Device as a Service Market Report Scope & Overview:

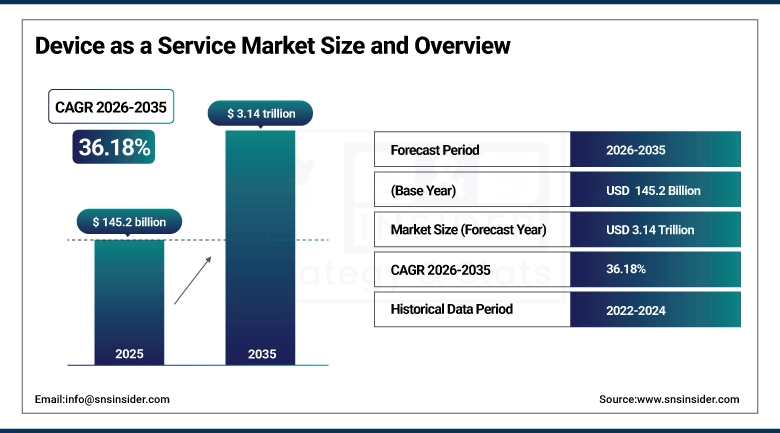

The Device as a Service Market size was valued at USD 145.2 billion in 2025 and is expected to reach USD 3.14 trillion by 2035, growing at a CAGR of 36.18% from 2026-2035.

The Devices as a Service (DaaS) Market is expected to expand as a result of higher adoption rates for remote working and hybrid working models, an increased need for more versatile IT infrastructure, and DaaS that can manage devices through subscriptions.

IDC's 2024 Device as a Service Buyer Survey documents that organizations using DaaS models report 32% reduction in total IT device management cost compared to traditional ownership models with endpoint security incident reduction (28%), deployment time reduction (45%), and employee productivity improvement (18%) as the most consistently cited operational benefits beyond cost savings.

Device as a Service (DaaS) Market Size and Forecast

-

Market Size in 2025: USD 145.2 Billion

-

Market Size by 2035: USD 3.14 Trillion

-

CAGR: 36.18% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Device as a Service Market - Request Free Sample Report

Device as a Service Market Trends

-

AI-powered endpoint management integrated into DaaS platforms is enabling predictive device failure detection, automated patch deployment, and self-healing remediation that resolves common software issues without human IT intervention.

-

Zero Trust security architecture integration with DaaS platforms is ensuring that every managed device meets continuous compliance requirements identity verification, endpoint health attestation, and behavioral analytics before accessing corporate network resources.

-

Sustainability reporting requirements are driving DaaS adoption as ESG-conscious organizations recognize that device lifecycle management through DaaS providers enables more environmentally responsible procurement, refurbishment, and certified disposal than internal device management typically achieves.

-

Hybrid work permanence is sustaining elevated DaaS demand: organizations that distributed laptops to work-from-home employees during 2020-2021 and then adopted permanent hybrid work policies have embedded the distributed device management challenges that DaaS most effectively addresses.

-

AI PC generation devices with dedicated neural processing units for on-device AI inference including Microsoft Copilot+ PCs and Apple Silicon-powered Macs is creating a hardware refresh cycle that DaaS providers are positioning as the optimal upgrade pathway for organizations whose existing fleet lacks AI PC capability.

U.S. Device as a Service (DaaS) Market Size Outlook:

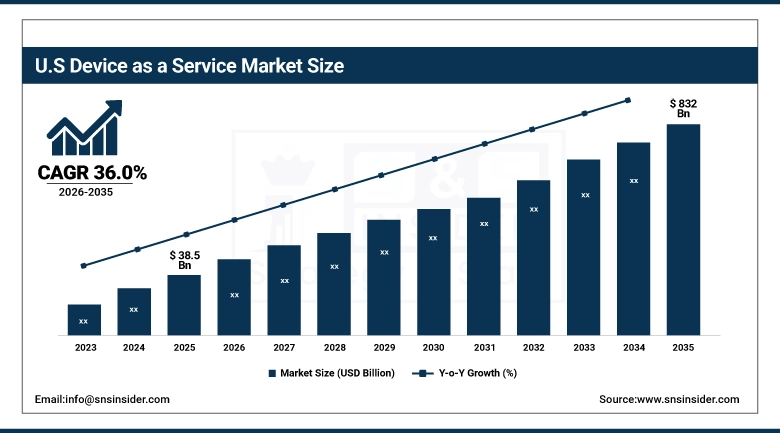

The U.S. Device as a Service (DaaS) Market was valued at USD 38.5 billion in 2025 and is expected to reach USD 832 billion by 2035, growing at a CAGR of 36.0% from 2026-2035.

The Device as a Service Market in the U.S. is witnessing high growth due to the prevalence of the hybrid work model, substantial spending by enterprises on IT services, and rising requirement for scalable subscriptions for managing devices. There has been an emphasis on cybersecurity, remote employee management, cost predictability, and lifecycle management of hardware.

Dell Technologies' APEX device subscription service launched in 2021 and expanded through 2024 — has enrolled over 2,000 enterprise customers representing over 400,000 devices under subscription management, demonstrating commercial validation of large-scale enterprise DaaS adoption beyond the SME segment that early DaaS services primarily targeted.

Device as a Service Market Segment Analysis

-

By Component, Hardware dominant historically; Software growing fastest driven by SaaS endpoint management platform adoption.

-

By Device Type, Desktop dominated with 38.8% share in 2025; Smartphone & Peripheral growing at fastest CAGR.

-

By Organization Size, Large Enterprise dominated in 2025; SME growing at fastest CAGR.

-

By End-Use Industry, IT & Telecom dominated with 24.7% share in 2025 and also growing at fastest CAGR.

By Component: Hardware dominant, Software growing fastest

Hardware has historically held the dominant component position in the Device as a Service Market reflecting the device hardware itself as the primary cost element in DaaS programs whose per-device monthly fee is anchored in the amortized hardware cost, financing interest, and residual value assumptions that determine the economics of the service provider's offering. DaaS hardware procurement by service providers who purchase devices in volume from Dell, HP, Lenovo, and Apple to bundle into subscription programs represents the most capital-intensive component of the DaaS value chain.

Software is growing at the fastest component CAGR, driven by the value-added software layer that differentiates competitive DaaS offerings above commodity hardware subscription. Endpoint management platforms (Microsoft Endpoint Configuration Manager, Jamf for Apple devices, VMware Workspace ONE), security suites (Microsoft Defender for Endpoint, CrowdStrike Falcon), and productivity software licensing (Microsoft 365, Google Workspace) bundled within DaaS subscription programs create software revenue that compounds with hardware subscription base.

By Device Type: Desktop dominates, Smartphone & Peripheral growing fastest

Desktop computers held approximately 38.8% of the Device as a Service Market in 2025, reflecting the large installed base of desktop computing in enterprise environments particularly in finance, healthcare, and manufacturing where the stationary workstation remains the primary computing interface for intensive applications requiring large displays, high processing power, and continuous power availability that portable devices cannot match. Enterprise desktops in corporate headquarters, bank branch networks, hospital nursing stations, and factory floor workstations represent a stable large-population device category whose management complexity software configuration, security patching, peripheral device management makes DaaS service model economics compelling for IT organizations whose helpdesk capacity is consumed by routine desktop support tasks.

The Smartphone and Peripheral segment is growing at the fastest device type CAGR, driven by the enterprise mobile device management market's evolution from basic MDM (Mobile Device Management) toward full device lifecycle service for corporate smartphones and tablets. Corporate smartphone programs whose lifecycle management carrier plan management, app deployment, security policy enforcement, lost device replacement, and end-of-life trade-in is bundled into per-device monthly fees represent the smartphone DaaS market segment that is growing fastest as organizations recognize that employee smartphones' management complexity mirrors corporate laptop management but has historically been handled less systematically.

By End-Use Industry: IT & Telecom dominates and grows fastest

IT and Telecommunications held approximately 24.7% of the Device as a Service Market in 2025 and is simultaneously projected to grow at the fastest end-use industry CAGR a dual-dominant-and-fastest-growing position that reflects the IT sector's self-adoption of the service models it sells to other industries and the telecom sector's integration of DaaS with its managed connectivity services. Technology companies' adoption of DaaS for their own employee device fleet reflects the logical consistency of SaaS-first software companies whose technology procurement philosophy favors subscription models across all technology categories including the devices on which their employees run their SaaS applications.

The BFSI (Banking, Financial Services, and Insurance) sector is a major DaaS end-user whose adoption is driven by the combination of large device fleets, stringent security compliance requirements, and the operational efficiency mandate that financial institution CEOs and CFOs apply to technology spending. Global banks whose employee device fleets span thousands of branch locations, trading floors, and back-office operations find DaaS's centralized management, automatic security patching, and compliance documentation particularly valuable for regulatory examination purposes. Healthcare is a rapidly growing DaaS end-use as hospital system IT departments whose clinical device management challenges infection control between device users, frequent software update requirements for clinical applications, and the high cost of clinical device downtime find DaaS service models address multiple operational challenges simultaneously.

Device as a Service Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

85% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

China |

40% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

North America DaaS Market Insights

North America dominated the global DaaS Market, led by the United States whose combination of large enterprise IT budgets, managed service provider ecosystem density, and subscription-first technology procurement culture creates the world's most commercially developed DaaS market. The U.S. market's DaaS maturity is reflected in the competitive intensity of its supply side: Dell Technologies, HP Inc., Lenovo, Apple (through certified reseller programs), Microsoft (through Surface-as-a-Service), and hundreds of managed service provider intermediaries all compete for enterprise DaaS contracts a competitive density that sustains service innovation and price efficiency above markets with fewer competing providers. U.S. government DaaS adoption including DoD's IT-as-a-Service initiatives and federal civilian agency modernization programs provides large public sector contract volumes that sustain DaaS provider scale beyond the private sector alone.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific DaaS Market Insights

Asia Pacific is the fastest-growing regional DaaS Market, driven by Japan's enterprise IT modernization programs, China's growing enterprise software adoption, India's rapidly expanding IT services sector, and South Korea's technology-forward corporate culture. Japan's corporate digital transformation driven by the government's Digital Agency mandate to modernize government and corporate IT systems is creating DaaS demand at Japanese organizations whose technology procurement was historically biased toward perpetual license and owned hardware models that are now transitioning toward subscription models. India's IT services sector whose multinational clients increasingly mandate DaaS-compatible device management standards is adopting DaaS for both internal IT management and as a capability to offer clients whose device management they support as part of managed IT service contracts.

Europe DaaS Market Insights

Europe's DaaS Market is growing with GDPR compliance creating demand for managed device security that DaaS providers' centralized policy enforcement and audit documentation capabilities address more systematically than unmanaged corporate device programs. Germany, France, the UK, and the Nordic countries are primary markets, where sophisticated enterprise IT organizations and public sector digital modernization programs are creating DaaS procurement at meaningful scale. The European Investment Bank's digital infrastructure lending program which provides favorable financing for digital transformation investments including managed device programs is accelerating DaaS adoption by reducing the capital cost barrier for mid-market European companies whose DaaS interest has been constrained by transition cost rather than operational conviction.

MEA and Latin America DaaS Market Insights

The Middle East's DaaS Market is growing with the Gulf states' government digitalization programs and the region's growing enterprise IT adoption as economic diversification creates private sector organizations whose technology infrastructure requirements mirror developed market peers. Saudi Arabia's NEOM project and UAE's digital economy initiatives are creating corporate entities whose technology procurement from inception favors as-a-service models rather than the capital-intensive owned infrastructure models that existing organizations built around. Latin America's DaaS market is growing in Brazil and Mexico, where multinational company regional headquarters are standardizing device management practices across their global operations creating DaaS adoption that follows global corporate IT policy rather than local market preference.

Device as a Service Market Growth Drivers:

-

Subscription IT economics and hybrid work permanence driving extraordinary device as a service market growth globally

The increase in preference towards subscription models in the IT world and the permanency of hybrid work environments is one of the key drivers that will fuel the growth of the global Device as a Service (DaaS) Market. Businesses are opting for subscription-based business models by making an investment in the form of a subscription that covers not only devices but also software, support, security, and device management among others. This model ensures better cost-efficiency and budgeting. In addition, due to hybrid working models, there is an increase in demand for devices that allow for more flexibility in their deployment to ensure that employees are productive and secure while working remotely. DaaS vendors are able to upgrade devices easily while ensuring proper monitoring and maintenance.

Device as a Service Market Restraints:

-

Data security concerns and contract flexibility limitations creating device as a service market adoption friction globally

DaaS adoption is constrained by security concerns that arise from the managed service model's fundamental architecture: the DaaS provider has administrative access to the organization's device fleet for management purposes, creating a potential data access exposure that security-sensitive organizations find incompatible with their data governance policies. Financial institutions whose client financial data resides on managed devices, healthcare organizations whose devices process PHI protected under HIPAA, and defense contractors whose devices contain classified or controlled unclassified information each face security review processes for DaaS provider access that add procurement complexity and sometimes result in rejection of DaaS commercial proposals. Contract flexibility where multi-year DaaS commitments are commercially necessary for provider economics but constrain organizational flexibility to change device types, user counts, or service levels creates switching cost lock-in that requires careful contract negotiation.

Device as a Service Market Opportunities:

-

AI PC refresh cycle and IoT device management expansion creating transformative device as a service market growth globally

The AI PC generation Microsoft's Copilot+ PCs, Apple's M-series MacBooks, and Qualcomm Snapdragon X-powered thin clients whose dedicated neural processing unit hardware enables on-device AI inference represents a hardware refresh cycle that DaaS providers are positioning as the optimal delivery mechanism for AI-PC capability access. Organizations whose existing device fleets were purchased before AI PC hardware generation want to provide employees with AI PC capability on-device Copilot, real-time transcription, AI-assisted content creation without committing capital to a hardware generation whose AI application landscape is still developing. DaaS programs whose subscription structure enables AI PC access without capital commitment address precisely this organizational need, creating a new technology refresh driver that sustains DaaS demand above the baseline replacement cycle economics.

Recent Developments:

-

2026: Dell Technologies expanded its APEX PC-as-a-Service offering with integrated AI endpoint analytics that predict device failure probability 30 days in advance with 87% accuracy enabling proactive device replacement scheduling that eliminates the productivity loss of unexpected device failures during active work periods with Dell reporting 40% reduction in unplanned device downtime events at the 50 enterprise accounts piloting the predictive replacement program before full commercial launch.

-

2025: HP Inc. launched its HP Device as a Service with built-in sustainability reporting automatically generating quarterly ESG compliance documentation covering device procurement carbon footprint, refurbishment rates for returned devices, and certified e-waste disposal documentation targeting the growing segment of enterprise DaaS buyers whose CSR reporting requirements mandate electronics lifecycle documentation that internal IT programs cannot systematically provide.

Device as a Service (DaaS) Companies are:

-

Dell Technologies Inc. (APEX)

-

HP Inc. (HP Device as a Service)

-

Apple Inc.

-

Microsoft Corporation (Surface as a Service)

-

Cisco Systems Inc.

-

CDW Corporation

-

Insight Direct Inc.

-

Connection (PC Connection Inc.)

-

Computacenter plc

-

Bechtle AG

-

Logicalis Group

-

Tangoe Inc.

-

Jamf Holding Corp.

-

VMware Inc. (Workspace ONE)

-

Ivanti Software Inc.

-

Absolute Software Corp.

-

Managed Way LLC

-

Axios Systems Ltd.

Device as a Service Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 145.2 Billion |

| Market Size by 2035 | USD 3144 Billion |

| CAGR | CAGR of 36.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Device Type (Desktop, Laptop, Smartphone & Peripheral, Others) • By Organization Size (Large Enterprise, SME) • By End-Use Industry (IT & Telecom, BFSI, Healthcare, Retail, Education, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Dell Technologies Inc. (APEX), HP Inc. (HP Device as a Service), Lenovo Group Ltd., Apple Inc., Microsoft Corporation (Surface as a Service), Cisco Systems Inc., CDW Corporation, Insight Direct Inc., SHI International Corp., Connection (PC Connection Inc.), Computacenter plc, Bechtle AG, Logicalis Group, Tangoe Inc., Jamf Holding Corp., VMware Inc. (Workspace ONE), Ivanti Software Inc., Absolute Software Corp., Managed Way LLC, Axios Systems Ltd. |

Frequently Asked Questions

Ans: SMEs are growing at the fastest CAGR; Large Enterprise dominated in 2025.

Ans: The Device as a Service Market was valued at USD 145.2 billion in 2025.

Ans: IT & Telecom dominated with approximately 24.7% share and is also growing at the fastest CAGR.

Ans: Desktop dominated with approximately 38.8% share; Smartphone & Peripheral is growing at the fastest CAGR.

Ans: The Device as a Service Market is expected to grow at a CAGR of 36.18% from 2026 to 2035.

Get in Touch