Dry Ice Market Report Scope & Overview:

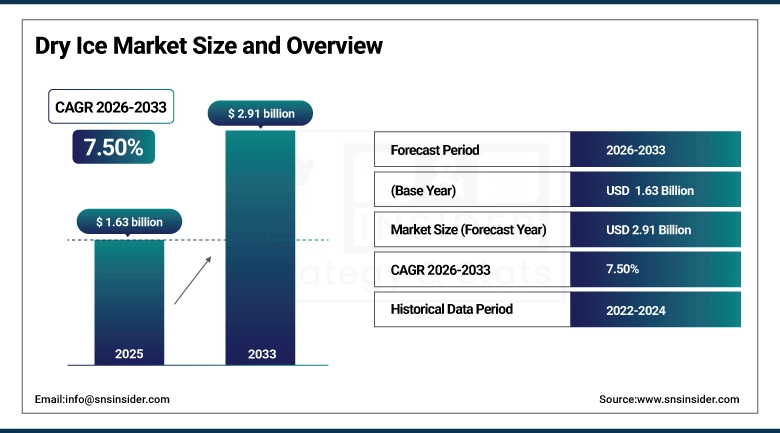

The Dry Ice Market Size was valued at USD 1.63 Billion in 2025E and is projected to reach USD 2.91 Billion by 2033, growing at a CAGR of 7.50% during the forecast period 2026–2033.

The Dry Ice Market analysis gives an astonishing source to the Dry Ice market and other fundamental subtleties relating to it. By type, the market is categorized into solid, pellet and block; by application, it is classified as food & beverages, healthcare, industrial cleaning, logistics and entertainment. The market is flourishing, due to growth in cold chain logistics demand, growth in food preservation and pharmaceuticals usage, and an increase of industrialization that implies more use cases for inexpensive, "green" cooling solutions.

Solid dry ice leads the Dry Ice Market, food & beverages is the largest application, commercial users account for the highest share, and direct sales capture over 25% of the market in 2025.

Market Size and Forecast:

-

Market Size in 2025: USD 1.63 Billion

-

Market Size by 2033: USD 2.91 Billion

-

CAGR: 7.50% from 2026 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Dry Ice Market - Request Free Sample Report

Dry Ice Market Trends:

-

Growing cold chain logistics market to promote dry ice application in food, pharma, and biotechnology sector requiring product safety maintenance throughout the transit.

-

The increasing realization of labor and eco-responsive cooling systems, reusing the environmentally benign form of a dry ice method.

-

Growth of e-commerce and online grocery delivery is driving up demand for dry ice to use in last-mile cold storage and temperature-sensitive shipments.

-

Industrial cleaning and specialized applications, such as fire suppression & metal treatment, are also turning into promising opportunities for dry ice use.

-

Dry ice demand for cryogenic preservation, sample shipping, and vaccination has been growing as healthcare and laboratories have become the industries using it more often.

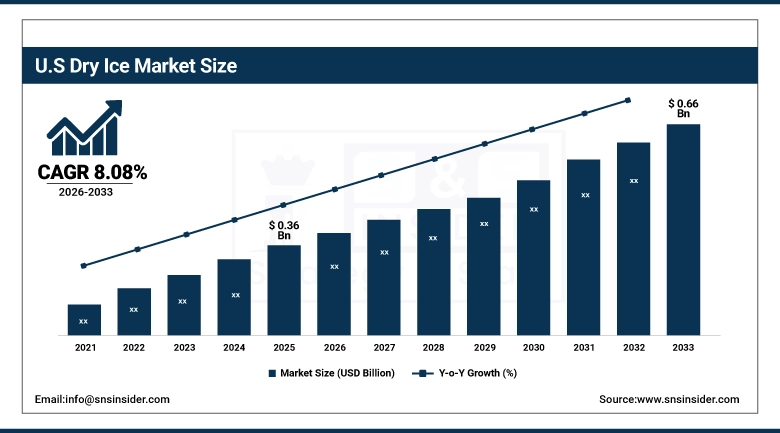

U.S. Dry Ice Market Insights:

The US Dry Ice Market was valued at USD 0.36 Billion in 2025, led by Solid Dry Ice and Food & Beverages applications. Commercial use dominated, with industrial and pharmaceutical sectors following. The market is projected to reach USD 0.66 Billion by 2033, growing at a CAGR of 8.08%.

Dry Ice Market Growth Drivers:

-

Growing cold chain logistics and pharmaceutical transport demand are driving significant opportunities in the dry ice market.

Dry Ice Market growth is driven by rising demand for cold chain logistics and temperature-sensitive shipments across food, pharmaceutical, and industrial sectors. The production of dry ice was expected to be around 1.2 million tonnes in 2025, which is forecasted to increase further over the coming decade reaching more than 2.1 million tons by 2033. Growing E-commerce, Pharmaceutical supply chain and industrial washing are driving profitable opportunities fostering higher acceptance across developed and developing economies globally.

Rising demand for cold chain logistics and pharmaceutical transport accounted for approximately 35% of global dry ice consumption in 2025.

Dry Ice Market Restraints:

-

High production costs and complex storage requirements are restricting dry ice availability and limiting broader market growth opportunities.

High costs of production and storage are limiting the growth in Dry Ice Market. CO₂ supply limitations and manufacturing capacity constraints caused 30% of dry ice production to be delayed in 2025. Delivery took an average 3–5 days longer owing to the transportation and manipulation requirements. Smaller and medium-sized dry ice producers cannot cover these costs, thus losing their competitive edge. Furthermore, strict safety standards, high energy requirements and labor shortages are reporting additional difficulties, slowing the market growth despite increasing demand for food, pharmaceuticals and industrial applications.

Dry Ice Market Opportunities:

-

Growing demand for eco-friendly, reusable cooling solutions and cryogenic storage is creating lucrative opportunities in multiple industries.

The Dry Ice market is gaining new opportunities across cold chain logistics, pharmaceutical transport, and industrial use. In 2025, dry ice use is projected to be more than 400,000 tons world-wide, and expected to exceed 750,000 tons by 2033. The rise of e-commerce, increased shipments of pharmaceuticals and adoption in industrial cleaning are leading to profitable opportunities. Rising expenditure on greener manufacturing and reusable coolants are also driving the market forward all the way up to 2033.

Cold chain logistics, pharmaceutical transport, and industrial applications accounted for 28% of dry ice usage in 2025, driven by e-commerce and industrial adoption.

Dry Ice Market Segmentation Analysis:

-

By Type, Solid Dry Ice held the largest market share of 45.87% in 2025, while Pellet Dry Ice is expected to grow at the fastest CAGR of 8.42%.

-

By Application, Food & Beverages dominated with a 38.65% share in 2025, while Pharmaceuticals is projected to expand at the fastest CAGR of 9.15%.

-

By End User, Commercial accounted for the highest market share of 42.33% in 2025, while Industrial is expected to record the fastest CAGR of 8.75%.

-

By Distribution Channel, Direct Sales held the largest share of 40.28% in 2025, while Online Retail is expected to grow at the fastest CAGR of 9.02%.

By Type Segment, Solid Dry Ice Dominated While Pellet Dry Ice Expands Rapidly:

Solid Dry Ice sector dominated by Type segment in 2025 and will generate a revenue of more than 520,000 tons, as they are extensively utilized in food transportation, industrial cleaning and pharmaceutical storage. It is easily processed, inexpensive and readily available which leads it to be the preferred material in many sectors. Pellet Dry Ice sector, the fastest growing Type segment due to growth in e-commerce cold chain logistics shipments and laboratory application; increasing demand for precise cooling for industrial products.

By Application Segment, Food & Beverages Dominated While Pharmaceuticals Expands Rapidly:

The Food & Beverages sector dominated the Application segment in 2025 with an estimated demand of over 460,000 tons of dry ice in 2025 owing to perishable goods storage, grocery delivery and frozen food logistics. And year-round demand and chain supply expansion help the segment. The Pharmaceuticals sector is the fastest-growing Application segment, projected to require about 150,000 tons in 2025, driven by vaccine distribution, laboratory sample storage, and increasing healthcare cold chain requirements. The growth of pharmaceuticals is opening new investment and production opportunities throughout the market.

By End User Segment, Commercial Dominated While Industrial Expands Rapidly:

Commercial sector dominated the End User segment in 2025 accounting for total consumption volume of dry ice over 490,000 tons, primarily used in restaurants, grocery chains, event management and cold storage room. With the regular demand, whose purchases are in bulk and frequent, it's the biggest part. The industrial sectors are the fastest-growing End User segment, using 170,000 tons in 2025, both for metal cleaning/manufacturing processes and specialty applications. The industry application segment is propelling the market with innovation and custom product segments.

By Distribution Channel Segment, Direct Sales Dominated While Online Retail Expands Rapidly:

Direct Sales sector dominated the Distribution Channel segment in 2025, with more than 480,000 ton of dry ice sold directly to direct to large commercial and industrial customers, providing convenience and bulk pricing. Good relationships with major buyers mean demand is consistent. The Online Retail sector is the fastest-growing Distribution Channel segment, distributing over 160,000 tons in 2025, driven by e-commerce grocery delivery, pharmaceutical shipping, and small-scale industrial orders. Online Retail is increasing market penetration and reaching new end users globally.

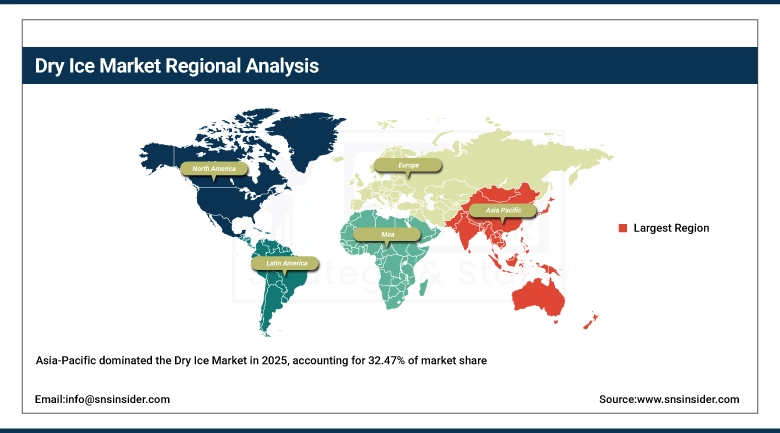

Dry Ice Market Regional Analysis:

Asia-Pacific Dry Ice Market Insights:

The Asia-Pacific Dry Ice Market dominated with more than 32.47% share in 2025, total consumption for the region being over 410,000 tons among these food & beverages, pharmaceuticals and industrial application. That puts China in the lead with 160,000 tons, followed by India at 95,000 tons. Dry Ice Blocks and Food & Beverages are the largest segments and with an increasing demand for Pellet Dry Ice. The market is mainly growing due to the growing cold chain logistics, e-commerce and rise in pharmaceuticals & industrial applications.

Get Customized Report as per Your Business Requirement - Enquiry Now

-

China Dry Ice Market Insights:

China consumed over 160,000 tons of dry ice in 2025, led by Solid Dry Ice and Food & Beverages applications. Some 95,000 tons were used in the commercial sector, with the balance applied to suit industrial and pharmaceutical requirements. Growth is fueled by the increasing cold chain logistics, e-commerce, and temperature-controlled shipments all across the country.

North America Dry Ice Market Insights:

The North America dry ice market has the fastest growing CAGR 8.46% dominated by US and Canada, consuming over 350,000 tons in 2025. It is dominated by Solid Dry Ice applications and Food & Beverages applications with Pellet Dry Ice gaining popularity. Some 200,000 tons are worth to commercial applications; the rest are utilized in industrial and pharma uses. Growth will be fueled by an increased cold chain logistics, e-commerce and temperature-sensitive shipments.

-

U.S. Dry Ice Market Insights:

In 2025, the U.S. consumed 180,000 tons of dry ice with Solid Dry Ice and Food & Beverages representing a larger share in the market. Commercial users consumed 110,000 tons and the rest went to industrial and pharmaceutical applications. Growth is widespread around the country, too, as cold chain logistics expand, e-commerce grows and there’s more demand for temperature-sensitive shipments.

Europe Dry Ice Market Insights:

The Europe Dry Ice Market exceeded 250 kilo tons in 2025; Germany accounted for over 85,000 tons while UK and France consumed over 70,000 tons & 60,000 thousand tons respectively. Of the total, 150,000 tons were for commercial sectors and the rest was used in industrial and pharmaceutical applications. Solid Dry Ice and Food & Beverages maintain its leading position; High Growth Expected for Pellet Dry Ice. Growth is supported by growth in cold chain logistics, e-commerce, and temperature-sensitive freight demand.

-

Germany Dry Ice Market Insights:

In 2025, there was a total of 85,000 tons of dry ice used in Germany (50,000 tons by commercial users and resin-glass-production; 35,000 tons by industrial and pharmaceutical applications). Strong in Solid Dry Ice & Food/Beverages; Growing Quickly in Pellet Dry Ice. Demand is being fanned by cold chain logistics, e-commerce and broader national demand for temperature-sensitive shipping.

Latin America Dry Ice Market Insights:

The Latin America used more than 35,000 tonnes of dry ice in 2025, with most in Brazil (15,000 tons), Argentina (10,000 tons) and Chile (5000 tons). By far the majority were for commercial use, industrial and pharmaceutical accounting for the rest. Growth is a result of the expansion of cold chain logistics, increased e-commerce adoption, and higher demand for temperature sensitive shipments in the region.

Middle East and Africa Dry Ice Market Insights:

The Middle East & Africa used the most dry ice in 2025 and was led by UAE at 12,000 tons and South Africa at 8,000 tons. Solid Dry Ice and Food & Beverages are the two dominate industries, with Pellet Dry Ice quickly expanding. Growth is driven by the rise of cold chain logistics, e-commerce and increasing demand for temperature-sensitive trades across the region.

Dry Ice Market Competitive Landscape:

Linde plc is leading the dry ice market with more than 25 plants by 2025. The company produces more than 500,000 tons of CO₂ per year, providing dry ice for use in food, pharmaceutical and industrial processes. With large concentrations of operations across North America, Europe and Asia, Linde prioritizes efficient operation and sustainability. Increase in infrastructure and logistic networks maintains that it remains to supply its demand, supporting its market superiority.

-

In February 2025, Linde expanded its Freeport, Texas CO₂ facility to increase dry ice production, enhancing supply for pharmaceutical and food logistics across North America. The expansion added over 50,000 tons annual capacity, improving delivery speed and reliability for temperature-sensitive shipments.

Air Products and Chemicals Inc. provides more than 400,000 tons of dry ice per year by 2025 from 20 production and distribution facilities around the world. Offering the key to food, pharmaceuticals and industry, it specializes in cryo-fermentation and cold-chain logistics. As e-commerce and temperature-sensitive goods shipping continue to increase, Air Products is growing its pellet dry ice production and logistics capabilities, ensuring that it remains the world's leading supplier of this critical product.

-

In April 2025, Air Products launched a new pellet dry ice product line designed for e-commerce cold chain deliveries. The line includes over 20 customized packaging options to optimize storage, handling, and rapid shipment for industrial and commercial customers.

The Messer Group GmbH has 18 plants in Europe and Asia, with more than 300,000 tons of CO₂ for dry ice use available from its operations in 2025. It serves the industrial, business and healthcare markets with solutions that increase productivity and ease of use. Through strategic partnerships and acquisitions, it has strengthened its distribution network for more rapid delivery and continue supply can support Messer to further consolidate its leading position in the dry ice market and enter new territories.

-

In March 2025, Messer introduced a high-density dry ice block series for industrial cleaning and food preservation applications. The new series, available in 10–50 kg blocks, aims to improve efficiency and handling while expanding its European and Asian market footprint.

Dry Ice Market Key Players:

Some of the Dry Ice Market Companies are:

-

Linde plc

-

Air Products and Chemicals Inc.

-

Messer Group GmbH

-

Air Liquide S.A.

-

Reliant Dry Ice

-

Cold Jet

-

Pacific Dry Ice

-

Continental Carbonic Products Inc.

-

SICGIL Industrial Gases

-

Polar Ice Ltd.

-

Tripti Dry Ice Co.

-

Dry Ice UK Ltd.

-

Central McGowan

-

ASCO Carbon Dioxide Ltd.

-

The Iceman

-

Chuan Chon Enterprise

-

CryoCarb

-

NEXAIR

-

Pro Trockeneis GmbH

-

Dry Ice Plus

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 1.63 Billion |

| Market Size by 2033 | USD 2.91 Billion |

| CAGR | CAGR of 7.50% From 2026 to 2033 |

| Base Year | 2025E |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Solid Dry Ice, Pellet Dry Ice, Block Dry Ice) • By Application (Food & Beverages, Healthcare & Pharmaceuticals, Industrial Cleaning, Shipping & Logistics, Entertainment, Others) • By End User (Commercial, Industrial, Healthcare, Food Processing, Others) • By Distribution Channel (Direct Sales, Distributors & Dealers, Online Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Linde plc, Air Products and Chemicals Inc., Messer Group GmbH, Air Liquide S.A., Reliant Dry Ice, Cold Jet, Pacific Dry Ice, Continental Carbonic Products Inc., SICGIL Industrial Gases, Polar Ice Ltd., Tripti Dry Ice Co., Dry Ice UK Ltd., Central McGowan, ASCO Carbon Dioxide Ltd., The Iceman, Chuan Chon Enterprise, CryoCarb, NEXAIR, Pro Trockeneis GmbH, Dry Ice Plus |

Frequently Asked Questions

Asia-Pacific dominated the Dry Ice Market with a 32.47% share in 2025.

Solid Dry Ice held the largest share in 2025, while Pellet Dry Ice is projected to grow at the fastest CAGR.

Growth is driven by rising cold chain logistics, increasing demand in food, pharmaceutical, and industrial applications, and expanding e-commerce shipments.

The market was valued at USD 1.63 Billion in 2025E and is projected to reach USD 2.91 Billion by 2033.

The Dry Ice Market is expected to grow at a CAGR of 7.50% during 2026–2033.

Get in Touch