Digital Media Market Report Scope & Overview:

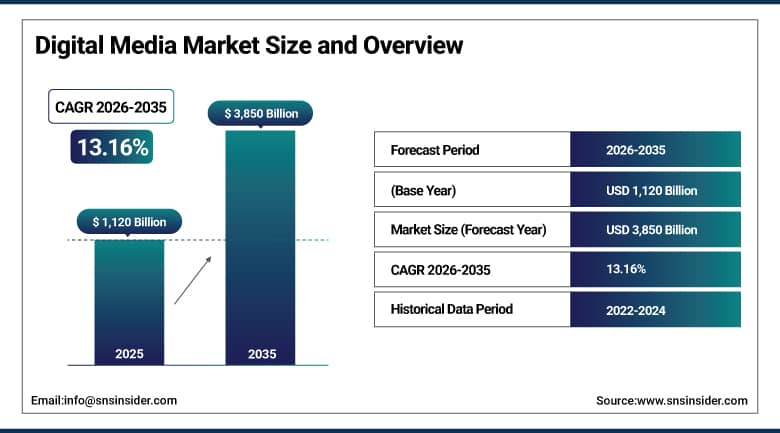

Digital Media Market was valued at USD 1,120 billion in 2025 and is expected to reach USD 3,850 billion by 2035, growing at a CAGR of 13.16% from 2026-2035.

The Digital Media Market is expanding owing to factors such as higher levels of internet connectivity, smartphone adoption, consumption of video and social media content, emergence of OTT services, development of digital advertising, and the need for more personalized and on-demand services.

The U.S. Bureau of Labor Statistics documents that Americans now spend an average of 4.1 hours per day consuming digital media more time than any other leisure activity including television. The ITU's Global Connectivity Report confirms that global internet users reached 5.4 billion in 2023, with over 400 million new connections added since 2021 alone.

Digital Media Market Size and Forecast

-

Market Size in 2025: USD 1,120 Billion

-

Market Size by 2035: USD 3,850 Billion

-

CAGR: 13.16% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Digital Media Market - Request Free Sample Report

Digital Media Market Trends

-

Generative AI tools are fundamentally reshaping content production economics what previously required a studio budget can now be produced with an AI co-pilot, collapsing the cost barrier for independent creators and small brand teams.

-

Short-form vertical video led by TikTok, Instagram Reels, and YouTube Shorts has become the dominant content discovery format among audiences under 35 globally, reshaping where advertising budgets flow.

-

Connected TV (CTV) advertising is growing at rates that outpace all other digital advertising channels as streaming platforms build out programmatic ad inventory on large living-room screens.

-

Podcast advertising has matured into a sophisticated measurable channel with dynamic ad insertion technology enabling campaign optimization that rivals search advertising in attribution quality.

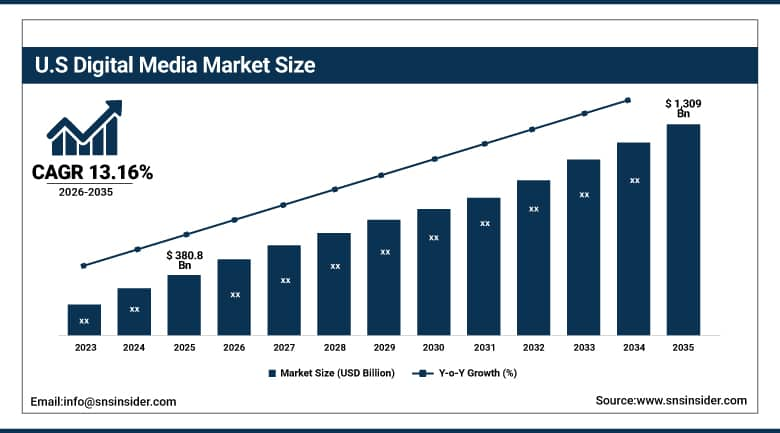

U.S. Digital Media Market was valued at USD 380.8 billion in 2025 and is expected to reach USD 1,309 billion by 2035, growing at a CAGR of 13.16% from 2026-2035.

The United States is the world's largest and most commercially sophisticated digital media market, hosting the global headquarters of every major platform YouTube, Netflix, Meta, Spotify, Amazon, and Apple that collectively define global content consumption patterns.

The Interactive Advertising Bureau's 2024 Internet Advertising Revenue Report documented that U.S. digital advertising reached USD 225 billion, with mobile accounting for 67% and connected TV growing at 25% year-over-year.

Digital Media Market Segment Analysis

-

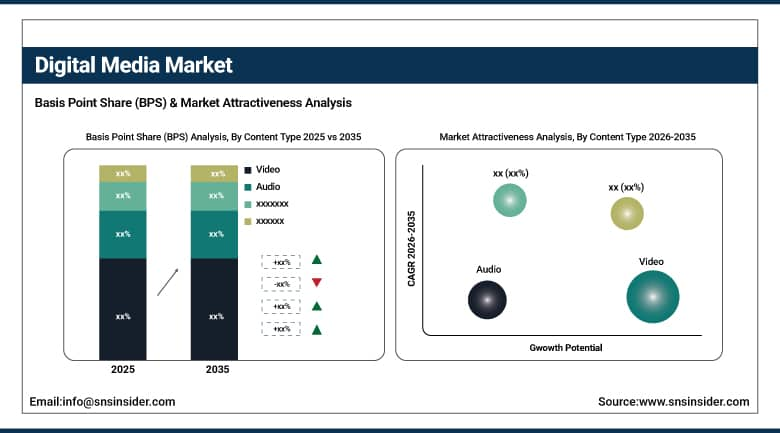

By Content Type, Video segment dominated with ~43% share in 2025; Audio segment expected to grow fastest at ~15.84% CAGR.

-

By Platform, Smartphone segment dominated with ~42% share in 2025; Computer segment expected to grow fastest at ~15.52% CAGR.

-

By Application, Marketing & Advertisement segment dominated with ~33% share in 2025; Streaming segment expected to grow fastest at ~15.26% CAGR.

-

By Industry Vertical, Entertainment segment dominated with ~27% share in 2025; Retail segment expected to grow fastest at ~15.20% CAGR.

By Content Type: Video dominates, Audio growing fastest

Video content held approximately 43% of the Digital Media Market in 2025, and that position reflects a reality about human attention that audio and text simply cannot compete with at the same engagement level. Video combines moving images, voice, music, and text overlay in a format that effortlessly holds viewer attention without requiring active reading or interpretation effort. The rise of streaming platforms Netflix, Amazon Prime Video, Disney+, HBO Max, and hundreds of regional equivalents has made professional-grade long-form video content available on-demand in every living room globally. YouTube's more than 800 million videos and its 2 billion monthly active users represent a different but equally powerful dimension of video dominance user-generated content that runs the full quality spectrum from smartphone selfie to near-studio-production quality, catering to niches that no traditional broadcaster would have found commercially viable.

Audio is the fastest-growing content type with a projected CAGR of approximately 15.84%, and the underlying driver is a form of consumption that no other format enables: you can listen while doing other things. Podcast audiences are not passive background listeners the way radio audiences historically were they are actively choosing shows, building habits around host relationships, and demonstrating purchase behavior that advertisers find consistently valuable. Spotify's podcast business now generates billions in revenue.

By Platform: Smartphone dominates, Computer growing fastest

Smartphones captured approximately 42% of the Digital Media Market in 2025, a leadership position that reflects two decades of mobile internet adoption converging with the rise of mobile-first content formats. The smartphone has become the default media consumption device for most of the world's population: 6.7 billion smartphones are in use globally, and in many markets particularly across Africa, South Asia, and Southeast Asia it is the only internet-connected screen a household possesses. Content platforms have designed their experiences around the smartphone form factor with a thoroughness that makes every other screen feel like an afterthought in some categories.

The computer segment encompassing desktops, laptops, and increasingly Chromebooks is expected to grow at the fastest platform CAGR of approximately 15.52% during the forecast period. Remote and hybrid work has restored the computer screen to centrality in daily life for hundreds of millions of professionals who previously used their devices only for workplace productivity. With those same computers now functioning as entertainment centers during off-hours, e-learning platforms during upskilling efforts, and gaming machines in leisure time, the intensity and variety of digital media consumption on computer platforms has expanded considerably.

By Application: Marketing & Advertisement dominates, Streaming growing fastest

Marketing and Advertisement held approximately 33% of Digital Media Market revenue in 2025, and the logic of its dominance is commercial rather than creative: digital media is where brand spending goes because digital media is where consumer attention lives. The measurability advantage of digital advertising over television or print is not marginal it is transformative. An advertiser running a campaign on a digital video platform can see, in real time, exactly how many people watched their ad, for how long, what they did next, and whether they ultimately purchased.

Streaming is expected to grow at the fastest application CAGR of approximately 15.26%, driven by the ongoing expansion of subscription video-on-demand services globally and the growing penetration of these services into lower-income market segments as pricing models diversify. The introduction of ad-supported tiers by Netflix, Disney+, and Max has simultaneously expanded subscriber base accessibility and created large new advertising inventory on premium streaming platforms closing the gap between streaming's audience scale and its advertising revenue potential.

By Industry Vertical: Entertainment dominates, Retail growing fastest

Entertainment held approximately 27% of the Digital Media Market by industry vertical in 2025, reflecting its position as both the largest producer and consumer of digital media content globally. The streaming wars the competitive investment by Netflix, Disney, Apple, Amazon, and dozens of regional platforms in original content production represent the largest single wave of entertainment content investment in history, with aggregate streaming content spending exceeding USD 200 billion annually when all platforms are included. Gaming's adjacency to entertainment digital media through game streaming on Twitch, esports broadcasts, game review content on YouTube, and the increasing integration of entertainment IP into game narratives creates a broad and overlapping entertainment digital media consumption ecosystem that sustains the segment's leadership.

Retail is projected to register the fastest industry vertical CAGR of approximately 15.20% through the forecast period, driven by the deepening integration of digital media into e-commerce purchase journeys. Every major e-commerce platform has built digital content capabilities Amazon's Live Shopping, Walmart's Vudu streaming, Shopify's media integration tools recognizing that consumers who engage with content convert at higher rates than consumers who search and browse without contextual content. The social commerce overlay where TikTok Shop, Instagram Shopping, and Pinterest enable purchase completion inside social video content further extends retail digital media's commercial reach.

Digital Media Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Asia Pacific |

China |

48% |

|

Europe |

United Kingdom |

24% |

|

Middle East & Africa |

UAE |

36% |

|

Latin America |

Brazil |

50% |

North America Digital Media Market Insights

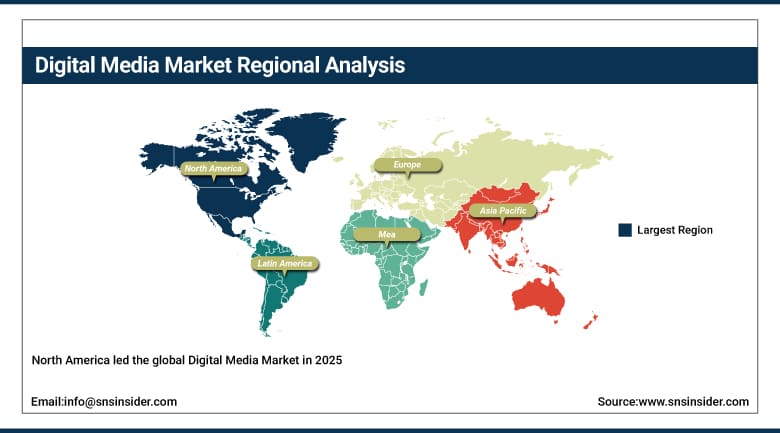

North America led the global Digital Media Market in 2025, and the U.S. market's dominance is anchored in structural advantages that extend well beyond market size. Silicon Valley's concentration of platform companies Alphabet, Meta, Apple, Amazon, Netflix, and Spotify means that the global platforms where digital media is consumed are primarily American-owned and American-engineered. That ownership shapes both product development and revenue capture in ways that are fundamentally different from markets where global platforms are external rather than domestic. The U.S. digital advertising ecosystem has reached a level of programmatic sophistication with auction dynamics, audience targeting, measurement attribution, and brand safety tools developed over two decades that other markets are still building toward. The country's high household income, willingness to pay for content subscriptions, and dense smartphone and broadband penetration collectively sustain per-capita digital media revenue that far exceeds any other national market.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Digital Media Market Insights

Asia Pacific is the fastest-growing regional Digital Media Market and will likely surpass North America in absolute scale within the forecast period, driven by China's enormous domestic digital ecosystem, India's rapidly expanding smartphone internet population, and the commercial maturity of South Korea and Japan's digital media industries. China's market operates on platforms that are entirely distinct from Western equivalents ByteDance (Douyin, Toutiao), Tencent (WeChat, QQ), Alibaba (Youku, Tmall), and Baidu collectively represent an autonomous digital media ecosystem of comparable scale to the entire Western internet. India represents the most dynamic market frontier: with 850 million smartphone users and rapidly growing data consumption, India's digital media market is adding users at a pace that no other country matches, though average revenue per user remains far below developed market levels.

Europe Digital Media Market Insights

Europe occupies an important but operationally complex position in the global Digital Media Market, where GDPR's data governance requirements have fundamentally shaped how digital advertising targeting operates, and where the Digital Markets Act is beginning to reshape how platform gatekeepers interact with publishers and advertisers. The UK, Germany, France, and the Nordic countries are the primary European digital media markets, with high smartphone penetration, strong subscription content culture, and sophisticated digital advertising ecosystems. European public broadcasting institutions BBC, ARD, RAI, and others have navigated the transition to digital with varying degrees of success, with the BBC's digital iPlayer and podcast strategy being among the most commercially successful public media digital transformations globally. GDPR's consent-based tracking requirements have reduced the depth of behavioral targeting available in European digital advertising, creating both a revenue headwind and an opportunity for contextual and cohort-based advertising approaches that do not depend on individual user tracking.

The European Data Protection Board's enforcement actions have resulted in aggregate GDPR fines exceeding EUR 4 billion against major digital media and advertising companies since the regulation came into force, reshaping data processing practices across the European digital advertising ecosystem.

Middle East & Africa Digital Media Market Insights

The Middle East and Africa represent two quite distinct digital media market stories within a single geographic classification. The Gulf Cooperation Council states particularly the UAE, Saudi Arabia, and Qatar are among the world's highest social media penetration countries by proportion of population, with highly affluent, mobile-first consumer bases that generate digital media revenue per user rates approaching Western markets. Saudi Arabia's Vision 2030 digital economy investment includes significant media and entertainment infrastructure development, with platforms including Anghami (Arabic streaming), Starzplay, and OSN building regional subscription content libraries. Africa's digital media opportunity is fundamentally different: a market of 1.4 billion people with rapidly expanding mobile internet access but limited monetization infrastructure, where the commercial digital media market is nascent relative to its eventual scale. Mobile money infrastructure development across East Africa is gradually creating the digital payment capability that enables content subscription models at meaningful scale.

Latin America Digital Media Market Insights

Latin America's digital media market is growing at rates above the global average, led by Brazil the largest national market by population and digital media spending alongside Mexico, Colombia, and Argentina. The region's young demographic profile (median age under 30 in most countries), very high social media engagement rates, and the rapid growth of mobile internet access through affordable 4G and expanding 5G networks create structural conditions for digital media market expansion. Music streaming has been a particular success story in Latin America, with regional genres reggaeton, funk carioca, and Latin pop generating global streaming volumes that outpunch the region's economic size. Digital advertising has historically been underdeveloped relative to the region's population scale, but improving programmatic infrastructure and growing e-commerce investment are both driving digital ad spend growth.

Digital Media Market Growth Drivers:

-

Mobile consumption explosion and AI-powered content personalization creating unstoppable digital media market expansion globally

The case for sustained digital media market growth does not require any single dramatic technology breakthrough it rests on the continued compounding of several forces that have been building for years. Mobile internet adoption keeps expanding into populations that previously lacked connectivity, bringing billions of new consumers into digital media ecosystems that are already monetized and growing. AI recommendation algorithms keep improving their ability to connect individual viewers with content they will engage with deeply, increasing the average time users spend inside digital media platforms. Production cost economics keep improving through AI-assisted creation tools, increasing the volume of quality content available and expanding the topics and formats creators can viably produce. Each of these forces individually would sustain market growth; their simultaneous operation creates a multiplier effect that makes the market's 13%+ CAGR entirely credible.

Cisco's Annual Internet Report projects that global IP traffic will reach 780 exabytes per month by 2026, with video streaming accounting for over 80% of total consumer internet traffic an infrastructure demand that reflects the foundational role of digital media in internet utilization.

Digital Media Market Restraints:

-

Data privacy regulations and cybersecurity risks creating compliance complexity limiting digital media market growth

Privacy regulation is the most consequential structural constraint on digital media market growth, particularly in advertising-supported segments. GDPR in Europe, CCPA in California, and the proliferation of similar frameworks across dozens of other jurisdictions are systematically reducing the behavioral data that digital media platforms can collect, process, and use for targeting and behavioral targeting has historically been the primary value proposition of digital advertising over traditional channels. Apple's App Tracking Transparency framework which defaults to opt-out for cross-app tracking on iOS reduced the targeting signal available to mobile advertisers in ways that directly affected revenue per impression on ad-supported platforms. The path forward involves investment in privacy-preserving alternatives, which exists and is progressing, but creates transition costs and period-of-transition revenue headwinds that constrain market growth during the adaptation phase.

Digital Media Market Opportunities:

-

Emerging market expansion and immersive media technology creating transformative new digital media growth opportunities globally

The billion-plus people who will join digital media ecosystems over the next decade overwhelmingly in Africa, South Asia, and Southeast Asia represent the largest single opportunity in the digital media market's history. Each new connected user becomes a potential content consumer, social media participant, streaming subscriber, and advertising target. The infrastructure challenge is no longer primarily coverage: affordable smartphones now reach price points below USD 50, and mobile data costs in many emerging markets have fallen to levels that make video streaming economically feasible. The commercial challenge is building monetization infrastructure payment systems, advertising networks, content libraries in local languages at the pace of new user growth. Platforms that invest ahead of this curve, building local content relationships and payment infrastructure before competitors, will capture user loyalty in the world's next billion digital media consumers.

Recent Developments:

-

2026: Netflix expanded its AI-powered content recommendation engine with real-time viewing context awareness, dynamically adjusting content surfacing based on time of day, device type, and session mood signals reportedly improving average session engagement by 18% versus the previous algorithm in controlled A/B testing across its 270 million global subscriber base.

-

2025: Spotify launched its Daylist feature into its AI DJ experience powered by a foundation model trained on 100 million users' listening patterns, enabling personalized playlist generation that changes hourly throughout the day matching music to inferred listener mood and activity context reaching 140 million monthly active listeners in its first year.

Digital Media Market Key Players

Some of the Digital Media Market Companies

-

Alphabet Inc. (Google/YouTube)

-

Meta Platforms Inc.

-

Netflix Inc.

-

Amazon.com Inc. (Prime Video/Twitch)

-

Apple Inc. (Apple TV+/Apple Music)

-

Spotify Technology SA

-

Microsoft Corporation (LinkedIn/Xbox Game Pass)

-

ByteDance Ltd. (TikTok/Douyin)

-

Comcast Corporation (NBCUniversal/Peacock)

-

The Walt Disney Company (Disney+/Hulu)

-

Warner Bros. Discovery Inc. (Max)

-

Snap Inc.

-

Pinterest Inc.

-

Twitter/X Corp.

-

Baidu Inc.

-

Tencent Holdings Ltd.

-

Alibaba Group (Youku/Tmall)

-

DAZN Group Ltd.

-

iHeartMedia Inc.

-

SiriusXM Holdings Inc.

Digital Media Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,120 Billion |

| Market Size by 2035 | USD 3,850 Billion |

| CAGR | CAGR of 13.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Content Type (Video, Audio, Text, Images, Others) • By Platform (Smartphone, Smart TV, Computer, Others) • By Application (Marketing & Advertisement, Streaming, Education, Gaming, Others) • By Industry Vertical (Entertainment, Retail, Healthcare, BFSI, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Alphabet Inc. (Google/YouTube), Meta Platforms Inc., Netflix Inc., Amazon.com Inc. (Prime Video/Twitch), Apple Inc. (Apple TV+/Apple Music), Spotify Technology SA, Microsoft Corporation (LinkedIn/Xbox Game Pass), ByteDance Ltd. (TikTok/Douyin), Comcast Corporation (NBCUniversal/Peacock), The Walt Disney Company (Disney+/Hulu), Warner Bros. Discovery Inc. (Max), Snap Inc., Pinterest Inc., Twitter/X Corp., Baidu Inc., Tencent Holdings Ltd., Alibaba Group (Youku/Tmall), DAZN Group Ltd., iHeartMedia Inc., SiriusXM Holdings Inc. |

Frequently Asked Questions

North America dominated the Digital Media Market in 2025.

Marketing & Advertisement dominated with approximately 33% share in 2025; Streaming is the fastest growing.

The Video segment dominated with approximately 43% share in 2025; Audio is the fastest growing segment.

The Digital Media Market was valued at USD 1,120 billion in 2025.

The Digital Media Market is expected to grow at a CAGR of 13.16% from 2026 to 2035.

Get in Touch