Fleet Management Market Report Scope & Overview:

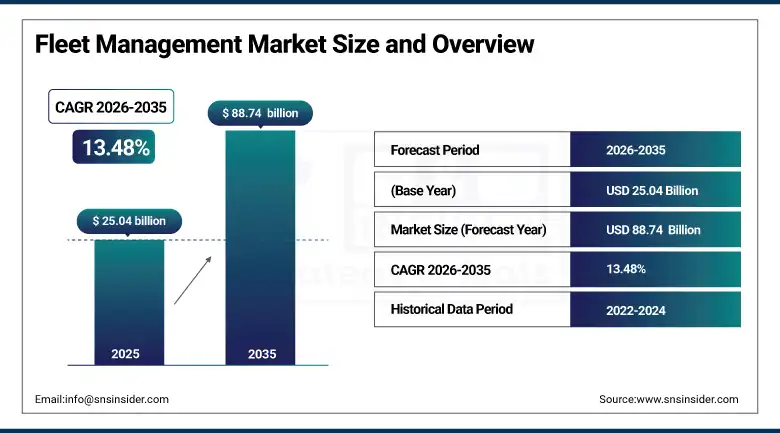

The Fleet Management Market was valued at USD 25.04 billion in 2025 and is expected to reach USD 88.74 billion by 2035, growing at a CAGR of 13.48% from 2026–2035.

Fleet management encompasses the systems, technologies, and operational processes through which organisations owning or operating vehicle fleets ranging from a small business's three-vehicle delivery vans through a logistics giant's hundred-thousand-unit truck and trailer network coordinate vehicle location tracking, driver behaviour monitoring, maintenance scheduling, and fleet asset lifecycle management in real time through integrated telematics and digital management platforms. The market encompasses the full technology and service stack supporting fleet management operations. The software platform layer of web and mobile fleet management applications that present captured data as operational dashboards, exception alerts, and management reports; the communication infrastructure connecting fleet assets to back-office systems through cellular networks, satellite communications, and dedicated short-range communications; and the professional services layer of system integration, training, and managed services that deploy and operate fleet management technology for fleet operators. The rapid adoption of electric commercial vehicles is creating new fleet management requirements around charging infrastructure integration, battery health monitoring, energy cost management, and range optimisation.

The American Transportation Research Institute's 2025 trucking cost analysis estimated that sophisticated fleet management technology deployment reduced fuel costs by 8 to 15%, maintenance costs by 10 to 25%, and accident-related costs by 15 to 30%, providing the quantified ROI evidence that is sustaining fleet management technology investment even during periods of overall trucking industry revenue pressure.

Market Size and Forecast

-

Market Size in 2026E: USD 28.41 Billion

-

Market Size by 2035: USD 88.74 Billion

-

CAGR (2026-2035): 13.48%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Fleet Management Market - Request Free Sample Report

Fleet Management Market Trends

-

AI-powered predictive maintenance analytics are enabling early component failure detection through continuous vehicle sensor data monitoring.

-

AI video telematics platforms are improving fleet safety through real-time risky driver behaviour detection and in-cab coaching alerts.

-

Electric vehicle fleet management platforms are expanding with integrated charging, range prediction, and battery monitoring capabilities.

-

Integrated fleet and supply chain visibility platforms are enabling real-time shipment tracking and customer delivery status updates.

-

Regulatory compliance mandates are accelerating investment in digital logging, tachograph, and automated driver record management systems.

The U.S. Fleet Management Market Outlook

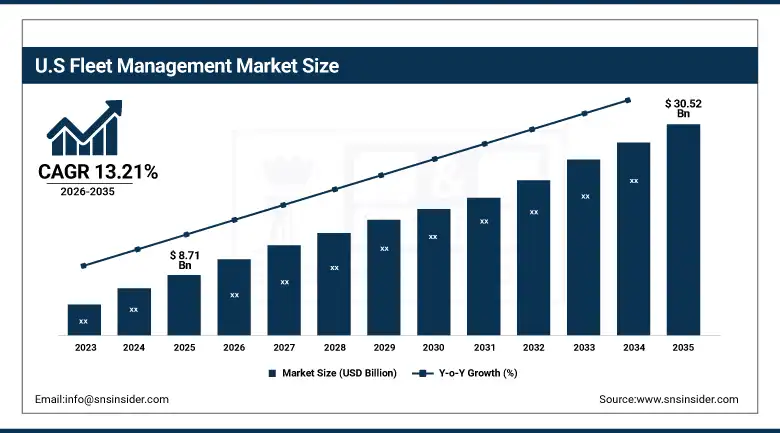

The U.S. Fleet Management Market was valued at approximately USD 8.71 billion in 2025 and is expected to reach approximately USD 30.52 billion by 2035, growing at a CAGR of 13.21%. The e-commerce delivery volume expansion driven by Amazon, Walmart, UPS, FedEx, and their last-mile delivery network partners is simultaneously expanding the commercial vehicle fleet size and intensifying the operational performance requirements on fleet management technology to support delivery density optimisation, dynamic route adjustment to actual traffic conditions, and real-time customer notification that competitive last-mile delivery requires. The U.S. Department of Transportation's Inflation Reduction Act electric vehicle commercial deployment incentives are accelerating electric commercial vehicle adoption in fleet contexts, creating the new fleet management technology requirements around charging management and battery optimisation that technology providers are investing to address.

The FMCSA's 2025 analysis confirming that commercial vehicle operators using advanced fleet telematics with predictive safety features demonstrated 22% lower reportable accident rates than comparable fleets using basic GPS tracking, creating an additional financial incentive for fleet technology investment beyond operational efficiency.

Fleet Management Market Segment Analysis

-

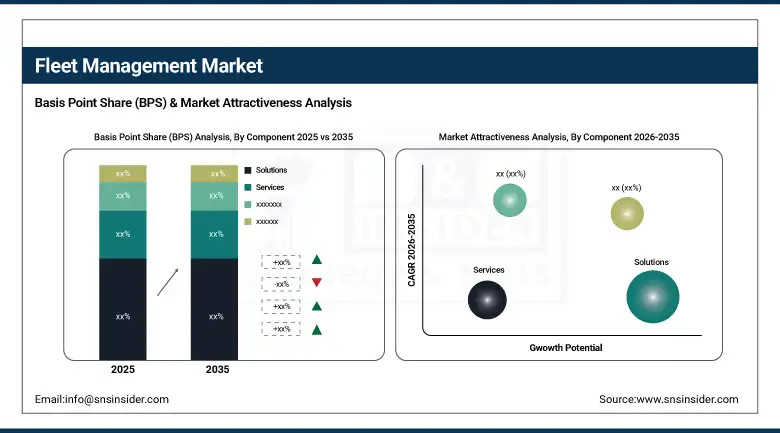

By Component, solutions dominated with approximately 65.10% of revenues in 2025; service is the fastest-growing segment at a CAGR of 15.20%.

-

By Vehicle Type, commercial vehicles held approximately 73.80% in 2025; passenger vehicles are the fastest-growing segment at a CAGR of 14.80%.

-

By Deployment Type, cloud led with approximately 63.40% in 2025 and is also the fastest-growing at a CAGR of 15.32%.

-

By Communication Technology, cellular systems led with approximately 60.20% in 2025; GNSS is the fastest-growing communication technology at a CAGR of 14.40%.

-

By Industry Vertical, transportation & logistics dominated with approximately 41.08% in 2025; oil & gas is the fastest-growing vertical at a CAGR of 14.10%.

By Component, solutions dominate, services are expected to grow fastest

Solutions retained the dominant component position with approximately 65.10% of the fleet management market in 2025, reflecting the central commercial value of integrated fleet management software platforms that transform raw telematics data into actionable operational intelligence. The leading fleet management solution platforms from Samsara, Geotab, Verizon Connect, Omnitracs (Solera), and Trimble provide comprehensive capability suites that support the full fleet management workflow from vehicle procurement through operational monitoring and end-of-life disposal, creating platform stickiness through data lock-in effects and integration complexity that sustain high customer retention rates and recurring subscription revenue.

Services are the fastest-growing component at a CAGR of 15.20% through 2035, as the growing complexity of fleet management technology ecosystems including multi-vendor telematics hardware, platform integration, electric vehicle charging management integration, and AI analytics layer implementation, and managed services that fleet operators without dedicated technology teams require to realise the full operational value of their fleet management platform investments. The managed services segment, where fleet management providers assume responsibility for monitoring fleet performance and proactively alerting fleet operators to exception conditions, is growing particularly rapidly as fleet operators increasingly prefer the outcome-focused operational oversight model over the self-service dashboards that require dedicated analyst time to monitor effectively.

By Deployment, cloud dominates and is also expected to grow fastest

Cloud deployment retained the dominant position with approximately 63.40% of fleet management market revenues in 2025 and represents the fastest-growing deployment model simultaneously, as the advantages of cloud-based fleet management platform delivery are so compelling across operational, economic, and technical dimensions that the market is experiencing a structural migration from on-premise fleet management software installations toward cloud-native SaaS alternatives. Cloud fleet management platforms eliminate the server hardware procurement and maintenance cost, provide immediate access to new features and regulatory compliance updates through software updates, enable real-time data access from any internet-connected device that field managers use for situational awareness while away from office workstations, and scale computational resources automatically to accommodate fleet size changes without infrastructure reconfiguration.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.5% |

|

Europe |

Germany |

26.8% |

|

Asia Pacific |

China |

42.4% |

|

Middle East & Africa |

Saudi Arabia |

31.3% |

|

Latin America |

Brazil |

43.9% |

North America Fleet Management Market Insights

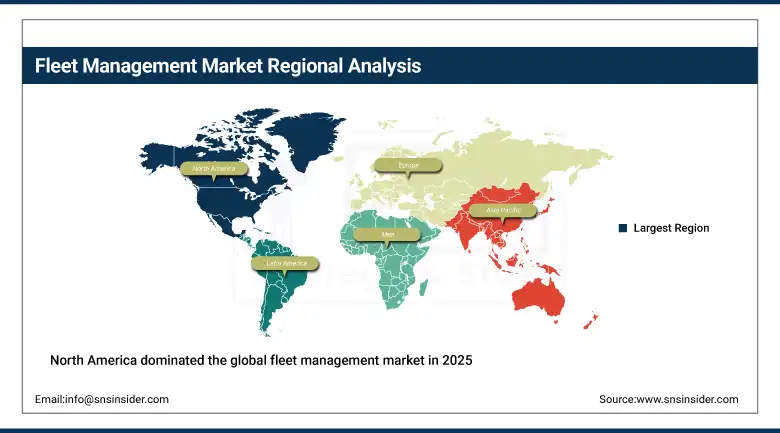

North America dominated the global fleet management market in 2025, with the United States accounting for approximately 87.5% of North American revenues as the world's largest commercial vehicle fleet market. The region's market leadership reflects the FMCSA's comprehensive electronic logging device mandate that established a regulatory baseline for fleet telematics across the commercial trucking industry, the concentration of major fleet management technology providers including Samsara, Geotab (Nasdaq-listed), Verizon Connect, and Trimble whose development investment and commercial reach sustain North American market technology leadership. Canada contributes approximately 12.5% of North American revenues through its own commercial fleet compliance requirements and a substantial resource extraction sector fleet management market in mining, oil sands, and forestry.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Fleet Management Market Insights

Europe is a large and regulation-driven fleet management market where the European Union's tachograph regulation requiring certified digital driver recording in commercial vehicles operating across EU member states, the Corporate Sustainability Reporting Directive's fleet emissions disclosure requirements, and national commercial vehicle operator licensing frameworks collectively create comprehensive regulatory compliance technology investment. Germany accounts for approximately 26.8% of European revenues through its combination of the EU's largest commercial trucking market, strong automotive and industrial fleet technology adoption.

Asia Pacific Fleet Management Market Insights

Asia Pacific is the fastest-growing fleet management market, driven by the combination of the world's largest and fastest-growing e-commerce delivery markets in China, India, and Southeast Asia due to the rapid technology adoption characteristics of Asian logistics operators who are investing in fleet management platforms as a competitive differentiator in a market where delivery speed, reliability, and customer visibility are increasingly the primary competitive battlegrounds. China accounts for approximately 42.4% of Asia Pacific revenues as the world's largest e-commerce market whose delivery fleet of hundreds of millions of vehicles is managed through fleet platforms from domestic providers including Meitrack, G7 Networks.

MEA & Latin America Fleet Management Market Insights

The Middle East and Africa and Latin America are growing fleet management markets where expanding logistics infrastructure, progressive commercial vehicle regulation implementation, and the operational efficiency imperative in industries including oil and gas, mining, and agriculture are driving fleet management technology adoption. Saudi Arabia leads MEA fleet management revenues at approximately 31.3% of regional revenues through its large government and energy sector vehicle fleets, Vision 2030 logistics infrastructure investment, and the operational efficiency requirements of ARAMCO and other major Saudi enterprise fleet operators.

Brazil leads Latin American revenues at approximately 43.9% of regional revenues through its large commercial vehicle fleet, the practical security motivation for vehicle tracking in a market where vehicle theft risk makes GPS-based stolen vehicle recovery a compelling baseline telematics investment that initiates broader fleet management platform adoption.

Market Dynamics

Growth Drivers: E-commerce delivery fleet expansion creating massive new fleet management demand

The primary growth drivers for the fleet management market are the extraordinary expansion of e-commerce delivery volumes that is simultaneously growing the commercial vehicle fleets of logistics operators and intensifying the operational performance requirements on fleet management technology to support delivery density optimisation, real-time customer communication, and driver performance management, combined with the maturation of AI-powered fleet analytics, maintenance cost avoidance, and accident cost reduction. The global shift toward electric commercial vehicles is creating a new fleet management technology investment cycle as operators transitioning to battery-electric trucks, vans, and delivery vehicles require charging infrastructure management, battery health monitoring, and range optimisation capabilities that are motivating both incumbent fleet management providers and EV-native technology startups to invest in electric fleet management platform development.

Restraints: Telematics hardware installation cost and complexity for fleet conversion, driver privacy concerns

A significant restraint on the fleet management market is the operational complexity and capital cost of retrofitting comprehensive telematics hardware across large legacy fleet vehicles that were not designed for integrated connectivity, particularly for smaller fleet operators. Driver privacy concerns represent a meaningful restraint in markets including the European Union where GDPR's restrictions on employee monitoring data collection and retention require fleet operators to implement privacy impact assessments, driver notification procedures, and data minimisation practices that add compliance cost and create potential labour relations friction in markets where driver union contracts may restrict the scope of telematics monitoring that operators can implement without negotiation.

Opportunities: Electric vehicle fleet management platform development, autonomous commercial vehicle management creating new fleet monitoring requirements

The electric commercial vehicle fleet management platform represents the most immediate and commercially significant new product development opportunity in the fleet management market, as the organisations that are implementing electric vehicle policies require purpose-built management capabilities around charging session optimisation, state of charge-aware route planning, charging network access and billing management, and battery health monitoring. Last-mile delivery route density optimisation represents a commercially compelling fleet management capability expansion opportunity, where the combination of real-time traffic data, historical delivery success rate data, parcel dimension and weight constraints, and customer delivery time preference data can generate route sequences that achieve 20 to 35% improvement in deliveries per vehicle per day compared with conventional routing approaches, directly addressing the most cost-intensive element of e-commerce logistics where last-mile delivery represents 40 to 50% of total supply chain cost.

Recent Developments:

-

2025: Samsara announced expanded AI-powered fleet safety capabilities including automatic detection of mobile phone use while driving, seatbelt compliance monitoring, drowsiness detection through eye-tracking camera analysis, and predictive risk scoring that identifies high-risk trip segments before incidents occur, expanding the fleet safety value proposition beyond reactive accident analysis.

-

2025: Geotab expanded its electric vehicle fleet management capabilities with dedicated EV dashboards incorporating charging session management, state-of-charge trend analysis, battery health tracking, and charging cost reporting for fleet operators managing mixed ICE and battery-electric vehicle deployments, positioning the platform for the accelerating commercial EV transition.

-

2025: Verizon Connect launched enhanced AI route optimisation capabilities incorporating real-time traffic, weather, and road condition data into dynamic route recalculation that reduces fuel consumption by automatically adjusting planned routes to avoid congestion, construction, and adverse weather conditions that fixed pre-planned routes cannot accommodate.

Fleet Management Market key players are:

-

Samsara Inc.

-

Geotab Inc.

-

Verizon Connect

-

Trimble Inc.

-

Omnitracs

-

Webfleet Solutions

-

Teletrac Navman

-

Motive

-

Lytx Inc.

-

Spireon

-

Azuga

-

Fleetio

-

Mix Telematics

-

Actia Group

-

Masternaut

-

Daimler FleetBoard

-

Microlise Group plc

-

Transics International

-

Trackunit A/S

-

G7 Networks

Fleet Management Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.04 billion |

| Market Size by 2035 | USD 88.74 Billion |

| CAGR | CAGR of 13.48% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Vehicle Type (Commercial Vehicles, Passenger Vehicles) • By Deployment Type (Cloud, On-Premise) • By Communication Technology (Cellular System, Satellite Communication, GNSS, DSRC, Others) • By Industry Vertical (Transportation & Logistics, Construction, Oil & Gas, Utilities, Healthcare, Government & Public Safety, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Samsara Inc., Geotab Inc., Verizon Connect, Trimble Inc., Omnitracs, Webfleet Solutions, Teletrac Navman, Motive, Lytx Inc., Spireon, Azuga, Fleetio, Mix Telematics, Actia Group, Masternaut, Daimler FleetBoard, Microlise Group plc, Transics International, Trackunit A/S, G7 Networks |

Frequently Asked Questions

North America dominated the fleet management market in 2025.

Solutions dominated with approximately 65.10% of revenues in 2025.

E-commerce delivery fleet expansion creating massive new fleet management demand.

The fleet management market was valued at USD 25.04 billion in 2025.

The fleet management market is expected to grow at a CAGR of 13.48% from 2026 to 2035.

Get in Touch