Diabetic Retinopathy Market Report Scope & Overview:

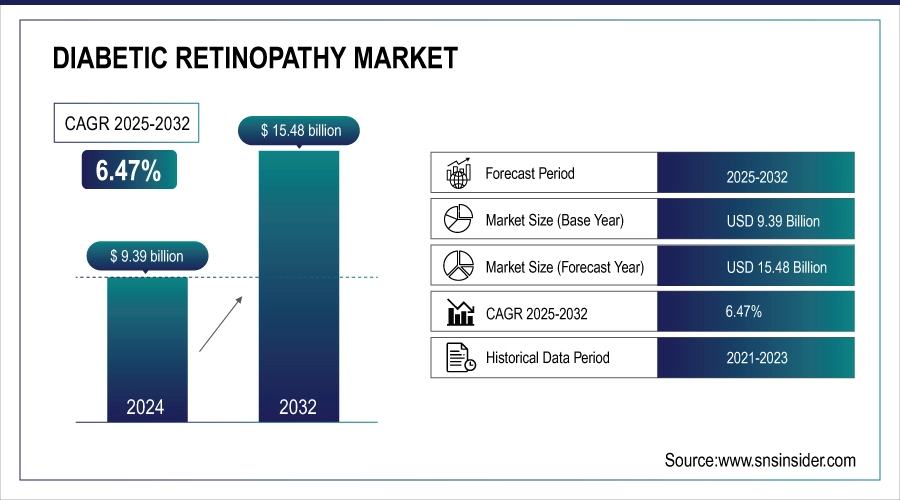

The diabetic retinopathy market size was valued at USD 9.39 billion in 2024 and is expected to reach USD 15.48 billion by 2032, growing at a CAGR of 6.47% over the forecast period of 2025-2032.

The global diabetic retinopathy market is expanding due to the growing number of diabetes cases, especially in rapidly urbanizing regions. Urban lifestyles often involve unhealthy diets, reduced physical activity, and chronic stress, factors that contribute to poor blood sugar control and increase the risk of developing diabetic retinopathy. In densely populated cities, lower-income groups face challenges, including limited healthcare access and delayed diagnosis, which raises the chances of disease progression. Countries including India and China are experiencing a sharp rise in diabetes-linked eye conditions due to these shifts. As a result, the demand for effective DR diagnosis and treatment is rising globally.

For instance, in January 2025, A Lancet study found that urban adults in India face a 2.5x higher diabetic retinopathy risk than rural populations due to lifestyle and delayed diagnosis.

Diabetic Retinopathy Market Size and Forecast

-

Market Size in 2024: USD 9.39 Billion

-

Market Size by 2032: USD 15.48 Billion

-

CAGR: 6.47% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2022–2024

To Get more information On Diabetic Retinopathy Market - Request Free Sample Report

Diabetic Retinopathy Market Trends

-

Rising prevalence of diabetes is driving demand, with over 530 million adults globally affected and nearly 30–35% developing diabetic retinopathy.

-

Increasing adoption of AI-based screening tools is improving early detection, reducing diagnosis time by 40–50% and expanding screening coverage in primary care settings.

-

Growing use of anti-VEGF therapies is boosting treatment outcomes, with these therapies accounting for over 60% of DR treatment revenues.

-

Expansion of teleophthalmology and remote screening is enhancing access, particularly in emerging markets, with screening rates increasing by 25–30% in underserved regions.

-

Rising investments in advanced imaging technologies (OCT and fundus cameras) are improving diagnostic accuracy by up to 35%, supporting early-stage intervention.

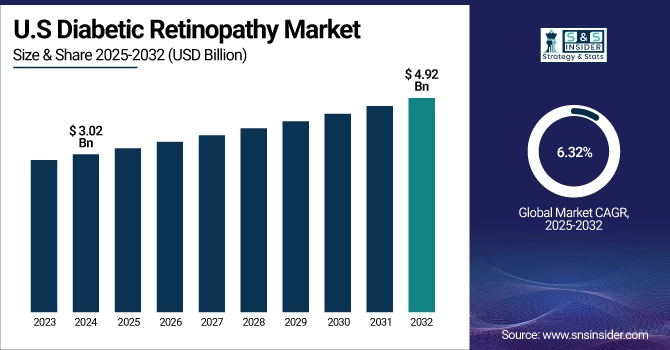

The U.S. diabetic retinopathy market was valued at USD 3.02 billion in 2024 and is expected to reach USD 4.92 billion by 2032, growing at a CAGR of 6.32% from 2025 to 2032. The U.S. is leading the diabetic retinopathy market in the region owing to high support from Medicare and Medicaid, which provide broad access to advanced treatments, telehealth services, and early diagnosis. Medicare pays for anti-VEGF drugs that the FDA has approved for macular degeneration and upfront teleconsultations, and Medicaid covers screenings and care for low-income people. Dual-eligible creates even better affordability and access. Innovative care delivery models and federal programs support the management of chronic diseases.

For instance, in May 2025, CMS reported a 22% rise in Medicare reimbursements and 15% increase in Medicaid DR screenings, boosting the U.S. diabetic retinopathy market share significantly.

Market Dynamics:

Drivers:

-

Technological Advancements, Driving the Diabetic Retinopathy Market Growth

The diabetic retinopathy market is primarily driven by technological advancements. Imaging tools based on AI, including OCT, enhance early and precise diagnosis, whereas genomics tools contribute to personalized treatments. Real-time monitoring is made possible by IoT devices and wearables, thus improving disease treatment. Other text: Telemedicine widens access to treatment in remote areas, while new drug delivery mechanisms ensure better treatment compliance. Together, these advances increase efficiency, access, and results, and drive the market substantially.

For instance, in February 2025, AAO reported that AI-based diabetic retinopathy tools improved diagnosis speed by 35% and early detection rates by 28%, enhancing patient outcomes significantly.

Restraints:

-

High Cost of Anti-VEGF Therapy, Restraining the Diabetic Retinopathy Market

The high cost of anti-VEGF drugs is a major challenge for the diabetic retinopathy market. Expensive, occasional injections reduce access in low-income areas and challenge health budgets, slowing the adoption of treatment. This limits overall market growth despite increasing demand. But it's also driving the use of biosimilars and innovation in depot therapies. These issues restrict the expansion of the diabetic retinopathy market share, particularly in low-cost and under-insured communities.

For instance, in April 2025, GlobalData reported 42% of DR patients in LMICs discontinued anti-VEGF due to cost, while biosimilar usage rose 31%, moderating market growth.

Segmentation Analysis:

By Type

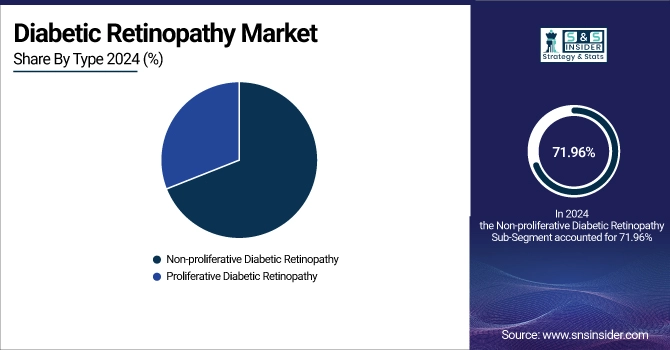

Non-proliferative diabetic retinopathy was the dominant segment in the diabetic retinopathy market analysis, with a market share of 71.96% share in 2024, owing to the higher incidence among early-stage diabetes patients and after diagnostic work-up. NPDR represents the majority of diabetic retinopathy diagnosed cases, with most patients entering this stage before advancing to proliferative diabetic retinopathy. With the early detection and increasing awareness, the screening programs and AI-powered tools all serve to increase the demand for treatment. This dramatically raises the diabetic retinopathy market share for NPDR-targeted diagnostics and therapies.

Proliferative Diabetic Retinopathy is emerging as the fastest growing segment in the global diabetic retinopathy market with a CAGR of 6.91%, driven by accelerated disease progression in untreated or inadequately treatment of diabetes cases. Growing demand for the advanced treatment, including anti-VEGF therapy and vitrectomy, is one of the key growth factors. This factor has a tremendous positive impact on the overall diabetic retinopathy market growth as severe cases demand intensive and high-cost treatments.

By Management

In 2024, the Anti-VEGF segment controlled the global diabetic retinopathy market share, owing to the established benefit in stopping the progression of the disease and improving visual outcomes, particularly in diabetic macular edema and proliferative phases. It receives wide clinical use, is FDA approved, and enjoys favorable reimbursement. This leadership position greatly amplifies the anti-VEGF diabetes retinopathy treatment market share within developed and emerging health systems.

The Laser Surgery is the fastest-growing segment in the diabetic retinopathy industry, owing to its low cost, availability in resource-limited settings, and proven effectiveness in visual preservation. Demand is fueled further by rising use during early-to-mid DR stages, particularly in low- and middle-income countries. This increase makes a major contribution to the overall market for diabetic retinopathy growth, particularly in areas with a poor supply of anti-VEGF treatments.

Regional Analysis:

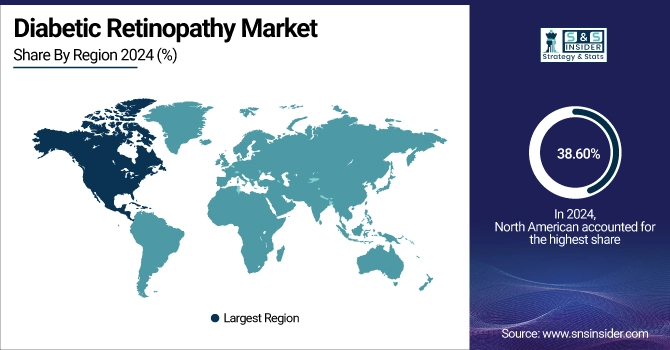

In 2024, the North American region dominated the diabetic retinopathy industry and accounted for 38.60% of the overall revenue share, owing to its strong health care system, high diabetes rates, and generous Medicare and Medicaid reimbursement policies. Its leadership is also backed by the use of state-of-the-art technology, including AI-guided retinal screening, OCT imaging, and anti-VEGF therapies. Strong awareness, regular screening, and availability of specialized care contribute to high early diagnosis and treatment rates. The existence of key market players and positive competition among them are the other factors that will supplement market growth. Together, these elements help to drive North America’s global diabetic retinopathy market share and make North America the global focus for advances in both diagnosis and treatment of the condition.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the second-largest player in the diabetic retinopathy industry market, attributable to the vast patient pool and the geriatric population, lifestyle-related health risks, and strong healthcare infrastructure. High participation in screening programmes, community-driven awareness campaigns supported by the government, and availability of sophisticated treatment methods have resulted in early diagnosis and successful treatment, and the chances of developing colorectal cancer excessively. Competent healthcare professionals and robust R&D also add to the innovative mix, ensuring steady diabetic retinopathy market growth in the region.

The Asia Pacific region is projected to grow with the fastest CAGR of 7.03% over the forecast period, owing to a growing diabetic population, urbanization, and altered lifestyle factors, including an imbalanced diet and a lack of exercise. Diabetes is increasing in epidemic proportions in several countries of the region, particularly India and China, and is directly increasing the prevalence of diabetic retinopathy. Advancements in healthcare infrastructure, increasing awareness about eye health, and growing screening programs are promoting early diagnosis and improved access to treatment. Governments are also putting funds into teleophthalmology and mobile screening efforts targeted at the rural masses. Furthermore, the rising accessibility of more affordable treatments and biosimilars is simplifying the care of DRONGL.

The Middle East & Africa are also developing as a potential market in the diabetic retinopathy industry, as diabetes is on the rise in urban areas. But, poor and inadequate access to specialized eye care, lack of awareness, and under developed health delivery system do not assist in early diagnosis and management. Continuous initiatives by both the government and NGOs to increase the number of screening programs and expand healthcare access are aiding the diabetic retinopathy market growth in some of countries of the region.

The diabetic retinopathy market in Latin America is also rising due to the increasing diabetic affected population and high urbanization. Nevertheless, health disparities, limited availability of sophisticated disease management, and poor screening rates are barriers that limit disease management across the population. Public health programs and awareness campaigns instituted by governments in the region are leading to early detection. These factors are increasingly contributing toward the growth of the diabetic retinopathy market in major countries, including Brazil, Mexico, and Argentina.

Key Players:

Diabetic retinopathy companies include Regeneron Pharmaceuticals, Inc., Roche Holding AG / Genentech, Novartis AG, Bayer AG, Alimera Sciences, Inc., Allergan, Carl Zeiss Meditec AG, Topcon Corporation, Optos plc, Eyenuk, Inc., and other players.

Recent Developments:

-

In February 2025, Regeneron launched Eylea HD (8mg) in the U.S. after FDA approval, offering extended dosing intervals for diabetic retinopathy and improving patient adherence and treatment outcomes.

-

In May 2024, Bayer presented real-world data at ARVO 2024 showing Eylea’s effectiveness in Asian DR patients, reinforcing its clinical value and supporting wider adoption in regional treatment protocols.

-

In October 2024, AbbVie (Allergan) initiated development of a next-generation corticosteroid implant for diabetic retinopathy, aiming for extended drug release and reduced injection frequency to improve long-term treatment adherence.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 9.39 billion |

| Market Size by 2032 | USD 15.48 billion |

| CAGR | CAGR of 6.47% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Proliferative Diabetic Retinopathy, Non-proliferative Diabetic Retinopathy) • By Management(Anti-VEGF, Intraocular Steroid Injection, Laser Surgery, Vitrectomy) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Regeneron Pharmaceuticals, Inc., Roche Holding AG / Genentech, Novartis AG, Bayer AG, Alimera Sciences, Inc., Allergan, Carl Zeiss Meditec AG, Topcon Corporation, Optos plc, Eyenuk, Inc., and other players |

Frequently Asked Questions

Regeneron Pharmaceuticals, Inc., Roche Holding AG / Genentech, Novartis AG, Bayer AG, Alimera Sciences, Inc., are the leading players in the global Diabetic Retinopathy Market.

The Diabetic Retinopathy Market is growing at a CAGR of 6.47% from 2025 to 2032.

North America regions are leading the growth in the Diabetic Retinopathy Market.

Technological Advancements driving the Diabetic Retinopathy Market Growth.

The current market size for the Diabetic Retinopathy Market is USD 9.98 billion.

Get in Touch