Mining Software Market Report Scope & Overview:

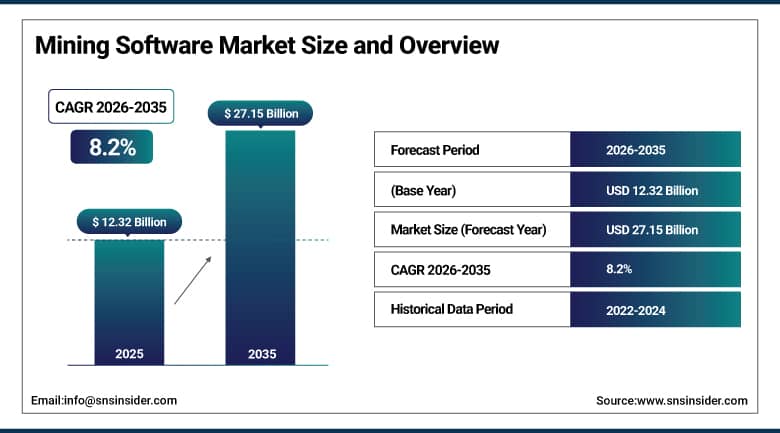

The Mining Software Market was valued at USD 12.32 Billion in 2025 and is expected to reach USD 27.15 Billion by 2035, growing at a CAGR of 8.2% from 2026–2035.

Mining Software Market Growth has been observed because of advancements in technology and the introduction of automation in the mining industry. The use of mining software makes mining processes easy and safe, and it is now necessary for mining companies to employ modern software for efficient operations while reducing costs and environmental damage. With the help of technology such as artificial intelligence and machine learning, prediction maintenance can take place and help analyze data for efficient mining. Furthermore, with the inclusion of automation and robotics in mining operations, including autonomous vehicles, safety and efficiency can be improved.

Hexagon AB, a global leader in digital reality solutions, acquired Mine Design Solutions in June 2025, integrating MDS’s expertise in mine planning and design with Hexagon’s advanced technology offerings.

Mining Software Market Size and Forecast:

-

Market Size in 2026E: USD 13.33 Billion

-

Market Size by 2035: USD 27.15 Billion

-

CAGR: 8.2% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Mining Software Market - Request Free Sample Report

Mining Software Market Trends:

-

AI and machine learning integration is enabling predictive maintenance and real-time data analytics across mining operations.

-

Automation and robotics adoption is enhancing safety through autonomous vehicles and remote monitoring systems.

-

Cloud computing is supporting collaboration through scalable data storage and remote access to critical information.

-

Environmental compliance software is strengthening through real-time emissions tracking and waste management monitoring.

-

IoT-enabled devices are collecting real-time equipment and environmental data to improve safety and productivity.

U.S. Mining Software Market Outlook:

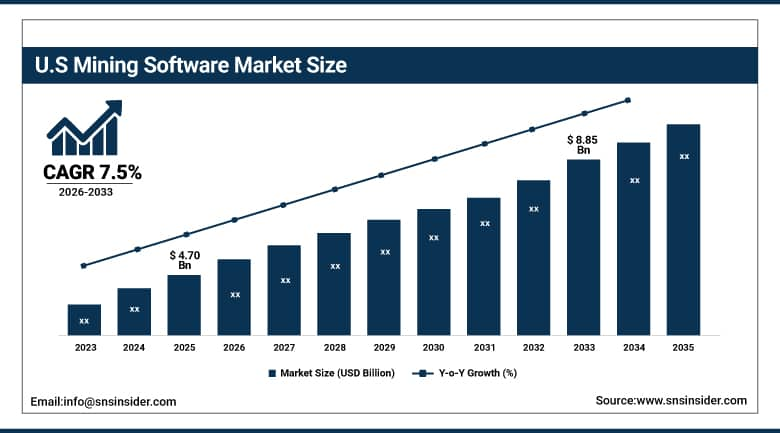

The U.S. Mining Software Market was valued at an estimated USD 4.70 Billion in 2025 and is projected to reach USD 8.85 Billion by 2033, growing at a CAGR of 7.5% from 2026 to 2033.

The U.S. Mining Software Market will experience growth because of the rising usage of digital technologies that help in better mine planning, increased efficiency, and safety for workers. With the rising need for data analytics, automation, AI, and predictive maintenance, there is an increase in the use of software for mining processes. In addition to these factors, increasing environmental regulations, increased investment in smart mining, and optimization of resources are driving growth in the market.

Advanced analytics has enabled a large North American open-pit mine to achieve 12% savings in maintenance labor, services, and spare parts costs while improving equipment availability by 5% within six months.

Mining Software Market Segment Analysis:

-

By Component, Solutions held the largest revenue share of 71.00% in 2025 driven by increasing adoption of mine planning, exploration, and fleet management tools, while Services is growing at the fastest CAGR of 9.15% through consulting and implementation demand.

-

By Mining Type, Underground mining dominated the market with a 62.00% share in 2025 through complex planning and safety monitoring needs, while Surface mining is experiencing the largest CAGR of 9.11% through expanding open-pit operations.

-

By Deployment Mode, Cloud deployment is increasingly favored for its scalable data storage and remote collaboration capabilities across distributed mine sites, while On-Premises retains importance among operators prioritizing data sovereignty for sensitive geological information.

By Component, solutions dominate, services grow fastest

Solution accounts for the highest share of revenue of 71.00% in the mining software market in 2025 due to the rising adoption of software solutions that help optimize operations, resources, and compliance. The key solutions covered under this category include mining planning software, exploration software, fleet management software, and environmental monitoring software, which are used in optimizing mining operations, with Hexagon AB rolling out the latest version of its mine planning and scheduling software, HxGN Mine Plan, which features AI analytics capabilities.

The services segment of the mining software market will witness the highest CAGR growth rate of 9.15% during the forecast period due to rising demand for services related to consulting, implementation, and after-sales support. With the adoption of mining software becoming more complicated, there is a growing need for consulting and implementation services to facilitate the adoption process, with RPMGlobal launching new service offerings for implementing mine scheduling software in 2025. In addition, Caterpillar's Mining Technology Solutions division has rolled out advanced service packages focused on training and maintenance of mining software.

By Mining Type, underground dominates, surface grows fastest

The underground mining market holds a leading position among all segments of the mining software market owing to its maximum share of 62.00% in 2025 as underground mining is considered one of the most complicated and demanding types of mineral extraction. It is important to mention that software used in the field is necessary to manage mine planning, monitoring of safety parameters, ventilation system control, as well as to trace assets, with Hexagon AB offering its solution called HxGN MinePlan providing underground mine planning along with 3D models and automated schedules, and Sandvik recently expanding functionalities of AutoMine, which manages underground mining operations and provides real-time monitoring.

The surface mining market is projected to exhibit the largest CAGR of 9.11%, owing to rising surface mining activities and an urgent need to implement innovations in the resource extraction process. Among other factors that contribute to the growth of this market segment is the necessity of utilizing software in surface mining operations to optimize planning, manage resources and haulage, and control equipment, with GeoVIA developing advanced solutions for surface mine planning and geospatial analysis, and RPMGlobal upgrading its surface mine scheduling software.

By Deployment Mode, cloud gains momentum, on-premises retains data control advantages

A cloud deployment strategy has increasingly become popular among all the mining software providers because of the ability to store and process data remotely and therefore enable better decision-making when accessing relevant data and software remotely. A cloud deployment strategy is very advantageous for mining firms that have several locations across which their operations take place as they need to have visibility into their operations and their performance wherever they operate to make the required decisions.

An on-premise deployment is important for mining companies that value having their data on-site as opposed to storing them on cloud computing platforms. Such a deployment will ensure that companies are able to plan effectively using their own hardware and do not have to worry about any internet connection issues that can affect access to critical data.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

South Africa |

31.5% |

|

Latin America |

Brazil |

43.8% |

Asia Pacific Mining Software Market Insights

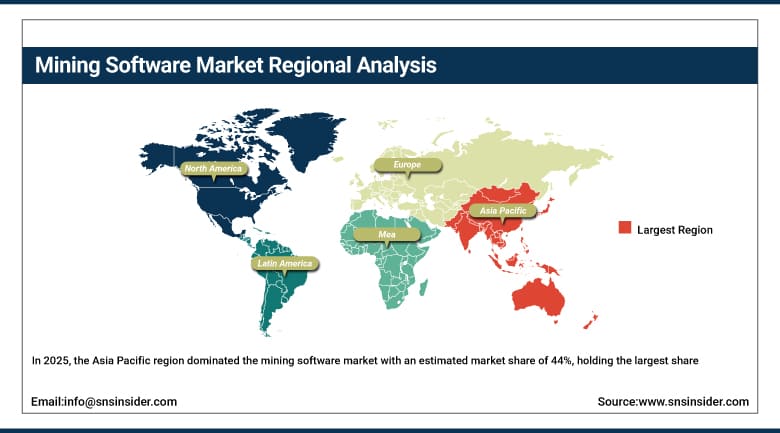

In 2025, the Asia Pacific region dominated the mining software market with an estimated market share of 44%, holding the largest share due to its robust mining industry and increasing adoption of technology to improve mining operations. The APAC region is home to some of the world’s largest mineral producers, including China, India, Australia, and Indonesia, which contribute significantly to global mining activities spanning coal, iron ore, copper, and rare earth element extraction.

The implementation of digitalization and automation in APAC’s mining industry, coupled with government initiatives to modernize mining practices, is further boosting demand for mining software solutions in this region. Australia’s advanced mining technology adoption and China’s scale of mineral extraction operations collectively anchor the region’s leading revenue position.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Mining Software Market Insights

North America is the fastest-growing region in the mining software market in 2025, with an estimated CAGR of 10.58% during the forecast period. The rapid growth can be attributed to increasing investments in technological advancements, rising demand for efficient mining practices, and the push toward sustainability in the region, with Caterpillar’s continuous innovations in autonomous mining trucks and equipment being supported by robust software solutions driving demand across both coal and metals mining segments.

The region’s strict environmental regulations are encouraging the adoption of software solutions to ensure compliance with sustainability and safety standards. The United States’ large mineral resource base alongside Canada’s established mining sector collectively sustains North America’s fastest-growing regional trajectory.

Europe Mining Software Market Insights

In 2025, Europe held a significant share of the mining software market due to its advanced mining technology adoption and strong regulatory framework. Countries such as Germany, Sweden, and Finland are focusing on modernizing mining operations and enhancing safety standards, with the increasing implementation of digital solutions, automation, and AI-driven analytics in mining operations fueling demand across both base metal and industrial mineral extraction operations.

Government support for sustainable mining practices across the region is further driving adoption of mining software solutions. Scandinavian countries’ advanced mineral processing technology and Germany’s industrial engineering expertise collectively sustain Europe’s technology-forward position in the global mining software market, with several European vendors increasingly exporting their expertise to mining operations in other regions.

MEA & Latin America Mining Software Market Insights

In 2025, the MEA region is gradually expanding its mining software market due to growing investments in mining infrastructure and modernization projects. Countries such as South Africa, Saudi Arabia, and UAE are increasingly adopting digital tools, IoT, and automation to enhance operational efficiency and safety, with rising focus on sustainability and environmental monitoring encouraging implementation of software solutions across both established and newly developed mining operations.

Latin America is witnessing steady growth in the mining software market in 2025, driven by large-scale mining operations in countries like Brazil, Chile, and Peru. The rising adoption of automation, real-time monitoring, and predictive analytics in mining operations is improving productivity and efficiency, with governments encouraging modernization of mining practices and environmental compliance.

Market Dynamics:

Growth Drivers: Automation adoption and advanced technology integration fueling sustained mining software demand

Some of the most important factors that have played a crucial role in the growth of mining software are automation and technological advancements. The introduction of automation in the form of robotic machines, sensors, and surveillance systems has enabled efficiency and has eliminated many manual operations in the process of mining. Technological advancements like artificial intelligence, machine learning, and Internet of Things have helped in predictive maintenance, resource optimization, and better decision making, with AI mining software analyzing and helping in identifying mineral rich areas for drilling and reducing downtime in both Greenfield and Brownfield mining operations.

Environmental compliance and sustainability are some of the key factors driving the growth in the mining software market. With governments across the globe taking stringent steps to reduce the adverse effects of mining on the environment, mining companies are forced to use mining software tools in order to comply with regulations, since such software helps monitor emission levels, manage waste, and other environmental factors to enable sustainability.

Restraints: High implementation and maintenance costs constraining adoption among smaller mining operators

Among the significant barriers that affect the mining software industry is the expense associated with the process of implementing and maintaining such software solutions. High-quality mining software applications often call for expensive hardware purchases, software licensing, and specialized training to be able to use such tools efficiently; however, some smaller and medium-sized businesses operating within the mining sector find themselves unable to implement these innovations because of the high cost of implementing the complete IT solution package.

Apart from the maintenance and updates required to keep the software working properly, additional expenses include integration problems with existing legacy solutions, as well as professional skills required to operate the application, making it difficult to implement new mining software among companies that experience difficulties in obtaining financing or have a lack of technological resources available.

Opportunities: AI-driven predictive analytics and sustainability compliance creating expanded mining software market categories

With advances in technology such as the combination of AI and machine learning, it is possible to undertake predictive maintenance and data analysis leading to optimal operations in the mines and therefore present great opportunities for software providers to prove themselves in terms of their ability to help the mining company achieve greater resource recovery and reduce operating costs. For mining companies, it is no longer the case where software can be seen as an elective investment in information technology because they are required to compete both in terms of their operations and regulatory compliance requirements especially since ore grades have been falling.

Concerning sustainability, which is becoming increasingly important amid attempts to curb climate change and preserve ecosystems, there is a lot of need for software within the mining industry. Since sustainability issues are increasingly gaining importance among stakeholders as well as investors, mining companies find it imperative to use technologies that provide sustainability and meet set standards, thus guaranteeing high demand for mining software.

Recent Developments:

-

2025: Hexagon AB acquired Mine Design Solutions, a Canadian mining software company specializing in mine design and planning software, integrating MDS’s engineering expertise with Hexagon’s advanced technology portfolio.

-

2025: RPMGlobal introduced new service models to support implementation of its mine scheduling software, focusing on end-to-end customer support for complex software deployment projects.

-

2023: MineSight announced a partnership with Caterpillar to integrate MineSight software with Caterpillar’s mining equipment, allowing customers to control and monitor equipment directly through the software platform.

Mining Software Market Key Players are:

-

Hitachi Ltd.

-

SAP SE

-

Microsoft Corporation

-

International Business Machines Corporation (IBM)

-

Hexagon AB

-

Komatsu Ltd.

-

Epiroc AB

-

Sandvik AB

-

RPM Global Holdings Limited

-

Trimble Inc.

-

Rockwell Automation Inc.

-

Siemens AG

-

ABB Ltd.

-

Cisco Systems Inc.

-

Accenture plc

-

Caterpillar Inc.

-

MineSight (Hexagon AB)

-

General Electric Company

-

Schneider Electric SE

-

Wenco International Mining Systems Ltd.

Mining Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.32 Billion |

| Market Size by 2035 | USD 27.15 Billion |

| CAGR | CAGR of 8.2% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Mining Type (Surface, Underground) • By Application (Exploration, Discovery/Assessment, Development, Production Operations, Reclamation/Closure) • By Deployment Mode (Cloud, On-Premises) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Hitachi Ltd., SAP SE, Microsoft Corporation, International Business Machines Corporation (IBM), Hexagon AB, Komatsu Ltd., Epiroc AB, Sandvik AB, RPM Global Holdings Limited, Trimble Inc., Rockwell Automation Inc., Siemens AG, ABB Ltd., Cisco Systems Inc., Accenture plc, Caterpillar Inc., MineSight (Hexagon AB), General Electric Company, Schneider Electric SE, and Wenco International Mining Systems Ltd. |

Frequently Asked Questions

The Mining Software Market is expected to grow at a CAGR of 8.2% from 2026 to 2035.

The Mining Software Market was valued at USD 12.32 Billion in 2025.

Increasing adoption of digital technologies, automation, and data analytics in mining operations, growing emphasis on environmental compliance and sustainability, and integration of AI and machine learning for predictive maintenance are the primary growth factors sustaining market expansion.

Solutions held the largest revenue share of 71.00% in 2025, driven by increasing adoption of mine planning, exploration, fleet management, and environmental monitoring tools, while Services is growing at the fastest CAGR.

Asia Pacific dominated the market with an estimated share of 44% in 2025 through its robust mining industry.

Get in Touch