Freestanding Emergency Department Market Report Scope & Overview:

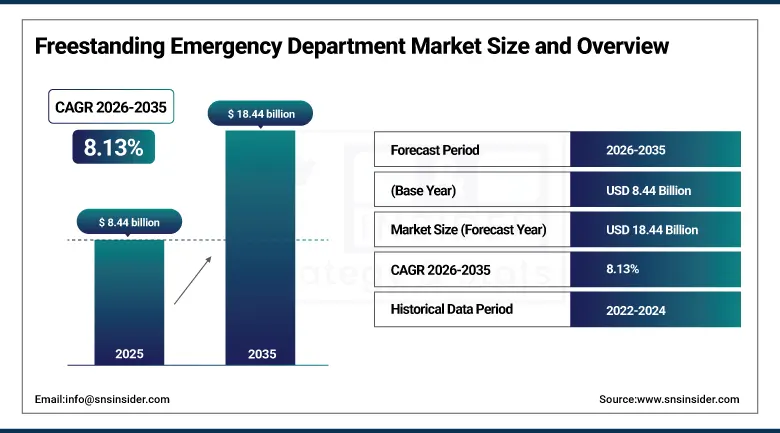

The Freestanding Emergency Department Market was valued at USD 8.44 billion in 2025 and is expected to reach USD 18.44 billion by 2035, growing at a CAGR of 8.13% from 2026–2035.

Freestanding emergency departments represent a structurally distinctive category of acute care facility that provides the full scope of emergency medical services including 24/7 physician-staffed emergency evaluation and treatment, advanced diagnostic imaging, laboratory testing, and stabilization for life-threatening conditions within a facility physically separate from an acute care hospital campus. The FED market encompasses two structurally distinct facility types whose regulatory treatment, reimbursement frameworks, and operational characteristics differ substantially: hospital-affiliated or off-campus emergency departments that operate under the license of an affiliated hospital system with access to the hospital's payer contracts, electronic health records, specialist referral networks, and transfer protocols that enable rapid escalation of patients who develop conditions requiring inpatient hospitalization; and independent or free-standing emergency departments that operate under their own license, negotiate their own payer contracts, and must establish individual referral relationships with inpatient hospital facilities for patient transfers. The hospital-affiliated model provides the operational support and commercial advantages of health system integration while enabling geographic expansion beyond the main hospital campus, while the independent model offers greater entrepreneurial flexibility and faster expansion at the cost of the integrated operational support that hospital system affiliation provides.

The American College of Emergency Physicians' 2025 emergency care access report documenting that over 65% of U.S. counties lack 24/7 emergency physician coverage and that hospital emergency department wait times in major metropolitan areas average 2.7 hours for non-critical presentations confirms the structural access gap that freestanding emergency departments are commercially positioned to address through geographically distributed facility deployment in underserved suburban and rural catchment areas.

Market Size and Forecast

-

Market Size in 2026E: USD 9.13 Billion

-

Market Size by 2035: USD 18.44 Billion

-

CAGR (2026 to 2035): 8.13%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Freestanding Emergency Department Market - Request Free Sample Report

Freestanding Emergency Department Market Trends

-

Accelerating private equity investment enables multi-site freestanding emergency department chains with standardized operations and stronger payer negotiating power.

-

Telemedicine integration in FEDs allows remote specialist consultations, improving clinical capability without requiring costly on-site specialist staffing.

-

Advanced diagnostic imaging adoption in FEDs enhances service quality through CT, MRI, ultrasound, and digital radiography expansion.

-

Rising consumer awareness positions FEDs as preferred emergency care options through digital marketing, branding, and health platform integration.

-

International expansion of FED models is growing in developed and emerging markets due to hospital overcrowding and access gaps.

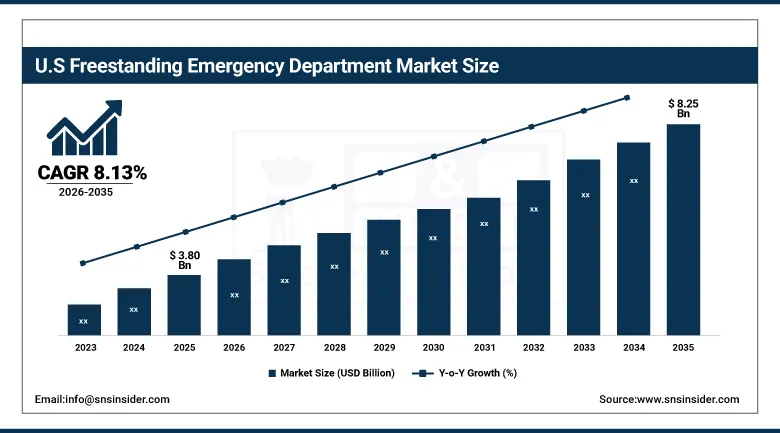

The U.S. Freestanding Emergency Department Market Outlook

The U.S. Freestanding Emergency Department Market was valued at approximately USD 3.80 billion in 2025 and is expected to reach approximately USD 8.25 billion by 2035, growing at a CAGR of 8.13%.

The United States is the birthplace of the freestanding emergency department model and commands the world's largest FED market by both facility count and revenue. The concentration of FED development in Texas, which hosts approximately 30% of all U.S. FEDs concentrated in Dallas-Fort Worth, Houston, and San Antonio metropolitan areas, reflects the state's historically permissive regulatory approach that enabled early and rapid market development, while states including Colorado, Ohio, Florida, and Arizona have developed significant FED facility networks as their regulatory frameworks have evolved to accommodate the model.

CMS's policy framework governing the reimbursement of off-campus provider-based emergency departments, which requires facilities to meet the same conditions of participation as hospital emergency departments to bill at facility fee rates rather than the lower professional fee rates applicable to urgent care centers, creates a regulatory quality standard that distinguishes FEDs providing genuine emergency care capabilities from lower-acuity urgent care operations seeking to access emergency department reimbursement rates, providing the framework that sustains FED commercial viability in Medicare and Medicaid-covered patient populations.

Freestanding Emergency Department Market Segment Analysis

-

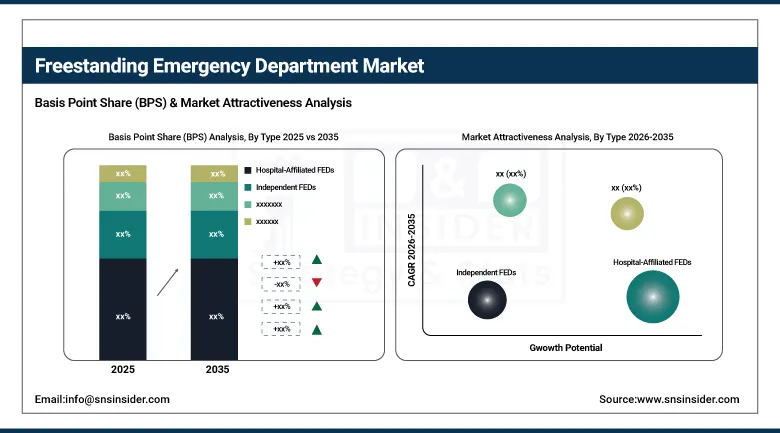

By Type, hospital-affiliated FEDs dominated with approximately 62.34% in 2025; independent FEDs are the fastest-growing at a CAGR of 9.26%.

-

By Service Type, emergency care services accounted for the largest revenue share of approximately 38.42% in 2025; diagnostic imaging services are the fastest-growing at a CAGR of 9.84%.

-

By Patient Type, adult patients dominated with approximately 71.48% in 2025; pediatric patients are the fastest-growing segment at a CAGR of 8.87%.

-

By Ownership, private dominated with approximately 68.22% in 2025; public ownership represents a smaller but growing component.

By Type, hospital-affiliated FEDs dominate, independent FEDs are expected to grow fastest

Hospital-Affiliated FEDs retained the dominant type position with approximately 62.34% of the freestanding emergency department market in 2025, reflecting the substantial operational and commercial advantages that health system affiliation confers on off-campus emergency department facilities whose payer contracting, physician credentialing, electronic health record integration, specialist consultation access, and patient transfer protocols all benefit from the hospital parent organization’s established relationships, infrastructure, and regulatory status. The hospital system perspective on FED development has shifted from the defensive stance of protecting existing hospital emergency department patient volume toward the affirmative market development recognition that off-campus FED networks can capture suburban patient populations whose geographic distance from the main hospital campus makes FED facilities their preferred emergency care access point, generating system revenue while relieving main campus emergency department congestion that compromises patient satisfaction and regulatory compliance.

Independent FEDs are the fastest-growing type at a CAGR of 9.26% through 2035, driven by the active deployment of private equity capital into physician-led and entrepreneur-operated FED chain development that is creating rapidly expanding independent FED networks in commercially attractive suburban markets where population density, insurance penetration, and median household income create the revenue per visit and patient volume economics that justify facility investment and operating cost. The private equity-backed FED operators including Integra Emergency Physicians, Elite Emergency Medical Services, and similar platforms are deploying standardized facility concepts, staffing models, and operational management systems across portfolios of independent FEDs that achieve the scale economies and brand consistency that individual facility operators cannot match.

By Service Type, emergency care services dominate, diagnostic imaging is expected to grow fastest

Emergency Care Services retained the dominant service type position with approximately 38.42% of freestanding emergency department market revenues in 2025, as the core clinical function of providing 24/7 emergency physician evaluation, stabilisation, and treatment for acute medical conditions that cannot safely await the next available primary care appointment constitutes the foundational revenue driver for every FED facility across ownership type, affiliation status, and geographic market. Emergency care services at FEDs encompass the same fundamental scope as hospital emergency departments including triage, emergency physician assessment, IV access and medication administration, vital sign monitoring, wound care, fracture management, and advanced life support stabilization, delivered in the convenient suburban locations and low-wait-time environments that differentiate the FED patient experience from hospital emergency departments.

Diagnostic Imaging Services are the fastest-growing service type at a CAGR of 9.84% through 2035, as the strategic imperative for FED operators to differentiate from urgent care competitors by demonstrating emergency medicine capability that extends beyond the basic radiology services that urgent care centers provide is driving investment in CT scanner installation, ultrasound capability enhancement, and in premium FED facilities MRI access that enables the comprehensive diagnostic workup that emergency physicians require for higher-acuity patient presentations. CT scanning capability is particularly commercially significant for FEDs because the inability to perform CT imaging forces transfer of stroke, pulmonary embolism, appendicitis, and abdominal pain presentations to hospital emergency departments whose imaging capability is required for definitive diagnosis, creating competitive disadvantage that sophisticated FED operators are resolving through CT installation investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.6% |

|

Europe |

United Kingdom |

30.4% |

|

Asia Pacific |

Australia |

34.8% |

|

Middle East & Africa |

UAE |

33.5% |

|

Latin America |

Brazil |

42.3% |

North America Freestanding Emergency Department Market Insights

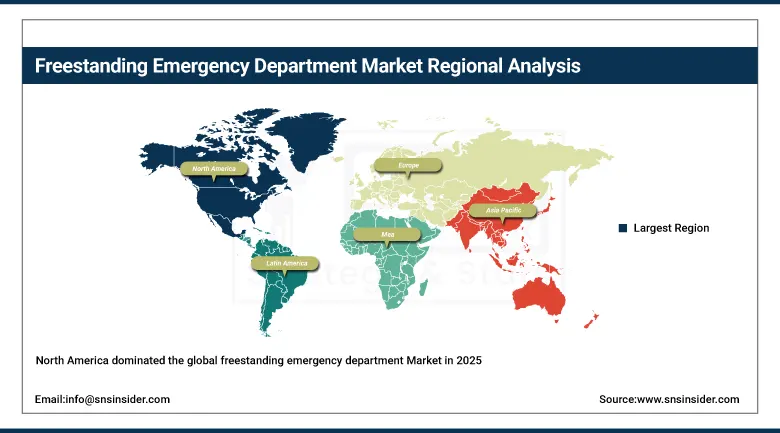

North America dominated the global freestanding emergency department Market in 2025, with the United States accounting for approximately 87.6% of North American revenues as the birthplace and most extensively developed national FED market globally. The region's dominance reflects the unique combination of the world's most commercially developed private healthcare market where the entrepreneurial opportunity for profitable FED operation has been demonstrated across hundreds of facilities, the most permissive regulatory environment for FED development among major healthcare markets where the majority of U.S. states permit FED operation without the restrictive certificate of need requirements that limit hospital capacity expansion in many states, and the most severe hospital emergency department overcrowding that creates the patient demand motivation for convenient alternative access that FED facilities satisfy.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Freestanding Emergency Department Market Insights

Europe is a developing FED market where the universal healthcare system architectures of most European countries create different structural conditions for FED development than the U.S. private healthcare market, as the NHS in England, statutory health insurance systems in Germany and France, and similar national frameworks determine how and whether FED facilities can be economically sustainable through public healthcare funding rather than private insurance reimbursement. The United Kingdom accounts for approximately 30.4% of European FED revenues as the market where NHS England's urgent treatment centre network and the development of private FED facilities in England's growing private healthcare sector most closely approximates the FED model as it exists commercially in the United States. The NHS's persistent accident and emergency department performance challenges, where the four-hour wait target has been consistently missed in recent years, are creating policy interest in distributed urgent and emergency care delivery that FED concepts could address if appropriately integrated into NHS commissioning frameworks.

Asia Pacific Freestanding Emergency Department Market Insights

Asia Pacific is the fastest-growing regional FED market, driven by rapid private healthcare investment in Australia, Singapore, India, and Southeast Asian markets where growing middle-class populations with private health insurance are creating commercial demand for convenient emergency care access outside overcrowded public hospital emergency departments. Australia accounts for approximately 34.8% of Asia Pacific FED revenues as the region's most commercially developed FED market where private hospital operators including Ramsay Health Care and Healthscope have deployed emergency department facilities at private hospital sites and in some cases standalone locations that serve the substantial privately insured Australian population seeking predictable, lower-wait emergency access. The Gulf Cooperation Council countries are emerging as a significant developing FED market through the private healthcare investment programmes of UAE, Saudi Arabia, Qatar, and Kuwait.

MEA & Latin America Freestanding Emergency Department Market Insights

The Middle East and Africa and Latin America are developing FED markets where expanding private healthcare investment, growing middle-class populations with private health insurance, and in the Middle East substantial government healthcare investment in world-class medical facilities are creating initial commercial conditions for FED development. UAE leads MEA FED revenues at approximately 33.5% of regional revenues through its concentration of premium private healthcare facilities in Dubai and Abu Dhabi, high private insurance coverage among the expatriate population that represents a significant proportion of UAE residents, and the government's healthcare infrastructure investment programme that includes emergency care access expansion in suburban areas of major Emirati cities. Brazil leads Latin American revenues at approximately 42.3% through its private healthcare sector's investment in emergency care expansion serving the substantial Brazilian private health insurance market.

Market Dynamics

Growth Drivers: Chronic hospital emergency department overcrowding creating persistent consumer demand for convenient alternative emergency access

The primary structural growth drivers for the freestanding emergency department market are the persistent and in most major developed healthcare markets worsening overcrowding of hospital emergency departments that creates the consumer demand motivation for geographically convenient, low-wait-time emergency care alternatives that freestanding emergency departments provide, combined with the availability of private equity capital for FED operator development that has capitalized the rapid expansion of independent FED chains across commercially attractive suburban markets and the strategic recognition by health systems that off-campus FED network development captures suburban patient populations, reduces main campus congestion, and improves system-wide patient satisfaction metrics that affect value-based care contract performance. The growth of high-deductible health plan adoption among commercially insured populations is creating patient sensitivity to emergency care venue choice based on out-of-pocket cost transparency and convenience that FED marketing programmes are capitalizing on through price transparency initiatives and digital booking capability.

Restraints: Reimbursement uncertainty following CMS site-neutral payment policy proposals

A significant restraint on the freestanding emergency department market is the regulatory and reimbursement uncertainty created by CMS proposals for site-neutral payment policies that would reduce hospital outpatient department and off-campus emergency department reimbursement rates toward the lower physician fee schedule levels applicable to non-hospital emergency facilities, potentially undermining the revenue per visit economics that hospital-affiliated FED financial models depend upon in markets where hospital facility fee billing sustains FED operational margins that professional fee billing alone would not support. Consumer confusion between freestanding emergency departments and urgent care centers regarding the acuity of conditions appropriately treated, the payment consequences of facility fee emergency billing versus urgent care billing, and the implications for insurance cost-sharing has created both patient dissatisfaction at unexpected bills and adverse media coverage that some state attorneys general have investigated as potentially deceptive facility naming or marketing practice.

Opportunities: Integrated virtual care and FED hybrid models combining telemedicine triage with in-person emergency visit optimization

The integration of telemedicine-based emergency triage with physical FED visit management, where patients initiate emergency care contact through a virtual platform that assesses presentation acuity and directs appropriate cases to the nearest FED with pre-registration and estimated wait time information, enables FED operators to optimize facility utilization by matching patient acuity to care setting capability and reducing inappropriate presentations that consume FED capacity while generating patient satisfaction dissatisfaction when emergency billing for conditions that could have been managed in an urgent care setting generates unexpected cost-sharing obligations.

Recent Developments:

-

2025: Several major U.S. health systems including HCA Healthcare, Ascension Health, and Common Spirit Health announced expanded off-campus emergency department development programmes targeting suburban growth corridors in high-demand metropolitan markets.

-

2025: Private equity-backed FED operators continued rapid facility count expansion in Texas, Colorado, and Ohio with several portfolio companies completing Series B and C funding rounds of USD 50 to 150 million to finance facility pipeline execution and operational infrastructure scaling.

-

2025: The American College of Emergency Physicians published updated guidance on telemedicine integration in freestanding emergency department settings, establishing clinical protocols for specialist teleconsultation in FED environments that address the most common capability limitations of community FED facilities in managing complex neurological, cardiological, and psychiatric presentations.

Freestanding Emergency Department Market key players are:

-

HCA Healthcare Inc.

-

Ascension Health

-

CommonSpirit Health

-

Tenet Healthcare Corporation

-

CHRISTUS Health

-

Integra Emergency Physicians

-

Elite Emergency Medical Services

-

Adeptus Health

-

FastMed Urgent Care

-

NextCare Holdings

-

Emerus Holdings

-

U.S. HealthWorks (Optum)

-

CareNow (HCA)

-

Concentra

-

MedStar Health

-

Baylor Scott & White Health

-

Memorial Hermann Health System

-

Texas Health Resources

-

Dignity Health (CommonSpirit)

-

Banner Health

Freestanding Emergency Department Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.44 Billion |

| Market Size by 2035 | USD 18.44 Billion |

| CAGR | CAGR of 8.13% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hospital-Affiliated FEDs, Independent FEDs) • By Service Type (Emergency Care Services, Diagnostic Imaging Services, Laboratory Services, Outpatient Services, Others) • By Patient Type (Adult Patients, Pediatric Patients) • By Ownership (Private, Public) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | HCA Healthcare Inc., Ascension Health, CommonSpirit Health, Tenet Healthcare Corporation, CHRISTUS Health, Integra Emergency Physicians, Elite Emergency Medical Services, Adeptus Health, FastMed Urgent Care, NextCare Holdings, Emerus Holdings, U.S. HealthWorks (Optum), CareNow (HCA), Concentra, MedStar Health, Baylor Scott & White Health, Memorial Hermann Health System, Texas Health Resources, Dignity Health (CommonSpirit), Banner Health |

Frequently Asked Questions

North America dominated with the FED market.

Hospital-affiliated FEDs dominated with approximately 62.34% of revenues in 2025.

Chronic hospital emergency department overcrowding creating persistent consumer demand for convenient emergency care access.

The FED Market was valued at USD 8.44 billion in 2025.

The FED Market is expected to grow at a CAGR of 8.13% from 2026 to 2035.

Get in Touch