Gaming PC Market Report Scope & Overview:

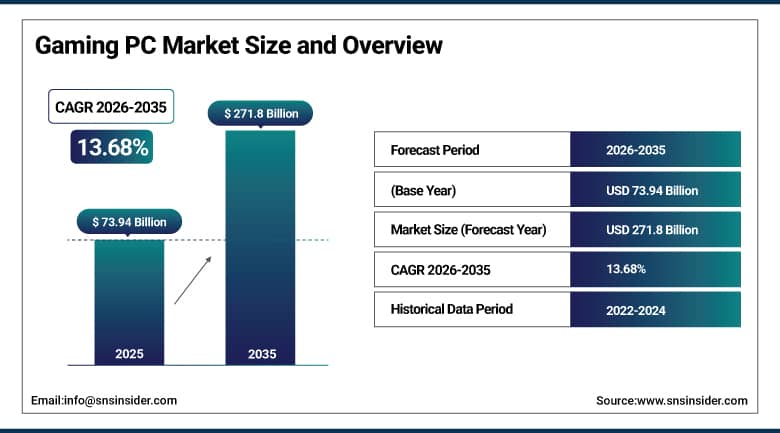

Gaming PC Market was valued at USD 73.94 billion in 2025 and is expected to reach USD 271.8 billion by 2035, growing at a CAGR of 13.68% from 2026-2035.

Gaming PC Market growth is influenced by factors like increased global adoption of games, the growing trend in the world of esports, and the demand for high-performance computers. The development of better graphics processing units, central processing units, and cooling systems is resulting in increased gaming experience and performance. Streaming platforms and competitive games are playing their role too in meeting demand for more powerful computers. Increasing disposable income and desire for better gaming experience also help in boosting demand for gaming computers.

Jon Peddie Research estimates global gaming PC and monitor revenues reached USD 45 billion in 2023. NVIDIA's GeForce GPU division reports that the installed base of gaming PCs exceeds 200 million units globally, with an average upgrade cycle of 3-4 years creating a consistent replacement demand stream independent of new user growth.

Gaming PC Market Size and Forecast

-

Market Size in 2025: USD 73.94 Billion

-

Market Size by 2035: USD 271.8 Billion

-

CAGR: 13.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Gaming PC Market - Request Free Sample Report

Gaming PC Market Trends

-

Rising demand for high-performance gaming experiences and immersive graphics is driving the gaming PC market.

-

Growing popularity of esports, game streaming, and competitive gaming is boosting market growth.

-

Expansion of AAA game titles and advanced game engines is fueling hardware upgrades.

-

Increasing focus on high refresh rate displays, ray tracing, and VR gaming is shaping adoption trends.

-

Advancements in GPUs, CPUs, cooling systems, and customizable PC builds are enhancing performance.

-

Rising disposable income and strong gaming community engagement are supporting market expansion.

-

Collaborations between hardware manufacturers, game developers, and esports organizations are accelerating innovation and global adoption.

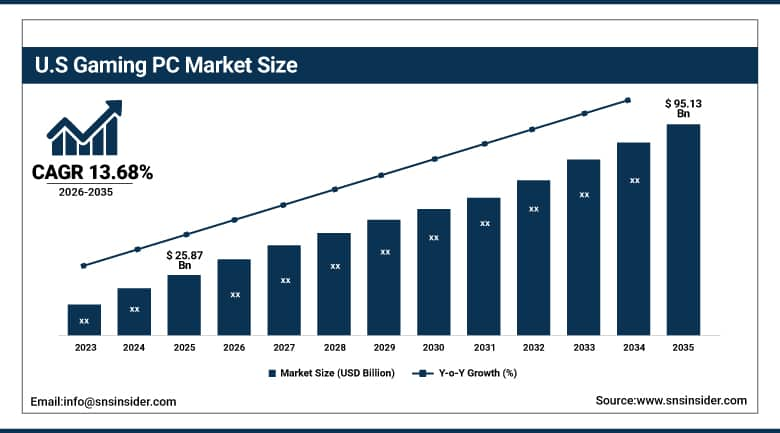

U.S. Gaming PC Market was valued at USD 25.87 billion in 2025 and is expected to reach USD 95.13 billion by 2035, growing at a CAGR of 13.68% from 2026-2035.

Growth in the U.S. Gaming PC Market is fueled by increasing trends in esports, an active gaming community, and high expenditure by consumers on high-end hardware. Growing demand for immersive experiences, technological developments in GPUs and processors, and an increasing trend of streaming contribute to continuous growth in the market.

The Entertainment Software Association reports that 97% of American households with children own a gaming device, with PC gaming representing a significant portion of household gaming hardware investment. NVIDIA's financial reports document that gaming GPU revenue continues to grow through each hardware generation as higher-performance tiers command premium pricing that more than offsets unit volume fluctuations.

Gaming PC Market Segment Analysis

-

By Product Category, Desktop segment dominated the Gaming PC Market in 2025 with ~61% share; Laptop segment fastest growing (CAGR).

-

By Price Range, High-end and Extreme High-end segment dominated the Gaming PC Market in 2025 with ~48% share; Mid-range segment fastest growing (CAGR).

-

By End-user, Professional Gamers segment dominated the Gaming PC Market in 2025 with ~52% share; Casual Gamers segment fastest growing (CAGR).

-

By Distribution Channel, Offline segment dominated the Gaming PC Market in 2025 with ~55% share; Online segment fastest growing (CAGR).

By Product, Desktop dominates, Gaming Laptop growing fastest

Desktop segment dominates the Gaming PC Market in 2025 because of the higher performance, greater ease of upgrading, and higher compatibility with cutting-edge gaming components. Professional gamers and esports athletes favor desktop computers for stable frames per second, better GPU performance, and effective cooling solutions. The growing preference for high-quality gaming rigs and customizable gaming setups makes the desktop segment more dominant.

The laptop segment will be the fastest-growing segment in the Gaming PC Market. The increasing preference for portable and powerful gaming equipment has resulted in advancements in lightweight GPUs, enhanced cooling technologies, and faster processors, which can support desktop-equivalent performance in laptops. With the increase in mobile gaming, esports competition, and flexible gaming lifestyles, the adoption rate is rising.

By Price Range, High-end and Extreme High-end dominates, Mid-range growing fastest

The High-end and Extreme High-end segment will have a significant presence in the Gaming PC Market in 2025 because there is heavy demand for these products amongst professional gamers, content creators, and esports enthusiasts who need exceptional performance. High-end products provide powerful GPUs, faster processing capabilities, and superior graphics quality to enhance their gaming experience. The rising popularity of AAA games and competition-oriented gaming further increases the demand for these products.

The Mid-range Segment will be the Fastest-growing in the Gaming PC Market 2025. This is because the price range of this type of product is affordable for consumers while still providing adequate performance. In this way, people can enjoy playing popular games on their computers without spending a lot of money. Additionally, the increasing number of casual gamers and beginners in gaming is also contributing to this growth trend.

By Product, Professional Gamers dominates, Casual Gamers growing fastest

The Professional Gamers segment leads the Gaming PC Market owing to a strong need for advanced gaming systems needed for playing games competitively and participating in gaming events and tournaments. Users in this segment spend considerably on advanced gaming configurations with the highest quality of graphic capabilities and processing power along with other customization options. Esports industry development and sponsorship for players further help this segment dominate in terms of the Gaming PC Market.

The Casual Gamers segment experiences the most rapid expansion within the Gaming PC Market due to growing popularity of gaming as a hobby around the world. Cost-effective gaming PCs, variety of gaming software, and easy availability contribute to a rapid increase in the number of users. The tendency towards shifting from mobile gaming to gaming on PCs adds to the popularity of this segment.

By Product, Offline dominates, Online growing fastest

Offline distribution segment dominates the Gaming PC Market due to greater consumer inclination toward brick-and-mortar shops, where buyers get to witness the performance of the computer system prior to buying. Retail shops, gaming shops, and authorized distributors offer personal assistance and customer service, contributing to increased buyer assurance. In many cases, high-end gaming computers have to undergo verification, and hence, the offline mode is more preferred.

Online Distribution is the fastest-growing segment in the Gaming PC Market because consumers prefer to make purchases online for convenience, product comparison, and lower prices. The rise in the popularity of direct selling channels and online customization tools has boosted sales in this segment. Furthermore, the quick proliferation of the internet and discounts on products are driving the growth of this segment.

Gaming PC Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

89% |

|

Asia Pacific |

China |

48% |

|

Europe |

Germany |

25% |

|

Middle East & Africa |

Saudi Arabia |

35% |

|

Latin America |

Brazil |

48% |

North America Gaming PC Market Insights

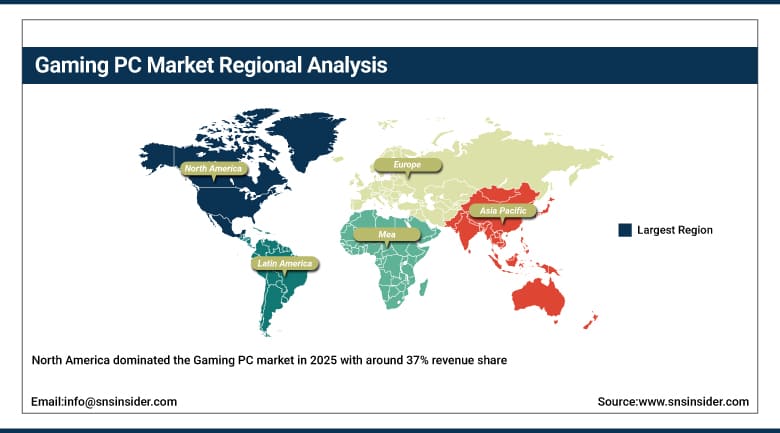

North America dominated the Gaming PC market in 2025 with around 37% revenue share owing to the highly developed and sophisticated gaming environment. Disposal income levels allow people to purchase the best gaming PCs. Also, North America is known for having a highly developed esports community, digital infrastructure, and broadband penetration. Presence of gaming hardware makers and hosting of gaming events is another factor supporting demand. Growth will be bolstered by growing popularity of gaming and streaming.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Gaming PC Market Insights

Asia Pacific is the fastest-growing regional Gaming PC Market, driven by China's enormous gaming population and established PC gaming culture anchored in multiplayer online games, South Korea's world-class PC gaming cafe (PC bang) infrastructure and professional esports ecosystem, Japan's hardware-enthusiast gaming culture, and the rapidly expanding gaming populations across Southeast Asia and India. China's PC gaming market is historically defined by the cultural and regulatory distinctions between PC online games which historically dominated Chinese gaming and console gaming which faced import restrictions. The lifting of those restrictions and the growing affluence of Chinese gamers is driving PC hardware upgrading toward higher performance tiers.

China's National Bureau of Statistics reports that domestic game market revenues exceeded CNY 303 billion in 2023. South Korea's Ministry of Culture, Sports and Tourism estimates that PC gaming cafes (PC bangs) operate approximately 15,000 locations nationally, each purchasing premium gaming hardware on regular 2-3 year replacement cycles.

Europe Gaming PC Market Insights

The Europe Gaming PC market is growing consistently owing to the existing culture of gaming, increased involvement of esports professionals, and the growing demand for superior computer systems. Some of the major contributors to this include Germany, UK, and France because of high disposable income levels and highly developed digital infrastructure. The increasing popularity of games that can be played online as well as the rise in usage of live streaming services is contributing to the increased demand.

Middle East & Africa and Latin America Gaming PC Market Insights

Middle East & Africa and Latin America Gaming PC Markets are growing gradually owing to increased numbers of young people, enhanced internet usage, and development of the gaming culture. The popularity of gaming tournaments and online multiplayer games is creating demand for gaming PCs. Better economic environment and reduced prices are facilitating the use of gaming PCs in Latin America, while investments in digital infrastructure and games are spurring interests in the Middle East & Africa region.

Gaming PC Market Growth Drivers:

-

Esports growth and AI-enhanced GPU performance creating sustained global gaming PC market expansion

Gaming PC market growth is being sustained by two forces that reinforce each other commercially. Esports has professionalized PC gaming in ways that justify hardware investment beyond hobby interest professional esports players earn six-figure salaries in major titles, streaming platforms pay content creators based on viewership that gaming PC performance directly affects, and the competitive player development ecosystem from high school esports programs to college varsity teams to professional league play creates institutional demand for high-performance gaming hardware. GPU technology advancement is the second force each generation of NVIDIA and AMD graphics cards delivers performance improvements that make previously inaccessible gaming experiences 4K high-refresh gaming, ray-traced lighting at high quality settings, and AI-enhanced visual fidelity achievable at the next price tier down, expanding the addressable market for premium gaming without requiring price reduction.

Gaming PC Market Restraints:

-

High hardware costs and complexity limiting gaming PC adoption among non-enthusiast consumers and budget-constrained markets

High-end gaming personal computers present a significant financial investment which restricts the size of the market available to individuals who have enough financial flexibility as well as passion for the game hobby. The lowest estimate of an adequately configured computer able to run current AAA games on maximum graphics and settings is $800-1,500, and a high-end computer costs upwards of $2,500-$4,000, making it something that requires proper planning for middle-class people. The difficulties involved in gaming with a PC like setting up drivers, adjusting configurations for optimal performance, diagnosing problems, etc., present another issue not present in console gaming.

Gaming PC Market Opportunities:

-

Pre-built gaming PC growth and gaming laptop performance improvement creating new market expansion opportunities globally

Pre-built gaming PC systems where consumers purchase complete systems from brands like Alienware, ASUS ROG, MSI, and CyberPowerPC rather than building their own are growing faster than the broader gaming PC market and represent the primary access point for gaming PC hardware among non-enthusiast buyers. Brands have improved pre-built PC value significantly in recent years, reducing the traditional pricing premium over equivalent DIY component costs while offering convenience, warranty support, and aesthetically designed systems that appeal to buyers who want gaming capability without technical involvement. The gaming laptop performance trajectory is a separate opportunity as mobile GPU architectures continue closing the performance gap with desktop equivalents, the laptop form factor will increasingly satisfy the performance requirements that previously required a desktop for competitive gaming and content creation applications, expanding the addressable high-end market to buyers who cannot or will not maintain a desktop gaming setup.

Recent Developments:

-

2026: NVIDIA launched its GeForce RTX 5090 flagship GPU using TSMC's 3nm manufacturing process, delivering a 70% performance improvement versus the RTX 4090 in full-precision gaming workloads and a 4x ray tracing performance increase through enhanced dedicated RT cores, establishing a new flagship gaming PC performance benchmark that accelerates upgrade cycles among the extreme high-end market segment.

-

2025: ASUS ROG announced its ROG Ally X Pro gaming handheld device powered by AMD's next-generation Ryzen Z2 Extreme SoC, achieving desktop RTX 3080-level GPU performance in a handheld form factor a performance milestone that validates the gaming handheld category as a legitimate premium gaming PC alternative for travel and portable gaming scenarios.

-

2025: Intel launched its Core Ultra 9 285HX mobile processor with integrated Xe2 Arc graphics delivering 1080p gaming at 60fps from a 45W processor package without discrete GPU, targeting the thin-and-light gaming laptop segment where thermal constraints previously prevented high-quality gaming without a discrete GPU.

Gaming PC Market Key Players

Some of the Gaming PC Market Companies

-

Acer

-

Advanced Micro Devices, Inc.

-

Alienware (Dell Inc.)

-

CORSAIR

-

NVIDIA

-

CyberPowerPC

-

Lenovo Group Ltd.

-

Razer Inc.

-

Digital Storm

-

Micro-Star International (MSI)

-

ASUS

-

HP Inc.

-

Samsung Electronics Co., Ltd.

-

Apple Inc.

-

Hewlett Packard Enterprise Company

-

Origin PC

-

XPG

-

Zotac

-

Maingear

-

Ibuypower

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 73.94 Billion |

| Market Size by 2035 | USD 271.8 Billion |

| CAGR | CAGR of 13.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Desktop, Laptop, Peripherals) • By Price Range (Low-range, Mid-range, High-end and Extreme High-end-range) • By End-user (Professional Gamers, Casual Gamers, Others) • By Distribution Channel (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Acer, Advanced Micro Devices, Inc., Alienware (Dell Inc.), CORSAIR, NVIDIA, CyberPowerPC, Lenovo Group Ltd., Razer Inc., Digital Storm, Micro-Star International (MSI), ASUS, HP Development Company, L.P., Samsung Electronics Co., Ltd., Apple Inc., Hewlett Packard Enterprise Company, Origin PC, XPG, Zotac, Maingear, iBUYPOWER |

Frequently Asked Questions

ANS: North America dominated the market with around 33% of the revenue share.

Ans: The Gaming Laptop segment is expected to register the fastest CAGR through 2035.

Ans: The Desktop segment dominated the Gaming PC Market in 2025.

Ans: The Gaming PC Market was valued at USD 73.94 billion in 2025.

Ans: The Gaming PC Market is expected to grow at a CAGR of 13.68% from 2026 to 2035.

Get in Touch