Patient Access Solutions Market Size Analysis:

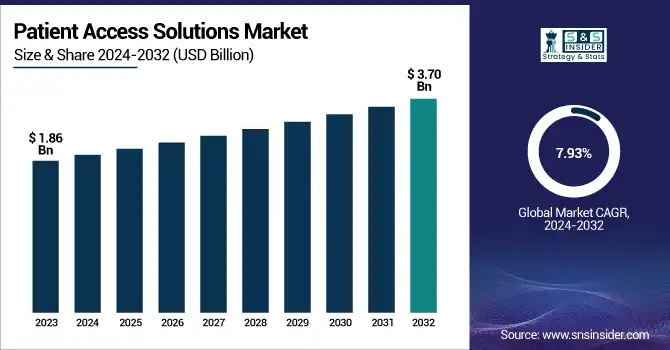

The Patient Access Solutions Market Size was valued at USD 1.86 Billion in 2023 and is expected to reach USD 3.70 Billion by 2032, growing at a CAGR of 7.93% over the forecast period of 2024-2032.

Get more information on Patient Access Solutions Market - Request Sample Report

The Patient Access Solutions Market is evolving rapidly, fueled by rising investments in AI-driven and cloud-based technologies. Investment and funding trends reveal increasing capital flow into automation and interoperability, while patent analysis highlights innovations shaping seamless healthcare access. Enhancing patient engagement and satisfaction levels remains a priority, driving demand for efficient scheduling and verification systems. End-user spending trends indicate a shift toward digital transformation, with hospitals prioritizing seamless workflows. Evaluating return on investment (ROI) for hospitals and clinics is crucial, as providers seek cost-effective solutions. Meanwhile, healthcare provider budget allocations reflect growing investments in digital infrastructure to ensure efficiency and compliance. Our report explores these key dynamics, offering a comprehensive market perspective.

Patient Access Solutions Market Dynamics

Drivers

-

Rising Integration of Blockchain Technology in Patient Access Solutions Enhances Data Security and Transparency

The integration of blockchain technology in patient access solutions is addressing critical challenges related to data security, interoperability, and transparency. Blockchain ensures tamper-proof data storage, reducing the risk of fraudulent activities and unauthorized access to patient records. With increasing concerns over data breaches in healthcare, blockchain-based solutions provide a decentralized and secure platform for managing patient data efficiently. Additionally, blockchain enhances interoperability by enabling seamless data sharing between healthcare providers, insurers, and patients, improving coordination in care delivery. The demand for transparent and secure transactions in the healthcare sector is accelerating the adoption of blockchain-based patient access solutions. As regulatory frameworks evolve to support blockchain integration, healthcare organizations are increasingly exploring its potential to enhance patient trust and compliance. Furthermore, blockchain-powered smart contracts are automating various administrative processes, such as insurance claims processing and patient consent management, improving overall efficiency. The growing collaboration between healthcare technology firms and blockchain service providers is also fostering innovation in patient access solutions.

Restraints

-

Concerns Over Data Privacy and Compliance Regulations Limit the Adoption of Digital Patient Access Solutions

Stringent data privacy regulations, such as HIPAA in the United States and GDPR in Europe, pose challenges to the widespread adoption of digital patient access solutions. Healthcare organizations must ensure compliance with these regulations while managing vast amounts of sensitive patient data. Any security breach or non-compliance can result in significant legal and financial repercussions, discouraging providers from adopting new digital solutions. Additionally, patient concerns regarding data privacy and unauthorized access to personal health information create hesitation in using digital platforms. The complexity of navigating compliance requirements across different regions further limits the seamless implementation of patient access solutions globally. Moreover, the growing adoption of cloud-based solutions raises additional security concerns, as cyberattacks and data breaches become more sophisticated. Healthcare providers must invest in robust cybersecurity measures, such as encryption and multi-factor authentication, to mitigate risks and ensure patient trust.

Opportunities

-

Expansion of Telehealth and Remote Patient Monitoring Creates New Growth Avenues for Patient Access Solutions Market

The rapid expansion of telehealth and remote patient monitoring services is opening new opportunities for patient access solutions. With the growing preference for virtual consultations, healthcare providers are investing in digital platforms that enable seamless patient onboarding, appointment scheduling, and remote access to medical records. Telehealth adoption has accelerated post-pandemic, driving the demand for integrated patient access solutions that support virtual care models. Additionally, remote patient monitoring tools require efficient data exchange between patients and healthcare providers, further necessitating advanced patient access platforms. As telehealth regulations continue to evolve, healthcare organizations are focusing on enhancing digital accessibility, paving the way for market growth. Furthermore, the integration of artificial intelligence (AI) and wearable technology is improving the accuracy and efficiency of remote patient monitoring. Healthcare providers are also leveraging cloud-based platforms to enable real-time access to patient data, enhancing decision-making and care coordination.

Challenge

-

Resistance to Digital Transformation Among Healthcare Providers Slows Down the Adoption of Patient Access Solutions

Despite the benefits of digital patient access solutions, resistance to technological change among healthcare providers remains a key challenge. Many hospitals and clinics continue to rely on traditional administrative processes, fearing operational disruptions during the transition to digital platforms. Limited technical expertise and staff reluctance to adopt new systems further hinder implementation efforts. Additionally, concerns about data security, system reliability, and interoperability issues contribute to hesitation in embracing digital transformation. Overcoming these challenges requires extensive training programs and robust change management strategies to encourage widespread adoption of patient access solutions. Furthermore, the reluctance of senior management to allocate sufficient budgets for IT upgrades is slowing down market penetration. Addressing these issues requires stronger collaboration between healthcare providers and technology vendors to ensure seamless integration and user-friendly system designs.

Patient Access Solutions Market Segmentation Analysis

By Offering

Software dominated the Patient Access Solutions Market in 2023 with a market share of 59.8%. Within this segment, Eligibility Verification emerged as the leading subsegment due to the increasing complexity of insurance policies and the growing emphasis on accurate pre-service financial clearance. The rising adoption of AI-driven solutions for real-time insurance verification by healthcare providers such as Epic Systems, Cerner (Oracle Health), and Change Healthcare has fueled this growth. Additionally, government initiatives like the Centers for Medicare & Medicaid Services (CMS) Interoperability and Prior Authorization Proposed Rule (2023) emphasize automation in eligibility verification, further driving market adoption. As hospitals and clinics seek to minimize claim denials and revenue losses, advanced software solutions integrating AI and machine learning are being widely implemented across healthcare networks.

By Delivery Mode

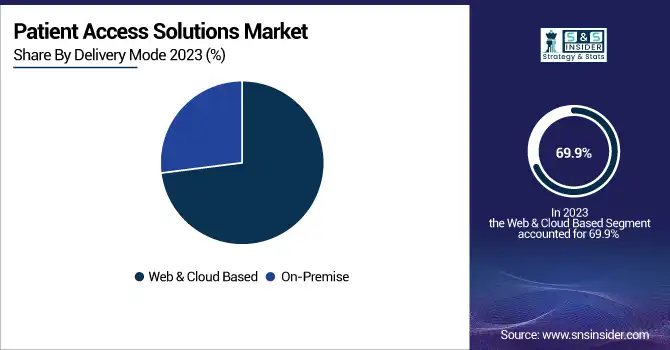

Web & Cloud-Based solutions dominated the Patient Access Solutions Market in 2023 with a market share of 69.9%. The dominance of this segment is driven by its scalability, cost-effectiveness, and ease of deployment, making it the preferred choice for hospitals, clinics, and large healthcare networks. The U.S. Department of Health and Human Services (HHS) has actively promoted cloud-based healthcare IT adoption to improve interoperability and patient data exchange. Major players such as Athenahealth, Allscripts, and Optum have expanded their cloud-based patient access platforms, allowing seamless integration with electronic health records (EHRs). Additionally, the Healthcare Information and Management Systems Society (HIMSS) has highlighted cloud-based solutions as a key enabler for enhancing patient engagement and reducing administrative burdens. The pandemic further accelerated cloud adoption, with healthcare providers prioritizing remote access to patient data and automated scheduling systems.

By End-User

Healthcare Providers dominated the Patient Access Solutions Market in 2023 with a market share of 45.4%. The growing need for efficient revenue cycle management, reduced administrative costs, and enhanced patient experience has driven hospitals, clinics, and outpatient facilities to invest in advanced patient access solutions. The American Hospital Association (AHA) and the Centers for Medicare & Medicaid Services (CMS) have emphasized the importance of digital patient access solutions to improve care coordination and reduce claim denials. Large hospital networks, including Mayo Clinic, Cleveland Clinic, and Kaiser Permanente, have adopted AI-powered patient access software to streamline eligibility verification, appointment scheduling, and prior authorizations. Additionally, the surge in patient volume post-pandemic has further fueled the demand for automated solutions that enhance operational efficiency and ensure compliance with evolving healthcare regulations.

Regional Insights

North America dominated the Patient Access Solutions Market in 2023 with a market share of 41.7%. The region's dominance is driven by the rapid digitalization of healthcare, favorable government initiatives, and the presence of key market players such as Optum, Cerner Corporation (Oracle Health), Epic Systems, and McKesson Corporation. The U.S. leads the market due to strong investments in healthcare IT infrastructure, stringent regulatory policies under the Health Insurance Portability and Accountability Act (HIPAA), and the 21st Century Cures Act, which mandates interoperability between healthcare providers. According to the Centers for Medicare & Medicaid Services (CMS), U.S. hospitals are increasingly adopting AI-driven patient access solutions to reduce administrative burdens and improve revenue cycle management. Canada is also experiencing significant adoption, with initiatives like the Pan-Canadian Interoperability Roadmap driving digital health transformation. The demand for cloud-based patient access solutions surged post-pandemic, leading to increased deployment across major healthcare networks.

Moreover, Asia Pacific emerged as the fastest-growing region in the Patient Access Solutions Market, with a significant CAGR during the forecast period. The region's growth is fueled by the increasing adoption of digital healthcare technologies, expanding healthcare infrastructure, and government-led initiatives promoting electronic health records (EHRs) and automated patient management solutions. China is leading the market due to its Healthy China 2030 strategy, which emphasizes digital health transformation and AI-driven healthcare IT adoption. According to the National Health Commission of China, over 80% of hospitals have implemented some form of digital patient access solutions. India is another major growth hub, with the Ayushman Bharat Digital Mission (ABDM) promoting interoperability and digital patient engagement platforms. Japan, backed by its Society 5.0 vision, is also investing heavily in healthcare automation, with hospitals adopting AI-powered eligibility verification and claims management software to streamline administrative processes.

Need any customization research on Patient Access Solutions Market - Enquiry Now

Patient Access Solutions Market Key Players

-

3M (M Modal Fluency for Coding, 3M 360 Encompass, 3M Health Data Management)

-

Allscripts Healthcare Solutions, Inc. (Allscripts Payerpath, Allscripts Revenue Cycle Management, Allscripts Practice Management)

-

Cognizant Technology Solutions Corporation (Trizetto Patient Access Solutions, Cognizant Health TranZform, Cognizant Intelligent Authorization)

-

Conifer Health Solutions (Conifer Patient Access Solutions, Conifer Revenue Cycle Solutions, Conifer Care Navigation)

-

Cerner Corporation (Cerner Registration Management, Cerner Eligibility & Coverage Verification, Cerner Revenue Cycle Management)

-

Cirius Group, Inc. (Cirius Eligibility Verification, Cirius Financial Clearance, Cirius Claim Management)

-

Craneware, Inc. (Trisus Patient Access, Chargemaster Toolkit, Trisus Claims Informatics)

-

Epic Systems Corporation (Epic Prelude, Epic Cadence, Epic Resolute)

-

Experian plc (Experian Health Patient Access, Experian eCare NEXT, Experian Revenue Cycle Management)

-

Genentech, Inc. (Genentech Access Solutions, Genentech MyPatientSolutions, Genentech Co-pay Programs)

-

Innovaccer Inc. (Innovaccer Health Cloud, Innovaccer Patient Relationship Management, Innovaccer Provider Network Management)

-

Kyruus (Kyruus ProviderMatch, Kyruus Patient Access Suite, Kyruus Connect)

-

McKesson Corporation (McKesson RelayHealth, McKesson Patient Access Solutions, McKesson Revenue Cycle Solutions)

-

MEDHOST (MEDHOST Enterprise Scheduling, MEDHOST Patient Access Solutions, MEDHOST Revenue Cycle Management)

-

Optum, Inc. (Optum One, Optum Eligibility & Claims Verification, Optum Financial Clearance)

-

Oracle Corporation (Oracle Health Revenue Cycle Management, Oracle Patient Access Solutions, Oracle Cloud Healthcare)

-

The SSI Group, LLC (SSI Access Management, SSI Claims Management, SSI Eligibility Verification)

-

TransUnion LLC (TransUnion ClearIQ, TransUnion Healthcare Eligibility Verification, TransUnion Revenue Cycle Solutions)

Recent Developments in the Patient Access Solutions Market

-

January 2025: Diatech Pharmacogenetics expanded its collaboration with Merck to enhance patient access to personalized medicine in the Middle East and Africa, improving RAS biomarker testing for colorectal cancer patients.

-

April 2024: CareMetx acquired PX Technology to streamline patient access to specialty medications, integrating digital solutions to reduce administrative burdens and improve efficiency.

-

April 2024: Kiosk Operators LLC (KO) acquired Wellmation to enhance healthcare and pharmaceutical access through advanced patient engagement solutions.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.86 Billion |

| Market Size by 2032 | USD 3.70 Billion |

| CAGR | CAGR of 7.93% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Offering (Services [Support & Maintenance, Training & Education, Implementation], Software [Eligibility Verification, Medical Necessity Management, Pre-Certification & Authorization, Claims Denial & Appeal management, Payments Estimation Software, Claims Payment Assessment Software]) •By Delivery Mode (Web & Cloud Based, On-Premise) •By End-User (Healthcare Providers, HCIT Outsourcing Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Optum, Inc., McKesson Corporation, Cerner Corporation, Epic Systems Corporation, Cognizant Technology Solutions Corporation, Experian plc, Conifer Health Solutions, Allscripts Healthcare Solutions, Inc., Oracle Corporation, 3M and other key players |

Frequently Asked Questions

Ans: North America dominates the Patient Access Solutions Market due to strong healthcare IT infrastructure and regulatory support.

Ans: In the Patient Access Solutions Market, the software segment leads, with eligibility verification as a key subsegment.

Ans: The Patient Access Solutions Market is seeing enhanced data security and interoperability through blockchain integration.

Ans: The Patient Access Solutions Market is driven by AI adoption, cloud-based technologies, and increasing digital transformation.

Ans: The Patient Access Solutions Market is expected to grow at a CAGR of 7.93% from 2024 to 2032.

Get in Touch