Diabetic Ketoacidosis Treatment Market Report Scope & Overview:

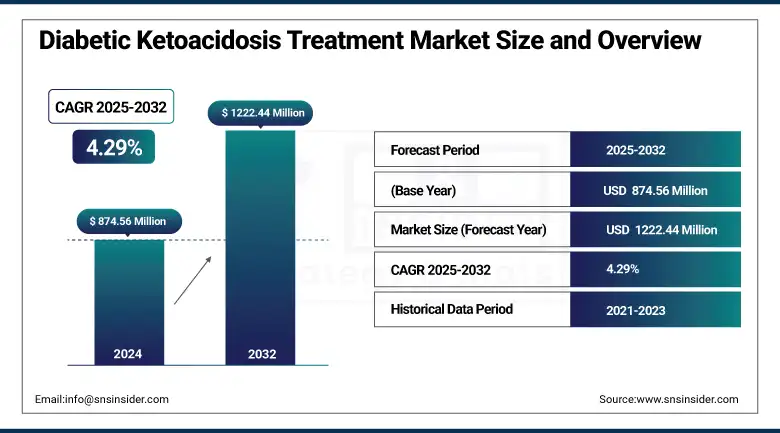

The diabetic ketoacidosis treatment market size was valued at USD 874.56 million in 2024 and is expected to reach USD 1222.44 million by 2032, growing at a CAGR of 4.29% over 2025-2032.

The diabetic ketoacidosis treatment market is an emerging market due to factors, such as increasing prevalence of diabetes, growing number of hospital admissions with acute diabetic complications, and raised awareness of early intervention and emergency care. Increasing prevalence of patients with type 1 diabetes and uncontrolled type 2 diabetes has been driving demand for rapid-acting insulin, fluid, and electrolyte treatments, and continuous glucose monitoring devices. The development of insulin delivery and blood ketone measuring technologies is also improving patient outcomes, which is also propelling the diabetic ketoacidosis treatment market.

In April 2025, Eli Lilly declared their extended clinical trials to create an ultra-rapid insulin for the treatment of acute episodes of DKA, highlighting continuous product innovation in the diabetic ketoacidosis treatment market analysis.

To Get more information On Diabetic Ketoacidosis Treatment Market - Request Free Sample Report

In addition, growing investment in healthcare infrastructure and emergency care centers, especially in developing countries, is enhancing access and affordability, thereby boosting diabetic ketoacidosis treatment market growth. Many DKA treatment companies are focusing on R&D for a new generation of insulin formulations and portable apps. Support from regulatory bodies, including the FDA, for fast-track approvals of new insulin analogs is boosting product accessibility and will spur the diabetic ketoacidosis treatment market share and help in improving patient outcomes. Larger companies, such as Novo Nordisk, Eli Lilly, and Sanofi are pouring millions of dollars into alternative methods of delivery and combination treatments in the hope of establishing the future directions of the global diabetic ketoacidosis market. This, along with increasing cooperation by pharmaceutical companies and research institutes, has increased both the demand and supply spread across regions.

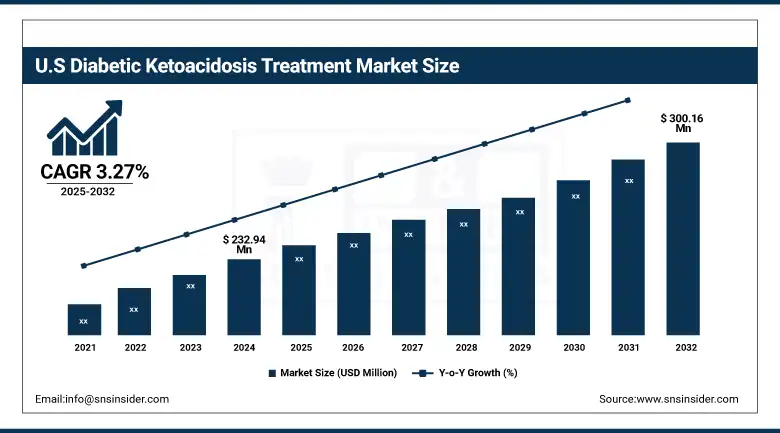

The U.S. diabetic ketoacidosis treatment market size was valued at USD 232.94 million in 2024 and is expected to reach USD 300.16 million by 2032, growing at a CAGR of 3.27% over 2025-2032. The U.S. is the frontrunner in the region, with strong healthcare expenditure and early uptake of expensive technology. According to the CDC, the U.S. reported over 188,000 DKA-related hospitalizations in 2023, highlighting the urgency of treatment demand. Canada is also notable in terms of presence, based on increasing impacting cases of type 1 diabetes, and increased government funding for access to insulin and continuous glucose monitors. Access to emergency diabetes care is slowly on the rise with national health initiatives in Mexico, but with ongoing disparities. Robust regulatory backing from the USFDA and the availability of key market players, Eli Lilly and Novo Nordisk, in the U.S. are other factors that facilitate the region’s stronghold over the market.

In May 2025, Novo Nordisk collaborates with hospitals in Southeast Asia to train AI models to predict blood glucose and ketone readings, demonstrating regional investments and the integration of technology. These developments highlight the changes in the diabetic ketoacidosis treatment market trends and are indicative of growth drivers, such as innovation and regulatory facilitation, and demand expansion at the global level.

Table: Regulatory Approvals Related to DKA Treatment (2022–2025)

|

Year |

Product/Device |

Company |

Region |

Approval Authority |

Indication/Impact |

|

2022 |

Lyumjev (Insulin Lispro-aabc) |

Eli Lilly |

U.S. |

FDA |

Faster insulin absorption |

|

2023 |

FreeStyle Libre 3 |

Abbott |

EU, U.S. |

EMA/FDA |

CGM for DKA-risk patients |

|

2024 |

Basalog One (biosimilar) |

Biocon |

India |

CDSCO |

Cost-effective insulin therapy |

|

2025 |

Control-IQ+ Closed-Loop System |

Tandem Diabetes |

U.S. |

FDA |

Automated insulin delivery |

Market Dynamics:

Drivers:

-

Rising Diabetes Burden, Increased Emergency Admissions, and Therapeutic Advancements are Significantly Driving the Diabetic Ketoacidosis Treatment Market

The diabetic ketoacidosis treatment market is mainly driven by the increasing incidence of diabetes globally, particularly among youth and middle-aged groups. As the International Diabetes Federation estimates, more than 1.2 million children and adolescents have type 1 diabetes, which represents a main risk group for DKA. Rising admissions for poor glucose control and insulin treatment delays are also driving the treatment requirements. In 2024, the American Diabetes Association reported a year-over-year 7% rise in emergency-room visits associated with DKA. On the supply side, drugmakers are speeding up insulin innovation and increasing the scale of production to keep up with demand. Indeed, portable ketone monitors and infusion pumps are on the rise.

For instance, Abbott in 2024 devoted USD 100 million to R&D investment in its next-gen biosensor-based monitoring platform. The favorable reimbursement, the protocol for emergency care, and acceptance for new types of insulins and insulin analogs, and combination therapies by the U.S. FDA are also driving the market to grow.

Recommendations by professional bodies, such as NICE (U.K.) and the ADA (U.S.) harmonize procedures, which in turn lead to enhanced patient safety and compliance with treatment. The cumulation of these factors is driving the expansion of the diabetic ketoacidosis treatment market, paving the way for even more product innovation and increasing adoption.

Restraints:

-

Several Barriers Hinder the Diabetic Ketoacidosis Treatment Market Including High Treatment Costs and Limited Awareness in Low-Resource Settings

High cost of insulin therapies and advanced monitoring devices, which are beyond the reach of patients, especially in low- and middle-income regions, are a major barrier in the diabetic ketoacidosis treatment market. In those countries where there is no generic competition, the insulin price imposes a low level of access to timely treatment.

In 2024, the RAND Corporation reported that the U.S. insulin prices were, on average, almost 8 times higher than in 32 other high-income countries, resulting in treatment delays and recurrent DKA episodes.

Furthermore, ignorance amongst the diabetics regarding early symptoms of DKA often leads to late-stage complications, thereby creating a greater risk of mortality. Trade restrictions can also exacerbate supply-chain disruptions that create difficulties for insulin, which depends on a cold chain, especially in rural and insecure places. Furthermore, the global diabetic ketoacidosis treatment market is confronted by challenges, such as regulation and logistical difficulties in implementing new therapies in fragmented health systems. The approval process for biosimilars and newer insulin combinations is hindered by regulatory hurdles in some countries. Additionally, the absence of standardized emergency care precludes efficient utilization of available resources. These limitations hinder market and patient care in diabetic ketoacidosis, particularly among underserved populations, emphasizing the requirement of global health equity efforts and subsidized access initiatives.

Segmentation Analysis:

By Type

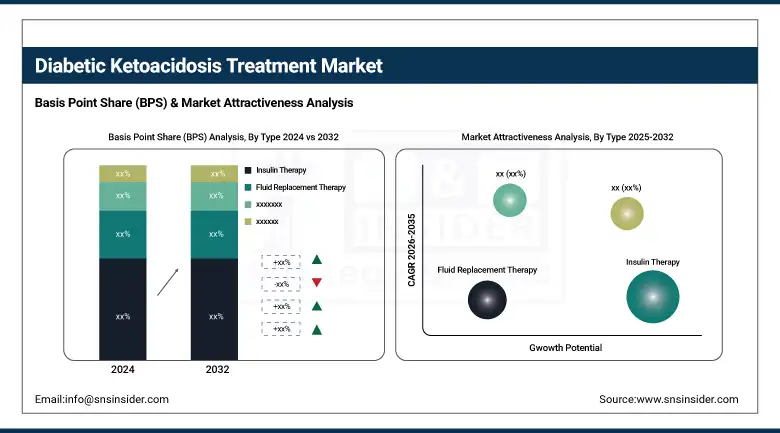

In 2024, insulin therapy led the diabetic ketoacidosis treatment market with a revenue share of 29.02% due to its vital function of reversing hyperglycemia and inhibiting ketogenesis in DKA attacks. Consideration also needs to be given to the dominance of rapid-acting insulin analogs and growing physician favor of IV insulin in the acute care setting, which is likely to have a major impact in this regard. Moreover, developments in insulin formulations and apparatuses for continuous infusion have furnished their widespread use in acute care settings and follow-up care.

The ‘Others’ category, which consists of new treatments including bicarbonate therapy, adjuncts in infection-related DKA, and research-based treatments, is the category with the highest growth rate. Emerging research focuses on addressing precipitating causes and comorbidities of DKA, and off-label use of adjunctive therapy, which is influencing this broadening application. Novel protocols and individualized combinations are also driving the diabetic ketoacidosis treatment market growth of this category.

By End-User

The hospital segment dominated the diabetic ketoacidosis treatment market by end-user market and accounted for 75.56% share of the market in 2024. Their predominance is based on DKA being a medical emergency with the necessity of frequent surveillance, intravenous treatment, and regular medical intervention, which are usually available in hospital wards. Due to the presence of ICU, ED, and trained endocrinologists, a good and systematic management characterized by the low mortality rate and the fact that ministrations are in hospitals, which are the main centres of treatment for the DKA patients.

At the same time, home care is the end-user segment that is growing most rapidly. Rising use of blood glucose monitoring devices at patients' homes, better patient education, and increasing investment in home-care infrastructure are helping patients to control the early signs of DKA at home. This has been reinforced additionally by considerations about post-hospital discharge care and the availability of telemedicine consultations. With healthcare transitioning towards the deinstitutionalization of care, home-based care for stable, recurrent DKA patients is emerging.

Regional Analysis:

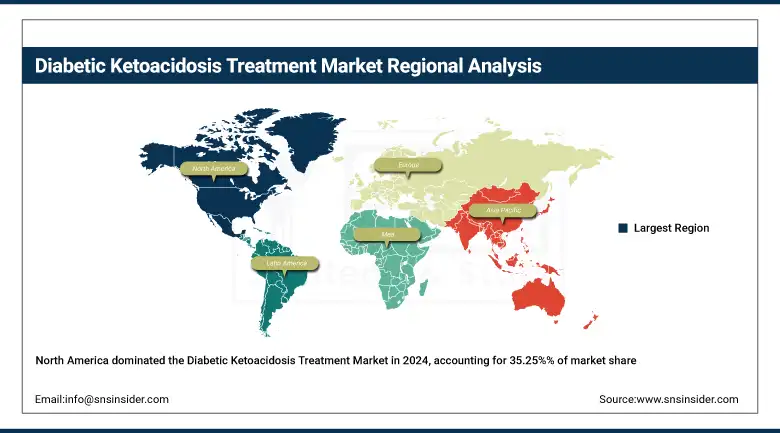

The diabetic ketoacidosis treatment market was led by North America in 2024, accounting for 35.25% of the market share due to the high prevalence of diabetes, developed healthcare infrastructure, and high acceptance rate of insulin therapies and emergency care protocols in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe holds a significant market share of diabetic ketoacidosis treatment owing to its well-developed healthcare system, government initiatives, and increasing focus on diabetes management.

Germany held the regional market for insulin pump DKA treatment with a major diabetic population and national funding of insulin pumps and DKA services. For Germany, there was a 3.5% increase in DKA hospitalizations in 2023 in young adults (Robert Koch Institute). The U.K. and France, as well, are leading contributors on account of the adoption of digital diabetes care platforms and national early screening programs. Conversely, among the remaining five Eastern European countries, Poland has the highest growth, as does the sub-region Turkey, due to better diabetes healthcare access and more investments in diabetes-related emergency care. The rapid diabetic ketoacidosis treatment market growth is also supported by harmonized EU regulations and joint research funding across member countries.

The Asia Pacific region is expected to grow at the highest CAGR in the diabetic ketoacidosis treatment market during the forecast period. The growth of this market segment can be attributed to the rising number of diabetics, greater focus on healthcare spending, and growing use of point-of-care testing techniques and insulin products.

India is at the forefront of this growth curve, with more than 77 million people with diabetes and a rapidly expanding burden of DKA resulting from suboptimal glycemic control and limited access to care in rural areas. Government schemes, such as the Ayushman Bharat and the National Digital Health Mission, are promoting early diagnosis and hospitalizations for acute diabetic complications. China is booming too, with AI-based glucose monitoring being pursued through state-driven investment and locally produced insulin. In 2023, the Chinese health ministry authorized two native made insulin biosimilars for the treatment of DKA, increasing access and affordability. Both Japan and South Korea are focusing on home-based care and the use of telehealth, further fueling market growth. Growth of the region is influenced by heightened onsets based on urbanization-related shifts in lifestyle and increasing medical technology penetration.

The Middle East & Africa (MEA) region is currently smaller but growing the fastest, driven by increasing diabetes rates, urbanization, and increased access to healthcare. The Saudi Arabian market is the largest, with high levels of obesity and diabetes in adults. A report in 2023 from the Saudi Ministry of Health showed an increase of 6.7% of ER visits for DKA between the years 2021 and 2022.

Table: Competitive Benchmarking of Key Players (2024 Snapshot)

|

Company |

Global Presence |

Product Range |

DKA Portfolio Strength |

Recent Innovation (2024–25) |

|

Novo Nordisk |

80+ Countries |

High |

Strong |

Smart pen with dose memory |

|

Eli Lilly |

70+ Countries |

Medium-High |

Strong |

Ultra-rapid Lispro trials |

|

Sanofi |

65+ Countries |

Medium |

Moderate |

Insulin biosimilar expansion |

|

Baxter |

50+ Countries |

High (IV) |

Moderate |

Enhanced electrolyte therapy |

|

Abbott |

60+ Countries |

High (Monitoring) |

Moderate |

Libre ketone sensor dev. |

Key Players:

Leading diabetic ketoacidosis treatment companies operating in the market comprise Novo Nordisk, Eli Lilly and Company, Sanofi, Pfizer, Baxter International, B. Braun Melsungen, Hikma Pharmaceuticals, Teva Pharmaceuticals, Fresenius Kabi, and Biocon.

Recent Developments:

-

In Feb 2025, the U.S. Food and Drug Administration approved insulin aspart‑szjj, representing the first short-acting biosimilar insulin for the treatment of diabetes.

-

In Feb 2025, Tandem launched the Tandem Mobi pump featuring Control‑IQ+ technology in the U.S. The first compact AID system with mobile app control and automated correction boluses, this launch marks a paradigm shift toward the prevention of DKA and lifelong wireless continuous diabetes care.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 874.56 million |

| Market Size by 2032 | USD 1222.44 million |

| CAGR | CAGR of 4.29% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Fluid Replacement Therapy, Electrolyte Replacement Therapy, Insulin Therapy, and Others) • By End User (Hospitals, Ambulatory Surgical Centers (ASCs), and Homecare Settings) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Novo Nordisk, Eli Lilly and Company, Sanofi, Pfizer, Baxter International, B. Braun Melsungen, Hikma Pharmaceuticals, Teva Pharmaceuticals, Fresenius Kabi, and Biocon. |

Frequently Asked Questions

Ans: Emerging diabetic ketoacidosis treatment market trends include AI-powered ketone monitoring devices and integrated insulin delivery systems for critical care in diabetes.

Ans: Major diabetic ketoacidosis treatment companies include Novo Nordisk, Eli Lilly, Sanofi, Baxter, and B. Braun, all investing in critical care innovations.

Ans: The U.S. diabetic ketoacidosis treatment market leads globally, while Asia Pacific is the fastest-growing due to expanding healthcare infrastructure for diabetes.

Ans: Key drivers include the rising global diabetes burden, increased use of insulin infusion therapy, and rapid adoption of point-of-care diagnostics in emergency care.

Ans: The diabetic ketoacidosis treatment market size was valued at approximately USD 874.56 million in 2024, driven by the increasing incidence of hyperglycemia complications and emergency diabetes care demand.

Get in Touch