Fumed Silica Market Report Scope & Overview

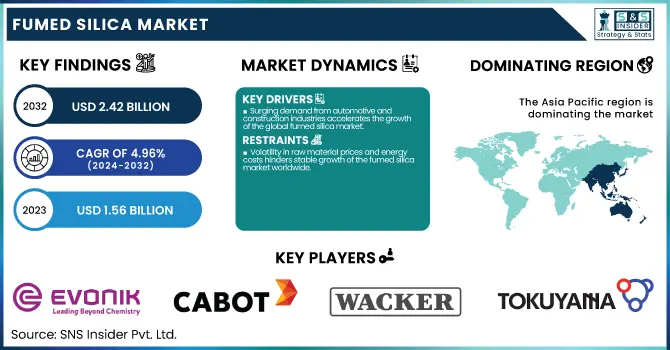

The Fumed Silica Market size was USD 1.56 billion in 2023 and is expected to reach USD 2.42 billion by 2032 and grow at a CAGR of 4.96% over the forecast period of 2024-2032.

The report offers a comprehensive analysis of production capacity and utilization rates by key producing countries and type (hydrophilic vs. hydrophobic) for 2023. It also details feedstock price trends, especially silicon tetrachloride, across major regions. The report evaluates regulatory influences, focusing on emission standards and safety regulations in North America, Europe, and Asia Pacific. Furthermore, it presents environmental performance metrics, including carbon footprint, waste handling, and circular economy initiatives. Additionally, the report highlights R&D investments and innovation pipelines, particularly in surface treatment technologies and next-gen dispersion systems.

The fumed silica market in the United States was Market size was USD 0.26 billion in 2023 and is expected to reach USD 0.43 billion by 2032 and grow at a CAGR of 5.42% over the forecast period of 2024-2032. This is due to its strong presence across high-demand end-use industries such as automotive, construction, personal care, and pharmaceuticals. The country is home to several major manufacturers and end-users that utilize fumed silica in applications ranging from adhesives and sealants to cosmetics and drug formulations. In addition, robust research and development efforts, coupled with advanced manufacturing technologies, have enabled consistent innovation and product optimization. Favorable regulatory frameworks and environmental standards have further encouraged the use of fumed silica in sustainable and energy-efficient solutions. Moreover, strong economic stability, high consumption patterns, and significant infrastructure spending continue to support market growth, while the presence of key players like Cabot Corporation and Wacker Chemie AG ensures consistent domestic supply and technological advancements.

Market Dynamics

Drivers

-

Surging demand from automotive and construction industries accelerates the growth of the global fumed silica market.

The global fumed silica market is witnessing strong growth driven by increasing demand from the automotive and construction sectors. In the automotive industry, fumed silica is widely used in adhesives, sealants, and coatings due to its thixotropic properties and ability to enhance mechanical strength. Meanwhile, the construction sector relies on fumed silica to improve rheology and workability in paints, coatings, and concrete mixtures. Growing infrastructure investments, especially in emerging economies like India and China, are further fueling product adoption. Moreover, the rise in electric vehicles and demand for high-performance materials contribute to expanded applications. With ongoing industrialization and urbanization trends, manufacturers are expanding production capacity to meet rising needs. This growing multi-sector demand solidifies fumed silica’s role as a critical additive, significantly driving market expansion across regions.

Restrain

-

Volatility in raw material prices and energy costs hinders stable growth of the fumed silica market worldwide.

The production of fumed silica heavily relies on feedstocks such as silicon tetrachloride and energy-intensive processes, making it susceptible to raw material price volatility. Any fluctuations in the prices of silica precursors, natural gas, or electricity directly impact production costs and market profitability. Additionally, global supply chain disruptions, trade restrictions, and geopolitical tensions have contributed to inconsistent supply and higher logistical costs. This has resulted in increased pricing pressure on manufacturers, especially those operating in cost-sensitive regions. For small- and medium-sized players, maintaining profit margins becomes increasingly difficult amidst these fluctuations. Furthermore, end-users in sectors like paints, adhesives, and personal care may shift to alternative or lower-cost additives if prices continue to rise. This cost sensitivity acts as a significant barrier, restraining the otherwise expanding global fumed silica market.

Opportunity

-

Expansion into high-growth sectors like pharmaceuticals and personal care presents lucrative opportunities for fumed silica producers.

The fumed silica market is poised for notable opportunities through expansion into pharmaceuticals and personal care segments. In pharmaceuticals, fumed silica is valued for its role as a glidant in tablet manufacturing and as a viscosity modifier in formulations. Its high purity, surface area, and inert nature make it ideal for drug delivery and controlled release applications. Simultaneously, the personal care industry leverages fumed silica for its thickening, anti-caking, and light-diffusing properties in cosmetics, sunscreens, and skincare products. The rise in health-conscious and beauty-conscious consumers, especially in Asia-Pacific and North America, is generating strong demand for high-quality and functional ingredients. Moreover, regulatory support for safe and non-toxic additives further strengthens this opportunity. Companies investing in product development tailored to these industries stand to benefit from substantial revenue growth in the coming years.

Challenge

-

Stringent environmental regulations and waste disposal challenges create operational complexities for fumed silica manufacturers globally.

Fumed silica production involves high-temperature processes that consume significant energy and produce emissions, drawing scrutiny under increasingly strict environmental regulations. Manufacturers face growing pressure to reduce carbon footprints, comply with emission standards, and implement sustainable production practices. In regions like the European Union and parts of North America, regulatory frameworks demand substantial investment in cleaner technologies and pollution control systems. Additionally, the proper handling and disposal of by-products such as hydrochloric acid require compliance with hazardous waste management laws, further increasing operational complexity. Companies failing to adapt may face legal penalties, production halts, or loss of market access. These compliance obligations pose a serious challenge, particularly for smaller manufacturers lacking the capital for eco-friendly upgrades. Therefore, regulatory constraints act as a critical hurdle that could slow down the momentum of market growth.

Segmentation Analysis

By Type

Hydrophilic dominated the market in terms of the largest share, around 64%, in 2023. due to its high versatility, coupled with high penetration in paints & coatings, adhesives & sealants, silicone elastomers, and personal care. Due to its unique properties of outstanding thickening, anti-settling, and reinforcement functions, it could be used to improve the performance of different types of products. Moreover, the production of hydrophilic grades is easier than for the hydrophobic types, which in turn reduces their manufacturing cost and increases their availability. As a result, this has made hydrophilic fumed silica an option of choice for price-sensitive markets and high-volume applications. Furthermore, its ease of compatibility with water-based systems corresponds with the growing need for environmentally friendly and sustainable products in areas like paint, cosmetics, and pharmaceutical applications. The unique combination of performance, cost-effectiveness, and sustainability lies at the heart of its leading position in the market.

By Application

The silicone elastomers segment held the largest market share at around 32% in 2023. It is driven by the silicone elastomers, as fumed silica is a vital reinforcing agent that greatly improves the mechanical, thermal, and rheological properties of silicone compounds. Due to their high thermal stability, durability, chemical resistance, and flexibility, these elastomers find usage across the automotive, electronics, healthcare, and construction industries. This virtual example is even more relevant in electric vehicles and consumer electronics paired with increasing demand for lightweight, high-performance materials, which has enlivened functional fumed silica adoption in silicone elastomers. Besides this, silicone elastomers are used in tubing, seals, and implants in the medical and healthcare industries, where fumed silica guarantees dimensional stability and processability.

By End-Use Industry

Building & Construction held the largest market share, around 25%, in 2023. This is due to the use of fumed silica in cement, adhesives, sealants, and coatings. Our fumed silica in construction can enhance mechanical strength, rheology, and durability, thus making it an ideal additive in high-performance formulations. It improves water repellency, anti-settling property, and thermal insulation, which are essential needs in contemporary infrastructure. Rapid urbanization, recently executing large-scale commercial and residential projects, and a growing investment in green building initiatives around the world, the primary driving force behind high-performance additives such as fumed silica, have increased in numbers recently. Besides, the growing government support for green and energy-efficient buildings has intensified the utilization of fumed silica-based materials, which, in turn, has helped the construction sector maintain its leading position in this market.

Regional Analysis

Asia Pacific held the largest market share, around 44%, in 2023. This is due to rapid industrial development, a booming construction sector, and high demand of end-user industries like electronics, automotive, and personal care. Fumed silica is driven in the APAC region by infrastructure development, higher urbanization, and a boost in manufacturing. The APAC fumed silica market is expected to witness high growth in countries such as China, India, Japan, and South Korea. China is a leading consumer and producer owing to its large base of chemical manufacturing and the expanding requirement of silicone elastomers, adhesives, and coatings, as well as pharmaceutical application. Moreover, supportive government regulations, rising foreign direct investment, and the availability of low-value raw materials and a large workforce pushed large companies to increase factory capacities in the region. Together, these factors promote the dominance of Asia Pacific in the global fumed silica market.

North America held a significant market share. It is due to the established industrial base coupled with the presence of key market players and demand from pharmaceuticals, construction, automotive, and personal care industries. The U.S., in particular, has driven higher consumption of fumed silica in silicone rubber and sealants used in construction and infrastructure projects. In addition to this, the region benefits from stringent R&D capabilities, formulation technology for products, and the environmentally friendly manufacturing environment that gives rise to specialty additive fumed silica. In addition, the emergence of strategic agreements and expansions in capacity by companies like Cabot Corporation and Dow Inc. has equally contributed to the regional market. Market Growth: Apart from this, the growing demand for lightweight materials and the booming high-performance coatings markets in North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Evonik Industries AG (AEROSIL 200, AEROSIL R 812)

-

Cabot Corporation (CAB-O-SIL M-5, CAB-O-SIL TS-720)

-

Wacker Chemie AG (HDK N20, HDK H15)

-

Tokuyama Corporation (REOLOSIL QS-102, REOLOSIL EP-10)

-

OCI Company Ltd. (OCI Fumed Silica, OCI Silica R820)

-

PPG Industries, Inc. (PPG Hi-Sil SBG, PPG Hi-Sil 243LD)

-

Henan Xunyu Chemical Co., Ltd. (XYSIL 200, XYSIL R972)

-

Shanghai Almatis Co., Ltd. (ALMASIL 200, ALMASIL R972)

-

Kemitura A/S (KEMISIL KS150, KEMISIL RS260)

-

Wynca Group (Wynca Silica H200, Wynca Silica R820)

-

Orisil (ORISIL 300, ORISIL R812)

-

Zhejiang Fushite Group (FST-200, FST-R972)

-

Yichang CSG Polysilicon Co., Ltd. (CSG-Silica 200, CSG-Silica R820)

-

Gelest Inc. (Gelest Fumed Silica 150, Gelest Silica R812)

-

Dongyue Group (Dongyue Silica 150, Dongyue Silica R972)

-

NovaCentrix (NanoFumed Silica 100, NanoFumed Silica R812)

-

Imerys (IMERYS Silica 200, IMERYS Silica R972)

-

Zhejiang Runhe Chemical New Material Co., Ltd. (RUNHE Silica 200, RUNHE Silica R972)

-

SupSil Materials (SupSil 150, SupSil R200)

-

Applied Material Solutions, Inc. (AMSIL 200, AMSIL R972)

Recent Development:

-

In June 2024: Evonik Industries AG launched a new production facility at its Rheinfelden site dedicated to AEROSIL Easy-to-Disperse (E2D) fumed silica. This development streamlines the dispersion process in paints and coatings, boosting both application efficiency and environmental sustainability.

-

In 2024, Cabot Corporation unveiled plans to establish a new fumed silica manufacturing facility in Carrollton, Kentucky, through a strategic partnership with Dow Corning. The initiative is designed to expand Cabot’s footprint in North America and address the increasing demand for premium-grade fumed silica.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.56 Billion |

| Market Size by 2032 | USD2.42 Billion |

| CAGR | CAGR of4.96% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hydrophilic, Hydrophobic), • By Application (Silicone Elastomers, Paints, Coatings & Inks, Adhesives & Sealants, UPR & Composites, Others) • By End Use Industry (Building & Construction, Electrical & Electronics, Automotive & Transportation, Personal Care & Beauty, Food & Beverages, Pharmaceuticals, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Evonik Industries AG, Cabot Corporation, Wacker Chemie AG, Tokuyama Corporation, OCI Company Ltd., PPG Industries, Inc., Henan Xunyu Chemical Co., Ltd., Shanghai Almatis Co., Ltd., Kemitura A/S, Wynca Group, Orisil, Zhejiang Fushite Group, Yichang CSG Polysilicon Co., Ltd., Gelest Inc., Dongyue Group, NovaCentrix, Imerys, Zhejiang Runhe Chemical New Material Co., Ltd., SupSil Materials, Applied Material Solutions, Inc. |

Frequently Asked Questions

Ans: Asia Pacific led the Fumed Silica Market in the region with the highest revenue share in 2023.

Ans: Surging demand from automotive and construction industries accelerates the growth of the global fumed silica market.

Ans: Hydrophilic will grow rapidly in the Fumed Silica Market from 2024 to 2032.

Ans: The expected CAGR of the global Fumed Silica Market during the forecast period is 4.96%

Ans: The Fumed Silica Market was valued at USD 1.56 Billion in 2023.

Get in Touch