Infusion Pump Market Report Scope & Overview:

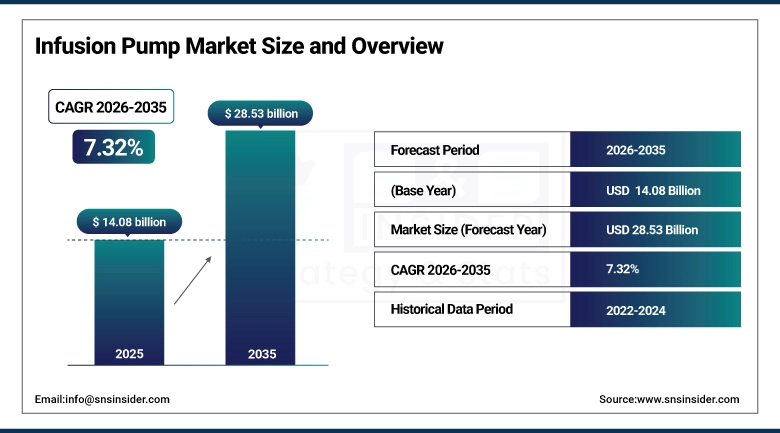

The Infusion Pump Market was estimated at USD 14.08 billion in 2025 and is expected to reach USD 28.53 billion by 2035 and grow at a CAGR of 7.32% over the forecast period of 2026-2035.

Growth in the infusion pump market can be attributed to an increase in cases of chronic diseases like diabetes, cancer, and pain disorders. Other factors that drive growth in this market include the increasing number of patients requiring home-based infusion treatments, development in the technology behind smart pumps, and positive regulatory approvals. The adoption of ambulatory and portable infusion products is another market trend that helps in making the experience better and more comfortable for patients. Infusion pump market growth can be seen through healthcare infrastructure growth in emerging countries, resulting in consistent global demand.

Infusion Pump Market Size and Forecast

-

Market Size in 2025: USD 14.08 Billion

-

Market Size by 2035: USD 28.53 Billion

-

CAGR: 7.32% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Infusion Pump Market - Request Free Sample Report

Infusion Pump Market Trends

-

Rapid adoption of smart infusion pumps integrated with dose-error reduction software (DERS), drug libraries, and IoT connectivity enabling real-time monitoring, automated dose alerts, and electronic health record integration.

-

Growing transition toward ambulatory and wearable infusion pump designs that allow patients to receive complex infusion therapies while maintaining mobility and an active lifestyle outside traditional hospital settings.

-

Increasing deployment of AI and machine learning in smart infusion systems for predictive occlusion detection, adaptive dosing algorithms, and automated pharmacokinetic modeling to optimize drug delivery precision.

-

Rising demand for home infusion therapy driven by healthcare cost containment goals, patient preference for home-based treatment, and growing availability of nurse-assisted home infusion services for chronic conditions.

-

Expansion of closed-loop insulin delivery systems combining continuous glucose monitoring (CGM) with insulin infusion pumps, representing a rapidly growing application in diabetes management technology.

-

Growing regulatory approvals for connected infusion platforms following the FDA's digital health guidance frameworks, enabling new smart pump software features including remote programming and real-time clinical decision support.

-

Increasing strategic acquisitions and partnerships among infusion pump manufacturers to expand product portfolios, enhance technological capabilities, and strengthen global distribution networks in emerging healthcare markets.

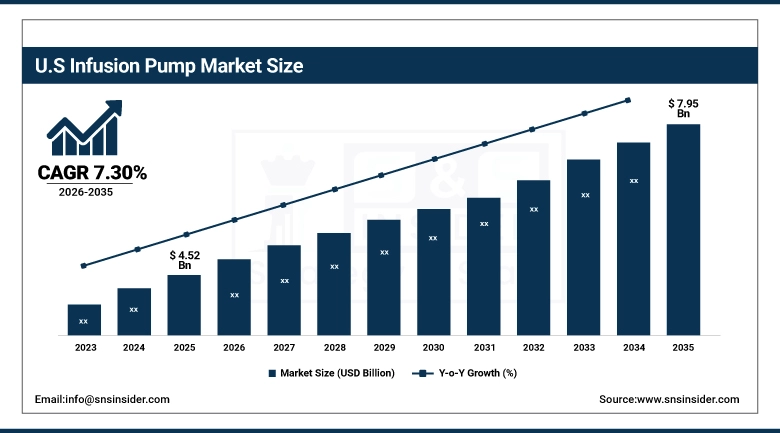

U.S. Infusion Pump Market was valued at USD 4.52 billion in 2025 and is expected to reach USD 7.95 billion by 2035, registering a CAGR of 7.30% during 2026-2035.

The US is the most dominant and advanced market for infusion pumps due to high prevalence rates of chronic illnesses, a supportive regulatory environment that promotes innovation within smart pumps, and reimbursement for home infusion treatment via Medicare. Market leaders such as BD (Becton, Dickinson and Company), Baxter International Inc., Medtronic plc, and ICU Medical, among others, ensure constant innovation and growth.

Infusion Pump Market Segment Analysis

-

Based on Product, Devices accounted for the largest market share in 2025; Accessories & Consumables expected to be the fastest-growing segment (recurring revenue model).

-

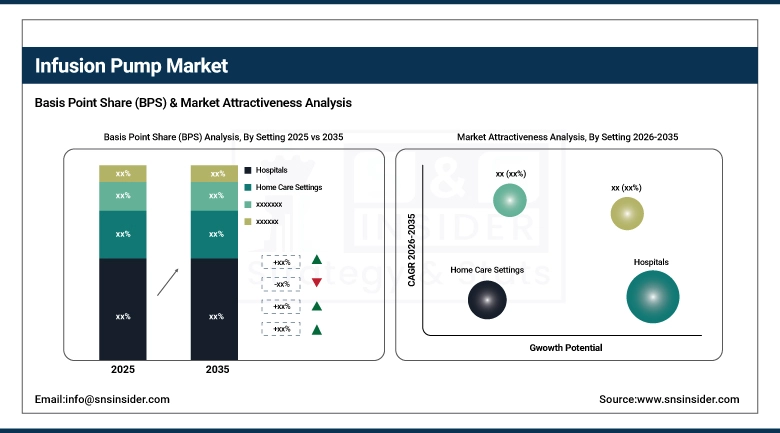

Based on Setting, Hospitals accounted for the largest market share (~48.15%) in 2025; Home Care Settings expected to be the fastest-growing segment (CAGR of 7.89%).

-

Based on Application, Diabetes accounted for the largest market share in 2025; Chemotherapy/Oncology and Pain Management are key high-growth application segments.

By Setting, Hospitals dominate, Home Care Settings expected to grow fastest

Hospitals emerged as the leading end-users of the infusion pump market due to high numbers of treatment cases, critical care requirements for patients, and the increased use of smart infusion pumps in intensive care units, oncology, and surgery rooms. Investments have been made in central infusion devices that link to electronic health records, pharmacy information systems, and nursing stations to facilitate better patient care services and streamline workflow processes.

Home care settings will emerge as the fastest-growing end-user segment in terms of CAGR of 7.89%. Factors contributing to this growth include the growing need for healthcare services at home, increase in the number of elderly patients, chronic disease prevalence, and the development of portable infusion pumps, among others. These settings offer patients comfort and convenience in managing their treatment.

By Application, Diabetes dominates, Chemotherapy/Oncology and Pain Management grow rapidly

The diabetes market led the infusion pump market during the forecast period of 2025 due to the fast-growing prevalence rate of diabetes especially type 1 and insulin dependent type 2 diabetes along with the growing preference for using the insulin pumps for accurate insulin administration. The advent of sophisticated closed-loop systems that include insulin pumps along with CGM sensors is bringing about revolutionary changes to diabetes care around the world.

Other high-growth segments include Chemotherapy/Oncology and Analgesia/Pain Management owing to the rising prevalence rate of cancer patients all around the world, rising preference for ambulatory chemotherapy pumps along with increased use of PCA pumps to deliver pain relief treatment.

By Product, Devices dominate, Accessories & Consumables expected to grow strongly

Devices hold major share in the infusion pumps market due to the critical part played by the pump devices in making possible the use of infusion therapy techniques. Large Volume Pumps, Syringe pumps, Enteral Feeding Pumps, and Ambulatory pumps are some examples of advanced devices used to meet specific needs in hospitals, homes, and specialist facilities.

Infusion pump accessories and disposables such as infusion sets, infusion tubes, cassettes, and syringes are becoming an increasingly important source of recurring revenues for pump manufacturers due to need-based periodic replacements.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

74% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

40% |

|

Middle East & Africa |

UAE |

30% |

|

Latin America |

Brazil |

44% |

North America Infusion Pump Market Insights

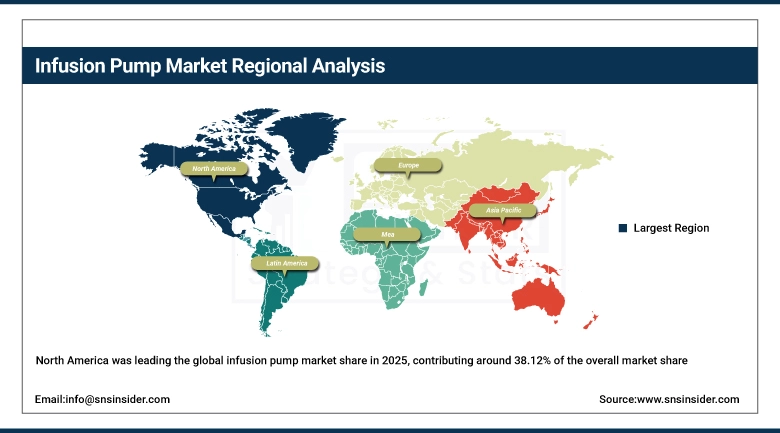

North America was leading the global infusion pump market share in 2025, contributing around 38.12% of the overall market share. North America enjoys a highly developed health care system and reimbursement schemes, along with a high acceptance rate for technology-based devices in the market. North America is considered as a key market owing to growing incidences of various chronic ailments that include diabetes, cancer, and cardiovascular disease among others that require the use of infusion pumps. Key industry players like Baxter, Medtronic, BD, and ICU Medical are making huge investments in intelligent infusion devices that can be digitally monitored.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Infusion Pump Market Insights

The Asia Pacific region is expected to experience the highest rate of growth in the infusion pump industry during the forecast period, owing to factors such as rapid healthcare infrastructure development, increased spending by hospitals, and enhanced knowledge about chronic conditions. The countries of China, India, Japan, and South Korea have experienced high demand for portable infusion pumps, insulin pumps, and sophisticated hospital infusion devices. Increased middle-class populations, greater availability of healthcare, and higher healthcare budgets from governments are some of the other factors contributing to the growth of the infusion pump industry.

Europe Infusion Pump Market Insights

The market share of Europe in the infusion pump market is substantial due to factors such as the advanced healthcare infrastructure, aging population, and prevalence of diseases that require prolonged infusions. Countries contributing to this market in Europe include Germany, France, United Kingdom, Italy, and Spain. With an increasing adoption rate of digital infusion pumps across hospitals, there is also the need to adopt smart infusion pumps that can be connected to digital monitoring tools and electronic health record systems. Factors such as high-quality regulations, increasing home care services, and advancements in healthcare technologies contribute to market growth.

Middle East & Africa and Latin America Infusion Pump Market Insights

The markets for infusion pumps in the regions of Middle East & Africa and Latin America are experiencing steady growth due to improved healthcare infrastructure, increased healthcare expenditure, and an increased understanding of modern medical devices and equipment. Nations like the UAE, Saudi Arabia, Brazil, and Mexico are making considerable investments in upgrading their healthcare systems, which is favoring the acceptance of infusion pumps. Moreover, the high prevalence of diseases such as diabetes, cancer, and renal ailments is also contributing to the growing need for infusion therapy.

Market Growth Drivers: Rising Chronic Disease Burden and Technological Advancements Driving Strong Infusion Pump Market Growth Globally

There is immense growth being witnessed in the global infusion pump industry as there has been an increase in the number of patients suffering from chronic illnesses like diabetes, cancer, and heart disease who require long-term therapy. The demand for precise and controlled medication delivery in order to improve patient care is resulting in more use of these products. Innovation in technology like smart infusion devices, connectivity through wireless technology, dose-error reduction devices, and electronic medical records is contributing further to improved healthcare.

Market Restraints: High Device Costs and Safety Concerns Limiting Widespread Adoption of Infusion Pump Technologies

While there is considerable demand for the products in the infusion pump industry, the market still encounters several barriers in terms of high costs of devices, maintenance, and difficulty in usage. In addition, small hospitals in developing nations find it difficult to implement the product due to issues related to financial constraints and the absence of skilled individuals for operating such pumps. Safety problems like drug administration mistakes, software problems, and issues related to compatibility with other systems also act as major barriers in the adoption of the technology.

Market Opportunities: Expansion of Home Healthcare Services and Smart Infusion Technologies Creating New Growth Opportunities Worldwide

The infusion pump industry offers various potentialities due to the fast growth of the home healthcare segment and increasing demand for innovative solutions in medical care. With the increase in demand for portable and wearable devices, it is possible for the patients to be treated at home and thereby cut down healthcare expenditures. IoT technology and artificial intelligence are contributing to the effectiveness and security of these devices. Emerging markets have shown growth in healthcare infrastructure development, while growing adoption of smart hospitals and personalized medication is generating revenue for infusion pump manufacturers.

Recent Developments:

-

2025 (Q2): Smiths Medical received FDA clearance for its CADD-Solis VIP Ambulatory Infusion Pump, designed for pain management and chemotherapy in outpatient and home care settings, expanding ambulatory infusion therapy options.

-

2024 (April): Baxter International secured FDA 510(k) clearance for its Novum IQ Large Volume Infusion Pump integrated with Dose IQ Safety Software, emphasizing secure and efficient infusion therapy in clinical settings.

Infusion Pump Market Key Players

-

Medtronic plc

-

Fresenius Kabi AG

-

ICU Medical, Inc.

-

Smiths Medical

-

Terumo Corporation

-

Moog Inc.

-

Nipro Corporation

-

Zyno Medical

-

B. Braun Melsungen AG

-

Insulet Corporation

-

Tandem Diabetes Care

-

Johnson & Johnson (Ethicon)

-

Roper Technologies (Roper Medical)

-

Micrel Medical Devices SA

-

Mindray Medical International

-

Shenzhen Biocare Medical Instrument Co.

-

Woo Young Medical Co., Ltd.

-

AMPall Co., Ltd.

Infusion Pump Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.08 Billion |

| Market Size by 2035 | USD 28.53 Billion |

| CAGR | CAGR of 7.32% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Devices, Accessories & Consumables) • By Setting (Hospitals, Home Care Settings, Ambulatory Care Settings, Academic & Research Institutes) • By Application (Diabetes, Chemotherapy/Oncology, Analgesia/Pain Management, Gastroenterology, Pediatrics/Neonatology, Hematology, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BD (Becton, Dickinson and Company); Baxter International Inc.; Medtronic plc; Fresenius Kabi AG; ICU Medical, Inc.; Smiths Medical; Terumo Corporation; Moog Inc.; Nipro Corporation; B. Braun Melsungen AG; Insulet Corporation; Tandem Diabetes Care; Johnson & Johnson (Ethicon); Roper Technologies (Roper Medical); Micrel Medical Devices SA; Mindray Medical International; Shenzhen Biocare Medical Instrument Co.; Woo Young Medical Co., Ltd.; AMPall Co., Ltd. |

Frequently Asked Questions

Ans: North America dominated the Infusion Pump Market in 2025, accounting for approximately 38.12% of global market revenue, driven by advanced healthcare infrastructure, high chronic disease prevalence, strong regulatory frameworks promoting smart pump innovation, and early adoption of home infusion therapy programs.

Ans: The Hospitals segment dominated the Infusion Pump Market in 2025 with approximately 48.15% revenue share, driven by high patient treatment volumes, critical care needs, and extensive smart pump adoption across ICUs, oncology departments, and surgical settings.

Ans: The Diabetes segment dominated the Infusion Pump Market in 2025, driven by the rapidly increasing global incidence of diabetes and the growing adoption of insulin pump therapy as the preferred method for precise continuous insulin delivery, including advanced closed-loop insulin delivery systems.

Ans: Increasing hospital admission rates, rising prevalence of chronic diseases including diabetes, cancer, and pain disorders, growing demand for home infusion therapy, and advancements in smart pump technology featuring AI-driven dose optimization and IoT connectivity are the primary drivers of sustained market growth through 2035.

Ans: The Infusion Pump Market was valued at USD 13.12 billion in 2025.

Ans: The Infusion Pump Market is expected to grow at a CAGR of 7.32% from 2026 to 2035.

Get in Touch