Endoscopes Market Report Scope & Overview:

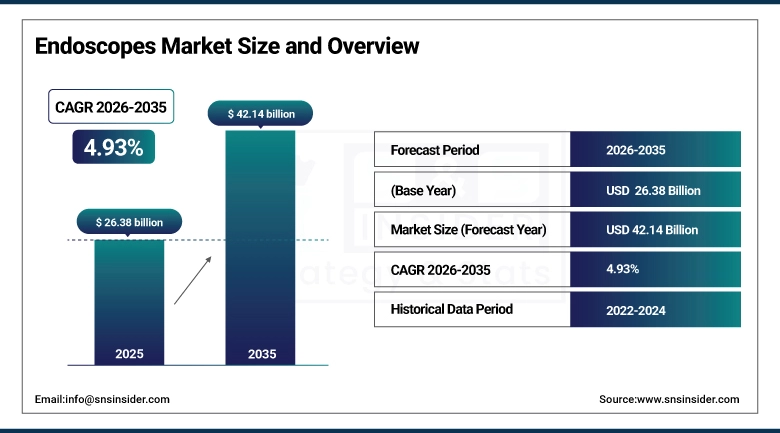

The Endoscopes Market was valued at USD 26.38 billion in 2025 and is expected to reach USD 42.14 billion by 2035, growing at a CAGR of 4.93% from 2026-2035.

The endoscope has been medicine's window into the body's interior for over a century, but what that window shows and what physicians can do while looking through it has changed almost beyond recognition in recent decades. Early rigid metal scopes offered a direct but limited field of view into body cavities accessible from natural orifices. Flexible fiberoptic endoscopes expanded the accessible anatomy dramatically, enabling visualization and biopsy throughout the gastrointestinal tract. Digital video endoscopes with high-definition chip-on-tip sensors, narrow band imaging, and AI-powered polyp detection brought the optical quality of endoscopy to television broadcast clarity. Capsule endoscopes freed the small intestine previously inaccessible to conventional endoscopy from diagnostic obscurity. Single-use digital flexible endoscopes are now challenging reusable designs' historical infection control advantages with devices that eliminate between-patient reprocessing entirely. At every stage, the market's growth has reflected a simple clinical logic: when physicians can see more clearly and intervene more precisely through minimally invasive approaches, patients benefit and demand for the enabling technology grows.

The American Cancer Society documents that colorectal cancer the primary clinical indication for colonoscopy screening is the second leading cause of cancer death in the United States, with the U.S. Preventive Services Task Force recommending screening colonoscopy beginning at age 45 for average-risk adults. The CDC's endoscopy capacity tracking data indicates that approximately 19 million colonoscopies are performed in the U.S. annually, making it the highest-volume endoscopic procedure category.

Endoscopes Market Size and Forecast

-

Market Size in 2025: USD 26.38 Billion

-

Market Size by 2035: USD 42.14 Billion

-

CAGR: 4.93% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Endoscopes Market - Request Free Sample Report

Endoscopes Market Trends

-

AI-powered polyp detection systems including Medtronic's GI Genius, Olympus's EndoBrain, and Fujifilm's CAD EYE are being integrated into colonoscopy workflows to reduce adenoma miss rates and provide documentation support.

-

Single-use flexible endoscopes are gaining regulatory clearance and clinical adoption for high-risk procedures where reusable endoscope reprocessing has been associated with cross-contamination incidents.

-

4K ultra-high-definition and 8K imaging capabilities are being incorporated into next-generation endoscope systems, providing surgical-quality visualization clarity for therapeutic endoscopy procedures.

-

Digital endoscope platforms with cloud connectivity enable real-time case sharing, remote expert consultation, and centralized procedure quality metrics tracking across hospital network endoscopy programs.

-

Robotic endoscopy systems including Medrobot and Invendoscopy platforms are entering clinical evaluation with the potential to improve colonoscopy completion rates and reduce operator skill variance.

-

Confocal laser endomicroscopy provides in vivo histological imaging during endoscopy, potentially enabling optical biopsy that reduces the need for tissue sampling in some clinical contexts.

-

Through-the-scope endoscopic submucosal dissection (ESD) techniques are expanding treatment of early gastrointestinal cancers that previously required open surgery, increasing procedure volumes and device complexity per case.

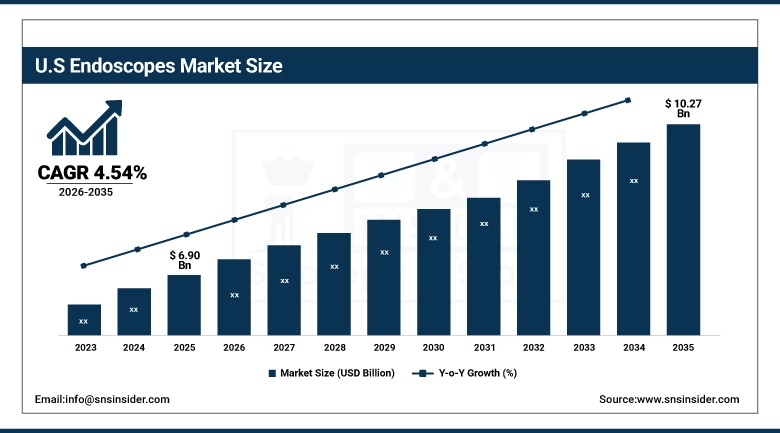

U.S. Endoscopes Market was valued at USD 6.90 billion in 2023 and is expected to reach USD 10.27 billion by 2032, growing at a CAGR of 4.54%.

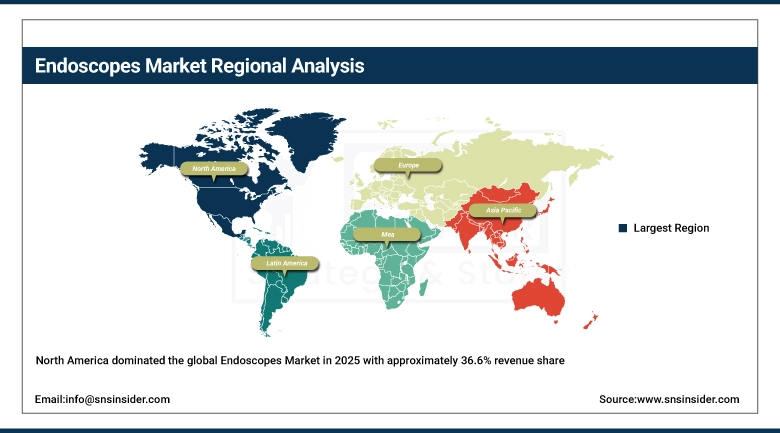

North America dominated the global Endoscopes Market with approximately 36.6% market share in 2025, driven by the United States' combination of one of the world's highest-volume gastrointestinal endoscopy programs driven by colorectal cancer screening mandates and colonoscopy quality metric tracking strong bronchoscopy and urologic endoscopy procedure volumes, and the advanced healthcare technology adoption culture that makes the U.S. the fastest market for innovation in endoscopy imaging and AI integration. Olympus America, Fujifilm Medical Systems, Karl Storz, and Johnson & Johnson's Ethicon endoscopy business all maintain substantial U.S. commercial operations that sustain deep hospital customer relationships. The U.S. regulatory environment with FDA-cleared AI endoscopy tools now available from Medtronic and Olympus has made the U.S. the global leader in clinical AI endoscopy deployment.

Medtronic's GI Genius AI colonoscopy assistance module received FDA clearance in 2021 and has been deployed across over 2,000 U.S. endoscopy centers, with clinical data from over 500,000 colonoscopies documenting a 40% increase in adenoma detection rate compared to standard colonoscopy without AI assistance. The Centers for Medicare & Medicaid Services' quality payment program includes colonoscopy adenoma detection rate as a reportable quality measure, creating institutional incentive for hospital endoscopy programs to invest in AI detection technology.

Endoscopes Market Segment Analysis

-

By Product, Flexible Endoscopes dominated the Endoscopes Market in 2025; Capsule Endoscopes growing fastest (CAGR).

-

By Usability, Reusable Endoscopes dominated with 83.3% share in 2025; Disposable Endoscopes fastest growing (CAGR).

-

By Application, Gastrointestinal dominated the Endoscopes Market in 2025; Respiratory and Urology growing steadily.

-

By End-User, Hospitals dominated the Endoscopes Market in 2025; Ambulatory Surgical Centers growing fastest.

By Product: Flexible Endoscopes dominate, Capsule growing fastest

Flexible Endoscopes held the dominant product position in the Endoscopes Market in 2025, reflecting the category's clinical versatility flexible endoscopes navigate the gastrointestinal tract's natural curves, the bronchial tree's branching anatomy, and the bladder's spherical interior in ways that rigid metal scopes cannot match. The upper GI endoscope (gastroscope), lower GI endoscope (colonoscope), bronchoscope, cystoscope, and ureteroscope are each flexible designs that serve their specific anatomical territories with specialized working channel diameters, tip deflection ranges, and illumination configurations optimized for the clinical tasks they must perform. Each major flexible endoscope platform from Olympus, Fujifilm, Karl Storz, or Pentax Medical requires a matching video processor, light source, and accessory ecosystem that creates vendor lock-in after initial platform investment, sustaining recurring equipment renewal and accessory revenue across multi-year customer relationships.

Rigid Endoscopes including laparoscopes, arthroscopes, hysteroscopes, and cystoscopes hold a significant market share in surgical endoscopy applications where the rigid optic delivers superior image quality compared to flexible alternatives and where the clinical setting (anesthestized patient in operating room) accommodates the rigid instrument's handling characteristics. Rigid endoscopes are the dominant instrumentation in laparoscopic abdominal surgery, arthroscopic joint surgery, and endoscopic sinus surgery each a high-volume surgical procedure category that sustains rigid endoscope market stability. Capsule Endoscopy where the patient swallows a vitamin-sized camera capsule that transmits wireless images as it traverses the gastrointestinal tract is the fastest-growing product segment, driven by growing adoption for small bowel disease surveillance, Crohn's disease monitoring, and celiac disease assessment in patients for whom conventional push enteroscopy is inconclusive.

By Usability: Reusable dominates at 83.3%, Disposable growing fastest

Reusable Endoscopes held approximately 83.3% of the Endoscopes Market in 2025, reflecting the established clinical and economic workflow that has been built around reusable high-definition endoscopy systems over decades of technology development and healthcare facility investment. A hospital endoscopy unit's reusable endoscope fleet typically 4-8 colonoscopes plus gastroscopes, bronchoscopes, and procedure-specific scopes represents capital investment of USD 500,000-1,000,000 that is amortized over 5–8-year equipment lifecycles with quarterly maintenance contracts and reprocessing supplies. This established infrastructure investment creates economic and workflow inertia that single-use endoscopes must overcome to achieve meaningful market share which they are beginning to do in specific application segments where reprocessing failure consequences are severe.

Disposable Endoscopes are the fastest-growing usability segment, driven by documented infection transmission incidents associated with inadequately reprocessed flexible endoscopes particularly duodenoscopes used for endoscopic retrograde cholangiopancreatography (ERCP) that have created patient safety concerns, hospital liability exposure, and regulatory scrutiny of endoscope reprocessing practices. The FDA's duodenoscope-related infection outbreak investigations and subsequent guidance recommending single-use duodenoscope evaluation have directly accelerated disposable endoscope adoption for this specific procedure type. Companies including Ambu, Boston Scientific (Exalt), Verathon, and Pentax Medical have each launched single-use flexible endoscopes targeting the ERCP, bronchoscopy, and cystoscopy applications where infection risk justification is strongest.

The FDA issued a safety communication in 2019 documenting over 700 adverse events from potentially contaminated reusable duodenoscopes between 2010 and 2019, with multidrug-resistant bacterial transmission the primary harm. This regulatory pressure directly drove hospital adoption of single-use duodenoscopes, with Ambu's aScope Duodeno gaining U.S. adoption across over 400 hospital systems within three years of clearance.

By Application: Gastrointestinal dominates, Respiratory and Urology growing

Gastrointestinal applications maintained the dominant position in the Endoscopes Market in 2025, encompassing the colonoscopy screening programs, diagnostic upper GI endoscopy, therapeutic ERCP, and advanced endoscopic mucosal resection and submucosal dissection procedures that collectively represent the world's highest-volume endoscopic procedure category. Colorectal cancer screening alone with colonoscopy recommended every 10 years for average-risk adults beginning at age 45 in the U.S. creates a massive recurring procedure demand that sustains colonoscope fleet utilization and accessories revenue. The quality metrics program that tracks adenoma detection rate, bowel preparation quality, and cecal intubation rates across U.S. endoscopy programs creates institutional incentive for continuous capital investment in higher-quality imaging technology.

Respiratory endoscopy bronchoscopy and endobronchial ultrasound (EBUS) for lung cancer staging and peripheral pulmonary lesion biopsy is growing as lung cancer screening programs expand and as bronchoscopic navigation systems including Monarch (Auris Health, J&J) and Ion (Intuitive Surgical) enable biopsy of peripheral pulmonary nodules that conventional bronchoscopy cannot access. Urological endoscopy cystoscopy, ureteroscopy, and percutaneous nephoscopy for bladder cancer surveillance, kidney stone fragmentation, and ureteral pathology sustains substantial annual procedure volumes driven by bladder cancer's high recurrence rate requiring regular surveillance cystoscopy.

Endoscopes Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

89% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

Japan |

38% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

50% |

North America Endoscopes Market Insights

North America dominated the global Endoscopes Market in 2025 with approximately 36.6% revenue share, anchored by the U.S. healthcare system's extraordinary endoscopy program scale, technology investment culture, and favorable reimbursement. The U.S. endoscopy market's commercial dynamics are distinctive: the combination of colorectal cancer screening driving high colonoscopy volumes, the quality metrics program creating institutional investment incentive, and the U.S. being the first-approval market for new endoscopy AI and navigation technology creates a market environment where product innovation converts to commercial adoption faster than anywhere else globally. Endoscopy center construction both hospital-integrated and freestanding ambulatory endoscopy centers has been active, driven by site-of-care migration from hospital outpatient to ambulatory surgical center settings that reduce per-procedure costs while improving patient convenience.

The American Society for Gastrointestinal Endoscopy's 2024 practice survey documents that U.S. gastroenterologists performed an average of 2,100 endoscopic procedures annually per physician, with colonoscopy representing approximately 65% of total procedure volume. The U.S. ambulatory surgical center industry association documents that approximately 60% of outpatient GI endoscopy procedures are now performed in freestanding ASCs rather than hospital outpatient departments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Endoscopes Market Insights

Asia Pacific is the fastest-growing regional Endoscopes Market, driven by Japan's world-class endoscopy culture Japan has the world's highest per-capita endoscopy rate, with gastric cancer screening driving near-universal upper GI endoscopy adoption China’s rapidly expanding hospital-based endoscopy program, India's growing private healthcare sector, and South Korea's comprehensive GI cancer screening program. Japan's endoscopy sophistication is extraordinary: Japanese endoscopists have developed many of the world's most advanced endoscopic mucosal resection and submucosal dissection techniques that are now spreading globally, and Japanese companies including Olympus, Fujifilm, and Hoya/Pentax dominate global flexible endoscope manufacturing with products that set the technical standard for optical quality and working channel performance.

Japan's National Cancer Center statistics document that Japan performs approximately 18 million upper GI endoscopies annually a per-capita rate approximately 5x higher than the U.S. driven by Japan's unusually high gastric cancer incidence and the government's stomach cancer screening program that recommends endoscopy every 2-3 years for adults over 50.

Europe Endoscopes Market Insights

Europe's Endoscopes Market is characterized by sophisticated gastroenterology and surgical endoscopy programs in Germany, France, the UK, Italy, and the Nordic countries, with EU healthcare systems sustaining high-quality endoscopy infrastructure through both public and private healthcare financing. Olympus Medical's European headquarters in Hamburg and Karl Storz's Tuttlingen-based operations the latter being the world's largest manufacturer of rigid endoscopes give Europe a significant endoscopy manufacturing presence that sustains both domestic supply and global export. The EU's single-use endoscope regulatory pathway which applies the same MDR 2017/745 framework as reusable devices has enabled competitive single-use endoscope clearance processes that have brought Ambu, Boston Scientific, and Olympus single-use products to European hospitals.

Middle East & Africa and Latin America Endoscopes Market Insights

The Middle East's Endoscopes Market is growing with the Gulf states' healthcare infrastructure investment, with large hospital complexes in Riyadh, Dubai, and Abu Dhabi maintaining full-service GI endoscopy, bronchoscopy, and surgical endoscopy programs that procure endoscope systems at international price points. Saudi Arabia's Vision 2030 healthcare goals targeting improved chronic disease management including colorectal cancer screening are driving endoscopy capacity expansion. Latin America's endoscopes market is most developed in Brazil and Mexico, where sophisticated GI endoscopy centers in major cities serve both private pay and insurance-covered patients across a growing menu of diagnostic and therapeutic endoscopic procedures.

Endoscopes Market Growth Drivers:

Cancer screening mandate expansion and minimally invasive surgical procedure growth driving sustained global endoscopes market growth

The endoscopes market's growth is built on two foundations that are each individually strong and mutually reinforcing. Cancer screening mandates for colorectal, gastric, esophageal, bladder, and lung cancers create population-level demand for endoscopic procedures that is non-discretionary and recurring. Every person who follows colorectal cancer screening guidelines will have a colonoscopy every 10 years from age 45 through their 70s, creating a guaranteed procedure demand stream that grows with population size and age. Minimally invasive surgery's expansion continuously converts procedures previously requiring open abdominal, thoracic, or urological surgery into laparoscopic or endoscopic cases, growing the procedure volume that creates endoscope demand while benefiting patients with shorter recovery times and lower complication rates.

Endoscopes Market Restraints:

High capital costs and endoscope reprocessing complexity creating adoption barriers in cost-sensitive healthcare markets

The endoscope system's total cost of ownership including capital equipment, reprocessing consumables, maintenance contracts, and replacement scope acquisition when devices are damaged is substantial enough to create procurement barriers for hospitals operating under tight capital budgets. A complete flexible endoscopy system including video processor, light source, two colonoscopes, two gastroscopes, and auxiliary equipment represents USD 150,000-300,000 in capital investment, plus ongoing reprocessing chemical and supply costs of USD 20-40 per scope pass, plus maintenance contracts of 8-12% of system value annually. For hospitals in developing markets where equipment budgets are constrained by reference to per-capita income, these costs create meaningful access barriers that limit endoscopy program scale below what clinical need would justify.

Endoscopes Market Opportunities:

AI-integrated colonoscopy and robotic endoscopy technology creating transformative endoscopes market growth opportunities globally

AI integration represents the most commercially active frontier of endoscope technology development, where machine learning models trained on millions of endoscopic images can identify polyps, characterize lesion morphology, and provide quality indicators in real time during the procedure improving both diagnostic accuracy and procedure documentation quality simultaneously. The clinical evidence is unambiguous: computer-aided detection systems increase adenoma detection rate by 40% in randomized controlled trials, a performance improvement that translates directly into earlier colorectal cancer detection and reduced cancer incidence. As regulatory clearance expands and reimbursement is established for AI endoscopy assistance, adoption across the installed base of endoscopy centers globally will be driven by both quality improvement and medicolegal documentation value.

Recent Developments:

-

2026: Olympus Corporation launched its EVIS X1 AI-integrated endoscopy platform with next-generation dual-focus optics providing simultaneous wide-angle panoramic and magnified views, integrated CADe/CADx AI polyp detection and characterization, and automatic procedure quality metrics documentation achieving FDA clearance in Q1 2026 and commercial availability across its North American and European distribution network.

-

2025: Ambu expanded its single-use endoscope portfolio with the aScope Uretero, a disposable flexible ureteroscope with digital 1080p chip-on-tip imaging, 270-degree tip deflection, and a 3.6Fr working channel targeting the growing recognition that reusable ureteroscopes' reprocessing damage accumulation and infection risk justify single-use replacement for complex upper urinary tract stone cases.

-

2025: Intuitive Surgical's Ion robotic bronchoscopy platform received expanded FDA clearance for peripheral pulmonary lesion biopsy using its articulating robotic catheter, with multi-center clinical trial data reporting a 97.8% success rate in reaching target lesions smaller than 2cm in diameter establishing a new clinical standard for pulmonary nodule diagnosis that was previously accessible only through CT-guided needle biopsy or surgical resection.

Endoscopes Market Key Players

Some of the Endoscopes Market Companies

-

Olympus Corporation

-

FUJIFILM Holdings Corporation

-

Karl Storz SE & Co. KG

-

Hoya Corporation (Pentax Medical)

-

Johnson & Johnson MedTech

-

Stryker Corporation

-

Medtronic plc

-

Boston Scientific Corporation

-

Ambu A/S

-

Richard Wolf GmbH

-

CONMED Corporation

-

Arthrex Inc.

-

Storz Medical AG

-

NovaBay Pharmaceuticals

-

Intuitive Surgical Inc.

-

Auris Health Inc. (J&J)

-

Verathon Inc.

-

Fortimedix Surgical BV

-

EndoChoice Holdings Inc.

-

Vision Sciences Inc.

Endoscopes Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 26.38 Billion |

| Market Size by 2035 | USD 42.14 Billion |

| CAGR | CAGR of 4.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product [Endoscopes (Reusable Endoscopes, Disposable Endoscopes)] • By End Use [Hospitals, Outpatient Facilities] |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Olympus Corporation, FUJIFILM Holdings Corporation, Karl Storz SE & Co. KG, Hoya Corporation (Pentax Medical), Johnson & Johnson MedTech, Stryker Corporation, Medtronic plc, Boston Scientific Corporation, Ambu A/S, Richard Wolf GmbH, CONMED Corporation, Arthrex Inc., Storz Medical AG, NovaBay Pharmaceuticals, Intuitive Surgical Inc., Auris Health Inc. (J&J), Verathon Inc., Fortimedix Surgical BV, EndoChoice Holdings Inc., Vision Sciences Inc. |

Frequently Asked Questions

North America dominated with approximately 36.6% share; Asia Pacific is the fastest growing region.

Gastrointestinal applications dominated the Endoscopes Market in 2025.

Reusable Endoscopes dominated with approximately 83.3% share in 2025; Disposable is the fastest growing.

The Endoscopes Market was valued at USD 26.38 billion in 2025.

The Endoscopes Market is expected to grow at a CAGR of 4.93% from 2026 to 2035.

Get in Touch