Drone Propellers Market Report Scope & Overview:

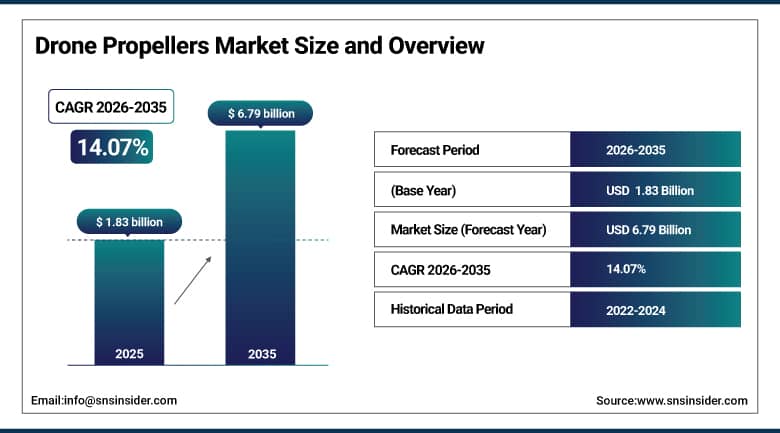

The Drone Propellers Market size was valued at USD 1.83 Billion in 2025 and is projected to reach USD 6.79 Billion by 2035, growing at a CAGR of 14.07% during 2026-2035.

The market for Drone Propellers is experiencing growth as there is an increase in the usage of drones in multiple sectors including commercial applications, defense applications, agriculture applications, and logistics operations. Growing preference for propellers that offer greater efficiency, light weight, and durability is driving growth in the market. Growth in drone delivery systems, surveillance activities, and precise farming techniques will further boost the demand for propellers.

Market Size and Forecast:

-

Market Size in 2025: USD 1.83 Billion

-

Market Size by 2035: USD 6.79 Billion

-

CAGR: 14.07% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Drone Propellers Market - Request Free Sample Report

Key Drone Propellers Market Trends

-

Increasing adoption of carbon fiber propellers for lightweight durability and enhanced flight efficiency across commercial drones.

-

Rising demand for low-noise propeller designs to support urban drone operations and regulatory compliance requirements.

-

Growth in customized and application-specific propellers optimized for agriculture, delivery, surveillance, and industrial drone use.

-

Advancements in aerodynamic blade design improving thrust efficiency, battery performance, and extended drone flight time.

-

Expansion of drone delivery and eVTOL ecosystems driving demand for high-performance, scalable propeller solutions globally.

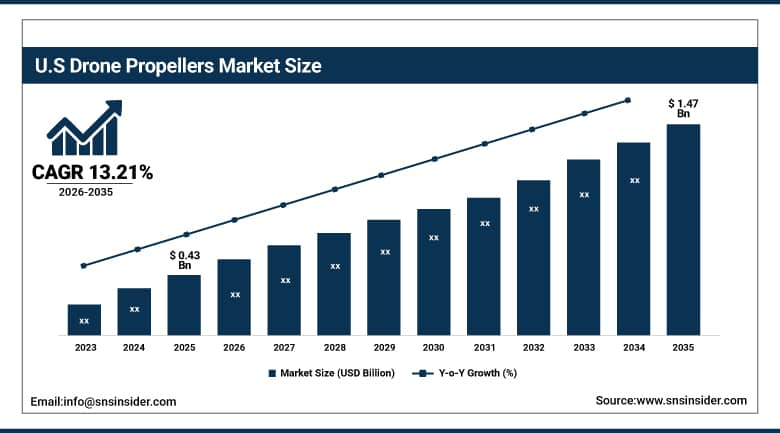

The U.S. Drone Propellers Market size was valued at USD 0.43 Billion in 2025 and is projected to reach USD 1.47 Billion by 2035, growing at a CAGR of 13.21% during 2026-2035. U.S. Drone Propellers Market is experiencing growth owing to increased usage of drones in the defense, agriculture, and commercial delivery segment. Increased investment in UAV technologies and increased demand for efficient components drive market growth.

Drone Propellers Market Growth Drivers:

-

Surging Multi-Industry Drone Adoption Driving Strong Demand for Advanced, Efficient, and Durable Propeller Technologies Worldwide

The market is growing at an accelerated rate because of the adoption of drones in many applications ranging from defense, agriculture, construction, logistics, and the media industry. The increase in the need for effective propulsion technologies is encouraging the development of light and durable propellers made of carbon fibers and composites. There has been an increased demand for propellers that help drones carry out tasks such as delivering packages, surveillance missions, and precision farming. Furthermore, there have been improvements in blade design that increase thrust efficiency while conserving the battery life.

Drone Propellers Market Restraints:

-

Stringent Regulations, Cost Pressures, and Technical Limitations Restricting Widespread Adoption of Advanced Drone Propeller Solutions

With considerable growth opportunities, this industry faces hurdles because of the stringent rules governing aircrafts and drones, especially when used for commercial purposes. Issues concerning noise pollution and the safety of the drone due to malfunctioning prevent extensive acceptance. The high cost associated with the use of advanced materials in the propeller and precision engineering makes the total cost of manufacturing a drone extremely high, making it unaffordable for small businesses. Moreover, the durability of the propeller is relatively low and requires frequent replacements.

Drone Propellers Market Opportunities:

-

Rapid Technological Advancements and Emerging Drone Applications Unlocking New Growth Opportunities for Innovative Propeller Solutions Globally

Many growth opportunities are emerging due to the application of drones in the field of healthcare services, emergencies, mining activities, and inspection of infrastructure. Since the emergence of urban air mobility and eVTOL, there has been an increased demand for efficient, noise-free propellers capable of generating high thrust levels. This is made possible through further research in areas like intelligent materials, 3D printing, and aerodynamics, which allow customization of the propellers based on application requirements. The growing demand for drones fitted with autonomous control mechanisms demands further performance from propellers.

Drone Propellers Market Segment Analysis

-

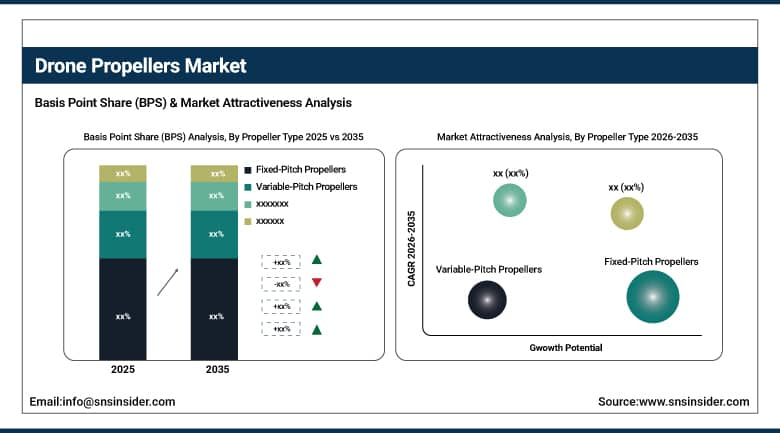

By Propeller Type, Fixed-Pitch Propellers dominated with 51.45% in 2025, and Variable-Pitch Propellers are expected to grow at the fastest CAGR of 16.53% from 2026 to 2035.

-

By Material, Plastic (ABS, Nylon, Polycarbonate) dominated with 45.23% in 2025, and Carbon Fiber Reinforced Polymer (CFRP) is expected to grow at the fastest CAGR of 15.47% from 2026 to 2035.

-

By Drone Type, Consumer / Commercial Drones dominated with 42.67% in 2025, and Military / Defense Drones are expected to grow at the fastest CAGR of 15.05% from 2026 to 2035.

-

By Distribution Channel, OEM dominated with 38.55% in 2025, and Online Retail is expected to grow at the fastest CAGR of 15.05% from 2026 to 2035.

By Propeller Type, Fixed-Pitch Leads While Variable-Pitch Propellers Show Fastest Growth in Drone Propellers Market 2026 to 2035

Fixed pitch propellers have the largest market share since they are easy, economical, and popularly employed by both consumer and commercial drones. Their ease of maintenance and durability makes them suitable for the general operation of drones. Conversely, variable pitch propellers are the fastest growing segment in the market because of their efficiency in providing optimized thrust during flight. Variable pitch propellers allow better control, efficient flight, and greater flexibility depending on flight circumstances. The increasing demand for sophisticated drones in military and industrial use is boosting the market growth for variable pitch propellers.

By Material, Plastic Propellers Lead Drone Propellers Market While Carbon Fiber Reinforced Polymer Set for Fastest Growth 2026 to 2035

The plastic-based materials such as ABS, nylon, and polycarbonate hold the majority share in the market owing to their economical nature, ease of production, and extensive use in both consumer and commercial drones. The material provides adequate resistance and strength for typical uses, thereby making it widely favored for bulk production. On the other hand, carbon fiber reinforced polymer (CFRP) represents the most rapidly expanding category of materials because of its favorable strength-to-weight ratio, increased durability, and effectiveness in optimizing the performance of flights.

By Drone Type, Consumer and Commercial Drones Lead While Military and Defense Drones Show Fastest Growth in Drone Propellers Market 2026 to 2035

Drones used for consumers and commerce have captured a major share of the market owing to their widespread use in photography, agriculture, monitoring, and deliveries. The high-volume manufacture and cost-effectiveness of such drones ensure regular demand for propellers. By contrast, military and defense drones are experiencing rapid growth owing to increasing spending on UAVs in surveillance, reconnaissance, and combat. Propellers needed for such drones must be highly robust and efficient enough to perform under severe environmental conditions.

By Distribution Channel, OEM Leads Drone Propellers Market While Online Retail Grows Fastest 2026 to 2035

OEM distribution remains at the forefront of this sector since many companies manufacture drones and use direct propellers supplied to them as part of the process to develop new drones. But there is rapid growth in e-retail due to higher demands for propeller replacements and upgrades among end-users and hobbyists. Online stores make it convenient for customers to purchase a wide range of products at affordable prices. Also, more people are building their own drones nowadays, which is also contributing to the growth of online retail.

Drone Propellers Market Report Analysis

North America Drone Propellers Market Insights

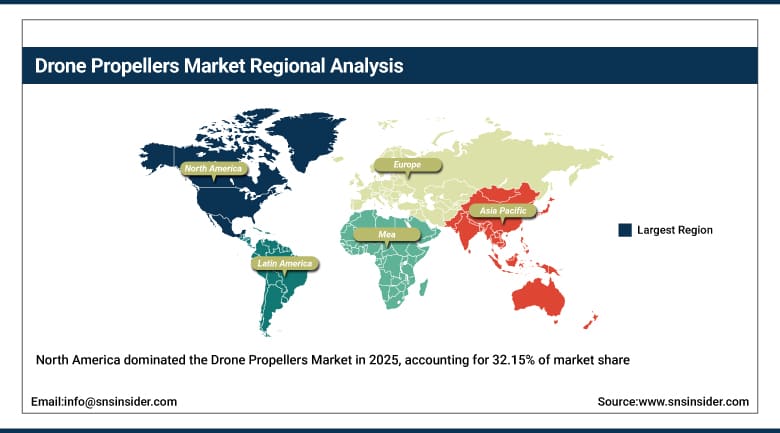

North America held a 32.15% share of the global Drone Propellers Market in 2025 at USD 0.59 Billion, growing at a CAGR of 13.55% through 2035. The region's market is anchored by the world's most active commercial drone regulatory development process, a defense procurement establishment that is the primary global buyer for military-grade drone systems, and an agricultural drone adoption program that while behind Asia Pacific in fleet size is growing rapidly in states including Kansas, Iowa, and California where BVLOS agricultural spray drone approval pathways are advancing. A disproportionately large regional share driven by Transport Canada's progressive drone regulatory framework and the country's active forestry, pipeline, and mining inspection drone operations in remote territories where fixed-wing and VTOL platforms with high-specification propellers are operationally justified by the access challenge.

Get Customized Report as Per Your Business Requirement - Enquiry Now

U.S. Drone Propellers Market Insights

The United States dominated North America's drone propellers market at 72.57%, USD 0.43 Billion in 2025. The FAA's expanding commercial drone approval pipeline, the DoD's Blue sUAS vendor list which certified American-made drones from Skydio, Joby-acquired Uber Elevate platforms, and Teal Drones for military use, and the expanding Wing and Amazon Prime Air delivery operations in Texas, Virginia, and Arizona between them generate the broadest and deepest propeller procurement base of any single country market outside China. The NDAA's restrictions on Chinese-made drone components for federal procurement has created a domestic propeller manufacturing development imperative that is beginning to generate production investment from APC Propellers, Master Airscrew, and Sensenich Propeller.

Europe Drone Propellers Market Insights

Europe held 23.90% at USD 0.44 Billion in 2025, growing at a CAGR of 14.34% through 2035. The EU's U-Space regulatory framework, which became operational across EU member states in 2023 and is enabling low-altitude commercial drone operations in designated geographic zones with digital traffic management, is progressively removing the regulatory ceiling that had limited commercial drone deployment in densely populated European airspace. Germany's DHL Parcelcopter operations, Manna Drone Delivery's Irish expansion, and multiple utility inspection programs across France's RTE power network are generating active propeller consumption that European manufacturers including Graupner in Germany and Czech Republic's Mejzlík Propellers are positioned to serve for EU defense and government procurement where domestic sourcing preferences apply.

Germany Drone Propellers Market Insights

Germany dominated the European Drone Propellers Market in 2025. Graupner GmbH, headquartered in Jägersmühl-Reutlingen, is Europe's most established drone and model aircraft propeller manufacturer, with a product line covering precision-moulded folding, fixed, and performance propellers used across commercial inspection, hobby, and increasingly light industrial applications. Germany's regulatory environment has been more permissive for commercial BVLOS operations in specific industrial zones than most EU peers, enabling the active industrial inspection drone programs at BASF's Ludwigshafen complex, at Volkswagen's Wolfsburg plant, and across the country's chemical industry corridor that generate consistent replacement propeller demand.

Asia Pacific Drone Propellers Market Insights

Asia Pacific led the global Drone Propellers Market with a 33.02% share at USD 0.60 Billion in 2025 and is the fastest-growing region at 15.05% CAGR through 2035, projected to reach USD 2.44 Billion. The region's dominance reflects both manufacturing concentration and end-use scale. The majority of the world's drone propellers by unit volume are designed and manufactured in the Pearl River Delta region of Guangdong Province, where DJI's Shenzhen headquarters anchor an ecosystem of propeller specialists including Gemfan in Guangzhou, T-Motor in Nanchang, and hundreds of smaller injection moulding and composite fabrication shops that supply the global aftermarket. China's domestic agricultural drone market, where XAG and DJI Agras operate fleets treating over 1 billion mu (roughly 167 million acres) of farmland annually, generates a propeller replacement market whose scale is unmatched outside the region. India's SMAM subsidy scheme is actively expanding agricultural drone adoption, with over 100 domestically approved agricultural drone models listed on the DGCA's type certificate register as of 2024.

China Drone Propellers Market Insights

China dominated the Asia Pacific Drone Propellers Market in 2025 and will maintain that position through 2035. DJI's global market share in consumer and commercial drones, estimated at over 70% by most industry analysts, makes DJI-compatible propeller specifications the effective global standard for the consumer segment every aftermarket propeller manufacturer in the world designs its consumer product line around DJI mount compatibility.

Latin America (LATAM) and Middle East & Africa (MEA) Drone Propellers Market Insights

Latin America held a 6.00% share at USD 0.11 Billion in 2025, growing at 13.64% CAGR through 2035, with Brazil and Mexico anchoring demand. Brazil's vast agricultural territory, where drone-based crop spraying adoption is accelerating through MAPA regulatory approvals that expanded the approved agricultural drone list significantly in 2024, generates propeller replacement consumption across both DJI Agras and domestically assembled agricultural platforms. Brazil's Embrapa agricultural research agency has formally incorporated agricultural drone recommendations into its crop management guidance, a signal that institutional adoption is moving past early-adopter phase. The Middle East & Africa held 4.93% at USD 0.09 Billion with a CAGR of 8.46%, the most modest growth in the market, where Gulf state military procurement and infrastructure inspection programs in the UAE and Saudi Arabia generate the primary demand. Israel's drone industry, which combines domestic military development with an active commercial export sector, operates a sophisticated propeller specification and testing infrastructure that serves both domestic platforms and the export programs that IAI, Elbit, and Rafael run across African and Asian customer defense agencies.

Competitive Landscape for Drone Propellers Market:

SZ DJI Technology Co., Ltd., headquartered in Shenzhen, China, is the world's dominant drone manufacturer and by extension the largest single propeller specification authority in the consumer and commercial drone market. DJI doesn't publicly position propellers as a standalone business but its proprietary 1.6-inch to 36-inch propeller systems across the Mini, Mavic, Phantom, Matrice, Agras, and Inspire product families collectively represent the highest-volume design specifications in the market.

-

In 2024, DJI launched the Agras T50 agricultural drone with redesigned four-blade folding propellers achieving 12% higher thrust efficiency than the T40 predecessor, reducing operating cost per hectare for large-scale spray operations and setting a new performance benchmark for agricultural drone propeller design that competitors including XAG and EAV have been actively engineering to match.

T-Motor, headquartered in Nanchang, Jiangxi Province, China, is the most technically respected propeller and motor brand in the professional drone and FPV community outside DJI's ecosystem, with its Flame Wheel, Pacer, and Navigator series CFRP propellers specified on premium commercial inspection drones and competition FPV frames globally. T-Motor's business model is distinctive in combining propeller and motor design in-house, allowing propulsion system optimization that suppliers who source motors and propellers separately cannot match.

- In 2024, T-Motor released its MA15 series CFRP propellers specifically designed for heavy-lift delivery drone platforms in the 25-50 kg maximum takeoff weight class, achieving a thrust-to-weight ratio improvement of approximately 9% over predecessor designs at equivalent tip speed through refined blade twist distribution and improved CFRP layup that reduces blade flutter at high rotor disc loading.

Drone Propellers Market Key Players:

-

SZ DJI Technology

-

Master Airscrew

-

APC Propellers

-

Gemfan Technology

-

XOAR International

-

HQProp

-

iFlight

-

Mejzlík Propellers

-

Sensenich Propeller Company

-

T-Motor

-

Foxtech

-

EMAX MODEL

-

Graupner GmbH

-

Carbon Fiber Gear

-

EchoBlue Ltd.

-

RobotShop Inc.

-

WhirlWind Propellers

-

KievProp America

-

E-PROPS

-

FP Propeller

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.83 Billion |

| Market Size by 2035 | USD 6.79 Billion |

| CAGR | CAGR of 14.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Plastic (ABS, Nylon, Polycarbonate), Carbon Fiber Reinforced Polymer (CFRP), Glass Fiber Reinforced Polymer (GFRP), and Metal (Aluminum, Titanium)) • By Drone Type (Consumer / Commercial Drones, Military / Defense Drones, Industrial / Enterprise Drones, and Racing / Competitive Drones) • By Propeller Type (Fixed-Pitch Propellers, Variable-Pitch Propellers, Folding Propellers, and Co-axial / Contra-rotating Propellers) • By Distribution Channel (OEM (Original Equipment Manufacturer), Aftermarket / Replacement, Online Retail, and Offline Distribution (Dealers / Distributors)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SZ DJI Technology, Master Airscrew, APC Propellers, Gemfan Technology, XOAR International, HQProp, iFlight, Mejzlík Propellers, Sensenich Propeller Company, T‑Motor, Foxtech, EMAX MODEL, Graupner GmbH, Carbon Fiber Gear, EchoBlue Ltd., RobotShop Inc., WhirlWind Propellers, KievProp America, E‑PROPS, FP Propeller. |

Frequently Asked Questions

Asia Pacific led the market share in 2025.

Plastic (ABS, Nylon, Polycarbonate) dominated in 2025.

Rising drone adoption across industries, demand for lightweight high-efficiency propellers, and advancements in materials and aerodynamics are driving market growth.

The market size was USD 1.83 Billion in 2025 and is projected to reach USD 6.79 Billion by 2035.

The market is expected to grow at a CAGR of 14.07% from 2026-2035.

Get in Touch