Digital Advertising Market Report Scope & Overview:

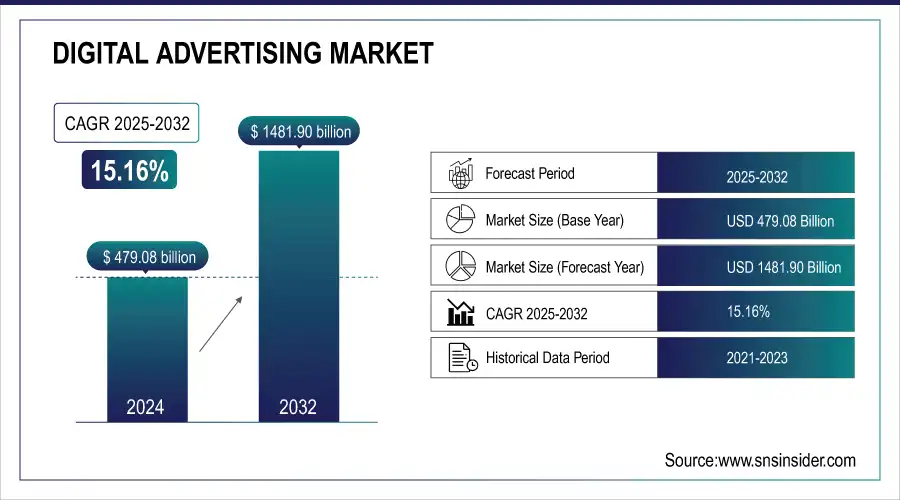

The Digital Advertising Market Size was valued at USD 479.08 Billion in 2024 and is expected to reach USD 1481.90 Billion by 2032 and grow at a CAGR of 15.16% over the forecast period 2025-2032.

Get more information on Digital Advertising Market - Request Sample Report

A key market growth is the rising penetration of the Internet and the widespread adoption of smartphones, which have led to a more expansive online ad audience. With consumers spending the majority of their time on digital platforms, advertisers have been dedicating less and fewer dollars to traditional media like TV & print, focusing more on digital channels. With the advent of social media platforms, search engines, and streaming services, advertisers were given fresh personalized tools to reach the right people. Moreover, the development of artificial intelligence (AI) and data analytics, which enable more personalized and efficient ad targeting will help the companies maximize the investment made on ads and achieve better return on investment (ROI). The world as of 2024 has 5.52 billion Internet users or 67.5% of the global population. There are more than 7 billion Smartphone users around the planet, and an average of 143 minutes each day is spent by internet users on social media. U.S. digital ad spend exceeded USD 25 billion and 3.3T impressions were served in Q1 2024 Moreover, AI is going to increase the efficiency level of ad targeting by 30–40%, leading to more personalized and effective campaigns.

Digital Advertising Market Size and Forecast:

-

Market Size in 2024: USD 479.08 Billion

-

Market Size by 2032: USD 1481.90 Billion

-

CAGR: 15.16% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

Digital Advertising Market Highlights:

-

Global digital advertising growth driven by e-commerce boom; total global e-commerce sales in March 2024 reached USD 6.09 trillion with 2.14 billion online shoppers.

-

Google Ads leads SEM with annual spend over USD 200 billion; Facebook and Instagram combined revenue USD 35 billion; YouTube has 2 billion monthly users.

-

Video advertising dominates engagement, fueled by platforms like YouTube and TikTok; 70% of digital video consumed on mobile.

-

Programmatic advertising adoption rises with AI and big data, enhancing targeting, efficiency, and ROI; 75% of global display ads purchased programmatically.

-

Real-time bidding (RTB) accounts for 50% of programmatic media; 40% of programmatic campaigns use AI for real-time optimization.

-

Market challenges include rising ad fraud and stricter privacy regulations (GDPR, CCPA) limiting data collection for targeted ads.

E-commerce adoption, especially post-COVID-19, is also a significant driver of digital advertising growth. With the rising momentum of online shopping, businesses are aware that they need to maintain a strong digital presence or risk losing market share. This change has led to a greater number of digital ad undeniable fact that paintings in driving sales such as search engine marketing (SEM), social media ads, video ads, and many others. Additionally, inventions such as programmatic and real-time bidding (RTB) have expedited digital ad purchasing, bringing efficiency and scalability improvements. Together with changing consumer behaviors and the continuous growth of the digital space, these factors are driving the persistent growth of the digital ad market. March 2024 total global e-commerce sales were USD 6.09 trillion with 2.14 billion online shoppers. Google Ads is still the king of SEM with annual ad spend exceeding USD 200 billion, while the combined ad revenue of Facebook and Instagram amounted to USD 35 billion. YouTube has 2 billion monthly users, with views on mobile driving 70% of views, and is responsible for much of the growth within video ads. U.S. display ads 88.2% bought programmatically Global programmatic transactions USD 595 billion Real-time bidding 50% of programmatic media traded via RTB.

Digital Advertising Market Drivers:

-

Video Content Dominates Digital Advertising Growth with High Engagement Mobile Consumption and Platform Expansion

The increasing significance of video content on different digital platforms is one of the major factors attributed to the growth of the digital advertising market. As video advertising has become one of the most captivating, appealing forms of content for consumers to engage with, it may be one of the best tools in the advertiser's arsenal. The growth of video streaming platforms like YouTube and TikTok, as well as streaming services like Netflix and Hulu, have played a massive role in driving up the consumption of video ads. Video ads offer advertisers the richness of an interactive medium with high-impact engagement − short-form ads, live-streaming, or long-form. Video ads also do an excellent job of demonstrating products or services more visually and engagingly, leading to higher engagement and, subsequently, larger returns on investment for advertisers. Given the rise in mobile device use to consume video, this format should continue to be one of the main engines of growth within the digital advertising space. According to 2024 statistics, 92% of internet users consume online video content and 1 billion hours of video is watched on YouTube every day. 70% of digital video consumption comes from smartphones, and 75% of all video plays are on mobile. YouTube has 2 billion monthly users and 70% of views from mobile. Over on TikTok, the short-form video platform broke through 1 billion monthly active users while users spent an average of 52 minutes per day on the app. These trends indicate the increasing highness of video files, particularly on cell phones.

-

Programmatic Advertising Drives Digital Market Growth with Automation AI Big Data and Real-Time Bidding

The growing acceptance of programmatic advertising is another major factor driving the digital advertising market. Programmatic advertising refers to the automated buying and selling of online ads through a sophisticated blend of technology and algorithms. This form of advertisement delivery guarantees ads are served to the appropriate audience, at the appropriate time. The transition from manual ad procurement to automated processes has streamlined advertising campaigns, making them more effective, cheaper, and scalable. Programmatic offers RTB and optimization, but it also enhances targeting accuracy through the use of big data i.e. data collected from consumer behavior. Programmatic advertising is made to grow more as it helps enhance ad performance and return on investment by utilizing sophisticated data-driven insights. The scale of advertising campaigns it manages and the richness of the analytics it provides into advertiser behavior make it a major engine of the digital advertising market, driving the overall migration from static, traditional advertising to a more fluid, automated form of advertising. In 2024, 75% of global digital display ads were purchased programmatically, yet 50% of those were purchased via real-time bidding (RTB). 35% of video ads were programmatic and big data was used for targeting 70% of campaigns. Moreover, 40% of programmatic campaigns apply AI for real-time optimization to enhance ad performance ROI.

Digital Advertising Market Restraints:

-

Rising Ad Fraud and Privacy Regulations Pose Major Challenges to the Growth of Digital Advertising Market

The digital advertising market suffers from one of the biggest ad fraud problems. With the evolution of digital ads, the more advanced the fraud activities come i.e. click fraud and fake impressions. This can result in ad budgets going to waste, and this makes marketing campaigns ineffective. This means advertisers are always having to scramble and always on the lookout to ensure their ad dollars do indeed reach real humans through much more than cast-iron monitoring tools and anti-fraud technologies. Privacy concerns and regulations are another major limitation. As consumers become more conscious about data privacy, and with regulations such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) coming into full effect, advertisers have to navigate a host of legal factors surrounding the use of consumer data. It restricts the amount of data that advertisers can collect for targeting and tracking, which in turn means ads will not be so targeted. Even with major advances in privacy protection from companies like Apple and the European Union, striking the balance between targeting customers with efficient and relevant ads and proper consumer privacy remains a challenge for marketers in the digital advertising space.

Digital Advertising Market Segment Analysis:

By Platform

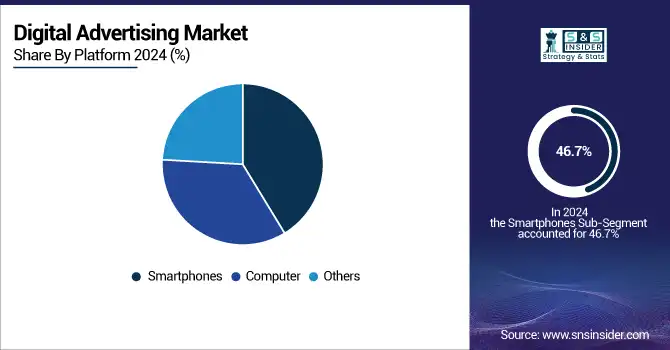

Smartphones dominated the digital advertising market in 2024 accounting for 46.7% of the total share. Mobile phones provide advertisers with the possibility to target users with location-based services and ads, mobile apps, and social media platforms, which enables advertisers to impact consumers profoundly. Mobile internet usage growth and increase in app use time as well as mobile commerce (m-commerce) are the biggest enablers of this domination. Advertisers can reach users wherever they are in the world at any time on mobile, leading to greater engagement and conversions. The seamless adoption of mobile devices into consumers' bone structure has designed them to the partners for investigating imitation for digital advertising.

Computers are anticipated to have the highest CAGR during the forecast period of 2025-2032. With the rise in productivity tools, remote work, and digitized services across various sectors, targeted advertising on computers (desktops, laptops, and tablets) is becoming more widespread. Also, computers have bigger screen real-estate, allowing for more immersive and functional ad formats and placements like long-form video and HD banners. Increasing e-commerce usage on desktops and the expansion of digital subscriptions and services (e.g., streaming, and software tools) will catalyze computer-based advertising and pull forward revenue growth for the segment.

By Offering

Solutions remained the largest segment in the digital advertising market in 2023 with 67.7% of the market. Solutions such as programmatic advertising platforms, analytics tools, and automated bidding systems empower advertisers to target their intended audiences much more accurately and efficiently. With businesses increasing their focus on data-driven strategies and technology to enhance advertising efficiencies, the need for end-to-end advertising solutions is rising. These solutions have become fundamental in the marketer's toolkit as organizations have wanted to combine data analytics, machine learning, and real-time optimization all under one umbrella to drive ROI and customer engagement.

Services are projected to grow at the highest CAGR between 2024 and 2032 owing to the rising demand for specialized expertise in managing and optimizing digital campaigns. With increased complexity in digital advertising, the current trend for businesses is to rely on an agency and third-party solution provider for services like campaign management, creative services, data analytics, as well as social media strategy. These services empower businesses to utilize the power of digital platforms, particularly for a myriad of functions ranging from influencer marketing, and content creation, to multi-platform campaigns. In a rapidly changing digital landscape, coupled with increasing demand for personalized marketing, the need for specialist services will expand, allocating the largest surge over the coming years in this category.

By Type

Search Advertising was the leading digital ad format in 2024, taking 37.5% of the total, continuing to benefit from the high specificity of its targeting options and the worldwide scale of search engines such as Google. With search advertising, advertisers can target users in the immediate moment that they are searching for certain products, services, or information. Because the user is already interested in what's being advertised, this intention-based advertising format results in higher conversion rates. This, in addition to the fact that search ads are less disruptive than other types of ads and are therefore more attractive to customers, is why search ads will continue to prevail. Search adverts have remained a mainstay of digital internet marketing tactics because of the potential to accurately target key phrases, and provide targeted adverts.

Interstitial Advertising is anticipated to witness the fastest CAGR during 2025-2032. Highly engaging in nature, ad placements captured in interstitials are usually full-screen ads coming in between the natural transitions of the app or website. As Mobile apps and games are becoming popular, interstitial ads can catch your attention completely during a user experience. With mobile continuing to grow globally, particularly for gaming and other app-based scenarios interstitial ads are becoming a popular and effective tool for advertisers. It can deliver rich, high-impact, non-skippable ads that are likely to accelerate the adoption and growth trajectory of this format making them a very important part of the future digital ad ecosystem.

By Format

Video continued its dominance in the digital advertising market in 2024, accounting for 46.3% of their share. Video ads allow advertisers to communicate more complicated messages and demonstrate their products in dynamic and visually appealing ways. This dominance has largely been fueled by the rising demand for video consumption on platforms like YouTube, TikTok, Instagram, and streaming services. Video is more engaging and promotes a better experience, which means consumers engage with them more and develop a stronger emotional connection. With the advent of short-form, live streaming, and video-centric social media, video advertising continues to be in the driver's seat, buoyed by improving mobile devices and broadband connectivity.

Text is anticipated to exhibit the fastest-growing CAGR (Cumulative Annual Growth Rate) from 2025 to 2032. Text-based advertising on platforms like search engine ads, display ads, and text in social media posts provides advertisers with a simple and quick way to get their specific messages to consumers. AI-powered marketing has changed how things work now, especially with personalized text-based ads. Additionally, they are ideal for low-bandwidth platforms or environments with very short engagement, like mobile and chat-based ads. Supported by the constant evolution of these platforms and technologies, text-based advertising is likely to face increasing demand and is expected to grow faster than other ad formats.

By End-Use Industry

Retail accounted for 30.5% of digital advertising spending in 2024, continuing the trend from previous years that reflects the sector's significant dependence on digital channels to reach consumers. When it comes to websites retailers have become better at driving them to make purchases as well, particularly around unrealistic holiday shopping times or other season sales events. With the boom of e-commerce, digital advertising in retail has rapidly expanded, targeting the consumption behavior of consumers who are online browsing or searching for products to buy. In e-commerce, digital channels like search engines, social media, and video ads will be used by retail advertisers to hook prospective buyers, enticing them with personalized experiences and deals to evoke purchase behaviors. Coupled with high-volume consumer interest and fast-moving commerce, it has left retail at the forefront of digital advertising.

Education is projected to have the highest CAGR growth from 2025 to 2032 due to the rising trend of online learning and the rising demand for digital marketing in the education industry. With the increasing number of educational institutions, online courses, and e-learning platforms, everyone is targeting students and learners through digital advertising. This encompasses strategies such as search and display ads for prospecting students and employing social media and video content to create brand visibility. Increasing conversion of classrooms to digital and remote-based learning after the pandemic is driving the demand for digital-based education advertisements. Finally, with the continued evolution of education technology, personalized messaging for students, and promotion of online courses and virtual events, education will become one of the fastest-growing categories of digital advertising in the next ten years.

Digital Advertising Market Regional Analysis:

North America Digital Advertising Market Trends:

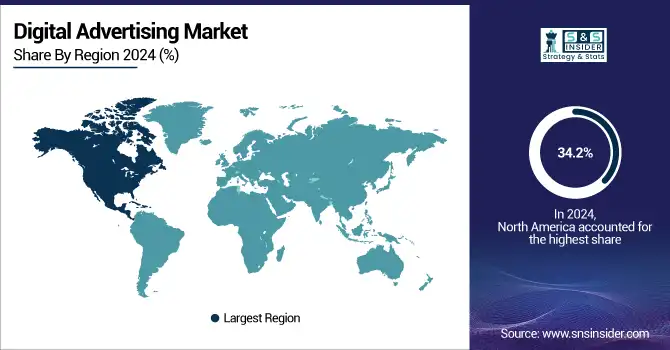

In 2024, North America held the largest share of the digital advertising market at 34.2%, primarily due to high internet penetration, a better technological infrastructure, and the presence of major tech giants like Google, Facebook (Meta), and Amazon. Digital advertising markets are most mature in North America, offering advertisers the ability to access large, diverse audiences across multiple channels including search, social, and video. The region's aggressive approach towards data-driven marketing and innovations such as programmatic advertising has further played an integral part in its dominance. For instance, Amazon's advertising platform, which helps retailers gain the attention of shoppers on its e-commerce site, is one of the most successful in the realm, allowing businesses the ability to reach a delicately wide statistic.

Need any customization research on Digital Advertising market - Enquiry Now

Asia-Pacific Digital Advertising Market Trends:

Asia Pacific is projected to have the highest growth CAGR from 2025 to 2032. Faster adoption of smartphones, expanding middle class, and growing digital platforms in nations such as India, China, and Southeast Asia are accountable for the high regionally-based spending. Key drivers of the growth of digital ads in the region include a disproportionate shift from traditional to digital media and high investments in mobile and video ads. For example, TikTok, a short video app that is massive in Asia, seems to be crushing the digital ad game. Brands are using TikTok's algorithm to their advantage to connect with younger audiences with hyper-creative personalized content. Likewise, in China, Alibaba and Baidu built huge digital advertising ecosystems to target tens of millions of consumers through mobile access, e-commerce marketing, and search engine marketing. With fast-growing internet penetration and usage of mobile internet, Asia Pacific has become one of the fundamental growth engines of digital advertising.

Europe Digital Advertising Market Trends:

Europe maintains steady growth in digital advertising, supported by high digital literacy and mature marketing ecosystems. Advertisers benefit from platforms like Google, Meta, and programmatic networks to reach diverse audiences across search, social, and video. Growth is fueled by increasing adoption of video, mobile, and programmatic advertising. Privacy regulations, such as GDPR, influence strategies, prompting more transparent and targeted campaigns.

Latin America Digital Advertising Market Trends:

Latin America is an emerging digital advertising market with rapid smartphone penetration and growing social media usage. Growth is primarily driven by mobile and social media advertising on platforms like Facebook, Instagram, and TikTok. Increasing investments in programmatic and video ads reflect the region’s ongoing shift from traditional media to digital channels.

Middle East & Africa Digital Advertising Market Trends:

The Middle East & Africa market is expanding due to rising internet penetration, mobile adoption, and growth of digital platforms. Social media platforms, including Facebook, Instagram, and TikTok, dominate digital engagement. Brands are increasingly leveraging programmatic and mobile-first campaigns, driving continued market development.

Digital Advertising Market Key Players:

-

Adobe (Adobe Experience Cloud, Adobe Advertising Cloud)

-

The Trade Desk (Demand-Side Platform, Data Management Platform)

-

WPP plc (GroupM, Ogilvy)

-

Omnicom Group (BBDO Worldwide, DDB Worldwide)

-

Publicis Groupe (Publicis Media, SapientRazorfish)

-

Google (Google Ads, Google Marketing Platform)

-

Facebook (Facebook Ads, Instagram Ads)

-

Amazon (Amazon Advertising, Amazon DSP)

-

Microsoft corporation (Microsoft Advertising, LinkedIn Ads)

-

Snap Inc. (Snap Ads, Snap Audience Network)

-

TikTok (TikTok Ads, TikTok For Business)

-

Twitter (Twitter Ads, Twitter Amplify)

-

LinkedIn (LinkedIn Ads, LinkedIn Marketing Solutions)

-

Spotify (Spotify Ads, Spotify Ad Studio)

-

Pinterest (Pinterest Ads, Pinterest Business)

-

Reddit (Reddit Ads, Reddit Promote)

-

Yahoo (Yahoo Ads, Yahoo Gemini)

-

Taboola (Taboola Feed, Taboola Newsroom)

-

Outbrain (Outbrain Amplify, Outbrain Engage)

-

Criteo (Criteo Dynamic Retargeting, Criteo Sponsored Products)

Some of the Raw Material Suppliers for Digital Advertising Companies:

-

Intel Corporation

-

Advanced Micro Devices (AMD)

-

NVIDIA Corporation

-

Qualcomm Incorporated

-

Broadcom Inc.

-

Micron Technology, Inc.

-

Taiwan Semiconductor Manufacturing Company (TSMC)

-

Samsung Electronics

-

Seagate Technology

-

Western Digital Corporation

Digital Advertising Market Competitive Landscape:

Adobe Inc., established in 1982, is a global leader in digital media and digital marketing solutions. The company develops industry-standard creative software, including Photoshop, Illustrator, and Premiere Pro, and provides innovative digital experience platforms for businesses to manage content, analytics, and marketing campaigns. Adobe continues to drive creativity, productivity, and digital transformation worldwide.

-

In October 2024, Adobe launched GenStudio for Performance Marketing, a generative AI tool designed to help marketing and creative teams accelerate campaign creation and optimization across platforms. The tool integrates with major platforms like Google, Meta, and TikTok to deliver personalized content at scale.

The Trade Desk, established in 2009, is a leading global technology company specializing in programmatic digital advertising. The company provides a demand-side platform (DSP) that enables advertisers to purchase and manage data-driven digital ad campaigns across display, video, audio, and connected TV. The Trade Desk focuses on innovation, transparency, and maximizing return on ad spend for clients worldwide.

-

In January 2025, The Trade Desk announced an agreement to acquire Sincera, a data company specializing in digital advertising insights. This acquisition will enhance The Trade Desk's platform with improved data signals and transparency for programmatic advertising.

Omnicom Group Inc., established in 1986, is a global leader in marketing, communications, and advertising services. The company operates through a network of agencies offering advertising, media buying, public relations, and digital marketing solutions. Omnicom delivers integrated campaigns for clients worldwide, leveraging creativity, data-driven insights, and strategic expertise to drive brand growth and market impact.

-

In August 2024, Omnicom launched the Omnicom Advertising Group (OAG), consolidating its creative networks like BBDO, DDB, and TBWA to drive innovation and growth.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 479.08 Billion |

| Market Size by 2032 | USD 1481.90 Billion |

| CAGR | CAGR of 15.16% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Computer, Smartphone, Others) • By Offering (Solution, Services) • By Type (Search Advertising, Banner Advertising, Video Advertising, Social Media Advertising, Native Advertising, Interstitial Advertising) • By Format (Text, Image, Video, Others) • By End Use Industry (BFSI, Automotive, IT & Telecommunication, Healthcare, Consumer Electronics, Retail, Media & Entertainment, Education, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Adobe, The Trade Desk, WPP plc, Omnicom Group, Publicis Groupe, Google, Facebook, Amazon, Microsoft, Snap Inc., TikTok, Twitter, LinkedIn, Spotify, Pinterest, Reddit, Yahoo, Taboola, Outbrain, Criteo. |

Frequently Asked Questions

In 2024, the North American region leads the Digital Advertising market, capturing approximately 34.25% of the total market share.

Restraints on the growth of the Digital Advertising Market include concerns over data privacy regulations, ad fraud, and consumer ad fatigue.

The major key drivers for the growth of the Digital Advertising Market include increased internet and mobile device penetration, the rise of social media platforms, and advancements in data-driven and programmatic advertising technologies.

The Digital Advertising Market Size was valued at USD 479.08 Billion in 2024 and is expected to reach USD 1481.90 Billion by 2032

The Digital Advertising Market is expected to grow at a CAGR of 15.16%.

Get in Touch