DNA Data Storage Market Report Scope & Overview:

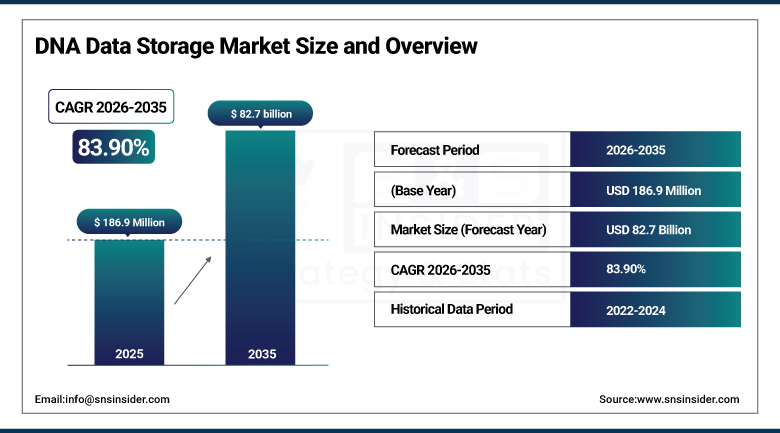

The DNA Data Storage Market was valued at USD 186.9 million in 2025 and is expected to reach USD 82.7 billion by 2035, growing at a CAGR of 83.90% from 2026–2035.

The DNA Data Storage Market is one of the most technologically advanced and high growth areas in the global data storage ecosystem providing a complement to conventional digital storage technologies that are facing fundamental as well as fast accelerating limitations, largely driven by the exponential growth in volumes of global data. DNA data storage takes advantage of the incredible information density densities reached by biological molecules, combined with natural stability in essentially a permanent state for thousands of years without the use of energy, to create an orderof magnitude better long-term archival media than magnetic tapes, hard drives and optical discs. Much of that investment is accelerating DNA synthesis and sequencing technologies to lower the cost per bit stored as well as boost read/write speed toward commercial viability and major tech companies such Microsoft, IBM, and Twist Bioscience are backing up these efforts with some substantial investments.

Previous scientific articles published in leading journals have conclusively demonstrated that DNA can contain information at data densities several million times surpassing state-of-the-art silicon-based storage media, with technological durability on geological timescales when stored under the appropriate conditions compared to 5–30 year degradation timelines for magnetic and optical storage thus allowing long-term electrochemical data preservation across geological time scales and proposing that DNA data storage represents a uniquely appealing technology to solving the global digital archive conundrum.

The primary technological enabler that is driving the transformation of DNA data storage from a laboratory curiosity to commercially viable archival storage at volumes meaningful enough for commercial deployment, with multiple technology roadmaps suggesting cost parity with conventional cold storage (within the forecast period), is the rapid maturation of combining DNA synthesis and nanopore sequencing technologies over decades of investment in genomics research which has already reduced the costs of synthesizing DNA by more than six orders-of-magnitude since 2000.

DNA Data Storage Market Size and Forecast

-

Market Size in 2025: USD 186.9 Million

-

Market Size by 2035: USD 82.7 Billion

-

CAGR: 83.90% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on DNA Data Storage Market - Request Free Sample Report

DNA Data Storage Market Trends

-

Advancing enzymatic DNA synthesis technologies reducing synthesis cost per base and improving throughput toward commercially viable write speeds for large-scale data storage.

-

Growing integration of AI and machine learning into DNA encoding, error correction, and retrieval algorithms improving data fidelity and access efficiency.

-

Rising investment by major technology corporations including Microsoft, IBM, and Seagate in DNA storage research and commercial development programs.

-

Expanding academic and government research programs validating DNA storage reliability, longevity, and retrieval accuracy across increasingly large datasets.

-

Development of nanopore sequencing-based random access retrieval methods enabling rapid, cost-effective targeted data retrieval from DNA archives.

-

Growing partnership activity between DNA synthesis providers, sequencing technology companies, and enterprise storage vendors to build integrated DNA storage systems.

-

Increasing regulatory and standardization activity around DNA data storage interoperability, as demonstrated by the SNIA DNA Data Storage Alliance’s initial technical specifications.

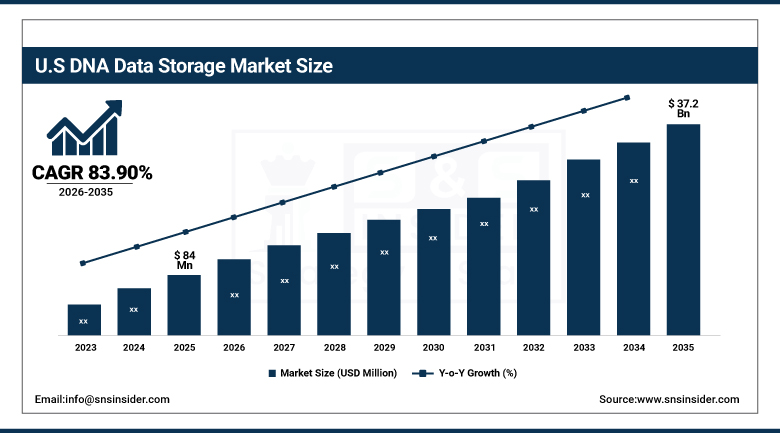

U.S. DNA Data Storage Market was valued at USD 84 million in 2025 and is expected to reach USD 37.2 billion by 2035, registering a CAGR of 83.90% during 2026–2035.

US DNA Data Storage Market Overview The US is the global technology development leader large R&D programs based at Microsoft Research and IBM Research have prime focused on the initial development of DNA storage, as well as a strong biotech ecosystem of synthesis & sequencing technology companies including Twist Bioscience, Illumina and Pacific Biosciences. The advanced DNA storage program development is funded by federal research grants from IARPA (Intelligence Advanced Research Projects Activity), DARPA, and NIH with China currently holding a significant technology gap out to market due to the powerful U.S.-led life sciences and synthetic bio-industries acting as essential critical technology infrastructures for commercialization.

IARPA’s investment in the U.S. intelligence community for DNA data storage, including ambitious technical milestones with MIST (specifying writing at 1 terabyte per day and reading at 10 terabytes per day), is both a direct procurement driver and a technology development forcing function that is expediting commercial DNA storage readiness beyond what would comport around pure commercial investments alone.

DNA Data Storage Market Segment Insights

-

Based on Type, Sequence-Based DNA Data Storage accounted for the largest market share (68.7%) in 2025; Structure-Based DNA Data Storage expected to be the fastest-growing segment (CAGR).

-

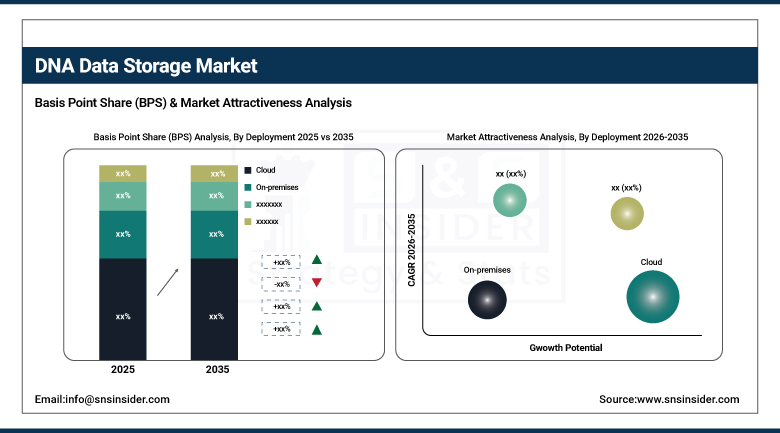

Based on Deployment, Cloud-Based accounted for the largest market share (58.3%) in 2025; On-Premises expected to be the fastest-growing segment (CAGR) driven by government and defense requirements.

-

Based on End-UseR, Biotechnology & Healthcare accounted for the largest market share (38.6%) in 2025; Government & Defense expected to be the fastest-growing segment (CAGR).

DNA Data Storage Market Segment Analysis

By Deployment, Cloud-Based dominates, On-Premises expected to grow fastest

Cloud-Based deployment segment dominated the worldwide revenue from DNA data storage with about 58.3% share in 2025. The cloud-based distribution also benefits enterprise customers accessing archived data as they all take advantage of different accessibility interface offered by cloud-storage interfaces. DNA storage services are cloud based which mean anyone who needs archival capabilities can get some without needing any biotechnology experience and no laboratory facilities.

On-Premises DNA based data storage deployment as most of the government agencies, defence organisations and financial institutions are mandated to adhere to strict data security, sovereignty and regulatory compliance by banning classified or highly sensitive information from being stored in cloud infrastructure. More compact, automated and operationally simplified DNA storage systems are extending the on-premises deployment potential for security-critical organizations as improvements in local DNA synthesis hardware continue to alleviate some infrastructure requirements of in-house DNA storage operations.

By Type, Sequence-Based dominates, Structure-Based expected to grow fastest

Sequence-based DNA data storage accounted for the largest type market share of 68.7% in 2025 as high-density multi-terabyte encoding experiments from leading academia and companies including Microsoft and UW continue to validate its ability to reliably encode and retrieve large volumes of data with high fidelity. Sequence–based methods translate binary digital data into sequences of DNA nucleotides (A, T, G, C)through advanced encoding algorithms using error correction redundancy to allow secure retrieval of stored information.

Structured DNA Data Storage segment expected to expand at highest CAGR throughout 2035. This new paradigm encodes data not purely in nucleotide sequence, but also in the three-dimensional shape and structural architecture of a DNA molecule, achieving greater (potentially) storage density per unit volume, higher read speeds using methods based on structure rather than full sequencing, and lower error rates for some observed algorithms. The advances in cryo-electron microscopy, AI-assisted structural prediction as well as molecular engineering are gradually making viable structure-based storage systems possible, with many research groups having already shown proof-of-concept demonstrations validating the core approach.

By End-User, Biotechnology & Healthcare leads, Government & Defense expected to grow fastest

The Biotechnology and Healthcare organizations were the biggest end use segment in 2025 due to the sector’s astonishingly increasing genomic and clinical data storage requirements. Whole-genome sequencing produces tens of hundreds to over a few hundred gigabytes (GB) of raw data per person, and as the costs of sequencing have plummeted over the past 15 years, population-scale genomic databases for precision medicine, pharmacogenomics analysis and biobanks in complex single-disorder diseases are producing petabyte-scale data volumes that can challenge traditional storage infrastructures.

Government and Defense is expected to register the fastest CAGR from 2026 to 2035, driven by national agencies’ compelling combination of massive long-term data preservation requirements, stringent security mandates precluding cloud storage of sensitive data, and strong financial resources to invest in pioneering storage technologies. Intelligence agencies, national archives, defense research laboratories, and government data centers are actively evaluating DNA storage as a strategic long-term archival solution for classified data and critical national records that must be preserved reliably for decades to centuries.

DNA Data Storage Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

80% |

|

Europe |

United Kingdom |

30% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

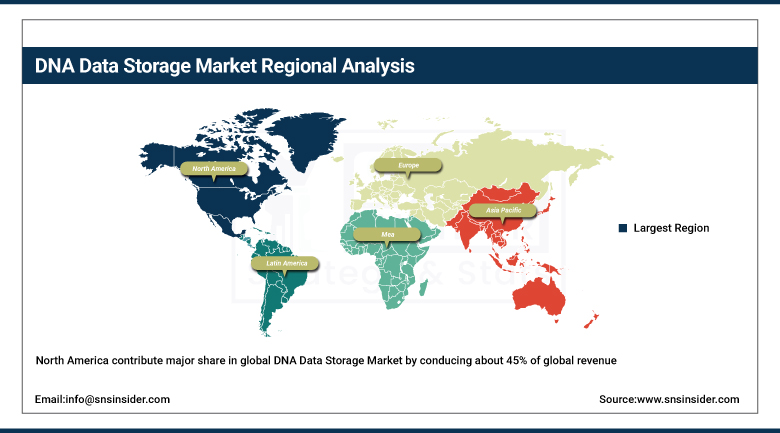

North America DNA Data Storage Market Insights

North America contribute major share in global DNA Data Storage Market by conducing about 45% of global revenue. This dominance is indicative of the unique concentration of genomic biotechnology companies, leading research university programs, federal research agency funding (NIH, DARPA, IARPA) and major technology company R&D driven DNA storage development in the United States. These three programs together, funded by Microsoft Research in cooperation with the University of Washington and molecular storage research from IBM Research as well as a dynamic ecosystem of synthetic biology start-ups have established the U.S. to be, by far, ahead when it comes to development and early commercialisation of DNA storage technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe DNA Data Storage Market Insights

European DNA Data Storage Market Overview 2025:Europe was the most lucrative region in globally for commercialisation of DNA data storage, as the European Commission remained a substantial supporter (through funding) of DNA storage research and development through its Horizon Europe program, world-leading academic research institutes in synthetic biology and molecular storage across the UK (and Germany, France, Netherlands) will further strengthen developments underway throughout the region alongside international standardization efforts on a number of fronts - such that company activity seen throughout Europe will take many forms. Genomics England and EMBL-EBI have combined to create a world-class genomics infrastructure in the UK, which generates demand for large-scale DNA data storage, meanwhile European data sovereignty concerns are causing governments to contemplate domestic DNA storage capabilities for maintaining critical national data.

Asia Pacific DNA Data Storage Market Insights

Asia Pacific is anticipated to achieve the highest CAGR owing to China leading massive government investment in genomic biotechnology through BGI Group and national genomics programs, Japan being one of the most active university-industry collaborations on molecular storage technologies and India expanding its biotech sector at an unprecedented overall growth rate. All the major government digital infrastructure investment programs across the region are familiarizing institutions with long term archival storage challenges, whereas there are rising regional biotech mom-and-pop stores who could eventually prove to be serious competition in the DNA synthesis and storage technology space against their Western count-part incumbents of choice.

Middle East & Africa and Latin America DNA Data Storage Market Insights

The DNA Data Storage Markets for the Middle East & Africa and Latin America - which are both nascent yet highly promising markets in a longer-term growth opportunity as the technology continues its gradual transformation into commercial viability. In the Gulf Cooperation Council (GCC) countries, national data infrastructure and smart government investments are on the rise, as have interest in DNA storage technology for storing DNA sequences at sovereign ultra-long-term archival preservation of sensitive national records and cultural heritage data. With DNA storage at the edge of efficacy, possible research will emerge from Latin American research universities and biotech centers in Brazil, Argentina and Colombia..

DNA Data Storage Market Growth Drivers:

-

Exponential global data growth and physical limitations of conventional storage technologies creating demand for DNA storage

The major factor boosting the growth of DNA Data Storage Market is, the exponential rate at which we generate global digital data (forecast to reach over 200 zettabytes by 2030) & physical capacity, energy consumption and longevity constraints of traditional magnetic & optical storage technologies. Traditional data centre storage constantly draws energy for climate control and data integrity, has physical degradation timelines of 5–30 years which drive costly media refreshing, and is taking up increasingly larger footprints that are expensive to expand. The information density, longevity without power requirements on the scale of millenia and intrinsic chemical stability that prevents electromagnetic interference makes DNA storage uniquely qualified to solve the archival storage problem that no other technology.

The global datasphere generated by AI model training, genomic sequencing, IoT sensor networks, autonomous vehicle sensor logging, and high-resolution digital content creation is expanding at a pace that makes DNA storage’s cost and throughput curve toward commercial viability not merely desirable but arguably necessary – as no combination of conventional storage technologies appears able to provide sufficient capacity, longevity, and energy efficiency to preserve the full record of human digital activity across coming decades and centuries.

DNA Data Storage Market Restraints

-

High synthesis and sequencing costs and slow read/write speeds limiting near-term commercial scalability

High costs associated with synthesizing DNA to write data into DNA molecules coupled with slow read/write speeds across large volumes of data as compared to conventional digital storage systems are the major challenges limiting the growth of DNA Data Storage Market. Cheaper than at least an entire two decades of DNA synthesis cost, still orders of magnitude costlier per gigabyte vs conventional storage for practical deployment over the next few years. Periodic DNA sequencing based data retrieval has very large latencies – hours to days for TBs of data – vs milliseconds in the current digital domain, making DNA storage intrinsically incompatible with active or more frequently accessed and thus severely restricting commercial applicability to deep archival use cases

DNA Data Storage Market Opportunities

-

Enzymatic synthesis and nanopore sequencing breakthroughs enabling affordable, high-speed DNA archival storage

The most promising near-term release in the technology development path for DNA storage lies in the development of enzymatic DNA synthesis approaches — where DNA strands are built using biological enzymes instead of chemical phosphoramidite chemistry. This might enable an estimated 10–100x decrease in the synthesis cost while also improving on speed and enabling short reads of longer DNA strands with decreased error rates significantly advancing the time to be commercial competitive. At the same time, advances in nanopore-based sequencing and targeted retrieval methods that finally allow for direct low-cost reading of specific data segments from DNA archives without full resequencing should reduce dramatically the cost and latency of retrieving DNA storage data to make a much broader class of archival use cases feasible within the timeframe of this forecast.

Recent Developments:

-

2026: Microsoft and the University of Washington demonstrated a fully automated DNA data storage and retrieval system achieving write speeds of 400 MB per day in a laboratory setting, representing a significant milestone toward commercial throughput targets. Twist Bioscience expanded its high-throughput DNA synthesis platform with enhanced error rates and longer oligo capabilities specifically optimized for DNA data storage encoding applications.

-

2025 (March): Researchers at the Technion Institute introduced DNAformer, an AI-based method that accelerates DNA sequence retrieval speeds by up to 3,200× while maintaining high accuracy, directly addressing one of the key practical limitations of sequence-based storage systems – slow and error-prone read operations – and representing a significant step toward practical DNA data retrieval at commercial timescales.

-

2024 (November): Microsoft Research released Trellis BMA, an advanced open-source DNA error correction algorithm that significantly enhances the reliability of synthetic DNA data storage by improving the accuracy of data encoding and decoding processes, demonstrating Microsoft’s ongoing commitment to maturing DNA storage technology toward production-grade reliability standards required for commercial deployment.

DNA Data Storage Market Key Players

Some of the DNA Data Storage Market Companies

-

Microsoft Corporation

-

Twist Bioscience Corporation

-

IBM Research

-

Illumina, Inc.

-

Oxford Nanopore Technologies Ltd.

-

Pacific Biosciences (PacBio)

-

Catalog Technologies, Inc.

-

DNA Script

-

Ansa Biotechnologies

-

Helixworks Technologies Ltd.

-

Molecular Assemblies Inc.

-

Western Digital Corporation

-

Seagate Technology Holdings PLC

-

Biomemory SAS

-

Thermo Fisher Scientific Inc.

-

Agilent Technologies, Inc.

-

Evonetix Ltd.

-

Iridia Inc.

-

Micron Technology, Inc.

-

BGI Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 186.9 Million |

| Market Size by 2035 | USD 82.7 Billion |

| CAGR | CAGR of 83.90% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Cloud, On-premises) • By Technology (Sequence-based DNA data storage, Structure-based DNA data storage) • By End User (Biotechnology & healthcare, Banking & finance, Government & defense, Media & entertainment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft Corporation, Twist Bioscience Corporation, IBM Research, Illumina, Inc., Oxford Nanopore Technologies Ltd., Pacific Biosciences (PacBio), Catalog Technologies, Inc., DNA Script, Ansa Biotechnologies, Helixworks Technologies Ltd., Molecular Assemblies Inc., Western Digital Corporation, Seagate Technology Holdings PLC, Biomemory SAS, Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Evonetix Ltd., Iridia Inc., Micron Technology, Inc., BGI Group |

| Company Profiles | Microsoft, Twist Bioscience, Illumina, Thermo Fisher Scientific, Catalog Technologies, IBM, Helixworks, Iridia, GenScript, Quantum Corporation, Zymo Research, Oxford Nanopore Technologies, Evonetix, DNA Script, Southwestern University & Microsoft Research Collaboration. |

Frequently Asked Questions

North America dominated the DNA Data Storage Market in 2025, accounting for approximately 45% of global revenue, driven by U.S. technology company R&D investment, federal agency research programs, and a world-leading synthetic biology ecosystem.

The Sequence-Based DNA Data Storage segment dominated the market in 2025, accounting for approximately 68.7% of total revenue, driven by its technological maturity and proven data encoding and retrieval capabilities.

Exponential global data growth exceeding the capacity and longevity limitations of conventional storage technologies, combined with advancing DNA synthesis and sequencing technologies reducing cost and improving throughput toward commercial viability.

The DNA Data Storage Market was valued at USD 186.9 million in 2025.

The DNA Data Storage Market is expected to grow at a CAGR of 83.90% from 2026 to 2035, making it one of the fastest-growing segments in the global data storage technology landscape.

Get in Touch