Digital Twin Grain Silo Market Report Scope & Overview:

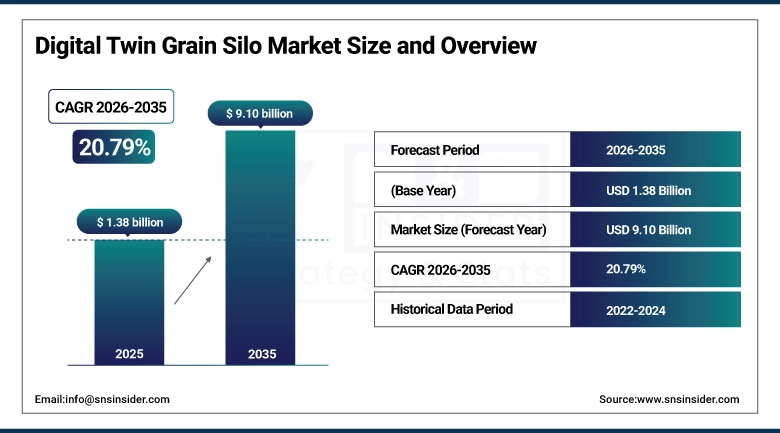

The Digital Twin Grain Silo Market Size was valued at USD 1.38 billion in 2025 and is expected to reach USD 9.10 billion by 2035 and grow at a CAGR of 20.79% over the forecast period 2026-2035.

The Digital Twin Grain Silo Market is growing at a rapid pace due to the burning need for efficiency and loss prevention in the agriculture industry. This technology allows for the creation of a dynamic virtual twin of real-world silos, which can be monitored and simulated in real-time. This technology has the power to enable the optimization of storage conditions, predict when maintenance is required, and prevent spoilage, thus ensuring the quality of the grain and maximizing its output.

Digital Twin Grain Silo Market Size and Forecast:

-

Market Size in 2025: USD 1.38 Billion

-

Market Size by 2035: USD 9.10 Billion

-

CAGR: 20.79%

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On Digital Twin Grain Silo Market - Request Free Sample Report

Key Digital Twin Grain Silo Market Trends:

-

Growing need to reduce post-harvest losses is driving adoption of real-time monitoring and control systems.

-

Rising integration of IoT and AI technologies is enhancing predictive analytics for maintenance and quality control.

-

Increasing focus on supply chain transparency and traceability is fueling demand for digital replicas.

-

Expansion of smart farming practices is encouraging the adoption of digital twin solutions in agriculture.

-

Stringent government regulations on food safety and quality are promoting technological advancements in storage.

-

Development of cloud-based platforms is making digital twin technology more accessible and scalable for operators.

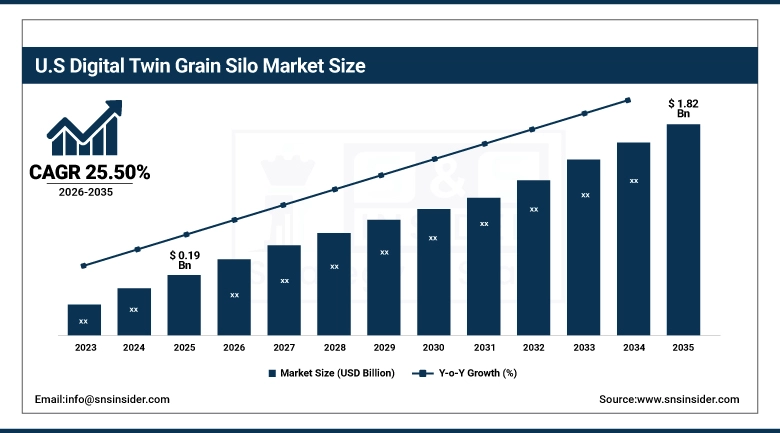

The U.S. Digital Twin Grain Silo Market Size was valued at USD 0.19 billion in 2025 and is expected to reach USD 1.82 billion by 2035 and grow at a CAGR of 25.50% over the forecast period 2026-2035. the U.S. Digital Twin Grain Silo Market is driven by the need to mitigate annual grain spoilage exceeding 5 million metric tons. This major loss pushes operators towards predictive systems that can minimize spoilage by 20% through monitoring of real-time environmental parameters. This demand accelerates expenditure in IoT sensor networks and AI analytics, allowing for a future grain storage infrastructure more resilient and efficient through the national supply chain.

Digital Twin Grain Silo Market Driver:

-

Increasing Need to Minimize Post-Harvest Losses and Optimize Grain Storage Drives Market Growth

The issue emerges due to the burning need for a solution to the global problem of massive post-harvest losses of grains in the millions of metric tons annually due to spoilage, insects, and unfavorable storage conditions. This has resulted in a massive need for innovative technological solutions that can provide real-time monitoring and control of the storage conditions of grains. As a result, digital twin technology emerges as a critical solution to this issue, enabling grain silo owners to simulate and predict the occurrence of spoilage and control climate conditions automatically.

A large North American grain co-operative launched a digital twin solution at its plants in March 2024. The solution successfully forecasted a possible spoilage issue in a silo based on temperature and humidity readings, enabling corrective action before it was too late, thereby saving an estimated $2 million of grain.

Digital Twin Grain Silo Market Restraint:

-

High Initial Investment and Integration Complexity Limit Widespread Market Adoption

The market is also challenged by a substantial restraint due to the high capital costs involved in the deployment of the entire digital twin ecosystem, including the cost of IoT sensors, software, cloud, and IT expertise. This results in a high initial financial burden, which impacts the calculation of the return on investment in a slower manner, thus deterring silo operators and agricultural cooperatives with limited capital expenditure budgets from adopting the technology, thus slowing down the adoption rate due to the high initial costs involved.

One of the regional grain storage facilities in the Midwest had delayed the initiation of its digital twin initiative towards the end of 2024, as the expense of installing sensors in the system had surpassed its annual technology budget by more than 300%.

Digital Twin Grain Silo Market Opportunity:

-

Integration with AI and Machine Learning for Predictive Analytics Opens New Avenues

The reason is the growth in data from IoT sensors in silos and the complexity of AI and machine learning algorithms. This is a great opportunity to move from monitoring to predictive and prescriptive analytics. This means that digital twin vendors can create solutions that not only alert users about current problems but also predict future problems with equipment, optimize grain blending, and manage energy, among other things. This means that vendors can create premium services with high margins, thus forging long-term relationships with their customers.

In February 2025, a leading technology provider launched an AI-powered module for its digital twin platform that predicts bearing failures in silo augers up to 30 days in advance, enabling planned maintenance and avoiding catastrophic operational downtime.

Digital Twin Grain Silo Market Segmentation Analysis:

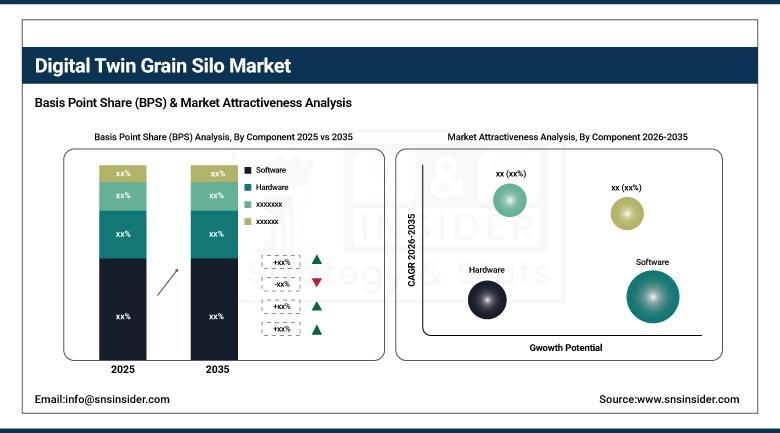

By Component: Software Leads Market While Services Register Fastest Growth

The Software segment dominates the global Digital Twin Grain Silo Market, capturing a 47% revenue share in 2025. This dominance is caused by the software platform being the core intelligence of the digital twin, responsible for data integration, visualization, simulation, and analytics. The effect is that it represents the essential, recurring-value component of the solution, commanding significant investment as it is critical for translating raw IoT data into actionable insights for silo operators, thus securing its revenue leadership. The Services segment is projected to grow at the fastest CAGR of 26.24%. This rapid growth is caused by the complex nature of deploying and integrating digital twins with existing silo infrastructure, which requires extensive consulting, system integration, and ongoing support and training. The result is that as the market grows, the demand for these specialized implementation and maintenance services shoots up, at times even surpassing the cost of the software, thus leading to the rapid growth of this market.

By Application: Inventory Management Leads Market, While Predictive Maintenance Registers Fastest Growth

The Inventory Management application is the leader in the Digital Twin Grain Silo Market, with a revenue share of 35% in 2025. This is because of the natural need for accurate and current information regarding the amount of grain, quality, and location within the storage facility for optimal logistics, trading, and reporting. This leads to the fact that this application provides direct and immediate financial benefit through the reduction of shrinkage and automated inventory reporting, making it the key application and first use driver. The Predictive Maintenance application is expected to have the highest CAGR of 26.18%. This is because of the significant financial benefits that can be realized through the prevention of unplanned downtime events of the critical silo equipment such as conveyors, augers, and aeration systems. This leads to the fact that the industry is experiencing significant investment in applications that predict equipment failures before they occur, thereby reducing operational downtime and high emergency repair costs, leading to rapid adoption of this application.

By Deployment Mode: On-Premises Leads Market While Cloud Registers Fastest Growth

The On-Premises segment dominates the global Digital Twin Grain Silo Market, holding a 69% revenue share in 2025. This leadership is caused by the prevalent data security and connectivity concerns among large agribusinesses and cooperatives, who prefer to maintain sensitive operational and inventory data on their own internal servers. The effect is that this deployment mode offers perceived greater control and reliability, especially in rural areas with intermittent internet, securing its dominance among established players. The Cloud segment is projected to grow at the fastest CAGR of 22.22%. This growth is caused by the lower upfront costs, easier scalability, and remote access benefits offered by cloud-based solutions. The effect is that these advantages are particularly attractive to smaller operators and new market entrants, making cloud deployment the preferred model for expansion and future-proofing, thus driving its faster growth rate.

By End-User: Grain Storage Facilities Lead Market, While Agriculture Registers Fastest Growth

The Grain Storage Facilities segment is the market leader in the Digital Twin Grain Silo Market, accounting for 45% of the revenue in 2025. This is because these facilities are most operationally focused on maximizing storage capacity, minimizing loss, and preserving grain quality for their customers. This has resulted in them having the scale and financial resources to invest in state-of-the-art technology like digital twins to optimize their core business processes, making them the largest consumers. The Agriculture segment is anticipated to have the highest CAGR of 24.18%. This is because there has been an increasing adoption of smart farming practices and the increasing scale of farming operations, which are now including on-farm storage and trying to optimize it with the same level of efficiency as commercial storage facilities. This has resulted in large-scale farming operations investing in digital twins to have better control over their post-harvest process, optimizing storage management with their overall smart farming strategy.

Digital Twin Grain Silo Market Regional Analysis:

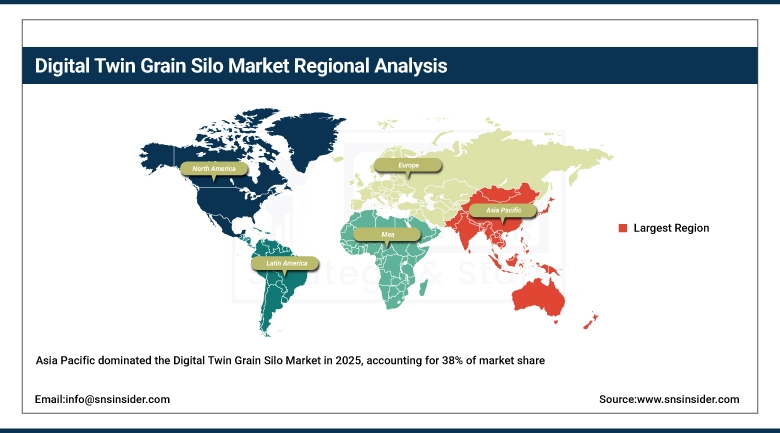

Asia Pacific Dominates Digital Twin Grain Silo Market in 2025

Asia Pacific is the dominant region, holding an estimated 38% market share in 2025. Driving Large agricultural output and government modernisation initiatives propel market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Dominates Asia Pacific’s Digital Twin Grain Silo Market

China currently leads the market in the region because of its enormous grain production and storage requirements, as well as its robust government policies and initiatives to modernize its agricultural infrastructure to ensure food security in the country. The government's initiative to embrace technology in the agricultural sector has led to the widespread adoption of digital twin technology in government and large grain storage silos.

North America is the Fastest-Growing Region in Digital Twin Grain Silo Market in 2024

North America is the fastest-growing region with an estimated CAGR of 21.5%. Driving High focus on operational efficiency and advanced tech adoption fuels rapid growth.

United States Leads Digital Twin Grain Silo Market Growth in North America

The U.S. leads in the regional market growth due to its large grain-exporting region and a strong focus on lowering operational costs and post-harvest losses in one of the largest grain-exporting regions in the world. The presence of major technology companies, high levels of farm mechanization, and the need for transparency in the supply chain are major drivers. American agribusinesses and cooperatives are quickly adopting digital twins to gain a competitive advantage.

Europe Digital Twin Grain Silo Market Insights

In 2025, Europe is a major market for the Digital Twin Grain Silo Market. The factors that drive the market are the stringent food safety regulations in the EU and the adoption of precision farming. The leader in this market is Germany, which has an advanced manufacturing base (Industry 4.0) and an efficient agricultural sector that embraces digital technology to meet regulations and improve sustainability.

Middle East & Africa and Latin America Market Insights

In 2025, the Digital Twin Grain Silo Market in Latin America and MEA is emerging, focused on improving food security and storage infrastructure. In Latin America, Brazil leads, driven by its massive soybean and corn exports and investments in port silo modernization. The MEA region shows potential, with growth influenced by initiatives to reduce dependency on food imports and minimize storage losses in challenging climates.

Digital Twin Grain Silo Market Competitive Landscape:

Siemens AG is a German multinational technology conglomerate and a leader in industrial automation and digitalization. Through its Siemens Xcelerator portfolio, the company offers a comprehensive digital twin platform that leverages its expertise in IoT, MindSphere, and industrial software. Its role is to provide an end-to-end solution that integrates with automation hardware in silos, offering high-fidelity simulation, process optimization, and predictive maintenance for large-scale grain storage operators, leveraging its global presence and engineering prowess.

-

Siemens announced a new partnership with a global agribusiness in Q1 2024 to deploy its digital twin technology across multiple grain export terminals, focusing on optimizing loading processes and preventing spoilage.

General Electric Company (GE) is a U.S.-based industrial giant with a strong focus on digital industrial solutions through its GE Digital arm. The company offers its Proficy-based digital twin solutions, applying predictive analytics and data modeling expertise from aviation and power to agriculture. GE's role is to provide robust asset performance management (APM) for critical silo infrastructure, helping operators predict equipment failures and optimize the health and efficiency of their storage assets.

-

GE Digital launched a new asset model library for grain handling equipment in early 2024, reducing implementation time for its digital twin solutions in the agricultural sector.

Emerson Electric Co. is a U.S.-based global technology and engineering company providing innovative solutions for industrial, commercial, and consumer markets. Its role in this market is strengthened by its extensive portfolio of measurement and analytical instruments, valves, and control systems essential for monitoring silo conditions. Emerson integrates these hardware components with its software platforms to deliver digital twins focused on precise environmental control and quality preservation within the silo.

-

In April 2024, Emerson introduced a new wireless sensor network solution designed for easy retrofitting onto existing grain silos, lowering the barrier to entry for its digital twin ecosystem.

ABB Ltd. is a Swedish-Swiss multinational corporation specializing in robotics, power, and automation technology. The company's Ability™ digital platform is central to its offering, providing capabilities for monitoring and optimizing silo operations. ABB's role is to leverage its strong expertise in electrification and process automation to create digital twins that not only monitor but also directly control the energy usage and material handling processes within grain storage facilities, aiming for maximum efficiency.

-

ABB released a case study in March 2024 highlighting a digital twin project that reduced energy consumption by 15% at a European grain facility by optimizing aeration system control.

Digital Twin Grain Silo Market Key Players:

-

Siemens AG

-

General Electric Company

-

Emerson Electric Co.

-

ABB Ltd.

-

Schneider Electric SE

-

Honeywell International Inc.

-

Rockwell Automation, Inc.

-

AVEVA Group plc

-

PTC Inc.

-

Dassault Systèmes SE

-

IBM Corporation

-

Microsoft Corporation

-

SAP SE

-

Oracle Corporation

-

Bosch.IO GmbH

-

Bentley Systems, Incorporated

-

Autodesk, Inc.

-

Aspen Technology, Inc.

-

Si-Ware Systems

-

GrainSense Oy

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.38 Billion |

| Market Size by 2035 | USD 9.1 Billion |

| CAGR | CAGR of 20.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Hardware, Services) • By Application (Inventory Management, Predictive Maintenance, Process Optimization, Quality Control, Others) • By Deployment Mode (On-Premises, Cloud) • By End-User (Agriculture, Food Processing, Grain Storage Facilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens AG, General Electric Company, Emerson Electric Co., ABB Ltd., Schneider Electric SE, Honeywell International Inc., Rockwell Automation, Inc., AVEVA Group plc, PTC Inc., Dassault Systèmes SE, IBM Corporation, Microsoft Corporation, SAP SE, Oracle Corporation, Bosch.IO GmbH, Bentley Systems, Incorporated, Autodesk, Inc., Aspen Technology, Inc., Si-Ware Systems, GrainSense Oy, and Others. |

Frequently Asked Questions

Asia Pacific dominated the Digital Twin Grain Silo Market in 2025.

The Inventory Management segment dominated the Digital Twin Grain Silo Market.

The major growth factor of the Digital Twin Grain Silo Market is the critical need to minimize significant annual post-harvest grain losses through real-time monitoring and predictive maintenance.

The Digital Twin Grain Silo Market size was USD 1.38 billion in 2025 and is expected to reach USD 9.10 billion by 2035.

The Digital Twin Grain Silo Market is expected to grow at a CAGR of 20.79% during 2026-2035.

Get in Touch