisfy sovereignty requirements by routing all workloads through public cloud infrastructure that may not provide the geographic data residency guarantees that regulations mandate.

By Deployment, cloud dominates, hybrid is expected to grow fastest

Cloud deployment retained the dominant position with approximately 52.2% of data center market revenues in 2025, as the sustained enterprise migration of applications and workloads from on-premise infrastructure to public cloud services from AWS, Azure, and Google Cloud continues to grow the managed infrastructure revenue that hyperscale providers generate from their data centre facilities. The cloud deployment model's commercial advantages including consumption-based pricing, elastic capacity scaling, managed security, and elimination of hardware refresh cycle capital expenditure have proven compelling to the majority of enterprise IT buyers who have the application portfolio characteristics and regulatory situation that make public cloud deployment the optimal choice from a total cost of ownership and operational agility perspective.

Hybrid deployment is the fastest-growing at a CAGR of 13.1% through 2035, reflecting the maturation of enterprise cloud strategy beyond the initial all-cloud enthusiasm toward the nuanced multi-environment architecture that optimizes each workload's placement based on latency, compliance, cost, and performance characteristics rather than defaulting all workloads to a single deployment model. Hybrid cloud infrastructure, where workloads run across a combination of private on-premise or colocation infrastructure and one or more public cloud environments with seamless data and application portability between them, is becoming the standard enterprise IT architecture as the limitations of pure public cloud for regulatory, latency, and cost-sensitive workload categories become apparent from operational experience.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.3% |

|

Europe |

United Kingdom |

23.8% |

|

Asia Pacific |

China |

42.6% |

|

Middle East & Africa |

UAE |

32.7% |

|

Latin America |

Brazil |

43.2% |

North America Data Center Market Insights

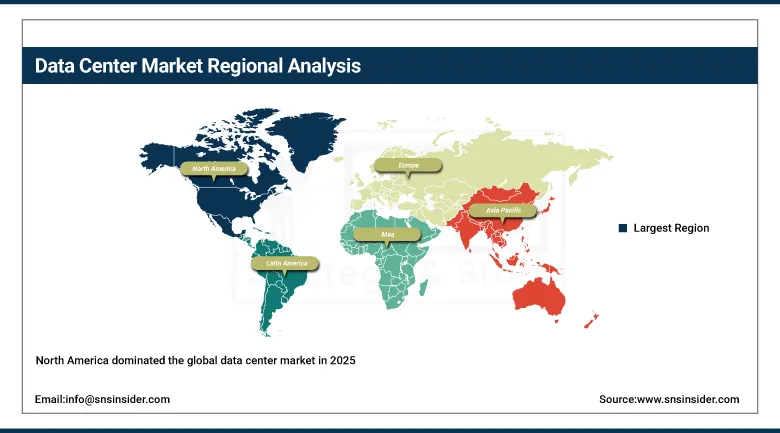

North America dominated the global data center market in 2025, with the United States accounting for approximately 87.3% of North American revenues as the world's largest data centre market by both installed capacity and annual capital investment. The region's commanding position reflects the concentration of all five of the world's largest hyperscale cloud providers' headquarters in the United States, whose combined data centre capital expenditure has created the world's largest and most technologically advanced data centre capacity base across Northern Virginia, Phoenix, Dallas-Fort Worth, Chicago, Silicon Valley, and the Pacific Northwest. The U.S. government's AI executive order provisions and the CHIPS Act's data centre infrastructure provisions are creating additional federal procurement and subsidy frameworks that sustain domestic data centre investment above the commercial market-driven baseline.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Data Center Market Insights

Europe is a sophisticated and rapidly growing data centre market characterized by the GDPR's data residency requirements creating domestic data centre demand, the Green Deal's energy efficiency and renewable energy targets shaping data centre sustainability investment, and the concentration of major colocation and hyperscale campuses in the Amsterdam-Frankfurt-London-Dublin-Paris corridor that serves as the primary European internet exchange and cloud interconnection hub. The United Kingdom accounts for approximately 23.8% of European data centre revenues as the region's largest single market, anchored by London's role as the European financial services data centre hub and the concentration of major UK colocation facilities from Equinix, Digital Realty, and CyrusOne that provide the interconnection infrastructure for European enterprise and cloud workloads.

Asia Pacific Data Center Market Insights

Asia Pacific is the fastest-growing data centre market, driven by the extraordinary AI infrastructure investment programmes of Chinese technology companies including Alibaba Cloud, Tencent Cloud, and Baidu alongside China's national AI development strategy funding, the rapid hyperscale expansion of Japanese data centre markets driven by Microsoft, Google, and Amazon's announced multi-billion-dollar Japan investment commitments, Singapore's position as the Southeast Asian data centre hub despite government moratoriums on new facility approvals that are redirecting investment to adjacent markets including Malaysia, Thailand, and Indonesia, and India's rapidly growing data centre market driven by the world's fastest-growing digital economy. China accounts for approximately 42.6% of Asia Pacific revenues through its combination of the world's second-largest absolute data centre capacity, active AI infrastructure construction, and the domestic cloud provider ecosystem that serves China's enormous digital economy.

MEA & Latin America Data Center Market Insights

Middle East and Africa and Latin America are rapidly growing data centre markets where hyperscale cloud provider expansion, smart city infrastructure investment, and digital economy development are driving significant data centre construction activity. UAE leads MEA data centre revenues at approximately 32.7% of regional revenues through its position as the region's primary data centre hub where Microsoft, AWS, Google, and Oracle have all announced or deployed regional cloud infrastructure, combined with the government's AI strategy investment and the country's role as a connectivity hub for data traffic between Africa, South Asia, and Europe. Brazil leads Latin American revenues at approximately 43.2% through its combination of the region's largest internet user population, well-developed domestic internet exchange infrastructure in Sao Paulo, and the active deployment of AWS, Azure, and Google Cloud Brazil regions serving the Latin American cloud market.

Market Dynamics

Growth Drivers: AI computing infrastructure investment creating unprecedented data centre construction demand

The primary structural growth drivers for the data center market are the extraordinary AI computing infrastructure investment cycle that is creating the largest single-application data centre construction demand in the industry's history, as every major technology company, AI research organization, and cloud provider is simultaneously investing at unprecedented scale in GPU cluster facilities that will train and serve the AI models whose commercial applications are transforming every industry, combined with the continued enterprise cloud migration that sustains hyperscale facility expansion demand independent of the AI investment wave and the proliferation of edge computing requirements that are creating entirely new categories of data centre deployment in geographies and applications where centralized cloud facilities cannot meet latency or sovereignty requirements.

Restraints: Power grid capacity constraints limiting hyperscale expansion timelines in primary data centre markets

A significant restraint on the data center market is the power grid capacity constraint that is increasingly limiting the pace of hyperscale data centre expansion in primary markets including Northern Virginia, where utility queues for new large industrial customer connections have extended to multi-year waiting periods that create serious competitive disadvantages for operators unable to secure power at the speed that AI infrastructure investment timelines require. The grid connection bottleneck is not merely a temporary queue issue but reflects the fundamental inadequacy of existing electricity transmission and generation infrastructure to absorb the hundreds of gigawatts of new data centre load that hyperscale expansion plans contemplate over the next decade, requiring multi-billion-dollar transmission infrastructure investments that take years to plan, permit, and construct.

Opportunities: AI infrastructure as a service business model creating new revenue streams

The commercialization of AI infrastructure as a service, where specialized providers including CoreWeave, Lambda Labs, and Crusoe Energy operate GPU cluster data centres and sell computing capacity on a pay-per-use basis to enterprises and AI development organizations that cannot or prefer not to build their own AI infrastructure, represents a distinct and rapidly growing data centre market segment whose unit economics of GPU compute rental at premium per-hour rates generate substantially higher revenue per square meter of data centre space than conventional server colocation. Advanced liquid cooling technology's commercial maturation is creating the technical foundation for dramatically denser data centre designs where direct liquid cooling enables rack power densities of 50 to 100 kilowatts per rack that air-cooled designs cannot sustain, enabling hyperscale operators to serve growing AI compute demand within constrained land and power footprints by increasing the compute density per square meter of data centre floor space.

Recent Developments:

- 2025: Schneider Electric launched a EUR 200 million smart data centre in Lyon, France specifically designed for AI, cloud, and digital enterprise requirements, incorporating AI-driven cooling optimization, modular design enabling rapid capacity expansion, and on-site renewable energy integration that cuts emissions by 40% while maintaining the high availability that mission-critical enterprise applications require.

- 2025: Microsoft announced a USD 80 billion global data centre investment commitment for fiscal year 2025, the largest single-year data centre capital expenditure announcement in corporate history, with over half of the investment directed toward U.S. facilities for AI infrastructure expansion that will serve both commercial Azure AI services and potential federal government AI computing requirements.

- 2025: Equinix expanded its xScale hyperscale data centre programme with new campus deployments in Singapore, Frankfurt, and Tokyo serving hyperscale cloud provider demand for wholesale data centre capacity in the fastest-growing international markets where cloud provider direct facility ownership is constrained by local regulatory or real estate barriers.

Data Center Market Key Players are:

- Amazon Web Services (AWS)

- Microsoft Corporation (Azure)

- Google LLC (Google Cloud)

- Meta Platforms Inc.

- Equinix Inc.

- Digital Realty Trust Inc.

- NTT Communications

- CyrusOne LLC

- Iron Mountain Inc.

- Switch Inc.

- Lumen Technologies

- Schneider Electric SE

- Vertiv Holdings Co.

- Eaton Corporation plc

- Cisco Systems Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise

- IBM Corporation

- Oracle Corporation

- CoreWeave Inc.

Data Center Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 295.16 Billion |

| Market Size by 2035 | USD 882.27 Billion |

| CAGR | CAGR of 11.66% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Hyperscale Data Centers, Colocation Data Centers, Edge Data Centers, Enterprise Data Centers) •By Component (Servers, Networking Equipment, Storage, Power Infrastructure, Cooling Systems, Others) •By Deployment (Cloud, On-Premise, Hybrid) •By End User (IT & Telecom, BFSI, Healthcare, Government & Defense, Retail & E-Commerce, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amazon Web Services (AWS), Microsoft Corporation (Azure), Google LLC (Google Cloud), Meta Platforms Inc., Equinix Inc., Digital Realty Trust Inc., NTT Communications, CyrusOne LLC, Iron Mountain Inc., Switch Inc., Lumen Technologies, Schneider Electric SE, Vertiv Holdings Co., Eaton Corporation plc, Cisco Systems Inc., Dell Technologies Inc., Hewlett Packard Enterprise, IBM Corporation, Oracle Corporation, CoreWeave Inc. |

Frequently Asked Questions

Get in Touch