Clinical Diagnostics Market Report Scope & Overview:

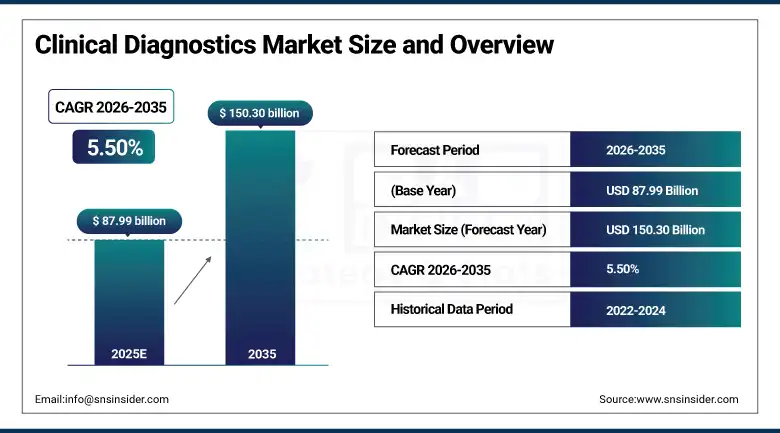

Clinical Diagnostics Market was valued at USD 87.99 billion in 2025 and is expected to reach USD 150.30 billion by 2035, growing at a CAGR of 5.50% from 2026-2035.

The clinical diagnostics market is growing due to rising prevalence of chronic and infectious diseases, increasing demand for early and accurate diagnosis, and expanding geriatric population. Technological advancements in molecular diagnostics, point-of-care testing, and automation are improving efficiency and accuracy. Growth in personalized medicine, preventive healthcare adoption, and expanding laboratory infrastructure in both developed and emerging healthcare systems are further driving steady market expansion over the forecast period.

The WHO projects global cancer cases will reach approximately 22 million annually by 2030, each requiring staging and monitoring diagnostic testing. The CDC reports that 38 million Americans have diabetes and 97 million have prediabetes both conditions requiring routine clinical laboratory monitoring as a standard of care.

Clinical Diagnostics Market Size and Forecast

-

Market Size in 2025: USD 87.99 Billion

-

Market Size by 2035: USD 150.30 Billion

-

CAGR: 5.50% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On Clinical Diagnostics Market - Request Free Sample Report

Clinical Diagnostics Market Trends

-

Rising prevalence of chronic and infectious diseases is driving the clinical diagnostics market.

-

Growing demand for early disease detection, preventive healthcare, and personalized medicine is boosting market growth.

-

Expansion of laboratory infrastructure, point-of-care testing, and home diagnostics is fueling adoption.

-

Increasing focus on faster turnaround times, accuracy, and cost-effective testing is shaping market trends.

-

Advancements in molecular diagnostics, immunoassays, and AI-enabled diagnostic tools are enhancing precision and efficiency.

-

Rising healthcare spending and awareness of routine health screening are supporting market expansion.

-

Collaborations between diagnostic companies, hospitals, and research institutions are accelerating innovation and global adoption.

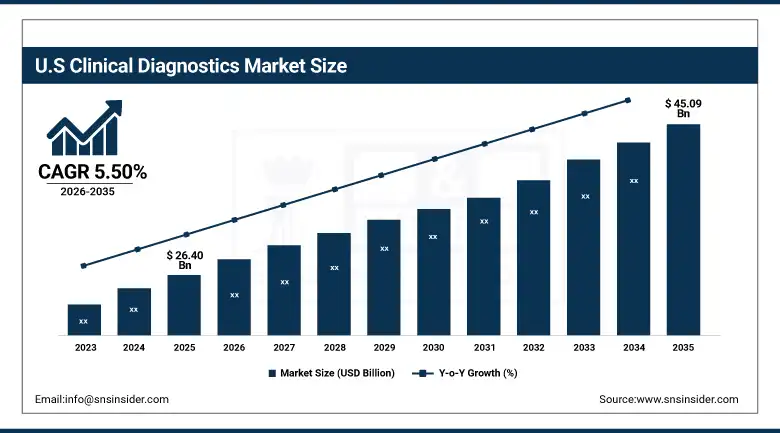

U.S. Clinical Diagnostics Market was valued at USD 26.40 billion in 2025 and is expected to reach USD 45.09 billion by 2035, growing at a CAGR of 5.50% from 2026-2035.

The U.S. clinical diagnostics market is growing due to rising chronic disease burden, increased demand for early and accurate diagnosis, advancements in molecular and point-of-care testing, and strong healthcare infrastructure. Adoption of personalized medicine and preventive screening further supports market expansion.

The CDC reports that U.S. clinical laboratories perform approximately 14 billion tests annually, making the U.S. the world's highest-volume diagnostic testing market. The Affordable Care Act's preventive care coverage mandate directly sustains routine clinical laboratory test volumes including lipid panels, glucose, and CBC testing at no out-of-pocket cost to insured patients.

Clinical Diagnostics Market Segment Highlights

-

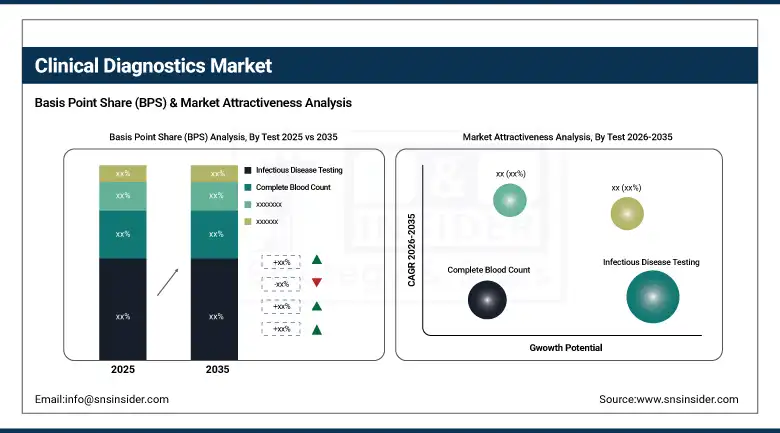

By Test, Infectious Disease Testing dominated with ~30.6% share in 2025; Complete Blood Count segment fastest growing (CAGR).

-

By Product, Reagents segment dominated the Clinical Diagnostics Market in 2025; Instruments segment fastest growing (CAGR).

-

By End User, Hospital Laboratory dominated the Clinical Diagnostics Market in 2025; Point-of-Care Testing fastest growing (CAGR).

Clinical Diagnostics Market Segment Analysis

By Test, Infectious Disease Testing segment dominates the Clinical Diagnostics Market, Complete Blood Count segment expected to grow fastest

Infectious Disease Testing held the largest share in the Clinical Diagnostics Market at about 30.6% in 2025. The rise in infectious disease incidence influenza, tuberculosis, HIV, hepatitis, and newer viral infections has driven sustained demand for accurate and timely diagnostic testing across all healthcare settings. Government and healthcare institutions globally have invested heavily in disease surveillance and early detection programs, creating institutional demand that runs independent of individual patient decisions.

Complete Blood Count testing is expected to grow at the fastest CAGR among test categories. CBC is about as foundational as clinical testing gets it is ordered in virtually every emergency room visit, as part of most routine annual checkups, and as standard monitoring for patients on medications affecting bone marrow function. The growing prevalence of chronic conditions that require CBC monitoring including diabetes-related anemia, chronic kidney disease, and chemotherapy-associated cytopenias means the underlying patient population requiring regular CBC testing is expanding continuously.

By Product, Reagents segment dominates the Clinical Diagnostics Market, Instruments segment expected to grow fastest

Reagents led the Clinical Diagnostics Market and generated the highest product revenue in 2025. Reagents are consumed in every test, while instruments are purchased once and maintained for years. Every sample that runs through a hematology analyzer, every immunoassay on a chemistry platform, every PCR reaction in a molecular lab consumes a defined quantity of reagents from that analyzer's manufacturer. This creates a large, predictable, and recurring revenue stream that grows proportionally with testing volume which is itself growing steadily.

Instruments is the fastest-growing product segment, driven by continuous innovation in diagnostic technology. Automated systems, AI-driven diagnostic equipment, and advanced testing instruments are enhancing the speed, accuracy, and efficiency of diagnostic procedures in ways that compel equipment investment cycles. The shift toward point-of-care platforms which require new instrument categories suitable for decentralized settings is creating incremental instrument demand that traditional central laboratory equipment does not serve.

By End User, Hospital Laboratory segment dominates the Clinical Diagnostics Market, Point-of-Care Testing segment expected to grow fastest

Hospital Laboratories held the dominant end-user share in 2025. Their position makes practical sense hospitals generate the highest concentration of diagnostic testing events because they serve the sickest patients who require the most comprehensive and urgent diagnostic workups. Hospital laboratories are equipped with the broadest analyzer portfolios, serving everything from stat chemistry panels in the emergency department to specialized endocrinology and immunology testing for complex inpatients.

Point-of-Care Testing is growing the fastest because the healthcare system has compelling structural reasons to want it. Decentralizing testing reduces emergency department congestion, enables faster treatment decisions in urgent care and primary care settings, and extends diagnostic access to underserved communities without central laboratory infrastructure. The technology has caught up with the ambition: modern POCT platforms can run multiplex respiratory panels, cardiac biomarker assays, and metabolic testing in 15-20 minutes with sensitivity approaching central laboratory performance.

Clinical Diagnostics Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

50% |

North America Clinical Diagnostics Market Insights

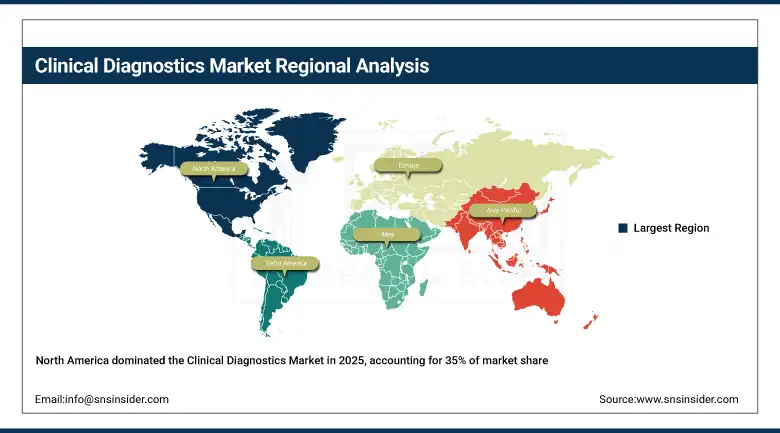

North America led the Clinical Diagnostics Market with the highest share of 35% in 2025, driven by its well-established healthcare infrastructure, high per-capita healthcare expenditure, and heavy emphasis on research and development. The United States specifically leads through widespread use of advanced diagnostic technologies molecular diagnostics and point-of-care testing in particular combined with strong government programs that sustain testing volume. The Affordable Care Act expanded access to preventive healthcare services including routine laboratory testing, ensuring broad insurance coverage for diagnostic procedures that maintains high testing volumes across the population. Major diagnostic product launches and partnerships among industry leaders are concentrated in North America, reinforcing the region's position as the primary commercial launch market for innovative diagnostic products.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. Centers for Medicare & Medicaid Services (CMS) annually updates its Clinical Laboratory Fee Schedule, the reimbursement framework covering hundreds of diagnostic tests performed for Medicare beneficiaries. Government initiatives supporting cancer early detection programs including NCI-funded multi-cancer early detection research are generating new diagnostic test categories that are being commercially developed by U.S. diagnostics companies.

Asia Pacific Clinical Diagnostics Market Insights

Asia Pacific is growing at a fast pace, fueled by better healthcare infrastructure, rising government expenditure on healthcare, and increasing awareness about early disease detection across the region. China, India, and Japan are seeing significant growth in diagnostic technology adoption, with molecular and genetic testing gaining particular traction. The region's healthcare expansion is supported by an aging population, rising chronic disease incidence, and growing demand for point-of-care solutions in geographically dispersed communities. Increased disposable incomes and improved healthcare access in emerging markets are additionally fueling diagnostic demand in ways that project continued above-average growth through the forecast period.

India's government Ayushman Bharat program providing health insurance to over 500 million low-income citizens has driven significant public investment in diagnostic infrastructure at government hospitals and empaneled private facilities. China's National Medical Products Administration (NMPA) has created accelerated review pathways for innovative in-vitro diagnostic products, stimulating both foreign market entry and domestic company innovation.

Europe Clinical Diagnostics Market Insights

Europe maintains a significant position in the global clinical diagnostics market, with Germany, France, the UK, and Switzerland as the primary markets. Strict quality standards enforced through the EU In Vitro Diagnostic Regulation (IVDR) which substantially raised conformity requirements for diagnostic products placed in the EU market are reshaping the competitive landscape by raising barriers for lower-quality products while supporting premium positioning for certified diagnostic companies. European public health systems generate consistent testing volumes through universal healthcare coverage, and increasing interest in preventive medicine and chronic disease management programs is sustaining growth in routine testing volumes across the region.

The EU In Vitro Diagnostic Regulation (IVDR 2017/746) increased scrutiny and clinical evidence requirements for diagnostic products sold in Europe, with full implementation reached in 2025. The European Centre for Disease Prevention and Control (ECDC) surveillance programs sustain significant ongoing demand for infectious disease diagnostic testing across EU member state public health laboratory networks.

Middle East & Africa and Latin America Clinical Diagnostics Market Insights

Both regions are experiencing growth in clinical diagnostics adoption driven by healthcare infrastructure investment, rising disease burden, and government commitment to improving diagnostic access. In the Middle East, Saudi Arabia and UAE are investing in advanced laboratory infrastructure at new hospitals and clinics under their respective national healthcare expansion programs. Africa represents a significant long-term opportunity as infectious disease burden including HIV, tuberculosis, and malaria drives demand for point-of-care testing suited to resource-limited settings.

The Africa Centres for Disease Control and Prevention (Africa CDC) Partnership to Accelerate COVID-19 Testing (PACT) expanded diagnostic laboratory infrastructure across 55 member states, establishing testing networks that are now being applied to broader infectious disease surveillance programs. Brazil's National Health Surveillance Agency (ANVISA) regulates in vitro diagnostic products under RDC standards aligned with international frameworks, supporting investment by major diagnostic multinationals in the Brazilian market.

Clinical Diagnostics Market Growth Drivers:

-

Rising chronic disease burden and AI-powered diagnostic innovation driving sustained global clinical diagnostics investment

The clinical diagnostics market grows when more people need more tests and both variables are moving in the right direction simultaneously. Chronic disease prevalence is rising globally across diabetes, cardiovascular disease, chronic kidney disease, and cancer, each requiring ongoing monitoring through clinical laboratory tests throughout the patient's treatment journey. Simultaneously, new diagnostic technology is creating test categories that did not previously exist: liquid biopsy cancer screening, pharmacogenomic testing to match patients to appropriate drug therapies, and multi-analyte point-of-care panels that replace sequences of single tests with simultaneous results.

The WHO estimates that access to essential diagnostic testing prevents an estimated 1.5 million deaths annually through enabling earlier treatment. The National Institutes of Health reports that molecular diagnostic test categories are growing at nearly double the rate of the overall in vitro diagnostics market, reflecting the technology's expanding clinical applications.

Clinical Diagnostics Market Restraints:

-

High equipment costs and strict regulatory requirements limiting diagnostic adoption in resource-constrained healthcare settings

Cost and regulation are the two structural constraints that genuinely slow the clinical diagnostics market's growth potential. Diagnostic devices, reagents, and high-end test kits can be extremely expensive particularly for smaller medical facilities in low-income countries where equipment procurement budgets are limited and reagent supply chains are fragmented. Genetic and orphan disease testing, which holds significant clinical value in identifying rare conditions and matching patients to targeted therapies, often carries costs far beyond what most healthcare systems can routinely reimburse, limiting real-world access.

Clinical Diagnostics Market Opportunities:

-

Personalized medicine expansion and home diagnostic testing demand creating new clinical diagnostics growth opportunities

Personalized medicine is one of the most compelling growth stories in clinical diagnostics because it directly multiplies the number of tests required per patient. Instead of a single diagnostic confirming a disease, genomic and biomarker testing identifies which specific variant of that disease a patient has, which therapeutic targets are present, and which treatment regimen is most likely to work each question answered by a different test. Cancer diagnostics in particular is moving in this direction rapidly, with companion diagnostic tests required for targeted therapy eligibility assessment at each treatment decision point. Outside oncology, pharmacogenomic testing identifying how individual patients will metabolize specific drugs is gaining traction in psychiatry, cardiology, and pain management.

Recent Developments:

-

2025: Roche launched expanded clinical chemistry test menus for its cobas Pro integrated laboratory system, adding 15 new cardiac biomarker and metabolic tests to the platform's menu to support hospital laboratories seeking to consolidate testing workflows from multiple platforms onto a single high-throughput analyzer architecture.

-

2025: Abbott received FDA 510(k) clearance for its Alinity i high-sensitivity cardiac troponin assay with improved analytical sensitivity enabling earlier rule-out of acute myocardial infarction within one hour of patient presentation in emergency department settings, representing a significant clinical advancement in time-critical cardiac diagnostic testing.

-

2026: Siemens Healthineers announced full commercial availability of its Atellica CI 1900 integrated analyzer system for hospital laboratories, combining immunoassay and clinical chemistry testing on a single platform with AI-powered maintenance prediction that reduces unplanned analyzer downtime by automatically scheduling maintenance before component failures occur.

Clinical Diagnostics Market Key Players

Some of the Clinical Diagnostics Market Companies

-

Abbott

-

bioMerieux SA

-

QuidelOrtho Corporation

-

Siemens Healthineers AG

-

Bio-Rad Laboratories, Inc.

-

Qiagen

-

Sysmex Corporation

-

Charles River Laboratories

-

Quest Diagnostics Incorporated

-

Agilent Technologies, Inc.

-

Danaher Corporation

-

F. Hoffmann-La Roche Ltd.

-

Thermo Fisher Scientific

-

Becton Dickinson and Company

-

bioMerieux SA

-

Hologic Inc.

-

Ortho Clinical Diagnostics

-

Luminex Corporation (DiaSorin)

-

Myriad Genetics, Inc.

-

Guardant Health, Inc.

| Report Attributes | Details |

|---|---|

|

Market Size in 2025 |

USD 87.99 billion |

|

Market Size by 2035 |

USD 150.30 Billion |

|

CAGR |

CAGR of 5.50% From 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Test [Lipid Panel, Liver Panel, Renal Panel, Complete Blood Count, Electrolyte Testing, Infectious Disease Testing, Other Tests] |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

|

Company Profiles |

Abbott, bioMérieux SA, QuidelOrtho Corporation, Siemens Healthineers AG, Bio-Rad Laboratories, Inc., Qiagen, Sysmex Corporation, Charles River Laboratories, Quest Diagnostics Incorporated, Agilent Technologies, Inc., Danaher Corporation, F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific, Becton Dickinson and Company, Hologic Inc., Ortho Clinical Diagnostics, Luminex Corporation (DiaSorin), Myriad Genetics, Inc., Guardant Health, Inc. |

Frequently Asked Questions

Ans: North America dominated the Clinical Diagnostics Market in 2025.

Ans: Point-of-Care Testing is expected to register the fastest CAGR in the Clinical Diagnostics Market through 2035.

Ans: Significant advancements in diagnostic technologies, including the rise of molecular diagnostics, digital health tools, and AI-driven diagnostics.

Ans: The Clinical Diagnostics Market was valued at USD 87.99 billion in 2025.

Ans: The Clinical Diagnostics Market is expected to grow at a CAGR of 5.50% from 2026 to 2035.

Get in Touch