Functional Beverages Market Report Scope & Overview:

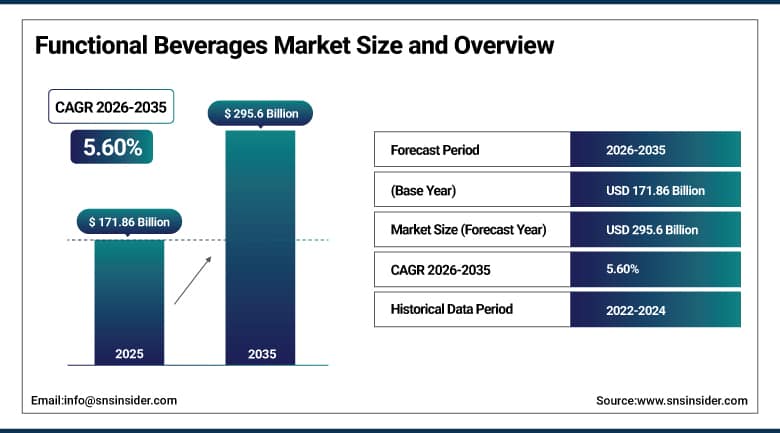

The Functional Beverages Market was valued at USD 171.86 Billion in 2025 and is expected to reach USD 295.6 Billion by 2035, growing at a CAGR of 5.60% from 2026–2035.

Functional drinks are those which have components such as vitamins, minerals, amino acids, herbs, or any other nutrients added to the drinks. Total consumption of functional beverages in 2025 was 12.5 billion liters, driven by greater awareness regarding health and a more active lifestyle, with an emphasis on wellness products in ready-to-drink format. The reasons for buying such drinks are not limited to just staying hydrated or energetic anymore. One of the most rapidly rising reasons is improving gut health by consuming probiotic and prebiotic beverages. Adaptogenic stress relief beverages are becoming increasingly popular among urban consumers in their working years. Beverage ingredient innovations are being pursued not only by existing energy drink makers such as Coca-Cola and PepsiCo but also by firms such as Monster Beverage. Independent manufacturers have managed to make a mark among large firms in probiotics, adaptogens, and clean energy markets.

The functional beverages market was valued at 12.5 billion liters by 2025. Over 70% of the new products introduced in this segment had health claims that either referred to energy, digestive health, immune system, or brain health, thus underscoring how vast the opportunities in the functional beverages market had become.

Market Size and Forecast

-

Market Size in 2026E: USD 181.48 Billion

-

Market Size by 2035: USD 295.6 Billion

-

CAGR: 5.60% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Functional Beverages Market - Request Free Sample Report

Functional Beverages Market Trends

-

Product introductions for beverages with probiotic and prebiotic benefits are increasing in dairy, kombucha, and ready-to-drink teas as consumers become more aware of their gut health and its link with immune and psychological wellness.

-

Health-focused consumers prefer clean-label energy drinks free of synthetic colorings, artificial sweeteners, or caffeine overload in favor of natural energy drinks that provide longer-lasting energy benefits than traditional energy drinks.

-

The launch of Simply Pop by Coca-Cola in February 2025 marked the entry of the largest beverage producer into the prebiotic soda segment, indicating that for this corporation, functional drinks constitute an integral part of their growth strategy, not merely an accessory line to their products.

-

The online shopping model coupled with a direct-to-consumer subscription system is allowing functional drinks brands to cultivate consumer loyalty without being restricted by traditional brick-and-mortar grocers.

-

Adaptogen-infused functional beverages incorporating ashwagandha, reishi mushroom, and lion's mane are moving from specialist health food stores into mainstream grocery channels as consumer familiarity with these ingredients grows through social media and wellness content.

The U.S. Functional Beverages Market Outlook

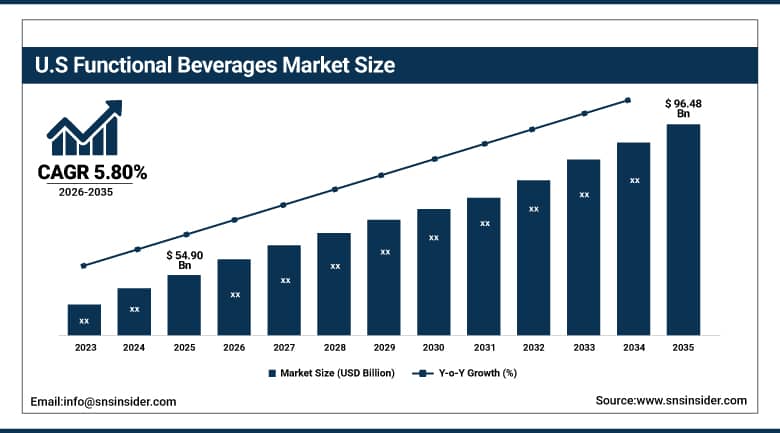

The U.S. Functional Beverages Market was valued at approximately USD 54.90 Billion in 2025 and is expected to reach approximately USD 96.48 Billion by 2035, growing at a CAGR of 5.80%.

The United States is the world's most commercially advanced functional beverages market. Its scale and innovation intensity reflect the country's strong fitness and wellness culture, high consumer spending on health products, and the concentration of major functional beverage brands. Companies like Monster Beverage, Red Bull, Celsius, Liquid I.V., Olipop, and Poppi, among many others, cater to consumers with above-average propensity to pay for beverages positioning themselves as healthy drinks. Clarification provided in the FDA guidance issued in 2024 with regard to the use of structure/function health claims on packages of products featuring health claims on probiotics and prebiotics in beverages was beneficial for manufacturers. The American market is undergoing a transition in terms of formulation approach toward natural functional beverages. It has already been proven by the prebiotic soda segment, comprising drinks offered by Olipop and Poppi, that consumers are ready to pay a premium for functional carbonated beverages.

The FDA's 2024 guidance on probiotic and prebiotic health claims for beverages provided clearer labelling pathways for functional drink brands. This regulatory clarity is expected to accelerate category investment and consumer confidence in clinically supported functional beverage health claims through the forecast period.

Functional Beverages Market Segment Analysis

-

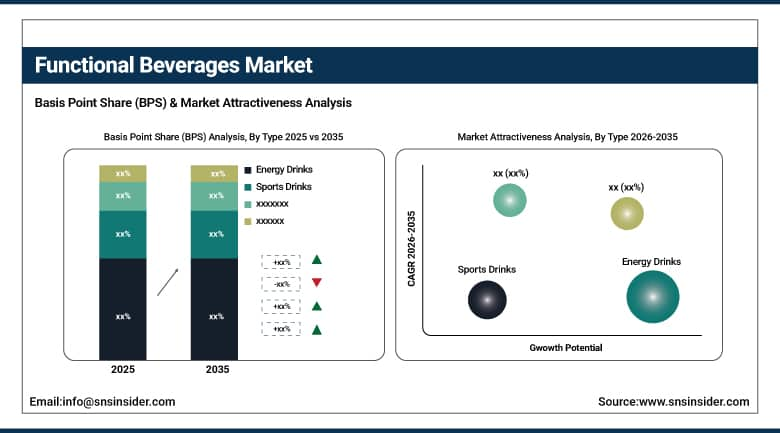

By Type, energy drinks held the largest share of approximately 39.56% in 2025 through their dominant retail presence and strong brand investment; nutraceutical and probiotic drinks are the fastest-growing type as gut health and immunity functional benefits drive new product development.

-

By Distribution Channel, supermarkets and hypermarkets held approximately 50.12% share in 2025 as the primary retail channel for mainstream energy, sports, and fortified beverage brands; online retail is the fastest-growing channel at a CAGR of 10.22% through direct-to-consumer platforms and subscription beverage models.

-

By Packaging, bottles held the largest share of approximately 37.05% in 2025 through their reusability and suitability for premium functional beverage positioning; cans are growing rapidly through the RTD cocktail adjacency and the energy drink category's dominant can format preference.

By Type, energy drinks dominate, nutraceutical and probiotic drinks grow fastest

Energy drinks held approximately 39.56% of the functional beverages market in 2025. The strength of domination rests on years of marketing efforts made by Red Bull, Monster, and Rockstar, as well as the wide distribution of their products all around the globe within the relevant sales channels. Energy drinks cater to one of the most primal consumer motivations, which is to receive an instant boost of energy. The consumer understands both the category of consumption and the reasons for purchasing energy drinks, and he is not overly price sensitive in the main mass market segment. In addition, innovation and product evolution in terms of developing sugar-free, natural energy, and flavored energy drinks prevents consumer switching from the category.

Nutraceutical and probiotic drinks are the fastest-growing type in the functional beverages market. Consumer awareness of the gut-brain connection is making digestive health a mainstream purchase motivation rather than a specialist health-food-store niche. Kombucha, kefir-based drinks, prebiotic sodas, and probiotic-fortified RTD teas are all growing their retail space across mainstream supermarkets. The prebiotic soda segment alone has demonstrated extraordinary commercial velocity. Brands including Olipop and Poppi have generated hundreds of millions in retail sales within a few years. Their success has attracted major corporate interest. PepsiCo acquired Poppi in 2025, validating the commercial scale of the probiotic beverage opportunity at the highest levels of industry investment.

By Distribution Channel, supermarkets and hypermarkets dominate, online retail grows fastest

Supermarkets and hypermarkets accounted for around 50.12% of revenue from the channel in 2025. The power of the channel is due to the importance that grocery retailing has in terms of the introduction and consumption of functional beverages. Shoppers are introduced to the brands of functional beverages alongside energy drinks available on supermarket shelves. In addition, the buyers within the supermarkets have been allocating an increasing share of space to functional beverages in several aisles including the sports nutrition aisle, the beverages aisle, and the natural and organic foods aisle.

Online retail is the fastest-growing distribution channel at a CAGR of 10.22% through 2035. Direct-to-consumer platforms allow functional beverage brands to communicate their health benefit stories with the depth and clinical detail that shelf packaging cannot accommodate. Subscription purchase models create predictable recurring revenue and improve customer lifetime value substantially above single-transaction retail economics. E-commerce enables brands to reach consumers in geographic markets where local retail distribution is unavailable. Premium and niche functional beverage brands have built commercially significant businesses entirely or primarily through online channels, demonstrating that retail distribution is no longer a prerequisite for category success.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.3% |

|

Europe |

Germany |

24.3% |

|

Asia Pacific |

China |

44.2% |

|

Middle East & Africa |

UAE |

28.4% |

|

Latin America |

Brazil |

43.6% |

North America Functional Beverages Market Insights

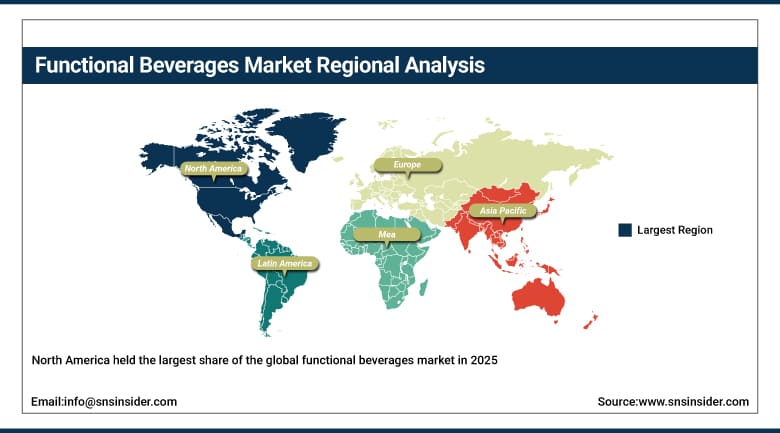

North America held the largest share of the global functional beverages market in 2025. The United States accounts for approximately 84.3% of North American revenues as the world's most commercially developed functional beverage market. The U.S. is home to Red Bull North America, Monster Beverage, Celsius Holdings, Olipop, Poppi, Liquid I.V., and hundreds of challengers brand whose combined investment in product development and marketing sustains the highest category innovation intensity globally. The U.S. regulatory framework, with FDA's increasingly clear structure/function health claim guidance, is creating commercial certainty for manufacturers investing in scientifically substantiated functional beverage formulations. Canada is a growing functional beverage market with particularly strong natural and organic category preferences among health-conscious urban consumers. Canadian retailers have expanded functional beverage assortments in response to consumer demand. The Canadian market shows strong adoption of probiotic and adaptogen beverages among younger demographic groups.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Functional Beverages Market Insights

Europe is a large functional beverages market characterized by strong consumer health awareness and progressive regulatory frameworks for health claim substantiation. Germany accounts for approximately 24.3% of European revenues as the EU's largest national consumer market with a long tradition of health-conscious food and beverage purchasing. European consumers show above-average preference for natural and clean-label functional formulations. EU health claim regulations under Regulation 1924/2006 require scientific substantiation before health claims can be used on packaging, creating a quality bar that favor s brands with genuine functional ingredient evidence over those relying on marketing-led health positioning without clinical backing.

The UK, France, Sweden, and the Netherlands each represent significant and growing national functional beverage markets. Sports drinks have strong European adoption across fitness culture demographics. Energy drinks are growing in Southern and Eastern European markets where younger consumer populations are driving above-average category growth. Probiotic dairy-based functional beverages have strong European heritage through brands like Danone's Actimel and Yakult's European operations, providing a consumer familiarity base that is being leveraged by newer non-dairy probiotic beverage entrants.

Asia Pacific Functional Beverages Market Insights

Asia Pacific is the fastest-growing regional functional beverages market. China accounts for approximately 44.2% of Asia Pacific revenues through its extraordinary consumer scale and the rapidly growing health beverage purchasing among its urban middle-class population. Japan has a deep functional beverage culture through brands like Yakult and Pocari Sweat whose decades-long market presence has established functional hydration and probiotic drinks as everyday consumption habits rather than premium health products. India is a high-growth market where rising disposable incomes and growing health consciousness are expanding the addressable functional beverage consumer base rapidly.

MEA & Latin America Functional Beverages Market Insights

The Middle East, Africa, and Latin America are growing functional beverage markets where rising urban incomes and health awareness are expanding the consumer base. UAE is the biggest revenue contributor in MEA due to its healthy expatriate community and superior retail infrastructure and holds about 28.4% of regional market share. Energy drinks consumption is common in GCC nations among young adults. The largest revenue generator in Latin America is Brazil due to its sizable urban population and dynamic local functional beverages industry and generates around 43.6% of Latin American market share. Sports drink category is well-established in Brazil whereas probiotics and natural energy drinks have emerged recently.

Market Dynamics

Growth Drivers: The growing demand for convenient wellness solutions and product innovation in gut health.

Consumer health awareness is translating directly into functional beverage purchasing. Consumers who were once purchasing regular sodas are switching to probiotic sodas, energy drinks that are environmentally friendly, and water fortified with vitamins, which can be used for targeted health purposes. Such a switch is structural in nature rather than cyclical. The move is caused by demographics as new consumers who have grown up with the knowledge of functional supplements reach the period when they earn and spend the most money. The sector enjoys robust secular tailwinds such as chronic disease awareness, sports and fitness participation, and personalized nutrition acceptance.

Product innovation is bringing about new consumption occasions and increasing the overall addressable market for the category. The launch of sleep and relaxation beverages brings about a consumption occasion that cannot be met by energy drinks. Functional coffee and matcha-based beverages are attracting coffee drinkers who want combined caffeine and adaptogen benefits. Beauty-from-within beverages incorporating collagen and hyaluronic acid are creating a new overlap between the functional beverage and personal care categories that has no clear precedent in mainstream grocery retail.

Restraints: High sugar content concerns, regulatory complexity around health claims, and intense price competition.

Sugar content continues to be the most commercially pertinent issue confronting the energy drink category. Public awareness campaigns concerning the dangers of sugary drinks have made consumers averse to products that have a higher sugar content than necessary. In the UK, the Soft Drinks Industry Levy has even directly targeted energy drinks that surpass the threshold of permissible sugar content in an effort to force reformulations. Discussions about introducing similar taxes are under way across Europe, Asia, and Latin America. Reformulation using natural sugars is costly, yet replicating taste has proven difficult.

Uneven regulatory standards pertaining to health claims lead to uneven competitive conditions among markets. While health claims are subjected to a stringent pre-approval requirement under EU regulation, many formulations using functional ingredients lack the wording of claims that motivates consumers to buy them due to the pre-approval process. On the other hand, the structure/function claim standard set forth in the U.S. allows more freedom, but it exposes the company to potential legal action in case the claim is not sufficiently substantiated.

Opportunities: GLP-1 companion beverage development and functional hydration for ageing populations represent the strongest growth opportunities.

GLP-1 weight management medication adoption is creating a new functional beverage opportunity. Patients on these medications need high-protein, nutrient-dense, lower-calorie beverages that support nutritional adequacy within reduced eating volumes. No established functional beverage brand has yet built a dominant position specifically formulated for GLP-1 patient nutritional needs. The patient population is growing rapidly and represents a high-income, health-motivated consumer segment willing to pay premium prices for products that support their treatment outcomes.

Ageing population demographics are creating new functional beverage demand in developed markets. Older consumers are increasing their spending on joint health, cognitive function, bone density, and cardiovascular wellness products. Functional beverages positioned for healthy ageing represent a less competitive segment than the crowded energy and sports drink categories. Brands that develop credible, well-formulated products for this demographic with appropriate clinical evidence and accessible retail positioning are entering a large and growing market with limited specialist competition currently.

Recent Developments:

-

2025: Coca-Cola launched Simply Pop, a prebiotic soda line under its Simply juice brand, entering the fast-growing prebiotic beverage segment and signaling major corporate validation of the functional carbonated beverage opportunity.

-

2025: PepsiCo acquired Poppi, one of the leading U.S. prebiotic soda brands, for approximately USD 1.65 billion, establishing PepsiCo as a significant player in the functional carbonated beverage market alongside its existing Gatorade and Rockstar portfolios.

-

2025: Celsius Holdings expanded its international distribution across European markets, reporting continued strong revenue growth driven by demand for its clean energy platform among fitness-oriented consumers.

-

2025: Danone expanded its probiotic beverage portfolio in Asia Pacific markets with new Activia drinkable yogurt varieties targeted at gut health-conscious urban consumers in China and Southeast Asia.

-

2025: Red Bull introduced a new Organics by Red Bull line extension incorporating botanical ingredients and reduced caffeine content, targeting health-conscious consumers who value the Red Bull brand but prefer cleaner formulation profiles.

Functional Beverages Market key players are:

-

The Coca-Cola Company

-

PepsiCo Inc.

-

Monster Beverage Corporation

-

Red Bull GmbH

-

Celsius Holdings Inc.

-

Danone SA

-

Nestlé SA

-

Keurig Dr Pepper Inc.

-

Yakult Honsha Co. Ltd.

-

Abbott Laboratories

-

GNC Holdings LLC

-

Clif Bar & Company

-

Liquid I.V.

-

Olipop PBC

-

Poppi

-

Athletic Brewing Company

-

Laird Superfood

-

Rebbl Inc.

-

Harmless Harvest

-

Califia Farms LLC

Funtional Beverages Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 171.86 Million |

| Market Size by 2035 | USD 295.6 Million |

| CAGR | CAGR of 5.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Energy Drinks, Sports Drinks, Nutraceutical & Probiotic Drinks, Dairy-Based Beverages, Others) • By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Specialty Stores, Others) • By Packaging (Bottle, Can, Tetra Pack, Sachet, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | The Coca-Cola Company, PepsiCo Inc., Monster Beverage Corporation, Red Bull GmbH, Celsius Holdings Inc., Danone SA, Nestlé SA, Keurig Dr Pepper Inc., Yakult Honsha Co. Ltd., Abbott Laboratories, GNC Holdings LLC, Clif Bar & Company, Liquid I.V., Olipop PBC, Poppi, Athletic Brewing Company, Laird Superfood, Rebbl Inc., Harmless Harvest, Califia Farms LLC |

Frequently Asked Questions

North America dominated the functional beverages market in 2025.

Energy Drinks dominated with approximately 39.56% of revenues in 2025.

Rising health consciousness and growing demand for convenient wellness solutions are the primary drivers.

The functional beverages market was valued at USD 171.86 Billion in 2025.

The functional beverages market is expected to grow at a CAGR of 5.60% from 2026 to 2035.

Get in Touch