Denim Market Report Scope & Overview:

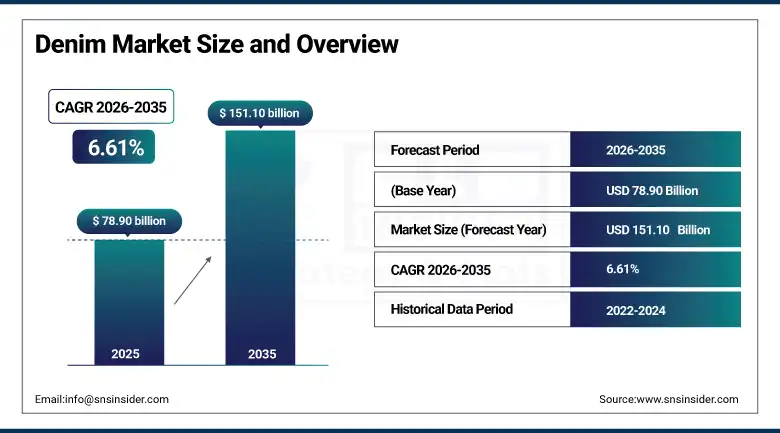

The Denim market was valued at USD 78.90 billion in 2025 and is expected to reach USD 151.10 billion by 2035, growing at a CAGR of 6.61% from 2026–2035.

Denim occupies a uniquely democratic position in global fashion, serving simultaneously as the casual uniform of the world's youth across every income level and cultural context, the artisanal craft object of premium fashion connoisseurs who invest hundreds of dollars in selvedge Japanese fabric and heritage workwear reproductions, the blank canvas of streetwear culture whose limited-edition collaborative releases command resale premiums as collectible cultural artefacts, and the workhorse workwear of industrial and agricultural labour whose durability requirements defined the original technical specification of the twill weave cotton fabric from which every denim product derives. The market's extraordinary breadth encompasses the complete range of denim-constructed garments and accessories from the foundational jean that has served as Western fashion's default casual trouser since the 1950s through the denim jacket whose periodic revivals track fashion cycles with remarkable predictability, the dungaree and jumpsuit formats that transition between workwear heritage and fashion-forward styling depending on prevailing trend direction, and the expanding denim accessories and footwear categories whose adoption of denim as a structural and decorative material extends the fabric's reach across the complete wardrobe.

Euromonitor International's 2025 apparel market analysis confirming that denim jeans remain the single most purchased clothing item globally by both unit volume and consumer purchase frequency across all major markets demonstrates the category's extraordinary demand resilience and validates the structural market opportunity that the global expansion of the middle-class consumer population represents for denim market participants over the 2026 to 2035 forecast period.

Market Size and Forecast

-

Market Size in 2026E: USD 84.11 Billion

-

Market Size by 2035: USD 151.10 Billion

-

CAGR: 6.61% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Denim Market - Request Free Sample Report

Denim Market Trends

-

Growing adoption of sustainable manufacturing technologies is reducing water consumption and improving ESG compliance in denim production.

-

Rising demand for stretch and performance denim is driven by increasing preference for comfort-focused casual wear.

-

Premiumization trends are encouraging consumer spending on high-quality and heritage denim products.

-

Expanding direct-to-consumer and digital-native denim brands are strengthening online apparel sales and personalized shopping experiences.

-

Increasing popularity of resale, vintage, and repaired denim products is supporting growth of the circular fashion economy.

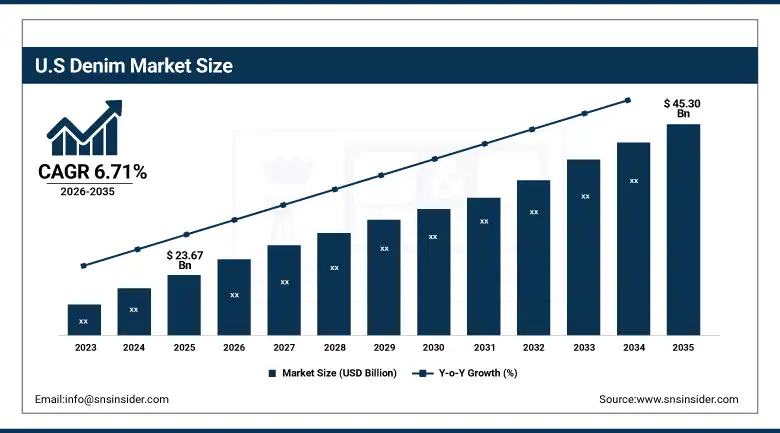

The U.S. Denim Market Outlook

The U.S. Denim Market was valued at approximately USD 23.67 billion in 2025 and is expected to reach approximately USD 45.30 billion by 2035, growing at a CAGR of 6.71%. This is driven by the world's most established denim purchasing culture, strong brand loyalty to domestic heritage denim brands including Levi's, Wrangler, and Lee, growing direct-to-consumer premium denim adoption, and sustained athleisure-influenced demand for stretch performance denim across age and income demographics.

The United States is the world's largest national denim market by revenue, where the cultural centrality of denim to American casual dress dating from the Gold Rush workwear origins through Marlon Brando and James Dean's cultural adoption of jeans as counterculture fashion through the contemporary wardrobe's default casual bottom creates a deeply embedded consumption habit that sustains per-capita denim spending above any other major market. Levi Strauss & Co.'s sustained leadership in the U.S. denim market, with annual revenues exceeding USD 6 billion despite intense competition from fast fashion, premium denim, and direct-to-consumer challengers, demonstrates the extraordinary brand equity durability of heritage denim brands whose origin stories, cultural associations, and quality reputation sustain consumer preference across generational transitions.

The U.S. apparel market's documented trend toward casual dressing that accelerated dramatically during the pandemic remote work period and has proven permanently resilient in the post-pandemic era, with office dress codes remaining substantially more casual than pre-2020 norms across the majority of white-collar workplaces, sustains the elevated frequency of denim wearing occasions that benefits the market's volume growth trajectory.

Denim Market Segment Analysis

-

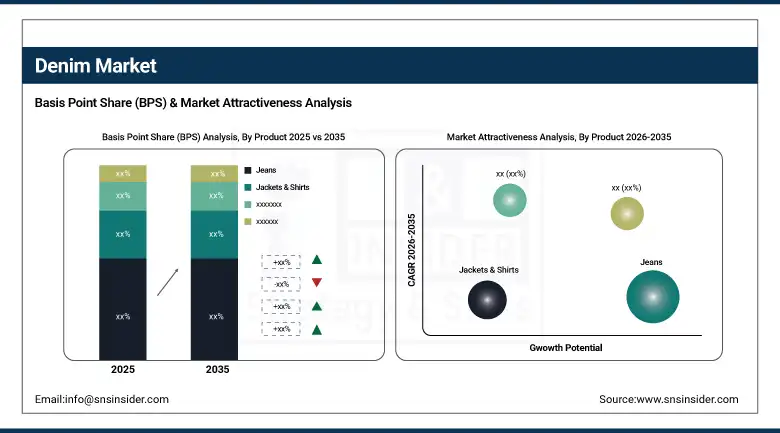

By Product, jeans led the market with approximately 45.23% share in 2025 through their universal appeal, versatility across occasions, and status as the category-defining denim product that anchors all other denim categories in wardrobe planning. Jumpsuits are the fastest-growing product at a CAGR of 9.10% driven by fashion versatility, growing gender-neutral styling adoption, and the influence of streetwear and workwear heritage aesthetics.

-

By Type, medium denim led with approximately 50.36% in 2025 as the most versatile weight for year-round wearing across the full range of denim product categories. light denim is the fastest-growing at a CAGR of 8.50% driven by demand for breathable, lightweight fabrics suitable for warm climates and the continuing casualisation of denim towards lighter, more comfortable everyday weights.

-

By Distribution Channel, offline dominated with approximately 60.51% in 2025 as specialty denim retailers, department stores, and brand flagships provide the fit trial experience that remains important for denim consumer confidence. Online is the fastest-growing at a CAGR of 14.32% as improved size recommendation technology, free returns policies, and direct-to-consumer brand growth reduce the fit uncertainty barrier to digital denim purchasing.

-

By End User, men held the largest share of 40.65% in 2025 through their historically higher denim purchasing concentration. Women are the fastest-growing segment at a CAGR of 11.30% driven by expanding style diversity in women's denim including high-rise, wide-leg, and fashion-forward silhouettes that command higher per-unit average selling prices and more frequent replacement cycles than menswear.

By Product, jeans dominate, jumpsuits are expected to grow fastest

Jeans retained the dominant product position with approximately 45.23% of the denim market in 2025, as the foundational denim product that has served as the default casual trouser across every market and demographic since its transition from workwear to everyday fashion maintains its commercial primacy through the unique combination of cultural ubiquity, extraordinary fit diversity encompassing dozens of silhouette and rise combinations for every body type, durability that sustains replacement demand without fashion obsolescence motivation, and the continuous innovation investment by denim brands that regularly refreshes the jean category's product proposition through new fabric technologies, sustainable production claims, and silhouette evolution that maintains relevance across generational transitions. The jean's commercial resilience through multiple fashion cycles that periodically declared its obsolescence has consistently proven more durable than its alternatives, returning from each forecast demise to resume its position as the world's most purchased single apparel item by volume.

Jumpsuits are the fastest-growing product at a CAGR of 9.10% through 2035, driven by their alignment with the gender-neutral dressing trend, the growing consumer preference for complete outfit solutions that eliminate styling decision complexity, the influence of workwear heritage and utilitarian aesthetics in contemporary streetwear that has elevated the jumpsuit from a specialist garment into a mainstream fashion staple for younger consumer demographics. The proliferation of jumpsuit styles from form-fitting fashion-forward interpretations through relaxed straight-leg heritage reproductions and technical cargo-influenced designs across premium and fast fashion brands is expanding the jumpsuit's consumer demographic and occasion versatility beyond the niche consumer who previously represented its primary purchaser.

By Distribution Channel, offline dominates, online is expected to grow fastest

Offline retail retained the dominant distribution position with approximately 60.51% of denim market revenues in 2025, as the physical fit trial experience remains an important consumer confidence factor for denim purchasing where the variability in sizing and silhouette across brands and style categories creates a meaningful risk of size mismatch that in-store try-on eliminates and that online purchasing requires consumers to either accept as returnable or resolve through established brand-specific size knowledge. Specialty denim retailers including Levi's brand stores, G-Star Raw flagships, premium denim boutiques stocking curated multi-brand selections, and department store denim destinations where trained denim specialists assist consumers through the brand and style selection process sustain the in-store denim shopping experience's commercial relevance despite e-commerce growth.

Online is the fastest-growing distribution channel at a CAGR of 14.32% through 2035, driven by the progressive resolution of the fit uncertainty barrier through AI-powered size recommendation algorithms that use purchased-returned product data to predict fit preferences with increasing accuracy, direct-to-consumer denim brands whose business models are designed for digital-first customer acquisition and retention rather than wholesale retail distribution, and the growing consumer comfort with returning ill-fitting online purchases that makes digital denim purchasing a lower-risk decision than the early e-commerce era's final-sale dynamics suggested.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.2% |

|

Europe |

Germany |

23.6% |

|

Asia Pacific |

China |

45.8% |

|

Middle East & Africa |

UAE |

27.4% |

|

Latin America |

Brazil |

44.3% |

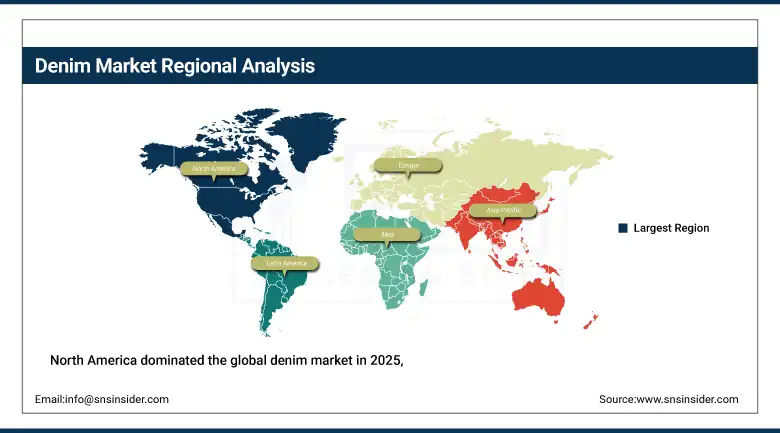

North America Denim Market Insights

North America dominated the global denim market in 2025, with the United States accounting for approximately 83.2% of North American revenues as the world's most established denim market where the category's cultural depth, brand heritage concentration, and sustained per-capita consumption create the highest absolute revenue base of any national market. The region's market leadership reflects the concentration of major denim brand headquarters including Levi Strauss & Co., Kontoor Brands operating Wrangler and Lee, G-III Apparel Group, and the U.S. design operations of PVH and Tapestry whose brand portfolios encompass multiple denim product lines serving diverse consumer segments from heritage workwear through contemporary fashion premium.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Denim Market Insights

Europe is a sophisticated denim market characterised by strong per-capita denim consumption across Western European markets, a premium denim culture that sustains higher average selling prices than Asian mass markets, and the concentration of influential denim fashion brands including G-Star Raw, Diesel, Replay, and the European operations of Japanese selvedge denim specialists that position European denim culture at the premium end of the global quality spectrum. Germany accounts for approximately 23.6% of European denim revenues as the region's largest national market through its combination of high consumer spending power, a strong outdoor and active lifestyle culture that sustains casual denim adoption, and the presence of major European apparel retail infrastructure providing broad denim product accessibility across price tiers.

Asia Pacific Denim Market Insights

Asia Pacific is the fastest-growing regional denim market, driven by the convergence of the world's largest young consumer population, rapidly rising incomes bringing hundreds of millions of new consumers into the commercially relevant denim purchasing demographic for the first time, the extraordinary cultural influence of Western fashion and American casualwear aesthetics across Asian youth markets, and the growth of domestic Asian denim brands competing effectively against international labels through superior local market knowledge and more accessible price points. China accounts for approximately 45.8% of Asia Pacific denim revenues through its combination of the world's largest youth population with growing fashion awareness, rapidly expanding middle-class income supporting branded denim investment, and a sophisticated domestic denim manufacturing and brand development industry that produces both for export and for the world's fastest-growing domestic denim consumption market.

MEA & Latin America Denim Market Insights

Middle East and Africa and Latin America are growing denim markets where youthful demographic profiles, rising urbanisation, and expanding middle-class populations with aspirational Western fashion preferences are creating sustained demand growth. UAE leads MEA revenues at approximately 27.4% through its high per-capita income supporting premium denim access and the cosmopolitan consumer culture of Dubai and Abu Dhabi whose retail infrastructure provides broad international brand availability. Brazil leads Latin American revenues at approximately 44.3% through its combination of the world's fourth-largest denim fabric producing capability, a sophisticated domestic denim fashion market with strong brand presence from Hering, Malwee, and international labels, and a youth-heavy demographic profile with strong fashion engagement.

Market Dynamics

Growth Drivers: Global middle class expansion bringing new denim consumers across emerging markets

The primary structural growth drivers for the denim market are the extraordinary scale of the global middle-class expansion across Asia Pacific, Africa, and Latin America that is continuously enlarging the commercially relevant denim purchasing demographic as hundreds of millions of consumers cross the income thresholds at which branded denim investment becomes financially accessible, combined with the sustained innovation investment across denim fabric technology, sustainability improvement, and digital consumer experience that continuously refreshes the category's relevance and justifies trading up to higher-value denim products among existing consumers. The cultural dominance of Western casual fashion globally, whose most identifiable garment remains the denim jean, sustains aspirational purchase motivation across new denim markets where wearing the same category as globally admired celebrity and influencer reference points carries meaningful cultural value beyond functional clothing utility.

Restraints: Cotton price volatility creating manufacturing cost uncertainty, fast fashion competition eroding margin sustainability for mid-tier denim brands

A significant restraint on the denim market is the commodity price volatility of cotton, which constitutes 60 to 80% of conventional denim fabric raw material cost and whose price is determined by agricultural conditions, geopolitical trade factors, and speculative investment demand that create manufacturing cost fluctuations that denim brands cannot reliably pass through to retail prices in competitive markets without risking consumer price resistance or private label switching. The sustainability challenge facing the denim industry's historical production processes, where conventional ring-spinning, dyeing with synthetic indigo, and stone-washing with pumice involve significant water consumption, chemical usage, and stone dust generation, has become a reputational risk that consumers and retail buyers increasingly scrutinise, creating compliance costs for brands investing in cleaner production technology and reputational risk for those who do not.

Opportunities: Regenerative cotton and organic denim premium positioning, denim circular economy through take-back and recycling programmes

The development of regenerative cotton supply chains that document and certify soil health improvement, carbon sequestration, and biodiversity enhancement across denim cotton farming operations represents a premium provenance story that resonates with environmentally conscious luxury and premium denim consumers who will pay price premiums for certified sustainable sourcing that contributes demonstrable environmental improvement beyond simply avoiding harm. Circular denim economy programmes that collect post-consumer denim products for mechanical recycling into new denim fabric blends, chemical depolymerisation into virgin-quality recycled cotton fibre, or upcycling into denim accessories and home textiles are creating brand differentiation stories and closing the material loop that linear take-make-dispose production economics cannot close.

Recent Developments:

-

2025: Levi Strauss & Co. announced a significant expansion of its Water<Less production programme incorporating ozone finishing and waterless dyeing technology across its global manufacturing network, reporting cumulative water savings exceeding 6 billion litres since the programme's inception and setting a target of using Water<Less techniques on 100% of its denim products by 2030.

-

2025: G-Star Raw launched an expanded range of ocean plastic-derived denim products incorporating Bionic Yarn fibre produced from ocean-recovered plastic waste, extending its pioneering raw denim sustainability positioning into circular economy material sourcing that supports the brand's premium environmental credentials across key European and North American markets.

-

2025: Diesel continued its premium positioning strategy with new limited-edition collaborative denim releases and expansion of its direct-to-consumer digital channel, reporting above-average growth in its premium tier above EUR 200 price point range that reflects the broader market premiumisation trend benefiting brands with strong luxury-adjacent heritage positioning.

Denim Market Key Players are:

-

Levi Strauss & Co.

-

VF Corporation (Wrangler, Lee)

-

G-Star Raw

-

Diesel S.p.A.

-

H&M Group

-

Inditex (Zara)

-

PVH Corp. (Calvin Klein, Tommy Hilfiger)

-

Gap Inc.

-

Kontoor Brands (Wrangler, Lee)

-

Pepe Jeans London

-

Tom Tailor Group

-

Replay S.p.A.

-

True Religion Brand Jeans

-

AG Jeans

-

Citizens of Humanity

-

Frame Denim

-

Madewell (J.Crew Group)

-

Naked & Famous Denim

-

Nudie Jeans Co.

-

Everlane

Denim Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 78.90 Billion |

| Market Size by 2035 | USD 151.10 Billion |

| CAGR | CAGR of 6.61% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Jeans, Jackets & Shirts, Trousers, Dresses, Shorts, Jumpsuits, Dungarees, Others) •By Type (Light Denim, Medium Denim, Heavy Denim) •By Distribution Channel (Online, Offline) •By End User (Men, Women, Children) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Levi Strauss & Co., VF Corporation (Wrangler, Lee), G-Star Raw, Diesel S.p.A., H&M Group, Inditex (Zara), PVH Corp. (Calvin Klein, Tommy Hilfiger), Gap Inc., Kontoor Brands (Wrangler, Lee), Pepe Jeans London, Tom Tailor Group, Replay S.p.A., True Religion Brand Jeans, AG Jeans, Citizens of Humanity, Frame Denim, Madewell (J.Crew Group), Naked & Famous Denim, Nudie Jeans Co., Everlane |

Frequently Asked Questions

North America dominated the denim market in 2025.

Jeans dominated with approximately 45.23% of revenues in 2025.

Global middle class expansion bringing hundreds of millions of new denim consumers across emerging markets.

The denim market was valued at USD 78.90 billion in 2025.

The denim market is expected to grow at a CAGR of 6.61% from 2026 to 2035.

Get in Touch