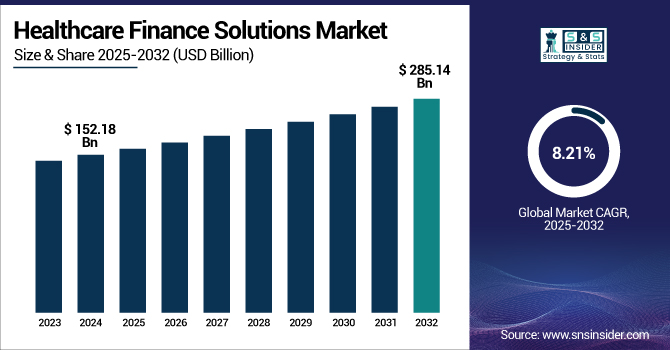

The Healthcare Finance Solutions Market size was valued at USD 152.18 billion in 2024 and is expected to reach USD 285.14 billion by 2032, growing at a CAGR of 8.21% over the forecast period of 2025-2032.

To Get more information on Healthcare Finance Solutions Market - Request Free Sample Report

The healthcare finance solutions market is growing rapidly owing to the growing healthcare spending, high demand for high-technology medical equipment, and an increase in the number of outpatient care centers.

The U.S. healthcare finance solutions market size was valued at USD 51.94 billion in 2024 and is expected to reach USD 95.54 billion by 2032, growing at a CAGR of 7.96% over the forecast period of 2025-2032. The U.S. maintains its lead in the North American healthcare finance solutions market in terms of share due to its sophisticated healthcare infrastructure, high capital expenditure on medical technology, and extensive use of financial services for equipment and facility growth. The availability of key financial providers and continuous digital transformation further enhances its leading position.

The increasing cost of chronic diseases in the U.S. is largely contributing to the expansion of the Healthcare Finance Solutions Market.

The CDC states that 6 out of 10 adults in the U.S. have at least one chronic condition, such as asthma, heart disease, or diabetes, requiring prolonged, intense, and often costly care. With nearly 90% of healthcare expenditures going toward treating chronic and mental illness, healthcare providers are facing pressure to invest in next-generation care delivery models, technologies, and infrastructure to deal with these intricate needs. This presents an expanding need for agile financial solutions to pay for everything from prescription medication management systems to home healthcare gear.

Furthermore, the increasing expense of health insurance premiums, which increased by 42% over the last decade, highlights the larger economic burden on individuals and healthcare providers alike. The imperative for enhanced access to care, cost-effectiveness, and operational resilience is leading providers to seek out structured financing solutions. Some of these involve equipment leasing, project financing, and working capital options, allowing providers to invest in chronic care management platforms, digital health platforms, and patient support initiatives without overusing internal funds, hence driving the healthcare finance solutions market globally.

Drivers:

Digital Transformation in Healthcare Driving the Market Growth

The digital transformation in healthcare is a key driver for the healthcare finance solutions market growth, as healthcare providers are increasingly embracing technologies such as electronic health records (EHRs), telemedicine platforms, artificial intelligence (AI), and machine learning (ML). These technologies demand high upfront investment in IT infrastructure, software, and data security systems. With healthcare organizations evolving to increase operational efficiency, better patient outcomes, and adapt to changing regulations, there is an increasing need for financing products to facilitate these digital improvements.

Rising Healthcare Expenditures Propel the Market Growth

One of the key drivers of the healthcare finance solutions market trends is the constant increase in global healthcare expenditure. With aging populations, increased rates of chronic diseases, and demands for new-fangled treatments, providers must meet the expenses of expensive medical devices, upgrading infrastructure, and technology. Such capital-intensive requirements tend to outweigh the available operating budgets of clinics, hospitals, and diagnostic centers. To fill this funding gap, healthcare suppliers are looking to specialized funding options, such as leasing, loans, and project-based finance, that provide more financial optionality, maintain cash flow, and facilitate the timely acquisition of necessary assets.

For instance, according American Medical Association,

Hospital and physician services were two of the biggest health spending categories between 2014 and 2023, with an average annual growth rate of 5.3% each. Clinical services and prescription medications, on the other hand, grew at average annual rates of 6.6% and 5.7%, respectively.

Personal health care spending increased by 9.4% in 2023, the largest annual growth since 1990. Hospital care increased by 10.4%, whereas prescription drug spending increased by 11.4%. Additionally, the growth rates for clinical services and physician services were 7.0% and 7.6%, respectively, which was a considerable rise over 2022.

Restraints:

Regulatory and Compliance Complexities Impede the Market Growth

One of the most important restraints in the healthcare finance solutions market analysis is the intricate and changing regulatory environment across various regions. Financial institutions and healthcare providers need to manage stringent compliance mandates around patient data protection, delivery of healthcare services, and standards for financial reporting. These complexities have the potential to delay approval for financing, restrict innovation in financial products, and raise operating expenses for lenders and borrowers alike. As regulations further constrict, particularly in surrounding digital health and cross-border transactions, market growth may be stifled, especially in developing markets with decreased regulatory certainty.

By Equipment Type

In 2023, the decontamination equipment segment dominated the healthcare finance solutions market by equipment type, with a 28.56% share in 2024, driven mainly by increased global awareness of infection control and hygiene in the wake of the COVID-19 pandemic. Hospital financial management solutions increased spending on sterilization equipment, washers, disinfectors, and supporting infrastructure to comply with tighter safety standards and regulatory compliance. Due to the significant initial investment in decontamination technologies, most providers resorted to financing options to balance budgets while maintaining compliance and patient safety, significantly fueling the demand for financial support in this segment.

The IT equipment segment is poised to witness the fastest growth rate during the forecast period driven by the continued digitalisation process in healthcare. Growing adoption of electronic health records (EHRs), telemedicine platforms, cybersecurity systems, and data analytics tools has created a pressing demand for IT infrastructure upgrades. Since these technologies involve high capital outlay and periodic upgrade expenses, healthcare providers are increasingly using financing models to implement and expand IT solutions cost-effectively, placing this segment in a rapid growth trajectory.

By Facility Type

In 2024, the hospitals & health systems segment dominated the healthcare finance solutions market share with 24.13% due to their enormous scale of operation needs, huge volumes of patients, and ongoing demand for cutting-edge medical technology. These institutions consistently undertake high-cost capital-intensive projects, including infrastructure upgrades, equipment purchases, and digitalization. As a result, hospitals and health systems are central purchasers of full-service financial solutions, such as project finance, equipment leasing, and corporate lending, solidifying their market leadership.

The outpatient surgery centres segment is projected to be the fastest-growing segment due to the international trend toward cost-saving and patient-focused care. Technological improvements in minimally invasive procedures, shorter recovery times, and positive reimbursement policies have boosted demand for ambulatory surgery services. To meet heightened patient expectations and expand service capacity, these centers are making investments in new technology and facility expansion, frequently with the help of flexible capital solutions, fueling aggressive growth in this segment during the forecast period.

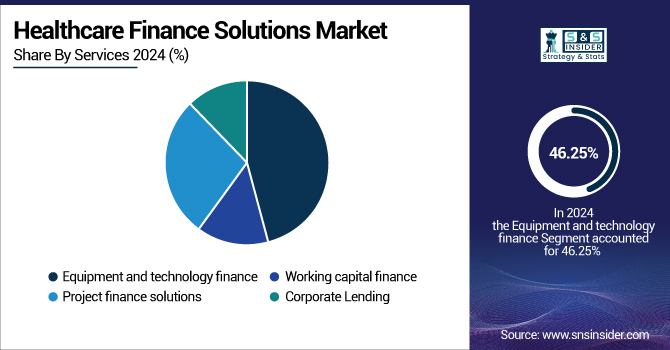

By Services

The equipment and technology finance segment dominated the healthcare finance solutions market in 2024 with a 46.25% share, primarily due to the ever-present demand for cutting-edge medical equipment in hospitals, imaging centers, and outpatient facilities. The capital-intensive purchases of diagnostic imaging equipment, surgical gear, and healthcare IT platforms pushed providers to seek structured financing solutions. Equipment financing offered flexibility, structured payment, and the ability to upgrade to new technologies. Therefore, it became the most used service among healthcare organizations that wanted to remain clinically competitive and operationally efficient.

The corporate lending segment will experience the most significant growth during the forecast period, fueled by growing demand for large-scale capital injections to finance mergers, acquisitions, expansions, and infrastructure growth. As healthcare systems diverge and converge, many organizations are using corporate loans to restructure debt, finance long-term strategic initiatives, and fund cash flow. Increasing collaboration between healthcare enterprises and financial institutions is also driving access to tailored corporate lending solutions, fostering growth in this segment.

Regional Analysis:

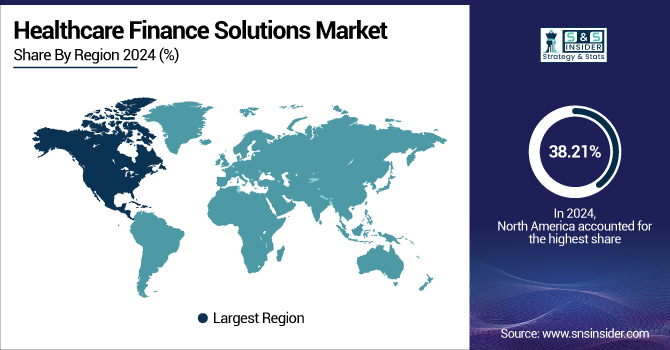

North America dominated the healthcare finance solutions market with a 38.21% share in 2024 due to its established healthcare infrastructure, large healthcare spending, and the prevalence of healthcare finance solutions companies with widespread coverage providing sophisticated financing solutions. The U.S., in particular, has a well-developed network of hospitals and outpatient care that often needs funding for upgrading diagnostic equipment, IT infrastructure, and facility expansion. Also, support from regulation of public-private partnerships, high use of digital health technologies, and robust reimbursement schemes help drive the high demand for tailored financial solutions.

For instance, according to NCBI, American hospitals are leading the digital revolution of healthcare, and other nations are only starting. For example, the United Kingdom has only recently encountered setbacks with its e-health programs, and Australian hospitals have just started to invest in the digitalization of their operations. At the level of the European Union, digital health is a key strategic priority, consistent with the European Strategic Plan 2019–2024 as presented by the European Commission.

Asia Pacific is expected to witness the fastest growth at 9.15% CAGR during the forecast period due to fast urbanization, growing healthcare investments, and an expanding middle class requiring better healthcare. China, India, and Southeast Asian countries are experiencing a boom in hospital construction, private clinic setup, and the use of the latest diagnostic tools, all demanding flexible financing solutions. Government programs to upgrade healthcare facilities and an increase in the involvement of international financial providers are driving market growth in this region.

Germany leads the European healthcare finance solutions market with its well-established healthcare infrastructure, robust public-private partnership, and significant healthcare expenditure. The country's strong healthcare network and continuous investment in the latest medical equipment drive demand for finance solutions to finance equipment purchasing, IT modernization, and infrastructure construction.

Europe's highly regulated yet pro-innovation finance system enables a variety of customized health financing structures. The availability of leading medical technology producers and specialized financial institutions further enhances its leadership role in the European market.

Latin America and the Middle East & Africa (MEA) regions are observing moderate growth in the healthcare finance solutions market during the short term. The growth is mainly attributed to the incremental enhancements in healthcare infrastructure, rising awareness regarding financial solutions, and expanding interest among private healthcare providers to update their facilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Market Players:

The key healthcare finance solutions companies are Siemens Financial Services, GE Healthcare Financial Services, McKesson Corporation, Oracle Corporation, Optum, Conifer Health Solutions, Change Healthcare, Cerner Corporation, First American Healthcare Finance, HealthCare Finance Direct, and other players.

August 2023 – McKesson Corporation, a diversified healthcare services leader, and Genpact, a global professional services company with expertise in digital transformation, announced the renewal of their strategic partnership. The new collaboration is designed to further transform McKesson's financial operations by applying automation and artificial intelligence (AI) to enhance efficiency and operational excellence.

October 2024 – Oracle Corporation announced significant new capabilities for its Oracle Health Data Intelligence platform. These new capabilities leverage the strong performance and security features of Oracle Cloud Infrastructure (OCI) and the most advanced artificial intelligence innovations available. The additions are intended to assist healthcare organizations with improving patient outcomes, optimizing financial results, and enriching data-driven decision-making across healthcare networks.

In 2025, GE HealthCare signed two long-term strategic enterprise agreements with Sutter Health in the U.S. and Nuffield Health in the U.K. The collaborations are designed to increase healthcare capacity, expand access to high-quality care, and drive growth for both GE HealthCare and customers. The announcement comes on the heels of a solid 2024, in which GE HealthCare launched approximately 40 innovations and signed more than 50 global strategic enterprise agreements, setting up a solid platform for future expansion.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 152.8 Billion |

| Market Size by 2032 | USD 285.14 Billion |

| CAGR | CAGR of 8.21% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Equipment Type (Diagnostic/Imaging Equipment, Specialist Beds, Surgical Instruments, Decontamination Equipment, IT Equipment) • By Facility Type (Hospitals & Health Systems, Outpatient Imaging Centres, Outpatient Surgery Centres, Physician Practices & Outpatient Clinics, Diagnostic Laboratories, Urgent Care Clinics, Skilled Nursing Facilities, Pharmacies, Other Healthcare Providers) • By Services (Equipment and Technology Finance, Working Capital Finance, Project Finance Solutions, Corporate Lending) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Siemens Financial Services, GE Healthcare Financial Services, McKesson Corporation, Oracle Corporation, Optum, Conifer Health Solutions, Change Healthcare, Cerner Corporation, First American Healthcare Finance, HealthCare Finance Direct, and other players. |

Ans: The Healthcare Finance Solutions Market is expected to grow at a CAGR of 8.21% from 2025-2032.

Ans: The Healthcare Finance Solutions Market was USD 152.18 billion in 2024 and is expected to reach USD 285.14 billion by 2032.

Ans: Digital transformation in healthcare is driving the market growth.

Ans: The “Hospitals & health systems” segment dominated the Healthcare Finance Solutions Market.

Ans: North America dominated the Healthcare Finance Solutions Market in 2024.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Capital Expenditure Trends in Healthcare (2024)

5.2 Financing Utilization by Service Type (2024)

5.3 Healthcare Infrastructure Projects Funded, by Region (2024)

5.4 Healthcare Provider Credit Risk Index, by Region (2024)

5.5 Private vs. Public Sector Participation in Healthcare Financing (2024)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new Product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Healthcare Finance Solutions Market Segmentation By Facility Type

7.1 Chapter Overview

7.2 Healthcare Finance Solutions

7.2.1 Healthcare Finance Solutions Market Trends Analysis (2021-2032)

7.2.2 Healthcare Finance Solutions Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Outpatient imaging centres

7.3.1 Outpatient imaging centres Market Trends Analysis (2021-2032)

7.3.2 Outpatient imaging centres Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Outpatient surgery centres

7.4.1 Outpatient Surgery Centres Market Trends Analysis (2021-2032)

7.4.2 Outpatient Surgery Centres Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Decontamination equipment

7.5.1 Decontamination equipment Market Trends Analysis (2021-2032)

7.5.2 Decontamination equipment Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 Physician practices & outpatient clinics

7.6.1 Physician practices & outpatient clinics Market Trends Analysis (2021-2032)

7.6.2 Physician practices & outpatient clinics Market Size Estimates and Forecasts to 2032 (USD Billion)

7.7 Diagnostic laboratories

7.7.1 Diagnostic laboratories Market Trends Analysis (2021-2032)

7.7.2 Diagnostic laboratories Market Size Estimates and Forecasts to 2032 (USD Billion)

7.8 Physician practices & outpatient clinics

7.8.1 Physician practices & outpatient clinics Market Trends Analysis (2021-2032)

7.8.2 Physician practices & outpatient clinics Market Size Estimates and Forecasts to 2032 (USD Billion)

7.9 Urgent care clinics

7.9.1 Urgent Care Clinics Market Trends Analysis (2021-2032)

7.9.2 Urgent Care Clinics Market Size Estimates and Forecasts to 2032 (USD Billion)

7.10 Skilled nursing facilities

7.10.1 Skilled nursing facilities Market Trends Analysis (2021-2032)

7.10.2 Skilled nursing facilities Market Size Estimates and Forecasts to 2032 (USD Billion)

7.10 Pharmacies

7.10.1 Pharmacies Market Trends Analysis (2021-2032)

7.10.2 Pharmacies Market Size Estimates and Forecasts to 2032 (USD Billion)

7.10 Other healthcare providers

7.10.1 Other healthcare providers Market Trends Analysis (2021-2032)

7.10.2 Other healthcare providers Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Healthcare Finance Solutions Market Segmentation By Equipment Type

8.1 Chapter Overview

8.2 Diagnostic/Imaging equipment

8.2.1 Diagnostic/Imaging equipment Market Trend Analysis (2021-2032)

8.2.2 Diagnostic/Imaging equipment Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Specialist beds

8.3.1 Specialist beds Market Trends Analysis (2021-2032)

8.3.2 Specialist beds Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Surgical instruments

8.4.1 Surgical instruments Market Trends Analysis (2021-2032)

8.4.2 Surgical instruments Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Decontamination equipment

8.5.1 Decontamination equipment Market Trends Analysis (2021-2032)

8.5.2 Decontamination equipment Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 IT equipment

8.6.1 IT equipment Market Trends Analysis (2021-2032)

8.6.2 IT equipment Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Healthcare Finance Solutions Market Segmentation By Services

9.1 Chapter Overview

9.2 Equipment and technology finance

9.2.1 Equipment and technology finance Market Trends Analysis (2021-2032)

9.2.2 Equipment and technology finance Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Working capital finance

9.3.1 Working Capital Finance Market Trends Analysis (2021-2032)

9.3.2 Working Capital Finance Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Project finance solutions

9.5.1 Project finance solutions Market Trends Analysis (2021-2032)

9.5.2 Project finance solutions Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Corporate lending

9.6.1 Corporate Lending Market Trends Analysis (2021-2032)

9.6.2 Corporate Lending Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Healthcare Finance Solutions Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.2.3 North America Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.2.4 North America Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.2.5 North America Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.2.6.2 USA Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.2.6.3 USA Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.2.7.2 Canada Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.2.7.3 Canada Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.2.8.2 Mexico Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.2.8.3 Mexico Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3 Europe

10.3.1 Trends Analysis

10.3.2 Europe Healthcare Finance Solutions Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.3.3 Europe Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.4 Europe Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.5 Europe Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3.6 Germany

10.3.6.1 Germany Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.6.2 Germany Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.6.3 Germany Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3.7 France

10.3.7.1 France Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.7.2 France Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.7.3 France Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3.8 UK

10.3.8.1 UK Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.8.2 UK Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.8.3 UK Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3.9 Italy

10.3.9.1 Italy Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.9.2 Italy Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.9.3 Italy Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3.10 Spain

10.3.10.1 Spain Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.10.2 Spain Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.10.3 Spain Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3.11 Poland

10.3.11.1 Poland Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.11.2 Poland Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.11.3 Poland Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3.12 Turkey

10.3.12.1 Turkey Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.12.2 Turkey Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.12.3 Turkey Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.3.13 Rest of Europe

10.3.13.1 Rest of Europe Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.3.13.2 Rest of Europe Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.3.13.3 Rest of Europe Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Healthcare Finance Solutions Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.4.3 Asia Pacific Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.4.4 Asia Pacific Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.4.5 Asia Pacific Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.4.6.2 China Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.4.6.3 China Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.4.7.2 India Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.4.7.3 India Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.4.8.2 Japan Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.4.8.3 Japan Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.4.9.2 South Korea Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.4.9.3 South Korea Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.4.10 Singapore

10.4.10.1 Singapore Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.4.10.2 Singapore Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.4.10.3 Singapore Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.4.11 Australia

10.4.11.1 Australia Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.4.11.2 Australia Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.4.11.3 Australia Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.4.12 Rest of Asia Pacific

10.4.12.1 Rest of Asia Pacific Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.4.12.2 Rest of Asia Pacific Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.4.12.3 Rest of Asia Pacific Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Trends Analysis

10.5.2 Middle East and Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.5.3 Middle East and Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.5.4 Middle East and Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.5.5 Middle East and Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.5.6 UAE

10.5.6.1 UAE Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.5.6.2 UAE Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.5.6.3 UAE Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.5.7 Saudi Arabia

10.5.7.1 Saudi Arabia Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.5.7.2 Saudi Arabia Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.5.7.3 Saudi Arabia Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.5.8 Qatar

10.5.8.1 Qatar Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.5.8.2 Qatar Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.5.8.3 Qatar Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.5.9 South Africa

10.5.9.1 South Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.5.9.2 South Africa Healthcare Finance Solutions Market Estimates and Forecasts by Equipment Type (2021-2032) (USD Billion)

10.5.9.3 South Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.5.10 Rest of Middle East & Africa

10.5.10.1 Rest of Middle East & Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.5.10.2 Rest of Middle East & Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.5.10.3 Rest of Middle East & Africa Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Healthcare Finance Solutions Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.6.3 Latin America Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.6.4 Latin America Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.6.5 Latin America Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.6.6.2 Brazil Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.6.6.3 Brazil Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.6.7.2 Argentina Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.6.7.3 Argentina Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

10.6.8 Rest of Latin America

10.6.8.1 Rest of Latin America Healthcare Finance Solutions Market Estimates and Forecasts, by Facility Type (2021-2032) (USD Billion)

10.6.8.2 Rest of Latin America Healthcare Finance Solutions Market Estimates and Forecasts, by Equipment Type (2021-2032) (USD Billion)

10.6.8.3 Rest of Latin America Healthcare Finance Solutions Market Estimates and Forecasts, by Services (2021-2032) (USD Billion)

11. Company Profiles

11.1 Siemens Financial Services

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Product/ Services Offered

11.1.4 SWOT Analysis

11.2 GE Healthcare Financial Services

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Product/ Services Offered

11.2.4 SWOT Analysis

11.3 McKesson Corporation

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Product/ Services Offered

11.3.4 SWOT Analysis

11.4 Oracle Corporation.

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Product/ Services Offered

11.4.4 SWOT Analysis

11.5 Optum,

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Product/ Services Offered

11.5.4 SWOT Analysis

11.6 Conifer Health Solutions

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Product/ Services Offered

11.6.4 SWOT Analysis

11.7 Change Healthcare

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Product/ Services Offered

11.7.4 SWOT Analysis

11.8 Cerner Corporation

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Product/ Services Offered

11.8.4 SWOT Analysis

11.9 First American Healthcare Finance

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Product/ Services Offered

11.9.4 SWOT Analysis

11.10 HealthCare Finance Direct.

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Product/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Equipment Type

By Facility Type

By Services

Request for Segment Customization as per your Business Requirement: https://www.snsinsider.com/enquiry/6968

Regional Coverage:

North America

Europe

Asia Pacific

Middle East & Africa

Latin America

Request for Country Level Research Report: https://www.snsinsider.com/enquiry/6968

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report: