Menstrual Care Products Market Report Scope & Overview:

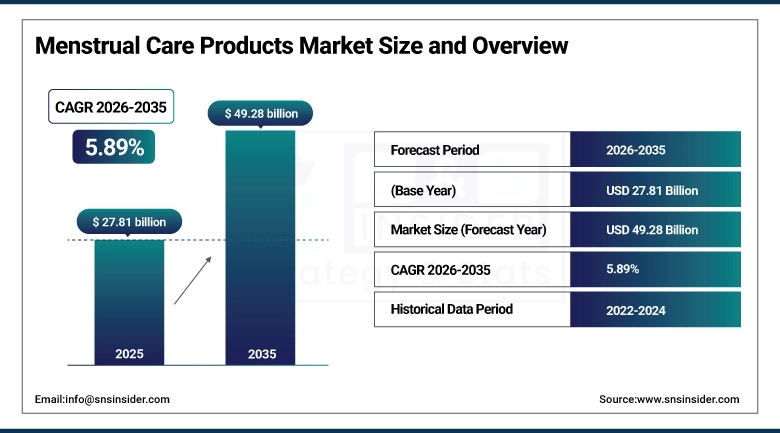

The Menstrual Care Products Market size was valued at USD 27.81 Billion in 2025 and is projected to reach USD 49.28 Billion by 2035, growing at a CAGR of 5.89% during 2026–2035.

The Menstrual Care Products Market is growing steadily owing to factors such as a rise in awareness of menstrual hygiene, an increase in the female population, and a rise in accessibility of products. In terms of product innovation, factors such as comfort, sustainability, and organic products are becoming popular. Factors such as urbanization and an increase in e-commerce activities are also boosting market penetration. In addition, government initiatives and campaigns are helping to reduce stigma associated with using such products, thereby boosting market growth.

Menstrual Care Products Market Size and Forecast:

-

Market Size in 2025: USD 27.81 Billion

-

Market Size by 2035: USD 49.28 Billion

-

CAGR: 5.89% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Menstrual Care Products Market - Request Free Sample Report

Menstrual Care Products Market Key Trends:

-

Increasing demand for organic, biodegradable, and sustainable menstrual care products.

-

Rising adoption of reusable products such as menstrual cups and period underwear.

-

Growing influence of e-commerce and direct-to-consumer brands.

-

Product innovation focused on enhanced comfort, absorbency, and skin-friendly materials.

-

Increasing awareness campaigns and normalization of menstruation through social and digital platforms.

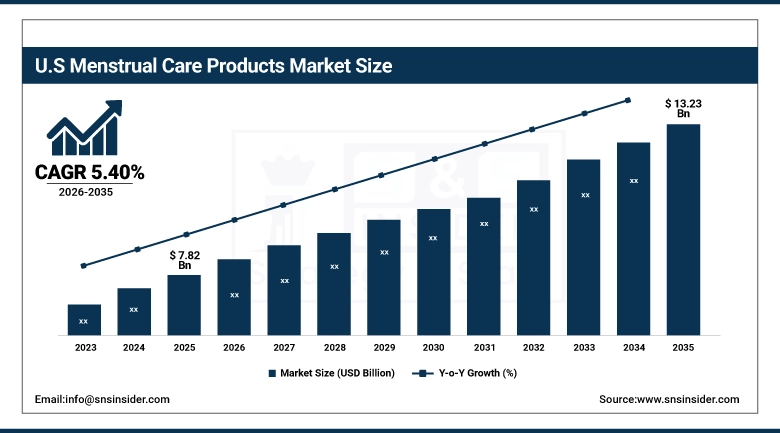

The U.S. Menstrual Care Products Market has been valued at USD 7.82 Billion in 2025 and is expected to reach USD 13.23 Billion in 2035, growing at a CAGR of 5.40% from 2026 to 2035.

Growth is driven by increasing awareness of menstrual hygiene, rising demand for organic and sustainable products, and continuous product innovation. Expanding e-commerce platforms and strong retail distribution improve accessibility. Additionally, supportive government initiatives, higher disposable incomes, and open discussions around menstrual health are encouraging product adoption, contributing to steady market expansion in the U.S.

Menstrual Care Products Market Drivers:

-

Rising Awareness of Menstrual Hygiene and Health

The growing awareness of women's menstrual hygiene and health is a major factor in the growth of the market for menstrual care products. This has been achieved through campaigns by governments, NGOs, and other organizations, which have helped in the awareness of women's safe hygienic practices and the need to use hygienic products. This has helped in changing perceptions and stigma around using such products, especially in developing countries where traditional practices were a hindrance to using modern products.

Menstrual Care Products Market Restraints:

-

Environmental Impact of Disposable Menstrual Products

Environmental issues associated with waste disposal of disposable menstrual hygiene products act as a major restraint for the market. Most of the traditional sanitary pads and tampons include plastic components, which are not biodegradable and contribute to waste disposal problems. Environmental awareness is creating a negative image of such single-use items. Improper disposal of these items is adding fuel to the fire, especially in those regions where waste disposal facilities are not available, thus creating a gradual move towards eco-friendly, biodegradable, and reusable products.

Menstrual Care Products Market Opportunities:

-

Innovation in Reusable and Organic Menstrual Solutions

The innovation in reusable or organic menstrual care products is a significant growth driver for this market. Organizations are launching products such as menstrual cups, period underwear, or cloth pads made from organic or chemical-free materials. Such products promise cost savings over a period of time, environmental benefits, as well as comfort. There have been improvements in design and material technologies to make these products more convenient to use. Additionally, there is a trend towards a sustainable lifestyle that is driving the adoption of such innovative menstrual care products.

Menstrual Care Products Market Segments:

-

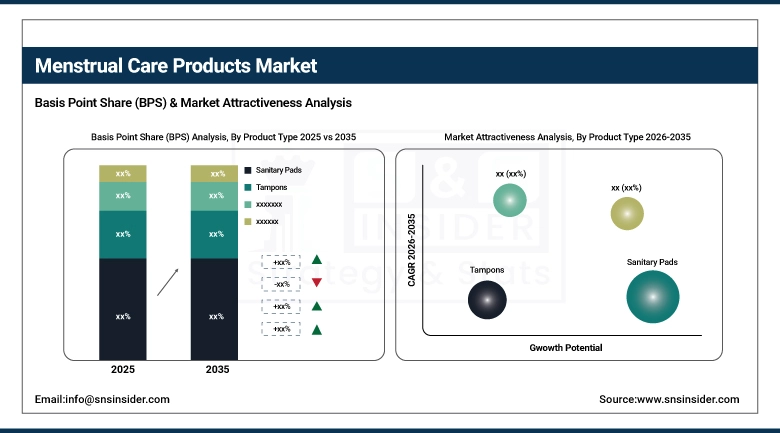

By Product Type: In 2025, Sanitary Pads dominated with 55% share; Menstrual Cups and Period Underwear fastest growing segment during 2026-2035

-

By Distribution Channel: In 2025, Supermarkets and Hypermarkets dominated with 48% share; Online Retail fastest growing segment during 2026-2035

-

By Material or Technology: In 2025, Disposable Products dominated with 70% share; Organic and Biodegradable Products fastest growing segment during 2026-2035

-

By End User: In 2025, Adults dominated with 65% share; Teenagers fastest growing segment during 2026-2035

Menstrual Care Products Market Segment Analysis:

By Product Type: Sanitary Pads Dominate, Menstrual Cups and Period Underwear Fastest-Growing

Sanitary pads hold a dominant position in the product type segment due to their accessibility, affordability, and high degree of consumer awareness. Sanitary pads are easy to use and are available across both urban and rural markets with a robust distribution network and government initiatives promoting menstrual hygiene.

Menstrual cups and period underwear are the fastest-growing product type segments, primarily because of the growing awareness of the benefits of sustainability. Consumers are increasingly opting for reusable products because of the environment and the benefits of product design, comfort, convenience, and hygiene.

By Distribution Channel: Supermarkets and Hypermarkets Dominate, Online Retail Fastest-Growing

Supermarkets and hypermarkets dominate the distribution channel segment due to their extensive product variety, strong brand visibility, and consumer preference for in-store purchases of personal care products. Discounts and promotional offers further strengthen their position.

Online retail is the fastest-growing segment, fueled by increasing internet penetration, discreet purchasing options, and the convenience of home delivery. Subscription models and direct-to-consumer brands are also accelerating growth in this channel.

By Material or Technology: Disposable Products Dominate, Organic and Biodegradable Products Fastest-Growing

Disposable products dominate the market due to their convenience, affordability, and widespread usage. Their easy availability and established consumer habits continue to drive demand globally.

Organic and biodegradable products have shown significant growth in this market, with more people becoming aware of saving the environment. There is a growing need for chemical-free products, which is prompting companies to introduce eco-friendly products to their lines.

By End User: Adults Dominate, Teenagers Fastest-Growing

Adults are the major contributors to the end-user segment, as they are the largest consumer group with a consistent pattern of consumption and higher levels of awareness about menstrual hygiene products.

Teenagers are the fastest-growing segment, with a significant increase in educational programs, early adoption of menstrual hygiene practices, and higher levels of awareness.

Menstrual Care Products Market Regional Analysis:

Asia-Pacific Menstrual Care Products Market Insights:

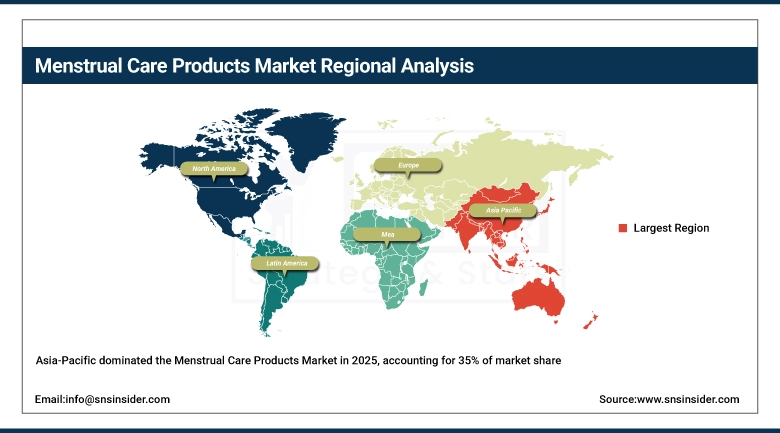

Asia-Pacific leads the menstrual care products market with a significant 35% of the total global market share in 2025. This is because the region has a huge and growing women’s population, coupled with a growing awareness of the importance of menstrual hygiene and a rise in the standard of living. The government and various non-governmental organizations’ initiatives toward the use of sanitary products are also adding to the growth of the market. The region is also witnessing rapid urbanization and an increase in the number of retail stores and e-commerce penetration.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Menstrual Care Products Market Insights:

North America region is witnessing the fastest growth in terms of menstrual care products. This growth can be attributed to the increasing demand for organic, sustainable, and premium products. In addition, increasing awareness about health, hygiene, and environmental concerns is fueling growth in this segment. The presence of key players, continuous product innovations, and availability of products are also contributing to growth in this region. Further, increasing open conversations about menstrual health are also contributing to the growth of this region.

Europe Menstrual Care Products Market Insights:

Europe has a substantial market share in the menstrual care products market owing to its high awareness of menstrual hygiene and the demand for premium products. European countries are moving towards organic, biodegradable, and reusable menstrual care products owing to stringent environmental regulations. The presence of well-established retail stores, key market players, and supportive government initiatives also contribute to the growth of the menstrual care products market in European countries.

Latin America Menstrual Care Products Market Insights:

Latin America is an emerging market for menstrual care products, with the market being driven by growing awareness of menstrual hygiene and the availability of affordable products. Factors such as growing urbanization, an increase in the number of stores selling these products, and health-related campaigns by the government are also driving the market for menstrual care products in Latin America. Despite certain challenges, growing investments in the market by both global and regional players will help the market grow steadily.

Middle East & Africa (MEA) Menstrual Care Products Market Insights:

The Middle East and Africa region is witnessing a growing market for menstrual care products due to the growing awareness of menstrual hygiene and the increased support from the government and non-government organizations. The efforts made to improve the availability of sanitary products at affordable prices are also contributing to the growth of the market. The cultural stigma is slowly disappearing in the region, and the growing retail infrastructure is also supporting the growth of the market.

Menstrual Care Products Market Competitive Landscape:

Procter & Gamble Co., headquartered in Cincinnati, Ohio, USA, is a leading global consumer goods company and a prominent player in the menstrual care products market, offering well-known brands such as Always and Whisper. The company focuses on product innovation, superior absorbency, and comfort-driven designs, along with strong global distribution and brand recognition. It emphasizes sustainability initiatives and consumer-centric solutions to strengthen its market position.

-

In March 2025: Procter & Gamble introduced eco-friendly sanitary pad variants with improved biodegradable materials, targeting environmentally conscious consumers and expanding its sustainable product portfolio.

Kimberly-Clark Corporation, headquartered in Irving, Texas, USA, is a major player in the global menstrual care products market, best known for its Kotex brand. The company specializes in feminine hygiene solutions with a focus on comfort, protection, and skin-friendly materials. It leverages strong research and development capabilities, global supply chains, and strategic marketing initiatives to maintain its competitive edge.

-

In February 2025: Kimberly-Clark launched a new line of ultra-thin, organic cotton-based sanitary products, aimed at meeting growing demand for natural and sustainable menstrual care solutions.

Menstrual Care Products Market Key Players:

-

Procter & Gamble Co.

-

Kimberly-Clark Corporation

-

Johnson & Johnson

-

Unicharm Corporation

-

Edgewell Personal Care Company

-

Hengan International Group Company Limited

-

Ontex Group NV

-

Essity AB

-

Kao Corporation

-

Unilever PLC

-

TZMO SA (Bella)

-

First Quality Enterprises, Inc.

-

Natracare LLC

-

The Honest Company, Inc.

-

Diva International Inc.

-

Saalt LLC

-

Cora (Cora Health, Inc.)

-

Lunette Menstrual Cup (Peptonic Medical AB)

-

Bodywise (UK) Limited (Natracare brand distributor)

-

Sirona Hygiene Pvt. Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.81 Billion |

| Market Size by 2035 | USD 49.28 Billion |

| CAGR | CAGR of 5.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type: (Sanitary Pads, Tampons, Menstrual Cups, Panty Liners, Period Underwear) • By Distribution Channel: (Supermarkets and Hypermarkets, Pharmacies and Drugstores, Online Retail, Convenience Stores) • By Material: (Organic and Biodegradable Products, Disposable Products, Reusable Products) • By End User: (Teenagers, Adults) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Procter & Gamble Co., Kimberly-Clark Corporation, Johnson & Johnson, Unicharm Corporation, Edgewell Personal Care Company, Hengan International Group Company Limited, Ontex Group NV, Essity AB, Kao Corporation, Unilever PLC, TZMO SA (Bella), First Quality Enterprises, Inc., Natracare LLC, The Honest Company, Inc., Diva International Inc., Saalt LLC, Cora (Cora Health, Inc.), Lunette Menstrual Cup (Peptonic Medical AB), Bodywise (UK) Limited (Natracare brand distributor), Sirona Hygiene Pvt. Ltd. |

Frequently Asked Questions

Ans: The Menstrual Care Products Market is expected to grow at a CAGR of 5.89% during 2026–2035.

Ans: The market was valued at USD 27.81 Billion in 2025 and is projected to reach USD 49.28 Billion by 2035.

Ans: The key drivers of the Menstrual Care Products Market include rising menstrual hygiene awareness, growing female population, increasing disposable income, government initiatives, product innovation, and expanding e-commerce distribution channels drive growth.

Ans: The sanitary pads segment dominated during the projected period.

Ans: Asia-Pacific dominated the Menstrual Care Products Market in 2025.

Get in Touch