Web Performance Market Report Scope & Overview:

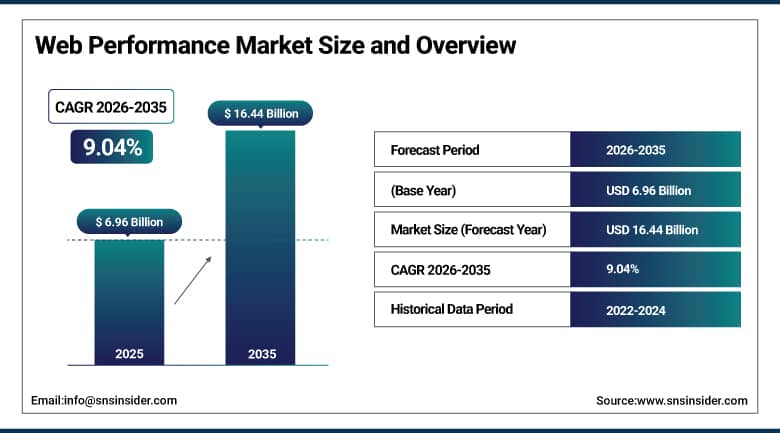

The Web Performance Market was valued at USD 6.96 Billion in 2025 and is expected to reach USD 16.44 Billion by 2035, growing at a CAGR of 9.04% from 2026–2035.

The global web performance market is growing at an exceptional pace. Web performance solutions encompass content delivery networks, performance monitoring tools, load testing platforms, application performance management, website optimisation software, and related services that ensure fast, reliable, and scalable digital experiences. The market is driven by the growing reliance on web-based services and platforms for business operations, the proliferation of data-heavy content including video, interactive media, and real-time applications, and the direct revenue impact that page load time has on e-commerce conversion rates and user retention.

In 2024, Akamai Technologies launched its AI-powered Edge Delivery platform, integrating machine learning-based traffic routing, real-time performance anomaly detection, and automated content optimisation that dynamically adapts delivery parameters to current network conditions. The launch reflects the commercial direction of web performance solution development toward autonomous optimisation systems whose AI decision-making operates at network speeds that human operator intervention cannot match, creating performance consistency improvements whose commercial value is measured in conversion rate and user engagement uplift.

Market Size and Forecast

-

Market Size in 2026E: USD 7.59 Billion

-

Market Size by 2035: USD 16.44 Billion

-

CAGR: 9.04% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Web Performance Market - Request Free Sample Report

Web Performance Market Trends

-

AI-powered web performance optimization is enabling automated improvements in content delivery, caching, and image management, helping websites achieve faster load times and better user experiences

-

Adoption of Core Web Vitals as a search ranking factor is encouraging organizations to invest in website performance to improve visibility, engagement, and conversion outcomes

-

Edge computing deployment is reducing content delivery latency by processing and serving data closer to end users, improving responsiveness across global digital platforms

-

Mobile-first performance strategies are gaining priority as the majority of web traffic originates from mobile devices operating under varying network conditions

-

Convergence of synthetic monitoring and real-user monitoring solutions is providing organizations with comprehensive visibility into website performance and user experience quality across digital environments

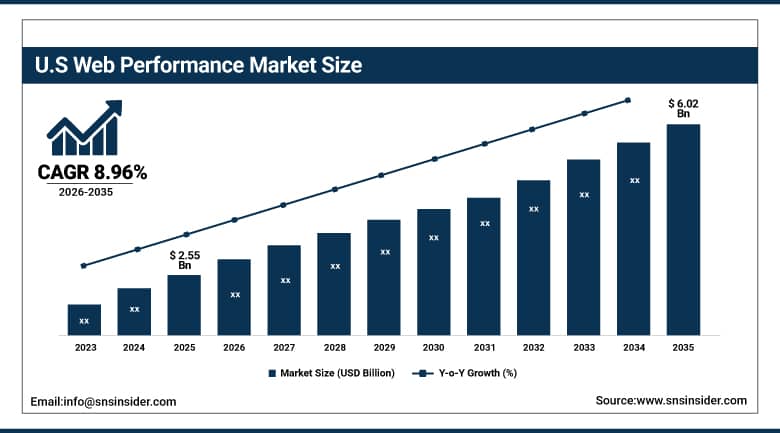

U.S. Web Performance Market Outlook

The U.S. Web Performance Market was valued at approximately USD 2.55 Billion in 2025 and is expected to reach approximately USD 6.02 Billion by 2035, growing at a CAGR of approximately 8.96%.

The U.S. is the world's most commercially sophisticated web performance market within North America's dominant revenue position. Akamai, Cloudflare, Fastly, New Relic, and Datadog are headquartered in the U.S. and collectively define the global web performance solution and CDN technology frontier. The U.S. e-commerce sector's above-average revenue sensitivity to web performance creates structured commercial motivation for premium solution specification. Google's Core Web Vitals search ranking factor creates regulatory-adjacent commercial pressure that sustains web performance investment independently of discretionary digital marketing budget cycles.

Cloudflare launched its AI-powered Workers AI inference platform in 2024, enabling developers to run machine learning models at Cloudflare's global edge network of over 310 cities, reducing AI inference latency for web applications whose real-time personalisation and content generation requirements create new performance optimisation challenges beyond conventional static content delivery. The platform creates a new commercial category of AI-powered edge application performance whose growth compounds with AI feature adoption in consumer-facing web applications.

Web Performance Market Segment Analysis

-

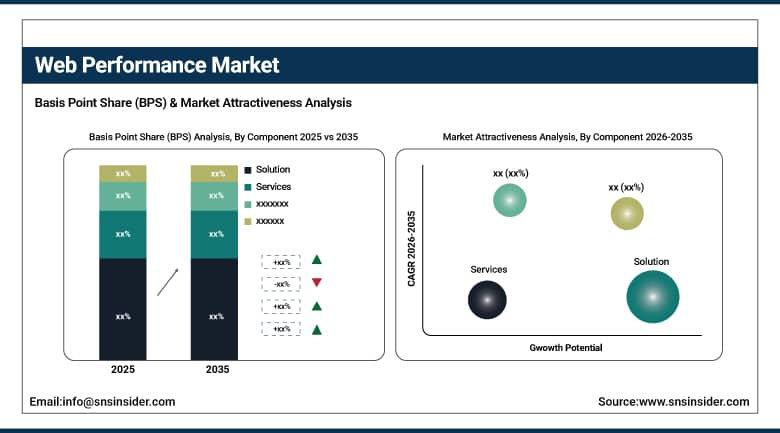

By Component, the Solution segment dominated the Web Performance Market with 69% share in 2025, while the Services segment is the fastest growing segment.

-

By Deployment Mode, the Cloud-Based segment dominated the Web Performance Market with approximately 58% share in 2025, while the Hybrid deployment segment is the fastest growing segment.

-

By Organisation Size, the Large Enterprises segment dominated the Web Performance Market with approximately 63% share in 2025, while the Small & Medium Enterprises segment is the fastest growing segment.

-

By End User, the IT & Telecom segment dominated the Web Performance Market with approximately 24% share in 2025, while the Retail & E-Commerce segment is the fastest growing segment.

By Component, solution dominates, services grow fastest

Solutions retained the dominant component position with 69% of the web performance market in 2025. Their commercial primacy reflects the foundational requirement for deployed technology platforms that create web performance capability. Content delivery network subscriptions, performance monitoring platforms, load testing software, and application performance management tools collectively constitute the solution portfolio whose procurement defines the majority of web performance commercial investment value. The solution segment's dominance reflects both the commercial maturity of web performance technology categories and the enterprise's recognition that web performance capability requires software-defined infrastructure whose deployment quality directly determines digital experience outcomes.

Services are the fastest-growing component because web performance's technical complexity creates consulting, implementation, and managed service demand that exceeds many enterprise teams' internal capability. Managed web performance services that operate CDN configurations, monitor performance metrics, and respond to performance degradation events create recurring revenue relationships whose service continuity compounds with the managed service model's commercial momentum. Performance consulting that architects the transition from legacy infrastructure toward modern edge-delivered architectures creates project-based revenue that sustains above-average services segment growth.

By Deployment, cloud dominates, hybrid grows fastest

Cloud-based deployment retained the dominant position with approximately 58% of the web performance market in 2025. Web performance solutions’ fundamental commercial logic naturally favours cloud delivery because the content delivery network infrastructure, the global points of presence, and the real-time traffic routing intelligence that web performance requires are inherently cloud-native capabilities whose geographic distribution cannot be replicated within on-premise data centre boundaries. Cloud-delivered CDN whose edge nodes span hundreds of cities globally creates latency reduction that on-premise alternatives cannot achieve regardless of infrastructure investment.

Hybrid deployment is the fastest-growing model because regulated enterprises whose data sovereignty requirements mandate on-premise processing of certain content categories must integrate cloud-delivered edge performance with on-premise origin infrastructure. Each enterprise whose e-commerce platform combines cloud-delivered static content acceleration with on-premise personalisation and transaction processing creates a hybrid architecture requirement whose performance management spans both environments and creates demand for unified monitoring and optimisation that hybrid deployment solutions address.

By End User, IT & telecom dominates, retail grows fastest

IT and Telecom retained the dominant end-user position with approximately 24% of the web performance market in 2025. The sector's leadership reflects its unique combination of the most demanding web performance requirements of any industry vertical, the deepest technical expertise to implement sophisticated performance architectures, and the most direct revenue sensitivity to digital experience quality. Telecom operators managing subscriber-facing portals, streaming platforms, and cloud service interfaces whose digital experience quality directly determines churn rate create structured web performance investment motivation that sustains the sector's market leadership.

Retail and e-commerce is the fastest-growing end user because the direct revenue impact of web performance on e-commerce conversion rates creates the most financially compelling commercial case for web performance investment of any end-user category. Each additional second of page load time reduces e-commerce conversion rates by up to 7%, creating a revenue impact calculation that directly funds web performance solution investment. The extraordinary growth of global e-commerce and the progressive migration of retail revenue from physical to digital channels creates a continuously expanding web performance investment pool whose commercial scale grows with e-commerce penetration.

By Organisation Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant organisation size position with approximately 63% of the web performance market in 2025. Large enterprise web performance investment reflects the direct revenue and brand impact that digital experience quality creates at above-average traffic volumes. Each major enterprise whose digital presence serves millions of daily users creates web performance investment whose return is measured in conversion rate improvement, brand experience consistency, and competitive differentiation whose combined commercial value justifies premium solution specification. Global enterprises whose web presence serves users across multiple geographies create particular demand for CDN and edge performance infrastructure whose geographic coverage creates consistent experience quality regardless of user location.

SMEs are the fastest-growing segment because cloud-delivered web performance solutions’ subscription pricing models are progressively making enterprise-grade CDN, performance monitoring, and optimisation capability commercially accessible at cost levels that small business digital marketing budgets can accommodate. Each new SME that migrates from self-hosted web infrastructure toward cloud-delivered performance solutions creates recurring subscription revenue whose aggregate across millions of SME websites compounds with digital adoption growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

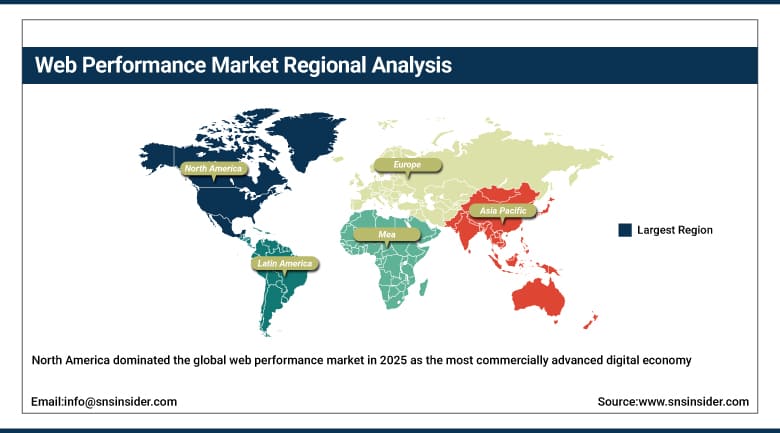

North America Web Performance Market Insights

North America dominated the global web performance market in 2025 as the most commercially advanced digital economy. The United States accounts for approximately 87.4% of North American revenues through Akamai, Cloudflare, Fastly, New Relic, and Datadog’s commercial dominance whose combined portfolio defines the global web performance technology standard. The e-commerce sector's above-average web performance sensitivity, Google's Core Web Vitals ranking factor, and the enterprise digital transformation investment collectively sustain the world's highest per-capita web performance solution investment.

Canada contributes approximately 12.6% of North American revenues through its e-commerce sector's growing digital investment, the technology industry’s web performance infrastructure, and the enterprise digital transformation programme whose combined demand sustains consistent market engagement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Web Performance Market Insights

Europe is a technically sophisticated web performance market where GDPR’s data residency requirements create performance architecture constraints whose resolution drives hybrid cloud web performance investment. Germany accounts for approximately 22.3% of European revenues through its advanced digital enterprise infrastructure, the e-commerce sector's above-average performance investment, and the technology industry's cloud adoption whose combined demand creates consistent procurement.

The United Kingdom, France, and the Netherlands are significant secondary markets where e-commerce penetration, digital media consumption, and enterprise cloud adoption create consistent web performance investment. Cloudflare’s London operations and Akamai’s European infrastructure sustain domestic market supply alongside global CDN networks.

Asia Pacific Web Performance Market Insights

Asia Pacific is the fastest-growing regional web performance market, driven by the extraordinary growth of digital commerce in China, India, Southeast Asia, and Australia whose combined e-commerce transaction volume creates above-average web performance investment motivation. China accounts for approximately 44.8% of Asia Pacific revenues through its e-commerce platforms’ extraordinary performance requirements serving hundreds of millions of daily active users, and Alibaba Cloud and Tencent Cloud’s domestic CDN infrastructure.

India represents the most commercially dynamic emerging market within Asia Pacific where the digital economy’s rapid expansion, UPI payment infrastructure’s e-commerce enablement, and the enterprise sector’s cloud adoption are creating above-average first-time web performance solution procurement across technology, retail, and financial services sectors.

MEA & Latin America Web Performance Market Insights

UAE leads MEA revenues at approximately 38.4% through its above-average digital economy sophistication, the e-commerce sector’s rapid adoption, and the enterprise technology investment creating structured web performance procurement. Brazil leads Latin American revenues at approximately 44.2% through its large e-commerce market, fintech sector’s performance-sensitive digital infrastructure, and the enterprise digital transformation programme.

Saudi Arabia’s Vision 2030 digital economy investment and South Africa’s growing technology sector represent significant secondary MEA markets whose digital adoption is creating expanding web performance solution procurement.

Market Dynamics:

Growth Drivers: E-commerce conversion rate sensitivity and Google Core Web Vitals creating non-discretionary performance investment

E-commerce revenue’s direct sensitivity to web performance metrics is the web performance market’s most compelling commercial growth driver. The documented correlation between page load time and e-commerce conversion rates—where each additional second reduces conversion by 7% and Walmart’s 1-second improvement created 2% revenue increase—creates a financial ROI calculation that directly funds web performance investment. As global e-commerce revenue grows toward USD 8 trillion by 2030, each percentage point of conversion rate improvement creates billions of dollars of incremental revenue whose financial magnitude sustains above-average web performance solution investment.

Google Core Web Vitals as a Search ranking signal creates compliance-driven web performance investment that is independent of discretionary digital marketing budget allocation. Each enterprise whose Search Engine Results Page position directly determines organic traffic volume has non-discretionary motivation to achieve Core Web Vitals passing thresholds whose technical requirements create web performance solution procurement. Google's progressive Core Web Vitals signal refinement creates continuous technical standard evolution that sustains ongoing web performance investment beyond initial compliance achievement.

Restraints: Implementation complexity for legacy infrastructure and data privacy constraints on performance monitoring

Legacy website infrastructure’s integration complexity with modern web performance solutions creates implementation barriers that delay adoption timelines for enterprises whose technical debt limits the pace of infrastructure modernisation. Each legacy application whose architecture prevents edge caching, requires server-side rendering incompatible with CDN delivery, or creates dynamic content that performance optimisation tools cannot process creates implementation engineering investment whose cost and timeline create commercial adoption resistance.

Data privacy regulations including GDPR’s restrictions on user tracking and CCPA’s consent requirements create constraints on real-user monitoring data collection whose limitation reduces web performance visibility into authentic user experience metrics. Each privacy regulation that restricts performance cookie deployment or user journey tracking creates measurement gaps whose impact on performance optimisation decision quality reduces the commercial value of performance monitoring investment.

Opportunities: AI-powered autonomous optimisation and edge computing performance for emerging markets

AI-powered autonomous web performance optimisation represents the most commercially transformative technology direction whose autonomous operation creates performance improvements without the human expertise that traditional performance engineering requires. Each AI optimisation platform that demonstrates measurable conversion rate improvement at enterprise scale without dedicated performance engineering staff creates a commercial value proposition that sustains premium solution pricing and accelerates adoption across organisations whose technical staff constraints previously limited performance investment.

Edge computing’s progressive global expansion into emerging market geographies is creating new web performance infrastructure whose proximity to previously underserved user populations creates latency reduction whose commercial value compounds with digital economy growth. Each new edge computing point of presence in Southeast Asia, Africa, or Latin America creates web performance improvement for the region’s growing digital commerce population whose improved experience sustains regional digital economic growth.

Recent Developments:

-

2024: Akamai Technologies launched its AI-powered Edge Delivery platform in 2024 integrating machine learning-based traffic routing, real-time performance anomaly detection, and automated content optimisation that dynamically adapts delivery to current network conditions.

-

2024: Cloudflare launched its Workers AI inference platform in 2024, enabling developers to run machine learning models at Cloudflare's edge network of over 310 global cities, reducing AI inference latency for real-time personalisation and content generation in consumer-facing web applications.

-

2024: New Relic launched AI-powered anomaly detection for web performance monitoring in 2024, providing automated root cause analysis for page load degradation events whose rapid identification reduces mean time to resolution from hours to minutes for performance engineering teams.

Web Performance Market Key Players:

-

Akamai Technologies

-

Cloudflare Inc.

-

Fastly Inc.

-

New Relic Inc.

-

Datadog Inc.

-

Google LLC (Cloud CDN)

-

Microsoft Azure (Azure Front Door)

-

Amazon Web Services (CloudFront)

-

Imperva Inc.

-

StackPath

-

KeyCDN

-

Sucuri Inc.

-

ThousandEyes (Cisco)

-

Dynatrace

-

AppDynamics (Cisco)

-

ZenQ

-

CA Technologies (Broadcom)

-

Limelight Networks (Edgio)

-

Yottaa

-

Instart Logic

Web Performance Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.96 Billion |

| Market Size by 2035 | USD 16.44 Billion |

| CAGR | CAGR of 9.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solution, Services) • by Deployment Mode (Cloud-Based, On-Premise, Hybrid) • by Organisation Size (Large Enterprises, Small & Medium Enterprises) • by End User (IT & Telecom, Retail & E-Commerce, BFSI, Healthcare, Media & Entertainment, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

Frequently Asked Questions

The Web Performance Market is expected to grow at a CAGR of 9.04% from 2026 to 2035.

The Web Performance Market was valued at USD 6.96 Billion in 2025.

E-commerce revenue's direct sensitivity to web performance where each second of page load delay reduces conversion by 7%, and Google Core Web Vitals as Search ranking signals creating compliance-driven non-discretionary performance investment.

Solution dominated the Web Performance Market with 69% share in 2025, while the Services segment is the fastest growing.

North America dominated the Web Performance Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch