Single-use Bioprocessing Market Report Scope & Overview:

To Get More Information on Single-use Bioprocessing Market - Request Sample Report

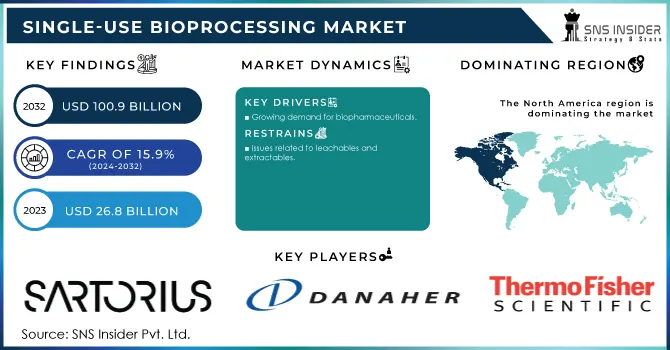

The Single-use Bioprocessing Market Size was valued at USD 26.8 Billion in 2023 and is expected to reach USD 100.9 Billion by 2032, growing at a CAGR of 15.9% over the forecast period 2024-2032.

Technological advancements, rising biologics demand, and government support are the factors behind the massive growth of the Single-use Bioprocessing Market. Biopharmaceuticals and biologics are becoming critical sectors for owned healthcare in multiple regions, and governments have begun to respond by investing in bioprocessing technologies. For example, in the United States, the NIH and BARDA have ramped up funding of biotechnology innovations. In 2023, NIH set aside an estimated $45 billion for medical research funding, which includes a significant amount for bioprocessing and drug development technologies like single-use systems. To contribute to this, an increased commitment has been made evident; it has helped create an environment that is widening the scope of the single-use bioprocessing market, which is perceived as a more feasible choice based on its cost-effectiveness, flexibility, and scalability over conventional stainless-steel systems.

The simplicity of single-use bioprocessing systems is another key factor driving their adoption. They provide more flexibility, reduced cleaning and sterilization, and shorter product development and manufacturing timelines. Consequently, the U.S. Food and Drug Administration (FDA) as well as the European Medicines Agency (EMA) as well have been instrumental in the implementation and adoption of single-use technologies in biologics manufacturing. In 2023, more than 40% of the worldwide bioprocessing market encompassed single-use systems, and increasing acceptance of single-use systems is likely to continue for the foreseeable future; aided by progressive regulatory frameworks and widespread technological advancements. Specifically, the rapid expansion of the oncology and autoimmune therapeutics sectors, supported by a growing innovation-led research base in many countries, is also driving the need for flexible, efficient, and cost-effective biomanufacturing solutions such as single-use systems. In April 2023, Merck KGaA introduced the Ultimus single-use process container film, offering superior durability and leak resistance for bioprocessing liquids. This innovation underscores the growing focus on enhancing the reliability and efficiency of single-use technologies, meeting the industry's demand for robust solutions in bioprocessing applications.

Market Dynamics

Drivers

-

The rise in biologics approvals, such as cancer therapies and vaccines, is fueling the demand for single-use bioreactors and associated technologies. This trend is expected to continue as biologics become more prevalent in treating complex diseases.

-

Governments, particularly in North America, are investing heavily in biomanufacturing, driving the demand for single-use bioprocessing technologies. This includes investments in vaccine production and therapeutic innovations, which benefit from disposable bioprocessing systems.

-

Single-use systems reduce operational costs by eliminating the need for cleaning and maintenance of traditional equipment. They also provide flexibility, making them ideal for fast-changing production requirements in biopharmaceuticals

The demand for biologics has been steadily increasing and this is expected to contribute to the growth of the single-use bioprocessing market by driving the adoption of disposable bioprocessing systems. The number of biologics approved by the global biopharmaceutical industry has exponentially risen, thanks to breakthroughs in precision medicine, gene therapy, and mRNA-based vaccines. For example, in 2023, the U.S. FDA approved Bioverativ Therapeutics' Altuviio, a factor VIII replacement therapy for hemophilia A, which highlights the growing demand for biologics. Additionally, the success of mRNA vaccines, like Moderna's Spikevax, has further fueled this trend.

Flexible and efficient manufacturing processes tailored to these biologics will be required to be implemented and single-use technologies are a good fit to be implemented to fulfill these requirements. The use of single-use bioreactors, filtration assemblies, and other disposable systems allows shorter production cycles and less cleaning and maintenance efforts. As a result, they are well suited to biologic drug manufacturers that are advancing their large-scale production of intricate therapies. Governments and organizations are also focusing on biomanufacturing infrastructure to realize this demand. In 2023, GBP 12 million was awarded to the UK Government's Future Vaccines Manufacturing Hub, to enhance vaccine manufacturing. This, combined with the increasing acceptance of biologics and related treatment solutions, is making certain a robust and stable demand for single-use bioprocessing options.

Restraints:

-

The disposable nature of single-use systems raises concerns about their environmental impact, especially in terms of waste generation.

-

Despite long-term cost savings, the high upfront cost of setting up single-use systems can be a barrier for smaller companies.

-

The complexity of regulatory requirements for single-use systems can slow adoption, particularly in emerging markets.

The single-use bioprocessing market has faced a key limitation in environmental issues associated with the waste produced by single-use systems. Bioreactors, filtration systems, and other single-use bioprocessing technologies are designed for one-off use, which means more plastic waste. This becomes a point of focus/concern especially today, as industries and regulators put a growing focus on sustainability and carbon footprint. Most of these systems are composed of plastics & other non-biodegradable materials which brings a question of eco-friendliness. This leads to increased loads on the waste pile as these commodities cannot be used again. Some companies are tackling this issue with new recyclable materials or more efficient waste management methodologies but environmental impact is still a core issue preventing adoption in environmentally focused markets.

Segment analysis

By Product

The simple and peripheral elements segment of the single-use bioprocessing market captured the largest market share of 48% in 2023. Such dominance stems largely from the growing usage of simple, off-the-shelf systems that offer a wide application space for biologics and vaccine production. Basic single-use items like bags, filters, and connectors play a critical role in minimizing the risk of cross-contamination and improving the process. The large-scale implementation of these machines in laboratories, pilot plants, and commercial-scale production facilities plays a major role in market dominance. Further, the proliferation of government-led programs for the economic alleviation of healthcare expenses and the availability of biologics has propelled the growth of this segment. As an example, the approval process for single-use components has been simplified and opened by the U.S. FDA which has made them more available and appealing to the biomanufacturers. Moreover, the immediate impact on single-use systems market dynamics resulting from the adoption of regulatory requirements on product quality assurance and modernization of regulatory framework for equipment used for bioprocessing by the FDA will foster the enhanced usage of incorporated and ancillary single-use components.

According to recent government reports, the number of FDA-approved biologics and biosimilars has grown significantly in recent years, with over 40 new biologics approved in 2023 alone, many utilizing single-use technologies in their production processes. The need for quicker and more efficient production methods of these biologics than previously has led manufacturers to use simpler systems with a faster turnover. Particularly connectors, tubing, and filtration peripherals pervade due to their broad applications and need for sterility and workstream scalability in bioprocessing applications.

By Workflow

The upstream bioprocessing segment accounted for the highest revenue share 45% in 2023, driven by the growing demand for biologics production and cell culture technologies. Upstream bioprocessing involves critical steps such as cell line development, media preparation, and fermentation, all of which benefit significantly from single-use systems due to their ability to reduce contamination risks, lower capital expenditure, and improve process efficiency. Government statistics underscore the growing demand for biologics and cell-based therapies, with reports from the U.S. Department of Health and Human Services indicating a rapid increase in funding for cell-based research and vaccine development, which drives demand for upstream bioprocessing solutions. More specifically, the boom in monoclonal antibody plus vaccine manufacturing was largely funded by the government like Operation Warp Speed) and largely through upstream processes, such as cell culture, where single-use systems show significant benefits relative to stainless-steel systems.

The U.S. FDA’s continuous support for innovation in biomanufacturing, through programs such as the Biomanufacturing Technology Initiative, has further encouraged the use of single-use systems in upstream processing. In 2023 the fund supported several initiatives to develop upstream bioprocessing (focused on early production stages) to accelerate the time it takes to get vaccines and other biological therapeutics into production. With the requirement for monoclonal antibodies and vaccines rising worldwide, the growing need for upstream processes plays a crucial market driver for the single-use systems used in monoclonal antibodies and vaccines applications.

By End-Use

The biopharmaceutical manufacturers held the largest market share 54% in 2023. The biopharma industry is primarily responsible for this dominance, with an increased focus on single-use technologies to manufacture biologics. The growing complexity of biologic drug development is driving biopharmaceutical manufacturers to adopt single-use systems for their attractive qualities of cost-effectiveness, speed, and flexibility to scale up production. The same trends are confirmed by government statistics, especially in markets like the U.S. where the biopharmaceutical industry has been the subject of massive government support. In 2023 the U.S. Food and Drug Administration (FDA) approved an unprecedented number of new biologics, most of which utilized single-use bioprocessing technologies for their production. The U.S. government has also sponsored efforts to lower biologics prices and broaden access to medicines, including incentives contained in the 21st Century Cures Act for implementing state-of-the-art manufacturing methods such as single-use systems.

Increasing demand for biosimilars in addition to the increasing incidence of chronic diseases such as cancer and autoimmune diseases, have cemented the biopharmaceutical sector’s requirement for flexible and scalable biomanufacturing solutions. Biopharmaceutical manufacturers benefit significantly from single-use systems as they enable faster product development cycles and more efficient manufacturing processes, reducing the time to market for new drugs and biologics. This shift in manufacturing strategy has been supported by regulatory bodies such as the FDA, which has streamlined the approval process for drugs produced using single-use systems.

Regional Insights

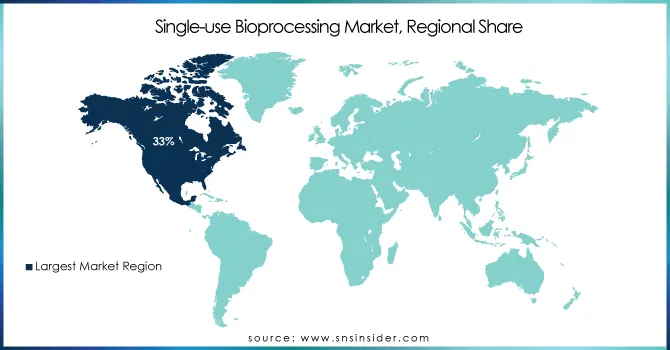

North America held the highest revenue share 33% of the single-use bioprocessing market in 2023. Several aspects, including the large presence of biopharmaceutical manufacturers, favourable research and development infrastructure, and conducive regulatory environments, underpin this region’s stronghold. Innovative biologics production initiatives in North America, especially those in the U.S., have benefitted from government initiatives such as the FDA’s new pathway for the approval of new biologic therapies and the National Institutes of Health funding bioprocessing research. Moreover, the U.S. government led by the government has played a leading role in promoting advanced manufacturing technologies like single-use bioprocessing systems through programs like the Advanced Manufacturing Initiative.

However, the Asia-Pacific region is expected to experience the fastest compound annual growth rate (CAGR) over the forecast period. Factors such as the rising adoption of biologics, development of healthcare infrastructure, and increasing government initiatives towards many biopharmaceutical sectors in countries like China and India, serve as the driving force for the Asia Pacific biopharmaceuticals contract manufacturing market. This has been supported by the governments of these countries who are also promoting the growth of the domestic pharmaceutical and biopharmaceutical industry, thereby driving increased demand for advanced manufacturing technologies (single-use). China's National Development and Reform Commission (NDRC) assented massive funds of their healthcare budget to the healthcare system and also development in life science, particularly biopharmaceutical reallocation in 2023.

Do You Need any Customization Research on Single-use Bioprocessing Market - Enquire Now

Recent Developments

-

AGC Biologics launched expansion plans for its Japan site in January 2024, adding mammalian cell culture, mRNA, and cell therapy capacity to support demand for biologics and advanced therapies.

-

In October 2023, GE Healthcare received FDA approval for its single-use bioprocessing platform designed for large-scale biologics manufacturing. This approval reflects the increasing regulatory confidence in single-use technologies and signals a shift toward larger-scale adoption in the biopharmaceutical industry.

Key Players

Service Providers / Manufacturers:

-

Thermo Fisher Scientific (HyPerforma Single-Use Bioreactors, BioProcess Containers)

-

Sartorius AG (Biostat STR Bioreactors, Flexsafe Bags)

-

Merck KGaA (Ultimus Film, Mobius Single-Use Systems)

-

Danaher Corporation (Xcellerex Bioreactors, Pall Allegro Systems)

-

GE Healthcare Life Sciences (Xcellerex XDR Bioreactors, WAVE Bioreactor Systems)

-

Eppendorf AG (BioBLU Single-Use Vessels, CelliGen BLU Bioreactors)

-

Corning Incorporated (HYPERStack Cell Culture Vessels, CellCube Modules)

-

Avantor, Inc. (J.T.Baker BPCs, Single-Use Mixer Systems)

-

Cellexus International (CellMaker Plus, CellMaker Regular)

-

Lonza Group AG (MODA-ES Bioprocess Software, Nunc Cell Factory Systems)

Key Users

-

Pfizer Inc.

-

Novartis AG

-

Amgen Inc.

-

Sanofi

-

Roche Holding AG

-

Eli Lilly and Company

-

Johnson & Johnson

-

Bristol-Myers Squibb

-

GlaxoSmithKline plc

-

Biogen Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 26.8 Billion |

| Market Size by 2032 | USD 100.9 Billion |

| CAGR | CAGR of 15.9% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Simple & Peripheral Elements {Tubing, Filters, Connectors, & Transfer Systems, Bags, Sampling Systems, Probes & Sensors, Others}, Apparatus & Plants {Bioreactors, Mixing, Storage, & Filling Systems, Filtration System, Chromatography Systems, Pumps, Others}, Work Equipment {Cell Culture System, Syringes, Others}) • By Workflow (Upstream Bioprocessing, Fermentation, Downstream Bioprocessing) • By End-use (Biopharmaceutical Manufacturers {CMOs & CROs, In-house Manufacturers}, Academic & Clinical Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific, Sartorius AG, Merck KGaA, Danaher Corporation, GE Healthcare Life Sciences, Eppendorf AG, Corning Incorporated, Avantor, Inc., Cellexus International, Lonza Group AG |

| Key Drivers | • The rise in biologics approvals, such as cancer therapies and vaccines, is fueling the demand for single-use bioreactors and associated technologies. This trend is expected to continue as biologics become more prevalent in treating complex diseases. • Governments, particularly in North America, are investing heavily in biomanufacturing, driving the demand for single-use bioprocessing technologies. This includes investments in vaccine production and therapeutic innovations, which benefit from disposable bioprocessing systems. |

| Restraints | • The disposable nature of single-use systems raises concerns about their environmental impact, especially in terms of waste generation. • Despite long-term cost savings, the high upfront cost of setting up single-use systems can be a barrier for smaller companies. |

Frequently Asked Questions

Ans:

- The disposable nature of single-use systems raises concerns about their environmental impact, especially in terms of waste generation?.

- Despite long-term cost savings, the high upfront cost of setting up single-use systems can be a barrier for smaller companies?.

Ans: Increasing demand from the biopharmaceutical industry and growing elderly population.

Ans: The North America region dominated the Single-use Bioprocessing Market in 2023.

Ans: The biopharmaceutical manufacturer's end-use segment dominated the Single-use Bioprocessing Market in 2023 with a 72% revenue share.

Ans: The CAGR of the Single-use Bioprocessing Market is 15.9% During the forecast period of 2024-2032.

Ans: The projected market size for the Single-use Bioprocessing Market is USD 100.9 billion by 2032.

Get in Touch