Health Data Liquidity Platforms Market Report Scope & Overview

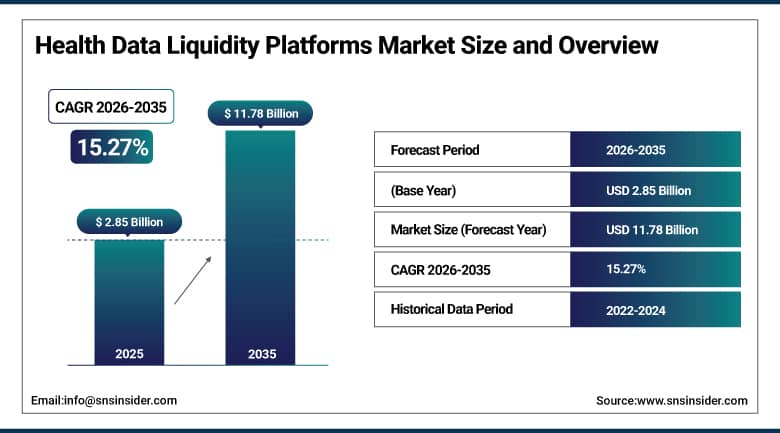

The Health Data Liquidity Platforms Market was valued at USD 2.85 Billion in 2025 and is expected to reach USD 11.78 Billion by 2035, growing at a CAGR of 15.27% from 2026 to 2035.

Market for Health Data Liquidity Platforms is flourishing owing to the fast-paced digital evolution of healthcare IT infrastructure along with the focus being laid on interoperability and data-centric care delivery. The rising adoption of cloud-based data platforms by hospitals and clinics is making it possible to bring together disparate clinical, administrative, and financial datasets, thereby enabling the transfer of data securely and in real time. The emergence of value-based care models, increasing need for population health management, and use of artificial intelligence technologies are driving the market growth for health data liquidity platforms.

In March 2025, Oracle Health added to its healthcare interoperability cloud solutions with the launch of more advanced AI-driven clinical data integration solutions designed to improve real-time sharing of patient information across healthcare networks. In January 2025, Microsoft announced new generative AI and cloud data platform solutions for healthcare that sought to improve interoperability, analytics and secure health information exchange

Market Size and Forecast:

-

Market Size in 2026E: USD 3.28 Billion

-

Market Size by 2035: USD 11.78 Billion

-

CAGR: 15.27% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Health Data Liquidity Platforms Market - Request Free Sample Report

Market Trends:

-

Interoperability mandates and data standardization are accelerating real-time health data exchange across healthcare ecosystems.

-

Cloud-native platforms and API-driven systems are improving integration of fragmented electronic health records.

-

AI and advanced analytics adoption is enhancing predictive insights and clinical decision-making capabilities.

-

Value-based care models are increasing demand for real-time, patient-centric data liquidity solutions.

U.S. Health Data Liquidity Platforms Market Outlook:

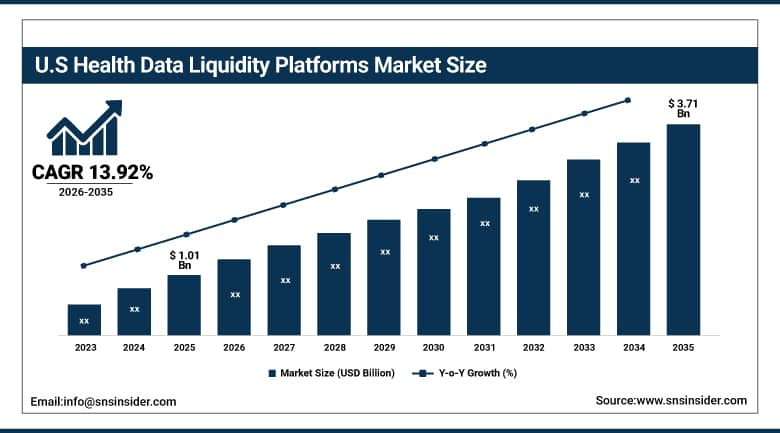

The U.S. Health Data Liquidity Platforms Market was valued at approximately USD 1.01 Billion in 2025 and is expected to reach approximately USD 3.71 Billion by 2035, growing at a CAGR of approximately 13.92% from 2026 to 2035.

US Health Data Liquidity Service The market growth is driven by strong federal interoperability mandates, rapid expansion of cloud-based healthcare infrastructure and increasing adoption of electronic health records across integrated healthcare systems. Real-time, secure and standardized exchange of patient data between providers, payers and life sciences organizations is also a need driven by the shift to value-based care. The increasing investments in AI-enabled healthcare analytics and API-based data architectures are also further strengthening the foundation for scalable health data liquidity ecosystems across the country.

Epic Systems in 2025 announced improvements to its interoperability network that would allow for more sophisticated FHIR-based integration capabilities for sharing electronic health record data across hospitals. In 2025, Oracle Health added AI-enabled clinical data exchange capabilities to its cloud healthcare platform to improve real-time liquidity of health information across provider networks and enterprise healthcare systems.

Health Data Liquidity Platforms Market Segment Analysis:

-

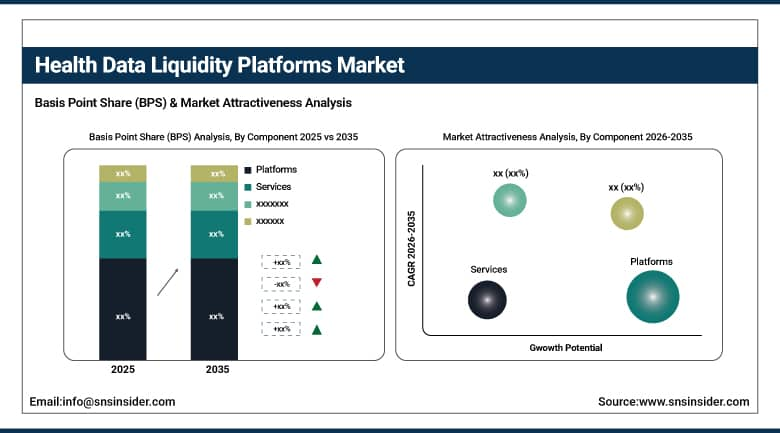

By Component, platforms dominated the health data liquidity platforms market with 44.00% share in 2025, while services are the fastest growing component segment from 2026 to 2035.

-

By Deployment Mode, cloud-based solutions dominated the health data liquidity platforms market with 57.00% share in 2025, while hybrid deployment is the fastest growing deployment segment from 2026 to 2035.

-

By Application, clinical data exchange dominated the health data liquidity platforms market with 41.00% share in 2025, while clinical research & analytics is the fastest growing application segment from 2026 to 2035.

-

By End User, healthcare providers dominated the health data liquidity platforms market with 38.00% share in 2025, while pharmaceutical & life sciences companies are the fastest growing end-user segment from 2026 to 2035.

By Component, platforms dominate, services grow fastest

Platforms dominated the health data liquidity platforms market with 44.00% share in 2025. Driven by their fundamental role of enabling interoperability, real-time healthcare data exchange and unified integration across disparate health IT systems. These platforms represent the foundational infrastructure layer that connects electronic health records, payer systems and life sciences databases. Strong adoption is driven by increasing demand for cloud-native architectures, API-based connectivity and scalable data management solutions that would allow seamless flow of information across healthcare ecosystems across the globe.

Services are expected to witness the fastest CAGR during the forecast period of 2026–2035.This growth is being powered by increasing demand for solutions that can be implemented in conjunction with data governance and integration support, including managed interoperability services. In the process of adopting new technologies and implementing new digital health platforms, it becomes increasingly important to ensure that organizations adopt these solutions securely and optimize their use. Complexity of modern healthcare data environments and increasing outsourcing of IT and interoperability needs add to the problem.

By Deployment Mode, cloud-based dominates, hybrid grows fastest

Cloud-based deployment dominated the market with 57.00% share in 2025, enabled by adoption of scalable, cost-efficient, and interoperable healthcare IT infrastructure. Cloud platforms enable hospitals, payers, and research organizations to exchange data in real-time while increasing the accessibility, storage, and analytics. The growing adoption of remote healthcare delivery, AI-driven analytics and centralized data management is continuing to boost the dominance of cloud deployment across global healthcare systems.

Hybrid deployment is expected to witness the fastest CAGR during the forecast period of 2026–2035.The reason behind the growth is the capability of maintaining a balance between regulatory compliance, data security, and flexibility in operations. “Organizations are opting for hybrid models, retaining their patients’ data on-premise but using cloud computing for analysis and other purposes.” It helps them with issues around digital transformation and regulatory compliance.

By Application, clinical data exchange dominates, clinical research & analytics grow fastest

Clinical data exchange dominated the market with 41.00% share in 2025, driven by the growing need to share patient data seamlessly and in a standardized way across healthcare providers, hospitals and integrated delivery networks. It gives immediate access to the patient’s records, allowing for better coordination of care, less duplication of diagnostic tests and faster clinical decisions. Its leadership position is further solidified by increasing interoperability mandates and digital health transformation initiatives.

Clinical research & analytics is expected to witness the fastest CAGR during the forecast period of 2026–2035.Growth will come from increased usage of AI-enabled research technology, evidence-based learning, and precision medicines. There has been an increase in the use of data liquidity platform capabilities among pharmaceutical firms and research organizations to tap into extensive datasets on patients. The increased investments in innovative data-based healthcare solutions have resulted in increased demand for analytics.

By End User, healthcare providers dominate, biopharmaceutical companies grow fastest

Healthcare providers dominated the market with 38.00% share in 2025. Backed up by robust utilization of interoperability platforms for managing patients’ information, optimizing workflow, and coordinating care processes. More hospitals and integrated healthcare systems are now implementing data liquidity solutions to increase efficiencies and effectiveness in their operations, and to improve patients’ outcomes by accessing consolidated information.

Biopharmaceutical companies are expected to witness the fastest CAGR during the forecast period of 2026–2035. The growth in the market can be attributed to the increasing adoption of data-driven approaches for R&D purposes such as greater emphasis on the use of real-world evidence, use of artificial intelligence in drug discovery, and improved clinical trials. The firms are using the health data liquidity platforms to utilize patient datasets effectively.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.0% |

|

Europe |

Germany |

22.6% |

|

Asia Pacific |

China |

44.2% |

|

Middle East & Africa |

UAE |

24.1% |

|

Latin America |

Brazil |

42.9% |

North America Health Data Liquidity Platforms Market Insights

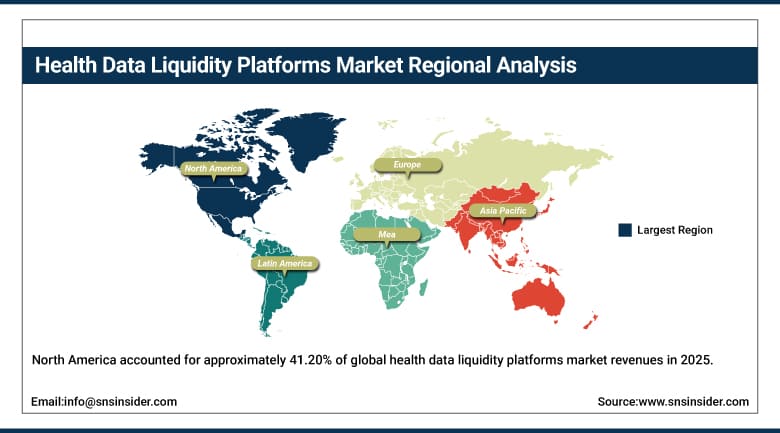

North America accounted for approximately 41.20% of global health data liquidity platforms market revenues in 2025.North America is dominating the global market due to the presence of highly advanced healthcare IT infrastructure, high adoption of electronic health record, and strong penetration of cloud-based interoperability platform. The United States is ahead in regional growth, with large-scale deployment of AI-enabled healthcare analytics, API-driven data exchange systems, and value-based care models that depend on real-time access to patient data. Large healthcare entities, payers and life sciences companies are investing in integrated data ecosystems to reduce fragmentation, improve care coordination and enable more efficient clinical decision-making across the healthcare value chain.

Canada is part of the regional expansion with ongoing efforts in digital health modernization, provincial EHR integration programmers and greater adoption of cloud-based healthcare platforms. Mexico is gradually upgrading its healthcare digital infrastructure, with growing investments in hospital digitization and interoperable health information systems. North America’s leadership in the global Health Data Liquidity Platforms Market is further reinforced by the increasing need for cross-border healthcare data exchange and the rising collaboration between public and private healthcare stakeholders.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Health Data Liquidity Platforms Market Insights

Europe accounted for approximately 27.80% of global health data liquidity platforms market revenues in 2025.The growth of the market in Europe is driven by presence of strong regulations such as GDPR, well-established public healthcare systems, and increasing adoption of standardized digital health infrastructure across member countries. Germany dominates the regional market owing to strong hospital IT modernization, increasing deployment of cloud-based interoperability platforms, and expanding healthcare data integration initiatives. Countries such as the UK and France are investing heavily in national health data networks and cross-border interoperability systems to enhance patient data accessibility and healthcare coordination.

The region is also witnessing an increasing adoption of AI-enabled healthcare analytics, increased adoption of electronic health records, and ambitious government-led digital health transformation programmers. The rising emphasis on secure, compliant and standardized health data exchange frameworks continues to boost the platform adoption within hospitals, clinics and public health institutions, strengthening Europe’s position in the global Health Data Liquidity Platforms Market.

Asia Pacific Health Data Liquidity Platforms Market Insights

Asia Pacific accounted for approximately 31.64% of global health data liquidity platforms market revenues in 2025. Asia Pacific is one of the fastest-growing regions, driven by rapid healthcare digitalization, expanding cloud infrastructure and large-scale government investments in health IT modernization. China is the market leader in the region with strong hospital digitization programmers, growing adoption of AI-enabled healthcare platforms, and rapid deployment of interoperable electronic health record systems. Public and private healthcare providers are adopting platforms in response to the growing need for integrated healthcare data ecosystems.

India, Japan and South Korea are also providing significant contributions through national digital health missions, smart hospital initiatives and increasing investment in healthcare data interoperability solutions. This, along with the increasing partnership between global technology vendors and regional healthcare systems, increasing focus on population health management and increase in telemedicine is further strengthening the position of Asia Pacific as the fastest growing regional market for the forecast period.

Middle East & Africa & Latin America Health Data Liquidity Platforms Market Insights

The Middle East & Africa and Latin America collectively accounted for approximately 10.73% of global health data liquidity platforms market revenues in 2025. The region is gradually adopting digital health and data interoperability solutions as healthcare systems modernize and invest in cloud-based healthcare infrastructure. The growing awareness of data-driven healthcare delivery, expanding hospital digitization programmers, and increasing government-led digital health initiatives in countries such as Brazil, Mexico, the UAE, and Saudi Arabia are supporting the integration of health data liquidity platforms across emerging healthcare ecosystems.

Middle East & Africa and Latin America markets are growing owing to increasing investments in healthcare digital transformation, expanding adoption of electronic health records and rising implementation of interoperable data exchange systems across hospitals and healthcare networks. More and more healthcare providers across a region are using cloud-enabled platforms to make patient data more accessible and to coordinate care. These data-driven healthcare digital transformation investments across these regions exceeded USD 4 billion in 2025, supporting smart hospital infrastructure and data integration systems expansion. Brazil is still the most advanced adopter in Latin America, while the UAE is making fast progress in the Middle East with major investments in AI-enabled healthcare ecosystems and national health data platforms.

Market Dynamics:

Growth Drivers: Rising regenerative medicine adoption and stem cell therapy research

The health data liquidity platforms market is expanding on account of increasing demand for seamless interoperability across fragmented healthcare systems and need for real-time clinical data access. Healthcare providers, payers and life sciences organizations are increasingly adopting cloud-based data liquidity platforms that bring electronic health records, administrative systems and analytics tools into unified ecosystems. Also, the move to value-based care models is rapidly driving demand for accurate, timely, and connected patient data to boost outcomes and reduce healthcare inefficiencies.

Increasing adoption of AI-based healthcare analytics, growing digital health infrastructure and robust regulatory support for standardized data exchange frameworks such as FHIR are key factors driving growth in the market. Increasing investments in healthcare IT modernization by leading providers and governments, are also supporting the deployment of scalable interoperability solutions. Moreover, the increasing demand for population health management and predictive analytics is further strengthening the need for advanced health data liquidity platforms across the globe.

Restraints: Data privacy concerns and high complexity of healthcare system integration

The market is hindered by stringent data privacy laws, cybersecurity concerns and integration of fragmented legacy healthcare systems. Interoperability gaps between multiple electronic health record platforms impede smooth data sharing and slow adoption. HIPAA, GDPR and other regional regulations compliance increases operational complexity & cost burdens thereby limiting scalability across healthcare organizations.

High deployment cost, lack of standardized data formats, and reluctance to digital transformation further hinder the growth of the market. Secure connectivity, data governance and keeping data accurate across stakeholders are just some of the challenges many healthcare providers face. These challenges are significant barriers especially for small and medium sized healthcare facilities and developing healthcare markets.

Opportunities: Expansion of AI-driven healthcare analytics and global digital health transformation

The market is expected to be driven by the rising adoption of AI, machine learning, and predictive analytics for healthcare data systems. These technologies enhance clinical decision-making, diagnostics and patient outcomes. As demand for precision medicine rises and the need for real-world evidence generation increases, global ecosystems are presenting increasing opportunities for data-driven healthcare innovation.

Fast digital health transformation, increased cloud adoption, and API-based interoperability frameworks are fueling an acceleration of market growth. Healthcare organizations are building connected care networks that enable the seamless sharing of data across hospitals, labs and research institutions. Strategic partnerships between health tech companies and providers are also fueling innovation and commercialization of advanced health data liquidity platforms.

Recent Developments:

-

In February 2026, Onyx expanded its interoperability capabilities through the acquisition of InteropX, strengthening payer-provider data exchange and accelerating CMS-aligned electronic prior authorization workflows.

-

In February 2026, the AI Centre and deepc launched FLIP, an open-source federated learning interoperability platform enabling cross-institutional AI collaboration while keeping patient data localized.

-

In November 2025, Greenlight Health Data Solutions launched its Intelligent Health Data Platform, integrating EHR connectivity, real-world data collection, and AI-ready analytics across life sciences and healthcare systems.

-

In October 2025, Rhapsody launched API Guardian, a healthcare API management platform designed to unify FHIR, HL7, and custom APIs for secure, AI-ready healthcare interoperability.

Health Data Liquidity Platforms Market Key Players are:

-

Epic Systems Corporation

-

Oracle Health

-

Microsoft Corporation

-

Google Cloud

-

Salesforce Inc.

-

InterSystems Corporation

-

IBM Corporation

-

Amazon Web Services

-

Snowflake Inc.

-

Health Gorilla

-

Redox Inc.

-

Rhapsody

-

Availity LLC

-

Veradigm Inc.

-

Datavant Inc.

-

Health Catalyst Inc.

-

Particle Health

-

1upHealth Inc.

-

Innovaccer Inc.

-

Komodo Health Inc.

Health Data Liquidity Platforms Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.85 Billion |

| Market Size by 2035 | USD 11.78 Billion |

| CAGR | CAGR of 15.27% from 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Platforms, Solutions, Services) • By Deployment Mode (Cloud-based, On-premise, Hybrid) • By Application (Clinical Data Exchange, Population Health Management, Revenue Cycle Management, Care Coordination, Clinical Research & Analytics) • By End User (Healthcare Providers, Healthcare Payers, Pharmaceutical & Life Sciences Companies, Government & Public Health Agencies, Health Information Exchanges) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Epic Systems Corporation, Oracle Health, Microsoft Corporation, Google Cloud (Google Health), Amazon Web Services (AWS), IBM Corporation, Salesforce Inc., InterSystems Corporation, Snowflake Inc., Health Gorilla, Redox Inc., Rhapsody, Availity LLC, Veradigm Inc., Datavant Inc., Health Catalyst Inc., Particle Health, 1upHealth Inc., Innovaccer Inc., Komodo Health Inc. |

Frequently Asked Questions

The Health Data Liquidity Platforms Market is expected to grow at a CAGR of approximately 15.27% during 2026–2035.

The Health Data Liquidity Platforms Market was valued at approximately USD 2.85 Billion in 2025, supported by rising investments in healthcare IT infrastructure and real-time data integration systems.

The major factor driving the market is the rising demand for seamless healthcare interoperability and real-time clinical data exchange, enabling better care coordination, improved patient outcomes, and efficient healthcare delivery.

Platforms dominated the market in 2025 due to their critical role in integrating fragmented healthcare data systems and enabling unified, real-time data exchange across providers, payers, and life sciences organizations.

North America dominated the market in 2025 due to advanced healthcare IT infrastructure, high adoption of electronic health records, strong regulatory support for interoperability, and large-scale deployment of cloud-based healthcare platforms.

Get in Touch