Grid Automation Market Report Scope & Overview:

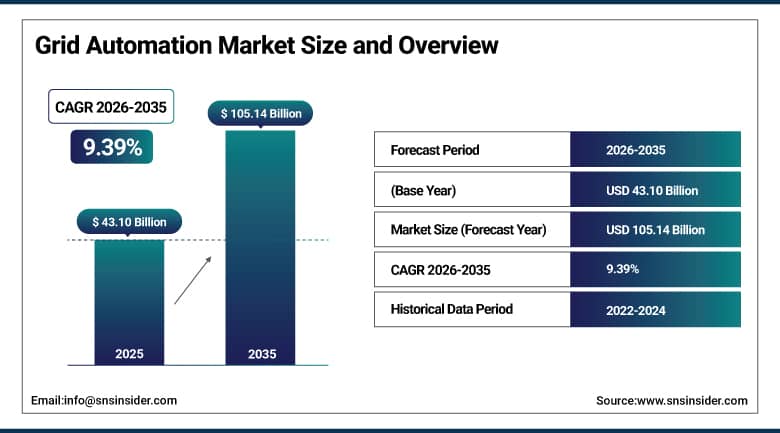

The Grid Automation Market was valued at USD 43.10 billion in 2025 and is expected to reach USD 105.14 billion by 2035, growing at a CAGR of 9.39% from 2026-2035.

Increasing investments in grid modernization and the replacement of aging transmission and distribution infrastructure are significantly boosting demand for grid automation solutions. Utilities are deploying advanced monitoring, control, and automation technologies to improve grid reliability, reduce outages, and enhance operational efficiency. Simultaneously, the rapid integration of renewable energy sources and distributed energy resources is increasing grid complexity, creating a strong need for automated systems capable of real-time monitoring, demand response, and dynamic load balancing, thereby accelerating the adoption of grid automation technologies worldwide.

According to the International Energy Agency (IEA), renewables are expected to meet approximately 95% of global electricity demand growth and provide more than one-third of total global electricity generation, increasing the need for advanced grid automation and digital grid management technologies.

Market Size and Forecast:

-

Market Size in 2026E: USD 46.89 Billion

-

Market Size by 2035: USD 105.14 Billion

-

CAGR: 9.39% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Grid Automation Market - Request Free Sample Report

Grid Automation Market Trends:

-

Increasing adoption of artificial intelligence for predictive maintenance and grid performance optimization.

-

Growing deployment of digital substations using intelligent electronic devices and advanced communication standards.

-

Rising integration of renewable energy sources requiring automated grid balancing and control systems.

-

Expanding implementation of cloud-based platforms for centralized grid monitoring and operational management.

-

Increasing use of Internet of Things sensors for real-time asset visibility and diagnostics.

U.S. Grid Automation Market Outlook:

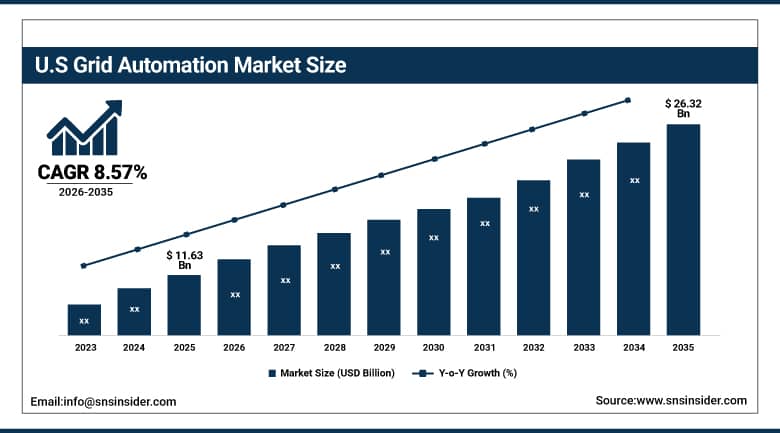

The U.S. Grid Automation Market was valued at USD 11.63 billion in 2025 and is expected to reach USD 26.32 billion by 2035, growing at a CAGR of 8.57% from 2026-2035.

The U.S. Grid Automation Market will be propelled by major investments made by the government in grid modernization along with the rise in renewable energy production. With the help of several government schemes, such as the Department of Energy’s grid resilience and innovation projects worth billions of dollars, the adoption of modern technologies for transmission and distribution systems will gain momentum. At the same time, growing installations of solar, wind and energy storage will lead to more complex grids, compelling utility companies to adopt automation systems.

The U.S. Department of Energy (DOE) is administering a USD 10.5 billion Grid Resilience and Innovation Partnerships (GRIP) Program to modernize transmission and distribution infrastructure, enhance grid resilience, and deploy smart grid technologies. The program has already announced more than USD 6 billion in funding for grid modernization projects across the United States.

Grid Automation Market Segment Analysis:

-

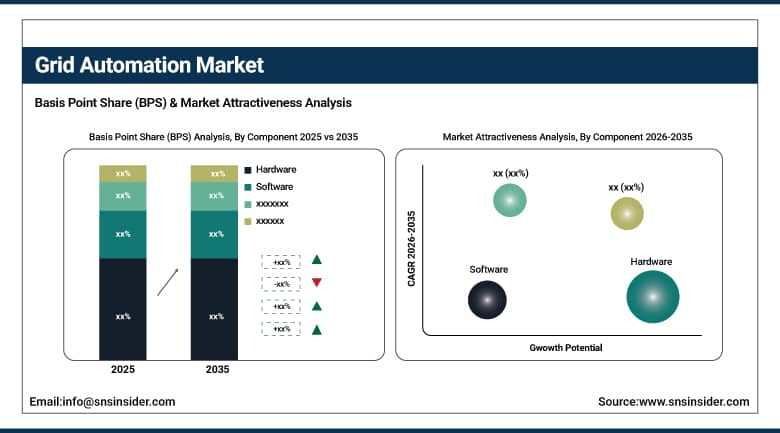

By component, hardware dominated the grid automation market in 2025 with 52.83% share; software is the fastest-growing segment with a 11.03% CAGR.

-

By automation type, substation automation dominated the market in 2025 with 38.45% share; distribution automation is the fastest-growing segment with a 10.57% CAGR.

-

By utility type, electric utilities dominated the market in 2025 with 84.28% share and is also the fastest-growing segment with a 9.93% CAGR.

-

By deployment mode, on-premise dominated the grid automation market in 2025 with 71.63% share; cloud-based is the fastest-growing segment with a 10.55% CAGR

-

By end user, public utilities dominated the grid automation market in 2025 with 48.56% share; renewable energy developers is the fastest-growing segment with a 13.04% CAGR

By Component, hardware segment dominates the grid automation market, software segment expected to grow fastest

The hardware segment dominates the grid automation market since grid automation systems involve huge capital investment in hardware components like intelligent electronics, sensors, remote terminal units, communication systems, and switchgear. It is important for utilities to upgrade their hardware in order to increase reliability, improve efficiency, and upgrade their transmission and distribution systems. The high installation base of substation and power system hardware globally helps the segment lead the market.

The software segment is projected to witness fastest growth driven by the rising implementation of sophisticated analytical tools and artificial intelligence and grid management software in the cloud. Software is being used by utilities for providing monitoring, maintenance, and decision-making capabilities. The demand for digital substations and management of distributed energy resources is driving software platform implementations.

By Automation Type, substation automation segment dominates the grid automation market, distribution automation segment expected to grow fastest

The substation automation segment dominates the market owing to the importance of substations in the power transmission and distribution chain. With utilities investing in automated substations to ensure improved reliability and shorter outages, along with the ability to remotely monitor and control, substation automation has emerged as the most profitable sector in the market, courtesy massive investments made to upgrade aging substations and integrate digital technology. The distribution automation segment will experience the fastest rate of growth, attributable to the investments being made for intelligent distribution networks and self-healing grid systems. Higher investments for renewable energy penetration, distributed generation, and electric vehicles are adding complications to the distribution system. Therefore, utilities are implementing advanced automation technology to cope with it.

By Utility Type, electric utilities segment dominates the grid automation market and is also expected to grow fastest

The electric utilities segment dominates the grid automation market since power utilities form the main end-users of grid automation solutions. Power companies have continued making significant investments in the modernization of grid networks and their transmissions, along with the improvement of their monitoring systems due to increasing demand for power. The high level of infrastructure and rising requirements for grid management contribute to the segment's dominant market position.

Besides, the electric utilities segment is also forecasted to grow at the fastest CAGR since there will be accelerated investments in renewables, grid digitalization, and electrification. The rising trend toward the adoption of grid automation solutions by electric utility companies is largely driven by government policies concerning smart grids deployment.

By Deployment Mode, on-premise segment dominates the grid automation market, cloud-based segment expected to grow fastest

The on-premise segment dominates the market because utilities prioritize data security, system reliability, and direct control over mission-critical grid operations. Many grid automation systems are integrated with legacy infrastructure that requires dedicated on-site deployment and highly secure communication networks. The need for low-latency operations and compliance with utility regulations has sustained the strong market position of on-premise solutions.

The cloud-based segment is expected to grow the fastest due to increasing demand for scalable, cost-efficient, and remotely accessible grid management platforms. Utilities are adopting cloud technologies to improve data analytics, enable predictive maintenance, and support centralized monitoring of distributed assets. The growing digital transformation of utility operations and advancements in cybersecurity are accelerating the migration toward cloud-based grid automation solutions.

By End User, public utilities segment dominates the grid automation market, renewable energy developers segment expected to grow fastest

Public utilities segment is dominating the grid automation market since the utilities which are owned by the government and are under regulation have extensive transmission and distribution systems and constitute the major share in the electricity supply around the globe. The utilities will keep on investing heavily in the automation of their grid systems due to several reasons, thus, becoming the biggest end users of these systems.

Renewable energy developers segment is expected to be the fastest growing one owing to the quick development of the projects related to the production of electricity through solar and wind energy and energy storage systems. Increasing investments in clean energy infrastructure and supportive government policies are driving the accelerated adoption of grid automation solutions among renewable energy developers.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.76% |

|

Europe |

Germany |

23.83% |

|

Asia Pacific |

China |

39.64% |

|

Middle East & Africa |

UAE |

24.17% |

|

Latin America |

Brazil |

46.26% |

North America Grid Automation Market Insights

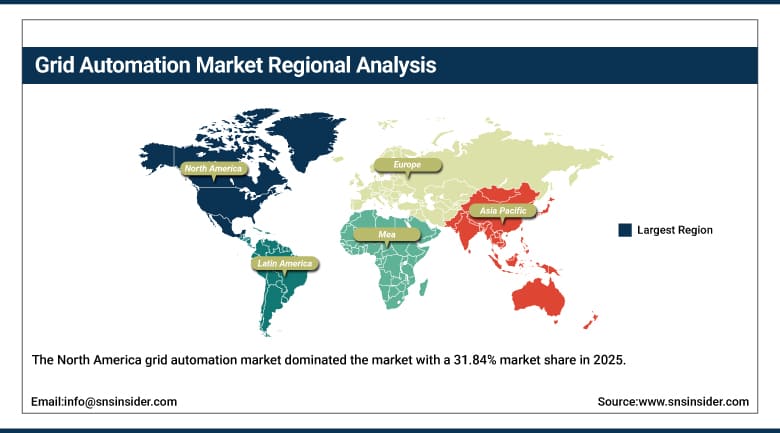

The North America grid automation market dominated the market with a 31.84% market share in 2025. This growth is due to major investments in grid modernization and the renewal of the old transmission and distribution systems. The utilities located in the US and Canada are installing sophisticated automation systems in order to enhance the reliability of the grid, decrease the downtime, and increase the grid resiliency in terms of extreme weather conditions. Moreover, government incentives and high capital spending on the development of the smart grids are encouraging the penetration of the intelligent grid monitoring and control systems.

Renewable energy sources installation and the growth of electricity consumption from the data center and electric vehicles are boosting the market demand. In addition, utilities are actively investing in distribution management systems, digital substations, and grid analytics in order to manage the power flow and enable the distributed energy sources.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Grid Automation Market Insights

The Europe grid automation market is fueled by the energy transition that is taking place aggressively in the region. The installation of smart grids is receiving significant investments to integrate renewable energy into the grid and improve energy efficiency. Digital substations, sophisticated monitoring, and intelligent grid control solutions are being deployed on an extensive scale as the countries are modernizing their electricity grids for the generation of sustainable electricity.

Cross-border electricity transactions and development of distributed energy sources are further adding fuel to the fire of demand for grid automation solutions. Advanced automation systems are required by the utilities to increase the flexibility of their grids and optimize power transmission and distribution.

Asia Pacific Grid Automation Market Insights

The Asia Pacific grid automation market is expected to be the fastest growing with a CAGR 10.89% in 2025. It is mainly propelled by fast urbanization, industrialization, and growing need for electricity in the major countries of the region including China and India. The government is making significant investments in upgrading the infrastructure of power transmission and distribution to meet the growing requirement of electricity. Smart city developments and grid automation projects are playing a major role in accelerating the growth of this market.

Renewable energy and distributed generation developments are another important factor responsible for the growth of this market in the region. Utilities in the region are implementing grid automation technology for managing the power generation and performance improvement of the grid as well as development of electric vehicle infrastructure.

Middle East & Africa and Latin America Grid Automation Market Insights

Growth in grid automation technologies in Middle East & Africa and Latin America is expected due to growing investments in power infrastructure upgradation and electricity grids. Various governments and utilities in these two geographical areas have plans for upgrading existing power grids and networks through the installation of smart technologies. These upgrades are mainly meant for improving the efficiency, reliability, and reduction in technical losses in the power grid. In addition, various smart city initiatives and rural electrification are contributing towards market growth.

Increasing adoption of renewable energy generation projects and emphasis on energy diversification in these regions is adding to the growth of the market. Growing number of grid automation technologies in these regions has made it possible to easily integrate solar power plants and other types of renewable energy sources into the grids without any disruption. Increased investments in clean energy infrastructure and initiatives for ensuring energy security and grid resilience in these two regions have created huge potential for grid automation technologies.

Market Dynamics:

Growth Drivers: Increasing Grid Modernization, Renewable Energy Integration, and Digital Infrastructure Investments Driving Market Growth

The increase in investments in the modernization of the grid system and the installation of new power infrastructures is contributing immensely to the rise in the adoption of grid automation. Many utilities have been investing in automated systems to boost their efficiencies by ensuring reliability and minimizing blackouts. At the same time, the increased inclusion of renewable energy sources and distributed energy resources in the grid system has complicated the grid structure and increased the need for grid automation systems.

The increase in the consumption of electricity due to urbanization, industrialization, and electrification projects has made many utilities invest in smart grid systems around the world. Utilities have been using advanced automation systems in order to improve power quality and boost efficiency. At the same time, the expansion of electric vehicles charging stations and data centers has made utilities need grid automation.

Restraints: High Capital Requirements and Growing Cybersecurity Challenges Restricting Grid Automation Adoption

The use of grid automation systems involves significant investment in technology, networks, and software platforms. Many utility companies, especially those operating in developing countries, have financial limitations that would hinder them from implementing large-scale automation in their operations. In addition, the integration of contemporary automation systems with the existing legacy systems is complicated and costly due to the extensive modifications involved.

The increasing digitalization of electrical systems has greatly increased the potential of cyberattacks on utility networks. The grid automation systems involve interconnecting systems and use of communication platforms, and are thus very susceptible to cyber attacks, data thefts, and operational disturbances. Hence, utility companies must invest a lot in cybersecurity issues in order to implement automation projects.

Opportunities: Rising Distributed Energy Resources and Artificial Intelligence Creating New Market Opportunities

The increasing adoption of distributed energy sources such as rooftop solar installations, battery energy storage systems, and microgrids has led to considerable opportunities for grid automation solutions. Utility companies need sophisticated automation systems to effectively handle bidirectional power flows, provide stability within the grid system, and enhance their distributed generation resources. More funding in decentralized energy systems and intelligent energy management systems is expected to create huge demand for intelligent grid automation systems.

The integration of artificial intelligence, cloud computing, and analytics within utilities has also opened up more growth opportunities for the Grid Automation Market. The use of AI platforms by utilities companies for predictive maintenance and asset management is becoming common among many companies. Cloud automation systems give utility companies more grid monitoring ability, enabling them to enhance their operation efficiency, lower downtime, and move towards digital and smart grids.

Recent Developments:

-

2024: Hitachi Energy launched new digital substation and grid-edge solutions integrating advanced automation, real-time analytics, and cybersecurity capabilities to support renewable energy integration and improve utility operational efficiency across modern electricity networks.

-

2025: Siemens Smart Infrastructure expanded its Gridscale X digital portfolio with advanced software applications for distribution management, outage management, and grid analytics, enabling utilities to accelerate digital transformation and support increasing distributed energy resources.

-

2026: GE Vernova Inc. launched GridBeats APS (Automation and Protection System), a new addition to its GridBeats software-defined grid automation portfolio. The solution is designed to simplify grid operations and protection, modernize electrical substations, reduce device footprints, and improve grid reliability as electricity networks expand and become increasingly complex, supporting utilities in managing evolving power system requirements efficiently.

Grid Automation Market key players are:

-

ABB Ltd.

-

Siemens AG

-

GE Vernova Inc.

-

Schneider Electric SE

-

Hitachi Energy Ltd.

-

Eaton Corporation plc

-

Honeywell International Inc.

-

Emerson Electric Co.

-

Cisco Systems, Inc.

-

Mitsubishi Electric Corporation

-

Toshiba Energy Systems & Solutions Corporation

-

Rockwell Automation, Inc.

-

Schweitzer Engineering Laboratories, Inc. (SEL)

-

Landis+Gyr Group AG

-

Itron, Inc.

-

S&C Electric Company

-

Fuji Electric Co., Ltd.

-

Oracle Corporation

-

Huawei Technologies Co., Ltd.

-

WAGO GmbH & Co. KG

Grid Automation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 43.10 Billion |

| Market Size by 2035 | USD 105.14 Billion |

| CAGR | CAGR of 9.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Automation Type (Substation Automation, Distribution Automation, Generation Automation, Transmission Automation) • By Utility Type (Electric Utilities, Water Utilities, Gas Utilities) • By Deployment Mode (On-Premise, Cloud-Based) • By End User (Public Utilities, Independent Power Producers (IPPs), Industrial & Commercial Facilities, Renewable Energy Developers, Transmission System Operators (TSOs), Distribution System Operators (DSOs)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB Ltd., Siemens AG, GE Vernova Inc., Schneider Electric SE, Hitachi Energy Ltd., Eaton Corporation plc, Honeywell International Inc., Emerson Electric Co., Cisco Systems, Inc., Mitsubishi Electric Corporation, Toshiba Energy Systems & Solutions Corporation, Rockwell Automation, Inc., Schweitzer Engineering Laboratories, Inc. (SEL), Landis+Gyr Group AG, Itron, Inc., S&C Electric Company, Fuji Electric Co., Ltd., Oracle Corporation, Huawei Technologies Co., Ltd., WAGO GmbH & Co. KG. |

Frequently Asked Questions

The Grid Automation Market is expected to grow at a CAGR of 9.39% from 2026 to 2035.

The Grid Automation Market was valued at USD 43.10 billion in 2025.

The major growth factor driving the Grid Automation Market is increasing investments in grid modernization and renewable energy integration, requiring advanced automation for reliable and efficient power management.

The on-premise dominated the Grid Automation Market in 2025.

North America dominated the Grid Automation Market in 2025.

Get in Touch