Feminine Hygiene Products Market Report Scope & Overview:

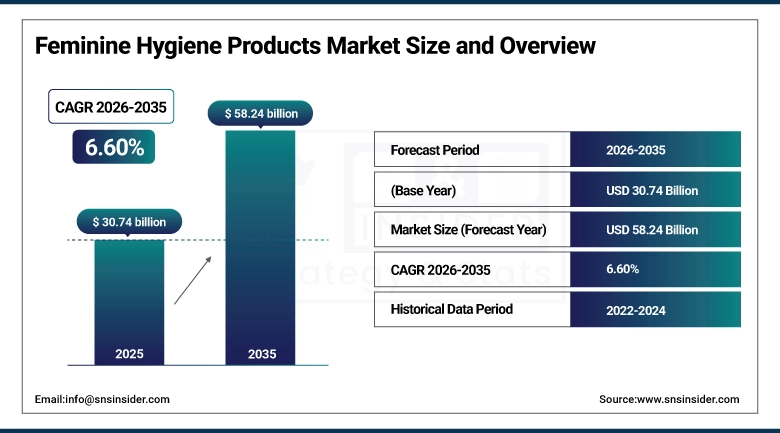

The Feminine Hygiene Products Market size was valued at USD 30.74 billion in 2025 and is expected to reach USD 58.24 billion by 2035, growing at a CAGR of 6.60% over the forecast period of 2026–2035.

Global feminine hygiene products market is expected to grow due to rising awareness regarding menstrual health, increasing participation of women in workforce, and improved access to hygiene products in developing as well-developed economy. Increasing focus on personal hygiene, driven by government-led education and awareness campaigns, is promoting regular consumption of the product among women in various age groups. Continuous product innovation in the form of organic, biodegradable, and skin-friendly material use is also supplementing the market due to their appeals towards sustainable and health safety concerns. Moreover, the increasing penetration of retail distribution channels, especially e-commerce platforms and pharmacy networks is also aiding access to these products across both urban and rural markets. Manufacturers are actively addressing changing consumer preferences and cultural sensitivities in this space by offering product differentiation, enhanced comfort, and discreet products packaging solutions.

For instance, in March 2024, a global health initiative reported a significant increase in menstrual hygiene awareness programs across Asia and Africa, leading to improved adoption of sanitary products and reinforcing long-term market growth potential.

Feminine Hygiene Products Market Size and Forecast:

-

Market Size in 2025: USD 30.74 billion

-

Market Size by 2035: USD 58.24 billion

-

CAGR: 6.60% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Feminine Hygiene Products Market - Request Free Sample Report

Feminine Hygiene Products Market Trends

-

Trend towards using organic and biodegradable feminine hygiene products fueled by increasing consciousness about environmental protection and health risks associated with chemicals.

-

Increase in usage of reusable products like menstrual cups and cloth pads due to their economic feasibility and sustainability features.

-

Growth in use of online platforms which provide discreetness and product accessibility even in underserved areas of the world.

-

Focus on constant product development that will be characterized by thinness, high absorbability, and increased comfort levels for customers.

-

Involvement of governments and NGOs in campaigns aimed at raising awareness about menstruation and creating affordable and accessible solutions for low-income communities.

-

Increasing investments into advertising, especially on social media, to attract younger consumers and educate them.

-

Increasing demand for dermatologically-tested premium hygiene products.

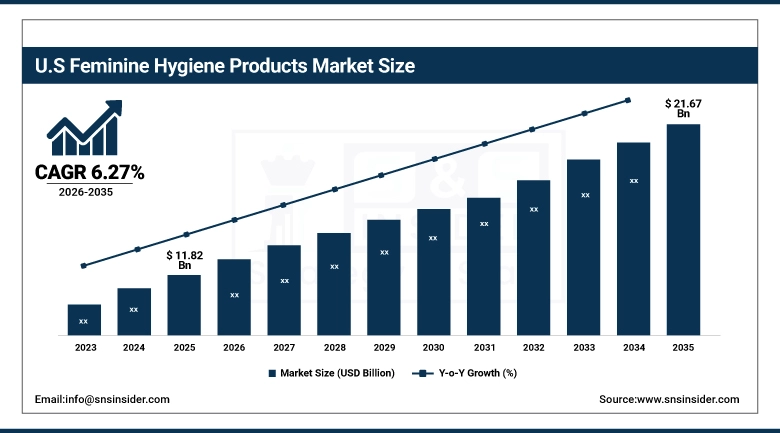

The U.S. Feminine Hygiene Products Market was valued at USD 11.82 billion in 2025 and is expected to reach USD 21.67 billion by 2035, growing at a CAGR of 6.27% from 2026–2035. High consumer awareness, well-established retail networks and presence of leading companies has helped the U.S. event to remain dominant in global feminine hygiene products market. Factors such as easy availability of products through supermarkets, pharmacy stores, and the internet; periodic innovation in the products; and premiumization propel the growth of this market. Additionally, increasing consumer demand for organic and sustainable products, as well as effective marketing strategies and supportive policies and legislations will aid the growth of market in upcoming few years.

Feminine Hygiene Products Market Growth Drivers:

-

Rising Awareness Around Menstrual Health and Hygiene is Driving the Feminine Hygiene Products Market Growth

The growing awareness regarding menstrual health, hygiene practices and the need for safe and reliable feminine care products is leading to a significant impact on consumer behavior trends across advanced as well as developing economies. Such increase in consumption of such products has been due to government programs, awareness drives and efforts made by different nonprofit organizations that have helped in removing the taboo on menstruation. In addition, the increasing availability of different types of products such as sanitary pads & menstrual cups are contributing to the continuing growth of this market.

For instance, in May 2024, the Indian government expanded its menstrual hygiene scheme to improve access to low-cost sanitary products in rural areas, significantly boosting product adoption and awareness among underserved populations.

Feminine Hygiene Products Market Restraints:

-

Environmental Concerns and Disposal Challenges are Hampering the Feminine Hygiene Products Market Growth

The escalating effects on the environment due to the disposal of non-biodegradable female health care products constitute one of the major issues facing the market growth. Regular sanitary products include components such as plastics, which result in environmental pollution over time. Also, poor waste management facilities in some developing regions are a hindrance to proper disposal procedures. All these issues are making way for the adoption of eco-friendly sanitary products, hence limiting the potential for market growth from 2026 to 2035.

Feminine Hygiene Products Market Opportunities:

-

Growing Demand for Sustainable and Organic Products is Creating Significant Opportunities for the Feminine Hygiene Products Market

The growing need for eco-friendly, organic, and reusable women’s hygiene products provides new opportunities for market expansion. People are becoming more interested in purchasing goods created using natural materials like organic cotton and biodegradable substances due to their environmental benefits as well as their impact on one’s health. The new products in terms of their designs like reusable menstrual cups and biodegradable pads become popular. It will bring numerous opportunities for development for brands producing such goods, help with differentiation, and build brands.

For instance, in March 2024, several leading personal care brands introduced biodegradable sanitary product lines, reporting a notable increase in consumer preference for sustainable alternatives and reinforcing the shift toward eco-conscious purchasing behavior.

Feminine Hygiene Products Market Segment Analysis

-

By product, menstrual care products held the largest share of approximately 48.35% in 2025, and the cleaning and deodorizing products segment is expected to register the highest growth with a CAGR of 11.23%.

-

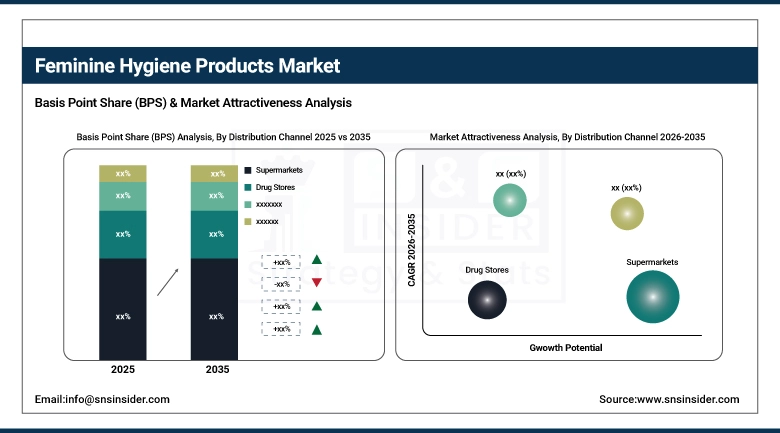

By distribution channel, supermarkets dominated the market with approximately 62.47% share in 2025, while the online retail stores segment is expected to register the highest growth with a CAGR of 11.58%.

By Distribution Channel, Supermarkets Dominate, While Online Retail Stores Show Rapid Growth

In 2025, the supermarkets segment accounted for the highest market share of 62.47% over others which is due to well-established retail presence, availability of variety and preference of customers towards purchasing personal care products via physical stores. Supermarkets contain a plethora of different kinds of feminine hygiene products, making it easier for customers to compare and purchase. During the forecasted period, online retail stores will witness the highest CAGR, driven by increased digitization, a trend towards discreet shopping and an increase of e-commerce platforms. Factors behind the rapid online retail growth include subscription-based products, more product variety and ubiquitous internet services.

By Product, Menstrual Care Products Lead the Market, While Cleaning and Deodorizing Products Register Fastest Growth

Menstrual care products occupied the highest market revenue share of 48.35% in 2025, attributable to the extensive use of sanitary pads, tampons, and menstrual cups among urban and rural communities. The menstrual care products meet hygiene requirements, comfort considerations, and the awareness concerning managing menstruation amongst females on an international scale. On the other hand, it is expected that the cleaning and deodorizing products will experience the highest CAGR of around 11.23% between 2026 to 2035. This is attributable to growing consumer preference for maintaining intimacy hygiene and daily cleanliness habits. Factors responsible for market growth are product innovations, hygiene products' growing prevalence, increased focus on preventing infections, and wide distribution of products in emerging economies.

Feminine Hygiene Products Market Regional Highlights:

North America Feminine Hygiene Products Market Insights:

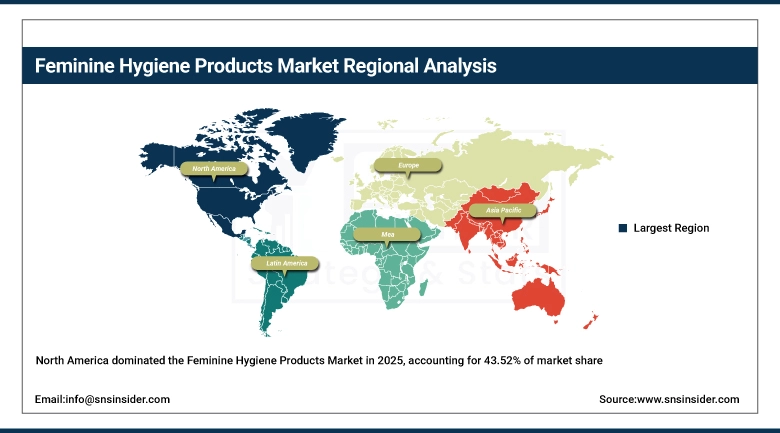

North America accounted for more than 43.52% of the total revenue generated in 2025 in the global feminine hygiene products market owing to the presence of a highly evolved healthcare infrastructure along with good consumer awareness about personal hygiene and constant innovations being made by key players in their products. The United States is one of the main sources of demand owing to a highly developed retail infrastructure along with an inclination towards organic and premium products in the country. North America thus holds the most dominant position in the market owing to such factors as well as initiatives towards sustainability.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Feminine Hygiene Products Market Insights:

The Asia-Pacific region is the fastest-growing region in the feminine hygiene products industry, recording a compound annual growth rate of 6.60% due to increased population, increased awareness regarding menstruation hygiene, and increased availability of affordable feminine hygiene products in countries such as China, India, Japan, and South Korea. Increased distribution networks, health campaigns initiated by governments, and increased production by local manufacturers have been crucial factors contributing to the growth of the market in the region. Menstrual health awareness campaigns, urbanization trends, and higher disposable income among the people are driving the growth of the market.

Europe Feminine Hygiene Products Market Insights:

Europe accounts for the second largest share of the global feminine hygiene products market, with robust consumer awareness, availability of various options in existing shops as well as online, and growing demand for organic/ eco-friendly alternatives driving sales growth across Germany, UK, France and Netherlands. Factors such as regulatory policies centered on ensuring product safety, environmental concerns, and usage of reusable menstrual hygiene products are fueling the market growth in the region. Increasing penetration of both retail stores and online stores along with sustainable material utilization in the region will continue to influence the market.

Latin America (LATAM) and Middle East & Africa (MEA) Feminine Hygiene Products Market Insights:

Increasing awareness about menstruation, better healthcare facilities, and improved infrastructure are slowly helping women in Latin America as well as Middle East & Africa to adopt feminine hygiene products. Brazil, Mexico, United Arab Emirates, and Saudi Arabia are some of the key markets in their respective geographies that are witnessing an upsurge in the adoption of sanitary products. The increased availability of cost-effective products, higher involvement of women in the workforce, and favorable policies are predicted to positively influence market penetration going forward. It is likely to aid the market in realizing consistent gains till 2035.

Feminine Hygiene Products Market Competitive Landscape:

Procter & Gamble, Co-Founded in 1837 is one of the world’s largest a supplier of feminine hygiene and personal care products and offers a complete line-up of sanitary pads, tampons, pantyliners and intimate care products under various household brands. P&G employs advanced material science and its proprietary consumer insights tech platforms to develop high quality hygiene products across multiple distribution verticals worldwide.

-

In February 2025, Procter & Gamble introduced an upgraded range of ultra-thin sanitary pads with improved absorbent core technology, enabling enhanced comfort and leakage protection for consumers across North America and emerging Asia Pacific markets.

Kimberly-Clark Corporation (est. 1872) is a diversified global personal care company with a strong feminine hygiene portfolio providing Kotex-branded sanitary products, liners, and tampons. The company integrates its product innovation pipeline with sustainable material sourcing and digital consumer engagement platforms to deliver improved product performance and environmental responsibility across global retail markets.

-

In August 2024, Kimberly-Clark launched a new line of biodegradable feminine hygiene products featuring plant-based materials and eco-friendly packaging, strengthening its position in the sustainable hygiene segment across Europe and North America.

Unicharm Corporation (est. 1961) is a global provider of personal hygiene solutions specializing in feminine care, baby care, and adult incontinence products. The company’s Sofy and Center-In product lines serve major markets across Asia Pacific, the Middle East, and Latin America, combining high absorption efficiency with ergonomic design and skin-friendly materials.

-

In October 2024, Unicharm expanded its premium sanitary napkin portfolio in Southeast Asia, introducing advanced breathable materials and enhanced fit technology to cater to evolving consumer preferences in countries such as Indonesia and Thailand.

Feminine Hygiene Products Market Key Players:

-

Procter & Gamble Co.

-

Kimberly-Clark Corporation

-

Unicharm Corporation

-

Johnson & Johnson

-

Essity AB

-

Edgewell Personal Care Company

-

Ontex Group NV

-

Hengan International Group Company Limited

-

Kao Corporation

-

Unilever PLC

-

First Quality Enterprises, Inc.

-

Bodywise (UK) Limited

-

The Honest Company, Inc.

-

Natracare LLC

-

Seventh Generation, Inc.

-

Maxim Hygiene Products

-

Corman S.p.A.

-

Groupe Lemoine

-

Drylock Technologies

-

Premier FMCG (Lil-Lets)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 30.74 Billion |

| Market Size by 2035 | USD 58.24 Billion |

| CAGR | CAGR of 6.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product [Menstrual Care Products (Sanitary Napkins, Tampons, Menstrual Cups, Others), Cleaning & Deodorizing Products (Feminine Powders, Soaps and Washes, Others)] • By Distribution Channel (Supermarkets, Drug Stores, Online Retail Stores, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Procter & Gamble Co., Kimberly-Clark Corporation, Unicharm Corporation, Johnson & Johnson, Essity AB, Edgewell Personal Care Company, Ontex Group NV, Hengan International Group Company Limited, Kao Corporation, Unilever PLC, First Quality Enterprises Inc., Bodywise (UK) Limited, The Honest Company Inc., Natracare LLC, Seventh Generation Inc., Maxim Hygiene Products, Corman S.p.A., Groupe Lemoine, Drylock Technologies, Premier FMCG (Lil-Lets) |

Frequently Asked Questions

The Feminine Hygiene Products Market was valued at USD 30.74 billion in 2025 and is projected to reach USD 58.24 billion by 2035, growing at a CAGR of 6.60% during the forecast period.

The Feminine Hygiene Products Market is driven by increasing menstrual health awareness, rising female workforce participation, expanding access to hygiene products, and continuous innovation in organic and sustainable product offerings.

North America holds the largest share in the Feminine Hygiene Products Market due to high consumer awareness, strong retail infrastructure, and increasing demand for premium and sustainable hygiene products.

Menstrual care products dominate the Feminine Hygiene Products Market, accounting for approximately 48.35% market share in 2025, supported by widespread use of sanitary napkins, tampons, and menstrual cups.

Key trends in the Feminine Hygiene Products Market include rising demand for biodegradable products, increased adoption of reusable menstrual solutions, expansion of e-commerce channels, and growing focus on product comfort and sustainability.

Get in Touch