Enterprise Agentic AI Market Report Scope & Overview:

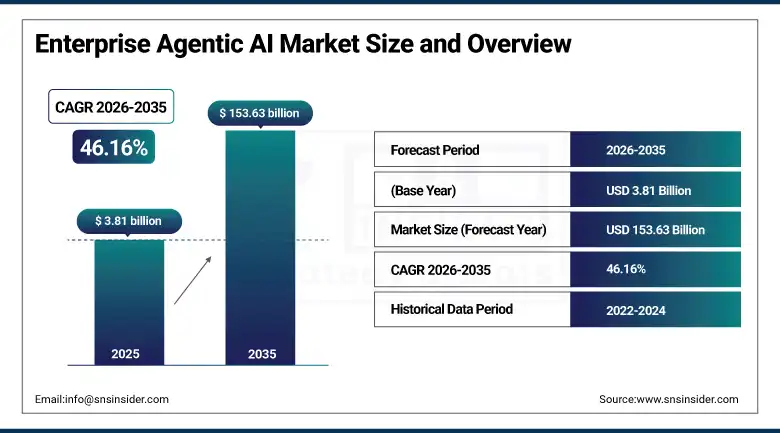

The Enterprise Agentic AI Market was valued at USD 3.81 Billion in 2025 and is expected to reach USD 153.63 Billion by 2035, growing at a CAGR of 46.16% from 2026–2035.

The global enterprise agentic AI market is at the beginning of its most commercially consequential growth phase as autonomous AI agents transition from research demonstrations into operational enterprise software that independently plans, reasons, executes multi-step workflows, and adapts its behaviour based on outcomes without requiring human involvement at each task step. Enterprise agentic AI systems differ fundamentally from earlier AI models and chatbots. They are goal-directed. They use tools, access APIs, query databases, write code, and coordinate with other agents to complete complex business processes that previously required dedicated human teams.

In 2025, global enterprise agentic AI adoption surged by 65%, with 70% of Fortune 500 firms piloting autonomous AI to enhance productivity. Agent creation surged 119% in the first half of 2025, with employee interactions with AI agents growing at an average monthly rate of 65%. Companies project an average ROI of 171% from agentic AI deployments, with U.S. enterprises expecting 192% ROI, demonstrating the commercial validation that is accelerating enterprise adoption across every industry vertical.

Market Size and Forecast

-

Market Size in 2026E: USD 5.57 Billion

-

Market Size by 2035: USD 153.63 Billion

-

CAGR: 46.16% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Enterprise Agentic AI Market - Request Free Sample Report

Enterprise Agentic AI Market Trends

-

Rising adoption of multi-agent orchestration frameworks where specialised AI agents collaborate across complex business workflows is enabling enterprises to automate end-to-end processes.

-

Growing deployment of pre-built enterprise AI agent templates through platforms including Salesforce Agentforce, Microsoft Copilot Studio, and ServiceNow Now Assist.

-

Increasing integration of agentic AI with enterprise data infrastructure including ERP, CRM, and ITSM systems is enabling autonomous agents to access, process, and act on real business data.

-

Rising enterprise focus on agentic AI governance, human oversight mechanisms, and audit trail capability is creating demand for explainable, controllable autonomous agent platforms.

-

Expanding investment in vertical-specific agentic AI applications including clinical documentation automation in healthcare, autonomous trade compliance in financial services.

U.S. Enterprise Agentic AI Market Outlook

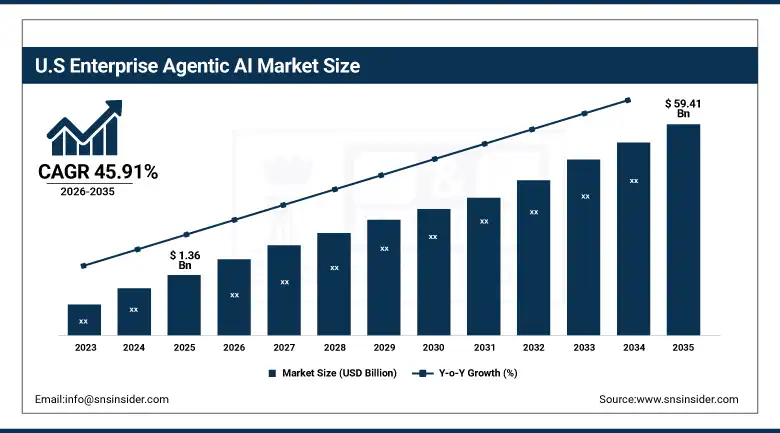

The U.S. Enterprise Agentic AI Market was valued at approximately USD 1.36 Billion in 2025 and is expected to reach approximately USD 59.41 Billion by 2035, growing at a CAGR of approximately 45.91%.

The United States is the world’s largest and most commercially advanced enterprise agentic AI market, anchored by the headquarters concentration of both the leading platform providers and the most sophisticated enterprise adopters whose AI investment programmes define global deployment standards. Microsoft, Salesforce, Google, Amazon AWS, ServiceNow, and Workday collectively dominate the enterprise agentic AI platform market from their U.S. headquarters, while the most aggressive early adopters across financial services, technology, healthcare, and professional services are concentrated in the North American enterprise community.

Salesforce’s Agentforce platform generated over USD 100 million in annual recurring revenue within its first commercial quarter following launch, with more than 5,000 enterprise customers deploying autonomous customer service, sales, and operational agents. The commercial velocity demonstrated by Agentforce’s rapid revenue generation validated enterprise agentic AI’s transition from pilot experimentation to production deployment at commercial scale.

Enterprise Agentic AI Market Segment Analysis

-

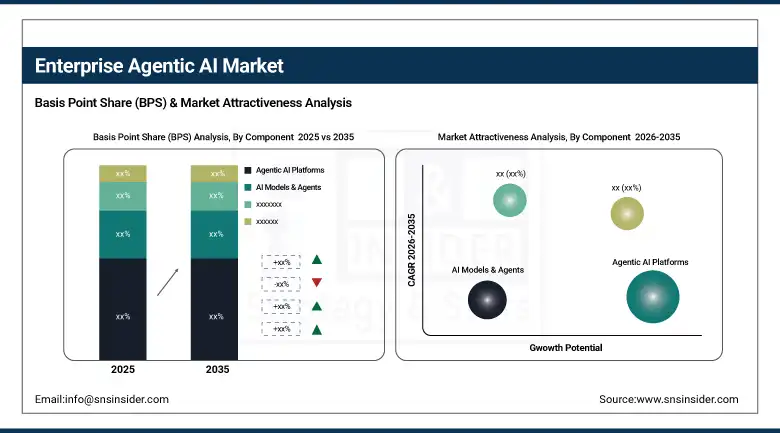

By Component, the Agentic AI Platforms segment dominated the Enterprise Agentic AI Market with 33.8% share in 2025, while the AI Models & Agents segment is the fastest growing at a CAGR of 29.6% during 2026–2035.

-

By Deployment Mode, the Cloud-Based segment dominated the Enterprise Agentic AI Market with 57.4% share in 2025, while the Hybrid Deployment segment is the fastest growing during 2026–2035.

-

By End User, the IT & Telecom segment dominated the Enterprise Agentic AI Market with 31.5% share in 2025, while the Healthcare segment is the fastest growing during 2026–2035.

-

By Application, the IT Operations & AIOps segment dominated the Enterprise Agentic AI Market in 2025, while the Customer Experience & CX Automation segment is the fastest growing during 2026–2035.

By Component, agentic AI platforms dominate, AI models & agents grow fastest

Agentic AI platforms retained the dominant component position with 33.8% of the enterprise agentic AI market in 2025. The commercial primacy of platforms reflects the enterprise procurement logic of consolidating agentic AI capability within established software vendor relationships whose security, compliance, and integration credentials are already validated within the enterprise’s existing technology governance framework. Platform dominance is self-reinforcing: each agent deployed through an established platform generates usage data that improves the platform’s model quality and workflow orchestration capability, strengthening the incumbent advantage over time.

AI models and agents are the fastest-growing component at a CAGR of 29.6% through 2035 as the commercial availability of increasingly capable foundation models from Anthropic, OpenAI, Google DeepMind, and Meta creates a continuously improving capability substrate for enterprise agent construction.

By End User, IT & telecom dominates, healthcare grows fastest

IT and Telecom retained the dominant end user position with 31.5% of the enterprise agentic AI market in 2025. The sector’s commercial leadership reflects its above-average AI technology adoption velocity, the direct operational alignment between IT operations automation and agentic AI’s autonomous task execution capability, and the scale of the sector’s AI investment budget relative to other enterprise verticals. IT and telecom organisations deploying agentic AI for incident detection and resolution, change management workflow automation, infrastructure monitoring, and network configuration management are achieving the most measurable and commercially quantifiable productivity improvements of any enterprise sector, creating reference case studies that accelerate cross-vertical adoption.

Healthcare is the fastest-growing end user segment in the enterprise agentic AI market because the sector’s combination of extraordinary administrative burden, physician time scarcity, and the measurable patient outcome improvements that automation enables creates one of the most commercially compelling agentic AI ROI cases of any enterprise vertical.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Enterprise Agentic AI Market Insights

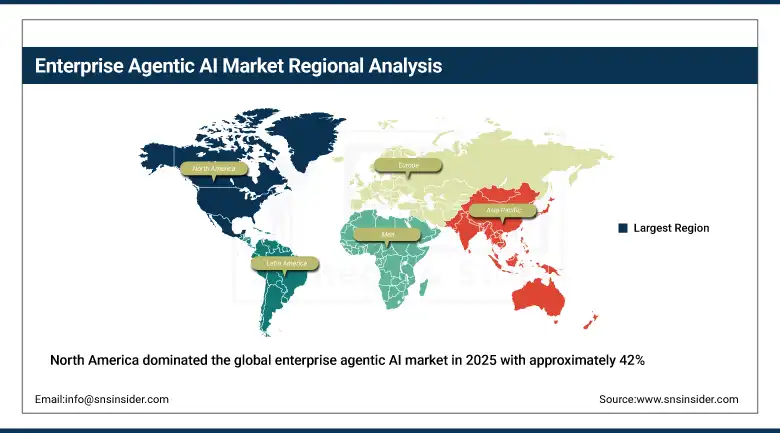

North America dominated the global enterprise agentic AI market in 2025 with approximately 42% of global revenues, with the United States accounting for approximately 87.4% of North American revenues. The region’s market leadership is grounded in its concentration of the world’s leading AI platform providers, the most commercially aggressive enterprise AI adopters, and the deepest AI engineering talent pool whose combined investment creates the most commercially advanced agentic AI deployment environment globally.

Canada contributes approximately 12.6% of North American revenues through its sophisticated enterprise technology market, active AI research ecosystem anchored by the Vector Institute and Mila, and the progressive enterprise AI adoption across its financial services, telecommunications, and public sector organisations whose agentic AI investment is accelerating in alignment with the federal government’s Pan-Canadian AI Strategy investment in commercialising Canadian AI research excellence.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Enterprise Agentic AI Market Insights

Europe is a commercially significant enterprise agentic AI market where the EU AI Act’s regulatory framework for high-risk AI systems, GDPR’s data processing requirements, and the progressive enterprise digital transformation investment of the continent’s largest corporations are collectively shaping a market whose commercial growth is occurring within a distinctly compliance-conscious procurement environment.

Germany accounts for approximately 22.3% of European revenues through its concentration of global industrial enterprises whose manufacturing, logistics, and finance operations are generating agentic AI investment in supply chain automation, predictive maintenance orchestration, and financial compliance workflow automation that represents some of Europe’s most commercially advanced production agentic AI deployments.

Asia Pacific Enterprise Agentic AI Market Insights

Asia Pacific is the fastest-growing regional enterprise agentic AI market, driven by China’s government-backed enterprise AI investment programme, India’s technology services sector’s rapid agentic AI adoption for service delivery automation, Japan’s manufacturing sector’s autonomous process optimisation investment, and Southeast Asia’s rapidly digitalising financial services and retail sectors whose enterprise AI adoption is accelerating with each year of cloud infrastructure maturation.

China accounts for approximately 44.8% of Asia Pacific revenues through its combination of government-sponsored enterprise AI adoption programmes, domestic platform providers including Baidu, Alibaba, and Huawei whose agentic AI capabilities serve the Chinese enterprise market, and the extraordinary pace of enterprise digital transformation investment that characterises the country’s commercial modernisation agenda.

MEA & Latin America Enterprise Agentic AI Market Insights

The Middle East and Africa and Latin America are growing enterprise agentic AI markets where government digital transformation investment, expanding cloud infrastructure, and the commercial adoption of AI productivity platforms by financial services and technology companies are creating structured demand for autonomous enterprise workflow automation.

UAE leads MEA revenues at approximately 38.4% of the regional total through Dubai’s Smart City AI investment programme, the DIFC financial sector’s active AI adoption, and the UAE government’s explicit national AI strategy whose enterprise adoption targets are creating institutional motivation for agentic AI deployment across public and private sector organisations.

Market Dynamics

Growth Drivers: Enterprise operational automation imperative creating strong AI agent ROI justification driving the market growth

The enterprise operational automation imperative is the market’s most powerful commercial growth driver. Enterprises across every sector face simultaneous pressure to improve operational efficiency, reduce labour cost, accelerate process execution, and improve output quality without proportional headcount growth. Agentic AI directly addresses this imperative by enabling autonomous execution of the repetitive, multi-step cognitive tasks that constitute the majority of knowledge worker time consumption. The demonstrated ROI of 171% average and 192% for U.S. enterprises creates a commercially compelling investment case that is accessible to any enterprise CFO evaluating technology capital allocation decisions, sustaining adoption momentum that is independent of discretionary technology enthusiasm.

Restraints: Enterprise trust deficit in autonomous AI decision-making for high-stakes workflows

The enterprise trust deficit in autonomous AI decision-making represents the most commercially significant barrier to agentic AI adoption acceleration. Business leaders whose approval is required for enterprise AI investment carry both the accountability for outcomes that autonomous agents produce and the personal career risk that AI system failures create in high-visibility business processes. This accountability structure creates a preference for human-in-the-loop deployment configurations that preserve oversight at commercially important decision points, limiting the full automation scope that agentic AI technology is capable of delivering and constraining the ROI that conservative deployment configurations achieve relative to full-autonomy alternatives.

Opportunities: Vertical AI agent specialisation creating premium-priced domain-specific deployment

Vertical specialisation represents the most commercially differentiated near-term opportunity in the enterprise agentic AI market. Generic agentic AI platforms deliver broad capability but require substantial customisation to achieve the domain-specific performance that enterprise procurement teams require for regulated, compliance-sensitive, or technically specialised business processes. Vertical AI agents purpose-built for clinical documentation, legal contract analysis, financial regulatory reporting, or manufacturing quality inspection command premium pricing and generate higher customer retention than general-purpose alternatives whose configuration burden creates implementation friction that specialist solutions eliminate.

Recent Developments:

-

2025: Microsoft Copilot Studio surpassed 100,000 active organisation deployments by early 2026, establishing Microsoft as the enterprise agentic AI platform market’s leading commercial deployment vehicle and validating the strategic effectiveness of embedding agentic AI capability within the Microsoft 365 and Azure enterprise software ecosystem that the majority of global enterprises already operate.

-

2025: Salesforce Agentforce generated over USD 100 million in annual recurring revenue within its first commercial quarter, with more than 5,000 enterprise customers deploying autonomous customer service, sales, and operational agents, demonstrating the commercial velocity that purpose-built enterprise agentic AI applications achieve when embedded within established CRM and enterprise software relationship frameworks.

-

2024: Google Cloud developed its Enterprise Agent Orchestration capability in Vertex AI Agent Builder in 2024, enabling companies to deploy teams of specialised AI agents that coordinate to complete complex tasks across enterprise data sources, creating an enterprise-grade multi-agent orchestration infrastructure whose integration with Google Workspace and BigQuery provides natural data access for enterprise agent deployments.

Enterprise Agentic AI Market Key Players

-

Microsoft Corporation

-

Salesforce Inc.

-

ServiceNow Inc.

-

Google LLC

-

Amazon Web Services Inc.

-

Anthropic PBC

-

OpenAI Inc.

-

Workday Inc.

-

UiPath Inc.

-

IBM Corporation

-

SAP SE

-

Oracle Corporation

-

Cohere Inc.

-

Inflection AI Inc.

-

Cognigy GmbH

-

Moveworks Inc.

-

Leena AI Inc.

-

Ema Inc.

-

CrewAI Inc.

-

LangChain Inc.

Enterprise Agentic AI Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.81 Billion |

| Market Size by 2035 | USD 153.63 Billion |

| CAGR | CAGR of 46.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Power Rating (Low-power Rating Projects, High-power Rating Projects) • By Converter Technology (Line Commutated Converter, Voltage Source Converter) • By Transmission Type (Point-to-Point, Back-to-Back, Multi-Terminal) • By Application (Offshore Wind Integration, Cross-Border Interconnections, Long-Distance Bulk Power Transmission, Urban Underground Transmission, Others) • By End-User (Utilities, Renewable Power Plants, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Microsoft Corporation, Salesforce Inc., ServiceNow Inc., Google LLC, Amazon Web Services Inc., Anthropic PBC, OpenAI Inc., Workday Inc., UiPath Inc., IBM Corporation, SAP SE, Oracle Corporation, Cohere Inc., Inflection AI Inc., Cognigy GmbH, Moveworks Inc., Leena AI Inc., Ema Inc., CrewAI Inc., LangChain Inc. |

Frequently Asked Questions

Get in Touch