Electrosurgical Devices Market Report Scope & Overview:

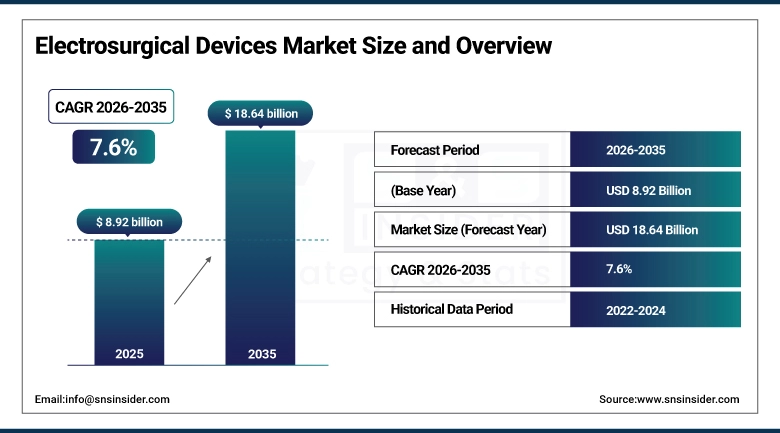

The Electrosurgical Devices Market size was estimated at USD 8.92 billion in 2025 and is expected to reach USD 18.64 billion by 2035 and grow at a CAGR of 7.6% over the forecast period of 2026-2035.

The global electrosurgical devices market is expected to grow rapidly due to the high number of surgeries being performed, preference toward minimally invasive surgical procedures, and emerging surgical energy technologies. The high prevalence of chronic diseases such as cancer, heart disease, and GI disorders are expected to boost the demand for electrosurgical devices. In addition, for higher accuracy, minimal hemorrhage during surgery, and shorter recovery time, electrosurgical approaches have thoroughly gained acceptance, especially amongst health care providers. Hospitals and ASCs are highly capitalizing on the electrosurgical equipment to elevate the efficiency of the procedure and the patient safety.

For instance, in March 2024, a clinical evaluation published in a leading surgical journal highlighted that the use of advanced electrosurgical systems reduced intraoperative bleeding by nearly 40% in minimally invasive procedures, strengthening the clinical preference for these technologies in modern operating rooms.

Electrosurgical Devices Market Size and Forecast:

-

Market Size in 2025: USD 8.92 billion

-

Market Size by 2035: USD 18.64 billion

-

CAGR: 7.6% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Electrosurgical Devices Market - Request Free Sample Report

Electrosurgical Devices Market Trends

-

The trend toward minimally invasive surgery and laparoscopy is a major driver of demand for advanced electrosurgical equipment across all medical specialties.

-

The ongoing development of electrosurgical generators and vessel sealers is increasing the precision and safeness during surgeries abroad complicated surgeries.

-

Advances in the design and development of electrosurgical devices that deliver cutting, coagulation, desiccation, and fulguration are increasing the speed and efficiency of surgical operations.

-

Abnormality in biphasic technology together with vessels nailed to sealers in venting delicate operations to reduce the thermal spread in tissues.

-

The increase in demand for ambulatory surgical centers is driving the demand for small size, affordable and portable electrosurgical equipment for usage.

-

Electrosurgical hand instruments continue to improve as a result of increasing emphasis on surgeon ergonomics and work-flow design.

-

Surgeons are upgrading their electrosurgical devices due to stringent safety standards and compliance requirements.

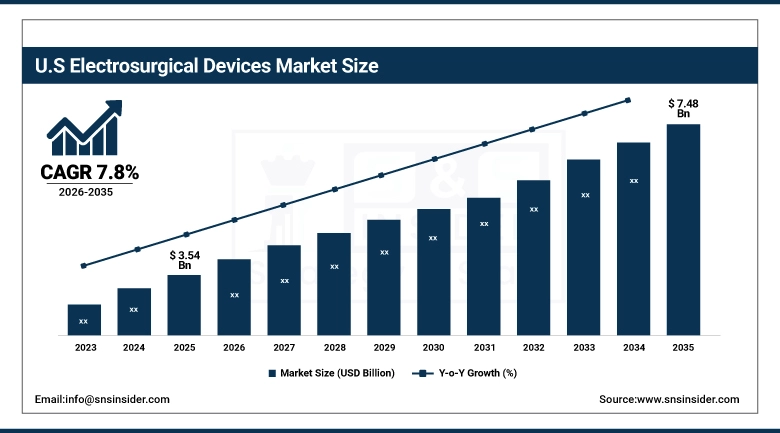

The U.S. Electrosurgical Devices Market was valued at USD 3.54 billion in 2025 and is expected to reach USD 7.48 billion by 2035 at a CAGR of 7.8% during the forecast period 2026-2035. US is one of leading regions in terms of global electrosurgical devices market as a consequence of developed surgical infrastructure, large number of surgeries performed in the country and adoption towards modern healthcare technology solution. Moreover, presence of the key players in the market, technological advancement in the surgical energy devices, and favorable reimbursement scenario have been the key factors enabling to grow at a sustainable rate.

Electrosurgical Devices Market Growth Drivers:

-

Rising Surgical Procedure Volumes and Demand for Minimally Invasive Techniques are Driving the Electrosurgical Devices Market Growth

The burden of chronic diseases is growing continuously along with the growing number of operations performed in several surgical fields including general surgery, gynecology, cardiology, and oncology, which is driving the demand for use of electrosurgical devices. Increasing adoption of minimally invasive procedures by medical professionals to minimize blood loss and length of hospital stay, as well as reduce recovery time, have contributed to the rising demand for electrosurgical technologies. Development of surgical systems having precisely controlled energy is also an indicative of development in surgical systems.

For instance, in September 2024, leading healthcare systems reported increased adoption of advanced electrosurgical platforms in laparoscopic and robotic-assisted procedures, contributing to improved surgical precision and reduced postoperative complications.

Electrosurgical Devices Market Restraints:

-

High Equipment Costs and Safety Concerns are Hampering the Electrosurgical Devices Market Growth

The high cost of electrosurgical generators, as well as additional accessories and maintaining requirements is hindering the widespread adoption of electrosurgery techniques, especially in smaller healthcare facilities and cost-sensitive markets. Other factors like thermal tissue damage, accidental burns and surgical smoke exposure raise reluctance for adopting these machines, thereby making it mandatory to follow stringent safety protocols, and training. In addition, the high aicity of regular equipment the calibration and the operational complexities disrupts workflow efficiency in the course of the techniques. All these factors cumulatively result in low adoption rates across the globe particularly in the developing regions and limit the overall growth trajectory of the market in the forecast period of 2026– 2035.

Electrosurgical Devices Market Opportunities:

-

Technological Advancements and Integration with Robotic Surgery Systems Unlock Significant Growth Opportunities for the Electrosurgical Devices Market

Integration of Electrosurgical Devices with Robotic-Assisted Surgical Systems and Imaging Technologies is the key Growth Factor for Electrosurgical Devices Market. Smart energy platforms, real-time tissue sensing, and advanced safety mechanisms are innovations that make surgical precision a reality with little collateral tissue damage. Those developments are allowing surgeons to complete complicated exercises with expanded mastery and reliability. In addition, rise in expenditure on healthcare infrastructure, coupled with the surging adoption of robotic surgery in developing economies are anticipated to provide further opportunities for the growth of this market and the adoption of products, ensuring long-term commercial success of electrosurgical technologies in various clinical applications.

For instance, in July 2024, manufacturers introduced next-generation electrosurgical systems integrated with robotic platforms, resulting in improved surgical accuracy and measurable gains in operating room efficiency across major healthcare institutions.

Electrosurgical Devices Market Segment Analysis

-

By product, electrosurgery instruments and accessories held the largest share of approximately 32.6% in 2025, and the argon and smoke management systems segment is expected to register the highest growth.

-

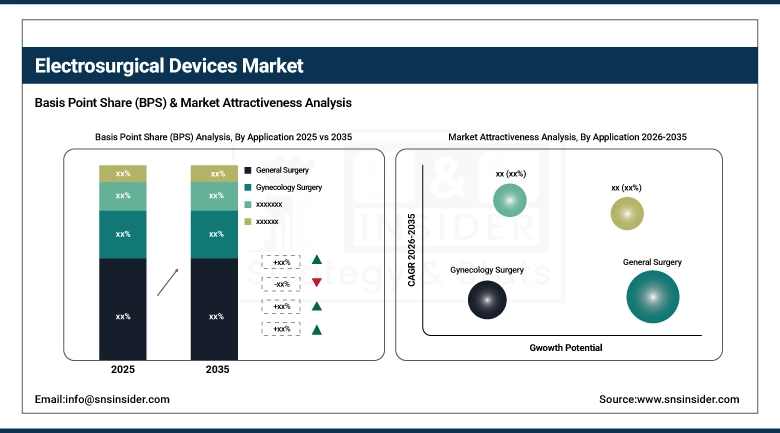

By application, general surgery dominated the market with approximately 22.8% share in 2025, while the cosmetic surgery segment is expected to register the highest growth.

-

By end-use, hospitals accounted for the leading share of nearly 61.5% in 2025, and ambulatory surgical centers are expected to register the highest growth.

By Application, General Surgery Dominates, While Cosmetic Surgery Shows Rapid Growth

In 2025, the general surgery market held largest share of revenue, accounting for 22.8% share of revenues, due to highest number of surgeries performed for various gastrointestinal, colorectal, and hepatobiliary conditions, that rely heavily on electrosurgical devices during procedures for cutting and coagulation. The increasing trend for minimally invasive surgeries in the general surgery market will provide a further boost to the market for electrosurgical devices. Based on forecast, the cosmetic surgery market is expected to achieve the highest growth through 2026-2035 owing to rising need for cosmetic surgeries, rising disposable income per capita, and a broadening acceptance of aesthetic benefits.

By Product, Electrosurgery Instruments and Accessories Lead the Market, While Argon and Smoke Management Systems Register Fastest Growth

The Electrosurgery instruments and accessories generated the largest market share of around 32.6% in 2025 due to the wide use of bipolar and monopolar surgical instruments for various operations. The electrosurgery instruments continue to play a vital role in both simple and complicated procedures because of their accuracy and efficiency in combination with modern electrosurgical generators. Instruments subsegment has captured a majority share due to their large-scale application and high-frequency replacement rates. On the other hand, the argon and smoke management systems segment is expected to exhibit the fastest growth from 2026 to 2035 as a result of growing concerns about the evacuation of surgical smoke, safety standards in operating rooms, and widespread use of argon coagulation technology.

By End-Use, Hospitals Lead, and Ambulatory Surgical Centers Register Fastest Growth

The hospitals accounted for the maximum share in 2025, estimated at about 61.5%, due to their well-developed surgical infrastructure, increased influx of patients, and expertise of surgeons. Such medical facilities will continue to dominate for complex and risky surgeries that require the use of high-performing electrosurgical units. It can be assumed that during the forecast period from 2026 through 2035, the ambulatory surgical centers will see the highest gains in market shares, considering the increasing popularity of ambulatory surgical procedures. Reduced costs and recovery time associated with the rise in the frequency of same-day procedures in such medical facilities will drive the adoption of electrosurgical equipment.

Electrosurgical Devices Market Regional Highlights:

North America Electrosurgical Devices Market Insights:

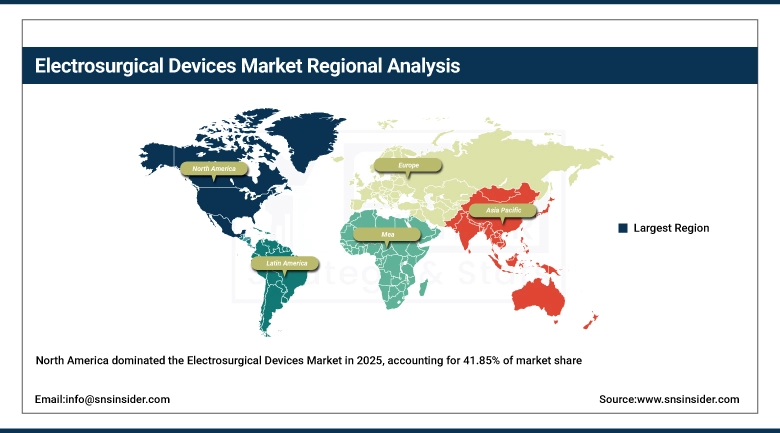

North America held the largest revenue share of over 41.85% in 2025 of the global electrosurgical devices market owing to the presence of well-established healthcare infrastructure, high surgical safety regulations, and steady investment in advanced technologies in the field of surgery. North America continues to be the largest source of demand, where increasing adoption of electrosurgical systems by hospitals, Outpatient surgical centers and specialty clinics is improving procedural accuracy, reducing operative time, and improving patient outcomes in the United States. The North America market maintains its pole position and continued revenue generation over the forecast period (2026–2035) owing to favorable reimbursement policies, high volume of surgical procedures performed annually, and continuous investment and technological innovation.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Electrosurgical Devices Market Insights:

The Asia Pacific region holds the title for being the fastest growing regional market for electrosurgical devices, driven by the development of healthcare facilities, higher numbers of surgical operations, and greater healthcare expenditure in countries like China, India, Japan, and South Korea. Growing knowledge about minimally invasive surgery, increased availability of advanced surgical equipment, and the presence of a large number of patients are some other factors contributing to regional market growth. Government efforts to develop healthcare facilities, increased private hospitals, and medical tourism are other factors aiding this market trend. The elderly population in the region and increasing instances of chronic ailments further boost the use of electrosurgical devices.

Europe Electrosurgical Devices Market Insights:

The European region accounts for the second biggest regional market share for electrosurgical devices, supported by mature health care systems, regulated environment and minimal invasive surgical procedures practiced by Germany, the UK, France and Italy. This growth is primarily driven by the increasing focus on patient safety, rising demand for energy-based surgical devices, and technological advancements in surgeries. Other factors that are providing a supportive growth included supportive government policies, presence of appropriate reimbursement policies, and capital investment by the hospitals in the new generation operating theaters.

Latin America (LATAM) and Middle East & Africa (MEA) Electrosurgical Devices Market Insights:

Electrosurgical devices are steadily penetrating Latin America and Middle East & Africa due to growing healthcare infrastructure to support growing surgical procedure volumes and rising investments in healthcare. Growth markets include Brazil, Mexico, the UAE and Saudi Arabia, where public and private healthcare providers have been trying to develop surgical capabilities and improve patient care. Yet, increasing affordability of surgical devices, rising awareness about advanced treatment solutions, and ongoing government initiatives for healthcare development are anticipated to scale up market penetration rate. However, these regions are expected to continue to show growth and improvement in access to modern surgical technologies through 2035.

Electrosurgical Devices Market Competitive Landscape:

Medtronic plc (est. 1949) is a global leader in medical technology, offering a comprehensive portfolio of electrosurgical generators, advanced energy devices, and vessel sealing systems. The company leverages its Valleylab energy platform and advanced bipolar technologies to deliver precise tissue dissection and coagulation across operating rooms, ambulatory surgical centers, and specialty clinics worldwide.

-

In February 2025, Medtronic introduced its next-generation electrosurgical energy platform with enhanced thermal spread control and integrated digital feedback systems, enabling improved surgical precision and safety across minimally invasive procedures in North America and Europe.

Johnson & Johnson MedTech (Ethicon) (est. 1886) is a diversified global medical devices company with a strong electrosurgery portfolio providing advanced energy instruments, ultrasonic devices, and surgical stapling technologies. The company integrates its electrosurgical solutions with digital surgery platforms to deliver improved clinical outcomes and procedural efficiency for hospitals and surgical centers globally.

-

In June 2024, Johnson & Johnson MedTech launched an upgraded advanced energy device platform featuring enhanced vessel sealing capabilities and real-time tissue sensing technology, strengthening its leadership in surgical energy systems across global healthcare markets.

Olympus Corporation (est. 1919) is a global provider of medical and surgical solutions specializing in electrosurgical systems, endoscopic energy devices, and minimally invasive surgical technologies. The company’s ESG series generators and advanced bipolar instruments serve major healthcare institutions across Asia Pacific, Europe, and North America, combining precision energy delivery with optimized workflow integration.

-

In October 2024, Olympus expanded its electrosurgical product portfolio across emerging Asian markets, collaborating with regional healthcare providers to deploy advanced energy-based surgical systems in high-growth hospital networks.

Electrosurgical Devices Market Key Players:

-

Medtronic plc

-

Johnson & Johnson MedTech (Ethicon)

-

Olympus Corporation

-

B. Braun Melsungen AG

-

Erbe Elektromedizin GmbH

-

CONMED Corporation

-

Smith & Nephew plc

-

Karl Storz SE & Co. KG

-

Applied Medical Resources Corporation

-

Boston Scientific Corporation

-

Kirwan Surgical Products LLC

-

Bovie Medical Corporation

-

Megadyne Medical Products, Inc.

-

Integra LifeSciences Holdings Corporation

-

Stryker Corporation

-

Zimmer Biomet Holdings, Inc.

-

LED SpA

-

Ellman International, Inc.

-

Utah Medical Products, Inc.

-

EMED Sp. z o.o.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.92 Billion |

| Market Size by 2035 | USD 18.64 Billion |

| CAGR | CAGR of 7.6% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Electrosurgical Generators, Active Electrodes, Dispersive Electrodes, Electrosurgery Instruments & Accessories, Argon and Smoke Management Systems, Others) • By Application (General Surgery, Gynecology Surgery, Urologic Surgery, Orthopedic Surgery, Cardiovascular Surgery, Cosmetic Surgery, Neurosurgery, Others) • By End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Medtronic plc, Johnson & Johnson MedTech (Ethicon), Olympus Corporation, B. Braun Melsungen AG, Erbe Elektromedizin GmbH, CONMED Corporation, Smith & Nephew plc, Karl Storz SE & Co. KG, Applied Medical Resources Corporation, Boston Scientific Corporation, Kirwan Surgical Products LLC, Bovie Medical Corporation, Megadyne Medical Products, Inc., Integra LifeSciences Holdings Corporation, Stryker Corporation, Zimmer Biomet Holdings, Inc., LED SpA, Ellman International, Inc., Utah Medical Products, Inc., EMED Sp. z o.o. |

Frequently Asked Questions

The Electrosurgical Devices Market was valued at USD 8.92 billion in 2025 and is projected to reach USD 18.64 billion by 2035, growing at a CAGR of 7.6% during the forecast period of 2026 to 2035.

The Electrosurgical Devices Market is driven by rising surgical procedure volumes, increasing preference for minimally invasive techniques, and continuous advancements in surgical energy technologies.

In the Electrosurgical Devices Market, electrosurgery instruments and accessories hold the largest share of approximately 32.6% in 2025 due to their widespread usage across various surgical procedures.

North America leads the Electrosurgical Devices Market with over 41.85% share in 2025, supported by advanced healthcare infrastructure and strong adoption of innovative surgical technologies.

Key trends in the Electrosurgical Devices Market include increasing adoption of minimally invasive procedures, rising use of bipolar and vessel sealing technologies, and growing demand for integrated and multifunctional electrosurgical systems.

Get in Touch