Digestive Health Supplements Market Report Scope & Overview:

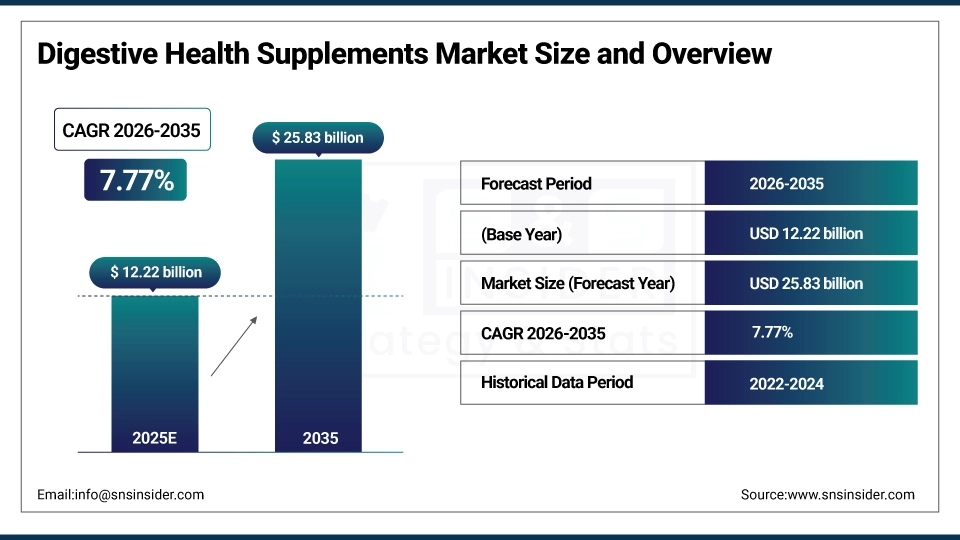

The Digestive Health Supplements Market size is estimated at USD 12.22 billion in 2025 and is expected to reach USD 25.83 billion by 2035, growing at a CAGR of 7.77% over the forecast period of 2026-2035.

The global digestive health supplements market trend is a growing demand for gut health optimization solutions such as probiotic formulations, prebiotic supplements, and digestive enzyme products as the growth of the market is driven by increasing awareness about microbiome health, rising prevalence of gastrointestinal disorders, and consumer shift toward preventive healthcare. This trend is also driven by a growing adoption of functional foods and beverages and the growing focus on holistic wellness as consumers become more focused on maintaining digestive balance and are more willing to invest in natural supplementation technologies, resulting in growth in the domestic and international market for vitamins and dietary supplements solutions.

For instance, in March 2024, growing awareness and improved probiotic research drove a 24% increase in digestive health supplement consumption for health-conscious consumers globally, boosting gut microbiome optimization and digestive wellness product adoption.

Digestive Health Supplements Market Size and Forecast:

-

Market Size in 2025: USD 12.22 billion

-

Market Size by 2035: USD 25.83 billion

-

CAGR: 7.77% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

Get more information on Digestive Health Supplements Market - Request Free Sample Report

Digestive Health Supplements Market Trends

-

Digestive health supplement solutions are being adopted because consumers demand effective gut microbiome support, improved digestive function, and natural alternatives to pharmaceutical interventions.

-

Customized probiotic formulations based on individual gut profiles, dietary preferences, and specific digestive conditions to improve wellness outcomes.

-

The development of advanced delivery systems, multi-strain probiotic combinations, and synbiotic formulations to improve the bioavailability and efficacy of digestive supplements.

-

Functional beverage integration, fortified food products, and convenient supplement formats are all available to ensure continuous digestive support and consumer adherence.

-

Increased demand for clean-label products, organic certifications and plant-based formulations to help transparency and natural ingredient preferences.

-

Collaboration between supplement manufacturers, microbiome research institutions and healthcare providers to develop evidence-based digestive health products and improve consumer education.

-

FDA, EFSA and national regulatory authorities promoting standards for probiotic strain identification, safety evaluation, health claim substantiation, and quality manufacturing practices.

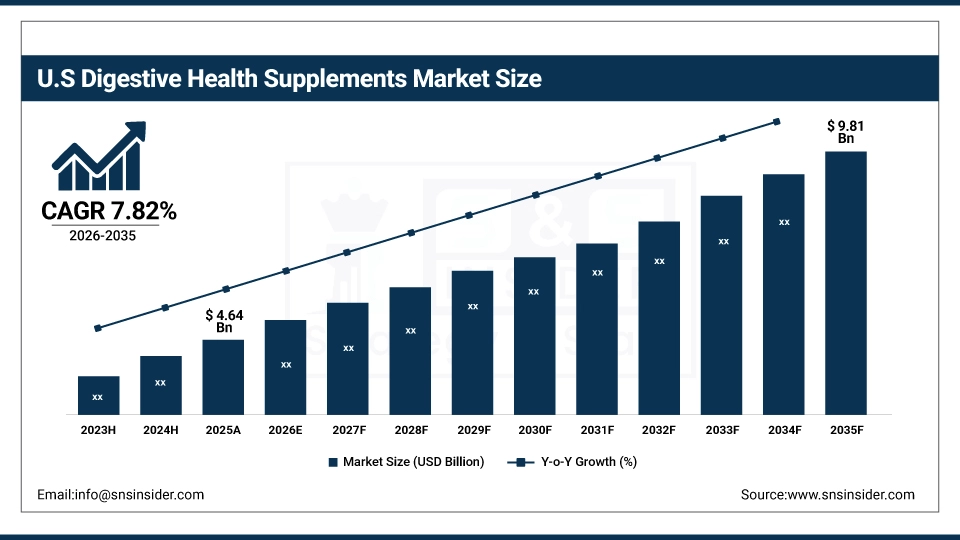

The U.S. Digestive Health Supplements Market is estimated at USD 4.64 billion in 2025 and is expected to reach USD 9.81 billion by 2035, growing at a CAGR of 7.82% from 2026-2035. The United States represents the largest market for digestive health supplements, primarily driven by the high prevalence of digestive disorders, extensive consumer awareness about gut health benefits, and well-developed retail distribution infrastructure. Consumer preference for preventive healthcare, moderately high levels of disposable income and increased spending on wellness products from health-conscious populations help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the innovative product development and swift adoption of probiotic and prebiotic supplement solutions.

Digestive Health Supplements Market Growth Drivers:

-

Rising Prevalence of Digestive Disorders and Gut Health Awareness is Driving the Digestive Health Supplements Market Growth

Rising prevalence of digestive disorders and gut health awareness take the center stage as a growth driver for the digestive health supplements market share, and are driven by the increasing incidence of irritable bowel syndrome, inflammatory bowel disease, and chronic indigestion conditions coupled with consumer education about microbiome importance. These solutions for digestive wellness and preventive gastrointestinal care are driving the base of the market, the penetration of probiotic & prebiotic markets, and adding to the overall market share globally.

For instance, in June 2024, probiotic and digestive enzyme supplements accounted for ~59% of the total global functional supplement investments, reflecting growing consumer preference and expanding market share.

Digestive Health Supplements Market Restraints:

-

Regulatory Complexity and Lack of Standardization are Hampering the Digestive Health Supplements Market Growth

Regulatory complexity & lack of standardization of digestive health supplements also restrict the digestive health supplements market growth, as a large number of products face difficulties establishing consistent probiotic strain viability, substantiating health claims, and navigating varying international regulatory frameworks. This might lead to consumer confusion, limited product credibility, and reduced market penetration for manufacturers. As a result, consumer trust suffers, and market growth is stunted in regions where regulatory oversight is fragmented and quality control standards remain inconsistent.

Digestive Health Supplements Market Opportunities:

-

Personalized Nutrition and Microbiome Testing Drive Future Growth Opportunities for the Digestive Health Supplements Market

The opportunity in the personalized nutrition and microbiome testing in digestive health supplements market is in the form of customized probiotic recommendations, targeted prebiotic interventions, and individualized digestive enzyme formulations. These solutions provide for precision gut health optimization, data-driven supplement selection, and enhanced therapeutic efficacy. Through improved consumer outcomes, scientific validation, and differentiated product offerings, particularly in areas with advanced health technology adoption, these innovations may improve digestive wellness, decrease gastrointestinal symptoms, and expand the market.

For instance, in April 2024, research institutions reported that 71% of wellness-focused consumers expressed interest in personalized digestive health solutions, highlighting rising demand and increasing opportunity for customized supplement products.

Digestive Health Supplements Market Segment Analysis

-

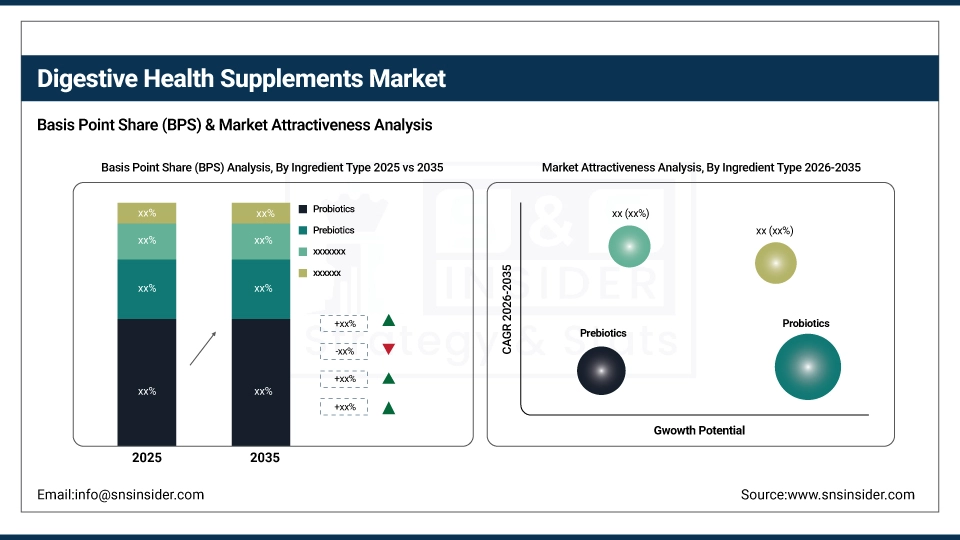

By ingredient type, probiotics held the largest share of around 46.82% in 2025E, and the prebiotics segment is expected to register the highest growth with a CAGR of 8.34%.

-

By product type, the vitamins & dietary supplements segment dominated the market with approximately 54.67% share in 2025E, while the functional foods & beverages is expected to register the highest growth with a CAGR of 8.12%.

-

By distribution channel, supermarkets/hypermarkets accounted for the leading share of nearly 38.91% in 2025E, and online pharmacies is expected to register the highest growth with a CAGR of 9.23%.

By Ingredient Type, Probiotics Leads the Market, While Prebiotics Registers Fastest Growth

The probiotics segment accounted for the highest revenue share of approximately 46.82% in 2025, owing to extensive scientific research supporting their efficacy, widespread consumer recognition of gut microbiome benefits, and diverse product availability across multiple formats. Emerging trends, including increasing strain-specific formulations and multi-strain probiotic combinations for targeted digestive conditions. In comparison, the prebiotics segment is anticipated to achieve the highest CAGR of nearly 8.34% during the 2026–2035 period, driven by the growing understanding of prebiotic fiber importance, synergistic benefits when combined with probiotics, and natural food-based ingredient preferences. Drivers include rising consumer interest in holistic gut health, the preference for dietary fiber supplementation supporting overall wellness.

By Product Type, the Vitamins & Dietary Supplements Segment dominates, while the Functional Foods & Beverages Segment Shows Rapid Growth

By 2025, the vitamins & dietary supplements segment contributed the largest revenue share of 54.67% due to concentrated dosage convenience, targeted therapeutic applications and established consumer supplement purchasing habits. Growing adoption of capsule, tablet and powder formulations coupled with e-commerce accessibility, consumers are increasingly choosing traditional supplement formats. The functional foods & beverages segment is projected to grow at the highest CAGR of about 8.12% between 2026 and 2035 due to the growing need for seamless nutrition integration and daily consumption convenience. Some of the reasons include better palatability compared to traditional supplements, innovative product development across yogurt, kombucha and fortified beverages, and consumer preference for food-first nutritional approaches.

By Distribution Channel, Supermarkets/Hypermarkets Lead, while Online Pharmacies Registers Fastest Growth

The supermarkets/hypermarkets segment accounted for the largest share of the digestive health supplements market with about 38.91%, owing to their extensive product variety, immediate availability, and in-person shopping preferences for health products. Reasons driving the physical retail segment include consumer desire for product examination and convenient one-stop shopping experiences. In addition, the online pharmacies segment is slated to grow at the fastest rate with a CAGR of around 9.23% throughout the forecast period of 2026–2035, as digital-native consumers seek subscription delivery models, comparative pricing transparency, and discreet purchasing options. Increased focus on e-commerce platform development and direct-to-consumer marketing contribute to their adoption, while improved product information accessibility and personalized recommendation algorithms drive continued investment.

Digestive Health Supplements Market Regional Highlights:

North America Digestive Health Supplements Market Insights:

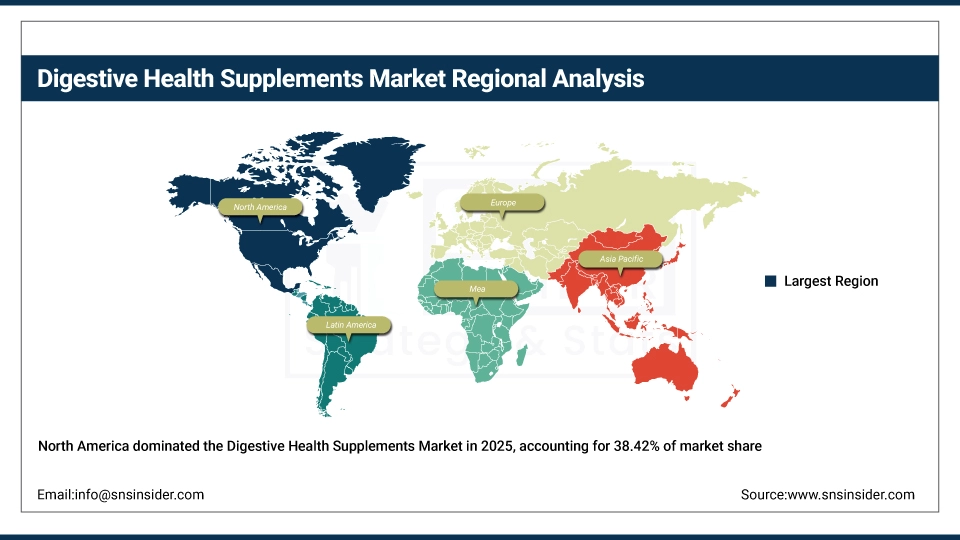

North America held the largest revenue share of over 38.42% in 2025 of the digestive health supplements market due to an established wellness industry infrastructure, high consumer health consciousness, and extensive product innovation from leading supplement manufacturers. Drivers include widespread understanding of gut-brain axis connections, an advanced retail distribution network, growing probiotic food category development and greater acceptance of preventive healthcare approaches stemming from chronic disease awareness. At the same time, various clinical research investments, healthcare provider recommendations and enormous marketing expenditures from nutraceutical companies are anchoring digestive health supplement products in the market, and ensuring multibillion dollar revenues around the world.

Get Customized Report as per your Business Requirement - Request For Customized Report

Asia Pacific Digestive Health Supplements Market Insights:

Asia Pacific is the fastest-growing segment in the digestive health supplements market with a CAGR of 8.56%, as the awareness about probiotic benefits, rising middle-class purchasing power, and traditional fermented food consumption patterns in developing nations is growing. Factors including rapid urbanization, changing dietary habits with increased processed food consumption, and growing uptake of Western wellness trends are stimulating the market growth. E-commerce expansion and health food store proliferation have been instrumental in improving product accessibility, especially in urban and semi-urban settings. Public health campaigns and increasing healthcare expenditure also help in advancing digestive wellness awareness and supplement adoption. Increase in demand in Asia Pacific region owing to rising lifestyle disease prevalence against historical health patterns and growing affordability and accessibility of functional food and supplement products.

Europe Digestive Health Supplements Market Insights:

The digestive health supplements market in Europe is the second-dominating region after North America on account of an increase in the adoption of functional foods, robust regulatory frameworks ensuring product quality, and increasing consumer preference for natural health solutions across healthcare systems. Rising implementation of evidence-based probiotic applications, advanced microbiome research, favorable government support for preventive nutrition, and cross-border supplement trade facilitation are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Digestive Health Supplements Market Insights:

In Latin America, and Middle East & Africa, the growing health consciousness and increase in retail infrastructure development with rising disposable incomes support the digestive health supplements market growth. The rising popularity of affordable probiotic products and increasing awareness about gut health benefits, along with international brand penetration, will aid nutritional supplement accessibility and consumer adoption. The increasing urban population and improving healthcare education in these regions are continuing to encourage market growth.

Digestive Health Supplements Market Competitive Landscape:

Procter & Gamble Company (est. 1837) is a leading global consumer goods corporation that focuses on health and wellness products across multiple categories. It uses its extensive research capabilities and global distribution networks to produce cutting-edge digestive health supplements with established consumer trust and brand recognition.

-

In February 2025, it expanded its digestive wellness portfolio with next-generation probiotic formulations featuring clinically-validated strains, aiming to improve gut microbiome support and consumer digestive comfort across its global product network.

Nestlé S.A. (est. 1866) is a well-known global nutrition and health company focused on functional foods, dietary supplements, and wellness products. It invests in science-based digestive health innovations and probiotic research with the hopes of revolutionizing gut wellness with clinically-proven, accessible, and consumer-friendly nutritional solutions.

-

In May 2024, launched an enhanced range of prebiotic fiber supplements featuring innovative delivery formats across European and North American markets, enhancing digestive support, microbiome nourishment, and overall gastrointestinal wellness.

Danone S.A. (est. 1919) is a leading international food and beverage company in the fields of dairy products, plant-based foods, and specialized nutrition. The company's digestive health product portfolio focuses on probiotic yogurt formulations and functional beverages, and features a strong commitment to microbiome research and continuous innovation to complement the strong market presence in both retail and healthcare settings.

-

In September 2024, introduced advanced multi-strain probiotic beverages with enhanced gut health benefits for its Activia brand, strengthening consumer engagement capabilities and expanding adoption among health-conscious populations globally.

Digestive Health Supplements Market Key Players:

-

Procter & Gamble Company

-

Nestlé S.A.

-

Danone S.A.

-

Abbott Laboratories

-

Reckitt Benckiser Group plc

-

Bayer AG

-

Amway Corporation

-

Herbalife Nutrition Ltd.

-

Glanbia plc

-

Chr. Hansen Holding A/S

-

DuPont de Nemours, Inc.

-

Yakult Honsha Co., Ltd.

-

Nature's Bounty Co.

-

Church & Dwight Co., Inc.

-

Garden of Life (Nestlé Health Science)

-

Probiotics International Ltd. (Protexin)

-

Jarrow Formulas, Inc.

-

Nutraceutix Inc.

-

Koninklijke DSM N.V.

-

PepsiCo, Inc.

-

General Mills, Inc.

-

NOW Health Group, Inc.

-

Rainbow Light Nutritional Systems

-

Life-Space Group Pty Ltd

-

Culturelle (i-Health, Inc.)

|

Report Attributes |

Details |

|---|---|

|

Market Size in 2025 |

USD 12.22 Billion |

|

Market Size by 2035 |

USD 25.83 Billion |

|

CAGR |

CAGR of 7.77% From 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

•By Ingredient Type (Probiotics, Prebiotics, Digestive Enzymes/Food Enzymes, and Others) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Procter & Gamble Company, Nestlé S.A., Danone S.A., Abbott Laboratories, Reckitt Benckiser Group plc, Bayer AG, Amway Corporation, Herbalife Nutrition Ltd., Glanbia plc, Chr. Hansen Holding A/S, DuPont de Nemours, Inc., Yakult Honsha Co., Ltd., Nature's Bounty Co., Church & Dwight Co., Inc., Garden of Life (Nestlé Health Science), Probiotics International Ltd. (Protexin), Jarrow Formulas, Inc., Nutraceutix Inc., Koninklijke DSM N.V., PepsiCo, Inc., General Mills, Inc., NOW Health Group, Inc., Rainbow Light Nutritional Systems, Life-Space Group Pty Ltd, Culturelle (i-Health, Inc.). |

Frequently Asked Questions

The Digestive Health Supplements Market was valued at USD 12.22 Billion in 2025.

The expected CAGR of the Global Digestive Health Supplements Market during the forecast period is 7.77%

The Digestive Health Supplements Market will be valued at USD 25.83 Billion in 2035.

Probiotics held the largest share in the Digestive Health Supplements Market in 2025.

The North America led Digestive Health Supplements Market.

Get in Touch