GPU As A Service Market Report Scope & Overview:

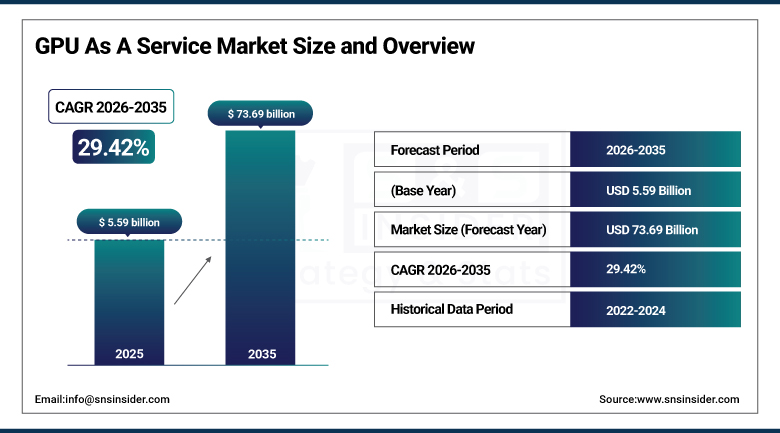

The GPU As A Service Market was valued at USD 5.59 billion in 2025 and is expected to reach USD 73.69 billion by 2035, growing at a CAGR of 29.42% from 2026-2035. This report includes key insights into adoption rates, highlighting increasing demand across industries such as AI and machine learning. It covers customer segmentation, with a focus on businesses seeking high-performance computing. Pricing trends reflect competitive models, while technological advancements in cloud infrastructure drive growth. Investment trends show a surge in funding, supporting innovation in GPU as a Service solutions, which are revolutionizing sectors like healthcare, automotive, and entertainment.

GPU As A Service Market Size and Forecast:

-

Market Size in 2025: USD 5.59 Billion

-

Market Size by 2035: USD 73.69 Billion

-

CAGR: 29.42% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To get more information on GPU As A Service Market - Request Free Sample Report

GPU As A Service Market Highlights:

-

Rising demand for AI and data analytics is driving the need for high-performance computing

-

High-performance GPUs enable faster computations and improved operational efficiency

-

GPUaaS provides cost-effective access to powerful GPU resources without large upfront hardware investments

-

High operational costs of cloud-based GPU usage can limit accessibility for smaller businesses

-

Growing adoption of edge computing is increasing demand for GPUaaS to process real-time data efficiently

-

GPUaaS offers scalable and agile computing solutions, reducing reliance on centralized data centers and lowering latency

GPU As A Service Market Drivers:

-

Rising Demand for AI, Machine Learning, and Data Analytics Drives High-Performance Computing Growth, Boosting the GPU as a Service Market

The fast growth of AI, machine learning, data analytics, and scientific computing is driving the demand for stronger computational capabilities to support intricate calculations. As companies increasingly rely on these technologies to glean insights and optimize operations, demand for high-performance computing continues to grow. Data in real-life scenarios has to be expressed in three dimensions so that GPUs which are parallel capable can take an important place in driving these applications for much shorter processing time and increased efficiency. As organizations seek cost-effective ways to access the required computational resources, GPU as a service (GPUaaS) provides an instrumental solution offering organizations on-demand access to general purpose GPUs without requiring high capital expenditure in purchasing physical hardware. This growing reliance on HPC is a significant facilitator for the GPUaaS market.

GPU As A Service Market Restraints:

-

High Operational Costs of GPUaaS Limit Its Accessibility for Smaller Businesses and Prolonged Usage

In a GPUaaS model, companies don’t have to purchase costly hardware, but the operational expenses for cloud-based GPU computing may still be significant. These are very expensive especially for long running/ compute intensive tasks where such cloud computing services usually charge based on time and use of resources. These expenses can add up to become a fiscal albatross for companies relying on persistent or massive amounts of GPU resources. This could restrict SMEs or startups who do not have sufficient budget for their IT infrastructure requiring the availability of GPUaaS and also limit the broader adoption, even with its benefits like flexibility and scalability.

GPU As A Service Market Opportunities:

-

Increased Adoption of Edge Computing Creates Growing Demand for GPU as a Service in Real-Time Data Processing

As edge computing gains ground, the requirement for high-performance computing to carry out computations closer to the point of data creation is on the rise. The change also drives massive demand for resource-based on GPU, which will enable complex computing in real-time, especially in the areas of autonomous vehicles, IoT devices, and smart cities. With the capability of offering on-demand access to the powerful GPU computing capabilities, GPU as a Service offers a flexible and scalable edge computing solution for businesses. With the capability of offering powerful GPUs at the edge, the need for a centralized data center is no longer required, making it more efficient and reducing latency. With more industries adopting edge computing to enable faster data processing, the demand for GPUaaS will increase, and the whole market will be opened.

GPU As A Service Market Segment Analysis:

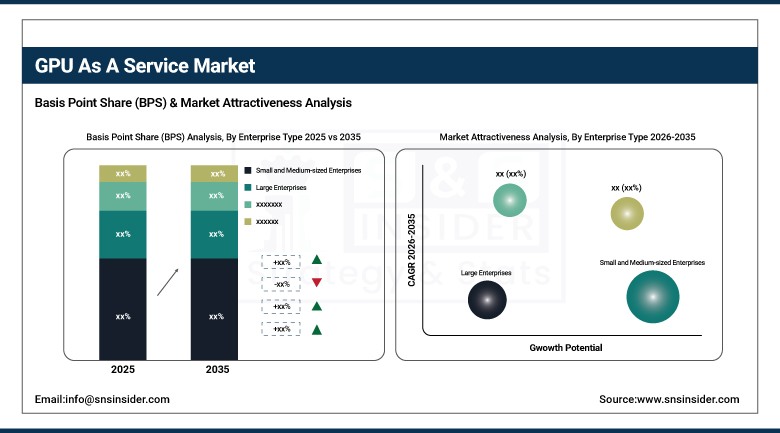

By Enterprise Type

Large Enterprises lead the GPU as a Service market because of their massive computing needs for tasks such as AI, machine learning, and big data analytics. Large Enterprises can afford the high operational costs associated with GPUaaS and have the infrastructure to support large cloud computing services using GPUs. Due to their large computing requirements and ability to adopt new technology, they are the market leaders in terms of revenue.

Small and Medium-sized Enterprises (SMEs) are projected to witness the highest growth rate in terms of CAGR, as cloud-based solutions are becoming increasingly accessible. SMEs are adopting the use of GPU as a Service in order to leverage high-performance computing capabilities without incurring high initial expenses, thus allowing them to expand their operations. Since GPU as a Service is a cost-effective solution, SMEs can compete effectively with large enterprises in the field of AI, data analysis, and innovation.

By Deployment Model

The Public GPU Cloud market segment led the GPU as a Service market because of its scalability, cost-effectiveness, and wide accessibility. Public cloud service providers offer flexible pricing structures, which enables companies to pay only for the services they consume. This attracts large businesses and SMEs. The scalability of computing capacity as needed, with low capital outlay, makes public GPU cloud services the service of choice for organizations.

The Hybrid GPU Cloud market is anticipated to register the fastest growth rate in terms of CAGR, as there is an increasing requirement for a combination of the benefits of public and private cloud services. Enterprises are looking for hybrid solutions that allow them to leverage the scalability of the public cloud and the security of the private cloud.

By Application

The IT & Telecommunication sector led the GPU as a Service market because of the growing need for high-performance computing in networking, data centers, and telecommunication. Service providers in this industry need GPU-enabled solutions for handling large datasets, supporting AI-enabled applications, and managing complex networks. As telecom operators are increasing their 5G networks and developing AI-enabled systems, GPUaaS has become a critical solution for improving efficiency.

The Healthcare segment is expected to grow at the fastest CAGR due to the increasing adoption of AI, machine learning, and big data analytics for medical research, diagnostics, and treatment planning. Healthcare organizations leverage GPU-powered cloud services for faster data processing, improved accuracy in diagnostic imaging, and the analysis of large patient datasets. As innovation in healthcare technologies expands, GPUaaS adoption accelerates, fueling rapid growth in the sector.

By Enterprise Type

Pay-per-use segment led the GPU as a Service market with the highest revenue share of around 69% in 2025 and is anticipated to register the fastest CAGR of around 30.20% from 2026 to 2035. The Pay-per-use pricing model is most widely adopted because of its flexibility and cost-effectiveness, which enables organizations to harness the power of high-performance GPU computing without incurring significant capital costs. The pricing model is appropriate for organizations that require scalable solutions to handle fluctuating workloads, especially small to medium-sized enterprises (SMEs) with constrained budgets.The adoption is fueled by the rising need for on-demand computing capabilities in AI, data analytics, and real-time computing applications. The flexibility to dynamically scale computing resources in real-time, along with the adoption of cloud computing, is driving the Pay-per-use segment.

GPU As A Service Market Regional Analysis:

North America GPU As A Service Market Trends:

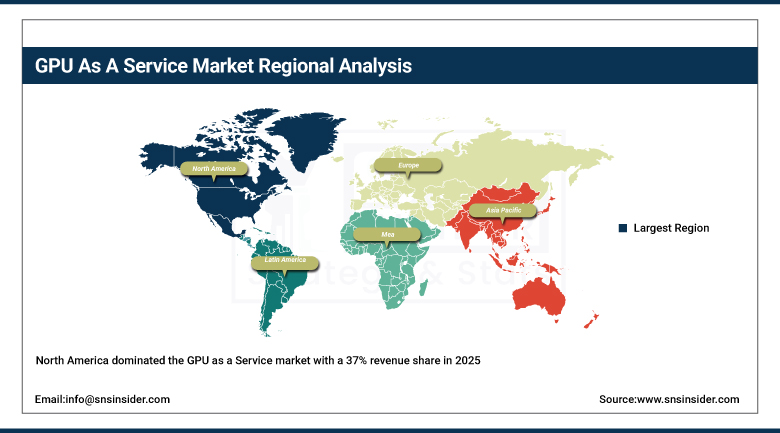

North America dominated the GPU as a Service market with a 37% revenue share in 2025 due to the region's strong presence in advanced technological sectors like AI, machine learning, and data analytics. The high adoption of cloud computing and strong infrastructure investments, especially in industries such as IT, telecommunications, and healthcare, further contributed to this dominance. Leading tech companies in the U.S. and Canada drive innovation in GPU-powered services, making North America a key market player.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific GPU As A Service Market Trends:

Asia Pacific is expected to grow at the fastest CAGR of about 31.16% from 2026-2035 due to rapid technological advancements and increasing digital transformation in industries like healthcare, automotive, and manufacturing. The increasing adoption of AI, IoT, and 5G technologies in the region, as well as the growing demand for high-performance computing, is driving the need for GPUaaS. In addition, the initiatives of the government to support innovation in technology are also adding to the rapid growth in this region.

Europe GPU As A Service Market Trends:

Europe accounted for a substantial share in the GPUaaS industry in 2025, due to large scale investments made in AI, ML and cloud computing infrastructure across nations including Germany, UK and France. Increasing emphasis on digital transformation in industries such as automotive, banking and healthcare along with strong support from the government for the adoption of technology are driving slowly but steady growth in the market. Europe is anticipated to grow at a steady pace due to the rising popularity of high-performance computing services among businesses in the region.

Latin America GPU As A Service Market Trends:

The adoption of GPUaaS is increasing in Latin America, especially in industries like finance, healthcare, and manufacturing. The growth of cloud infrastructure, interest in AI and HPC, and IT spending in Brazil and Mexico are factors that contribute to the growth of the market. The market in Latin America is expected to grow steadily during the forecast period as organizations adopt GPU solutions to improve computational efficiency.

Middle East & Africa (MEA) GPU As A Service Market Trends:

The MEA region is slowly entering the GPUaaS market, with the growth being driven by the adoption of cloud computing and AI adoption in sectors such as oil & gas, finance, and government services. The growth of the market is expected to be steady, with the support of the MEA governments in the development of the economy through technology.

GPU As A Service Market Key Players:

-

Alibaba Cloud (Elastic GPU, ECS GPU-optimized instances)

-

Vultr (GPU Compute Instances, Cloud GPU)

-

Linode LLC. (Linode GPU, GPU-Optimized Plans)

-

Amazon Web Services, Inc. (Elastic GPU, EC2 P3 Instances)

-

Google (Google Cloud GPU, Tensor Processing Units)

-

IBM Corporation (IBM Cloud GPU, Virtual Servers with GPU)

-

OVH SAS (GPU Cloud Instances, GPU Dedicated Servers)

-

Lambda Labs (Lambda GPU Cloud, Lambda GPU Workstations)

-

Hewlett Packard Enterprise Development LP (HPE GreenLake with GPU, HPE Cloud GPU Servers)

-

CoreWeave (GPU Cloud, Virtual GPUs)

-

Arm Holding PLC (Arm-based GPUs, Arm Compute Instances)

-

Fujitsu Ltd (Fujitsu Cloud GPU, Cloud Service with GPU)

-

HCL Technologies (HCL Cloud GPU, GPU-Optimized Virtual Machines)

-

Intel Corporation (Intel GPU Cloud Service, Xe Graphics Cloud Service)

-

Microsoft Corporation (Azure N-Series, GPU Virtual Machines)

-

NVIDIA Corporation (NVIDIA DGX, NVIDIA A100 GPU Cloud Instances)

-

Oracle Corporation (Oracle Cloud GPU, Virtual Machine GPU)

-

Qualcomm Technologies, Inc. (Snapdragon GPUs, Cloud AI Solutions)

-

Tencent Cloud (Tencent Cloud GPU, GPU Cloud Instances)

-

Huawei Cloud (Huawei Cloud GPU, Cloud GPU Servers)

-

Baidu AI Cloud (Baidu Cloud GPU, Cloud Computing with GPU)

-

Packet (Packet GPU, High-Performance GPU Instances)

-

DigitalOcean (DigitalOcean GPU, Cloud GPU Instances)

-

Rackspace (Rackspace GPU Cloud, GPU-Optimized Servers)

-

Scaleway (Scaleway GPU, Cloud GPU Instances)

-

Hetzner Online (Hetzner GPU Cloud, GPU Servers)

GPU As A Service Market Competitive Landscape:

-

In October 2024, Vultr introduced its GPU Stack and Container Registry, providing easy access to NVIDIA's NGC catalog of pre-trained large language models. This launch aims to accelerate AI and GPU-driven applications.

-

In January 2025, Qualcomm's Snapdragon X Series pushed the boundaries of the PC category with enhanced GPU performance, mini desktop designs, and NPU-powered AI capabilities.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.59 Billion |

| Market Size by 2035 | USD 73.69 Billion |

| CAGR | CAGR of 29.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Pricing Model (Pay-per-use, Subscription-based Plans) • By Deployment Model (Private GPU Cloud, Public GPU Cloud, Hybrid GPU Cloud) • By Enterprise Type (Small and Medium-sized Enterprises, Large Enterprises) • By Application (Healthcare, BFSI, Manufacturing, IT & Telecommunication, Automotive, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Alibaba Cloud, Vultr, Linode LLC., Amazon Web Services, Inc., Google, IBM Corporation, OVH SAS, Lambda Labs, Hewlett Packard Enterprise Development LP, CoreWeave, Arm Holding PLC, Fujitsu Ltd, HCL Technologies, Intel Corporation, Microsoft Corporation, NVIDIA Corporation, Oracle Corporation, Qualcomm Technologies, Inc., Tencent Cloud, Huawei Cloud, Baidu AI Cloud, Packet, DigitalOcean, Rackspace, Scaleway, Hetzner Online |

Frequently Asked Questions

Small and Medium-sized Enterprises (SMEs) are growing at the fastest CAGR due to the increasing accessibility of cloud-based solutions.

North America dominates the market with a 37% revenue share in 2025.

The Pay-per-use model holds about 69% of the revenue share in 2025 and is expected to grow at a CAGR of 30.20%.

The Hybrid GPU Cloud segment is expected to grow at the fastest CAGR of 31.16% from 2026-2035.

The GPU As A Service Market was valued at USD 5.59 billion in 2025 and is expected to reach USD 73.69 billion by 2035, growing at a CAGR of 29.42% from 2026-2035.

Get in Touch