HIV Drugs Market Report Scope & Overview:

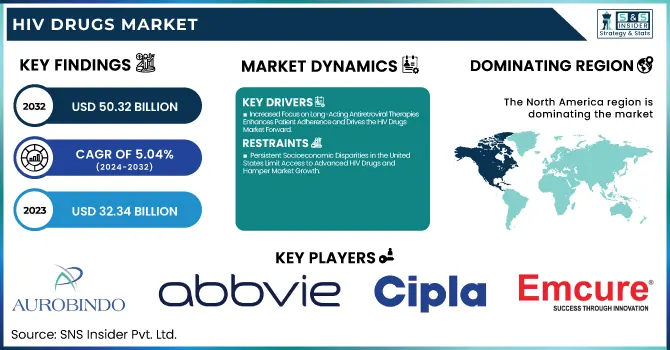

The HIV Drugs Market Size was valued at USD 32.34 Billion in 2023 and is expected to reach USD 50.32 Billion by 2032, growing at a CAGR of 5.04% over the forecast period of 2024-2032.

Get More Information on HIV Drugs Market - Request Sample Report

The HIV drugs market is undergoing a dynamic transformation fueled by innovation and global health efforts. Our report explores the pipeline of HIV drug candidates, revealing promising therapies poised to reshape treatment. It also examines treatment access in low-income countries, highlighting efforts to bridge healthcare gaps. Reimbursement policy comparisons by country shed light on affordability and patient access across diverse healthcare systems. The demographics of HIV drug users worldwide provide key insights into shifting demand, driven by age, gender, and regional factors. Rising adoption of pre-exposure prophylaxis (PrEP) underscores a proactive shift toward prevention. Together, these elements tell a story of a market evolving to meet global needs through scientific advancement, equitable access, and a focus on prevention.

The US HIV Drugs Market Size was valued at USD 14.63 Billion in 2023 with a market share of around 85% and growing at a significant CAGR over the forecast period of 2024-2032.

The US HIV drugs market remains one of the largest and most advanced globally, driven by robust R&D investments, strong regulatory support, and high treatment coverage. Growth is fueled by continuous innovation from companies like Gilead Sciences and Merck & Co., which have introduced long-acting therapies and combination treatments. The Centers for Disease Control and Prevention (CDC) and the U.S. President’s Emergency Plan for AIDS Relief (PEPFAR) support nationwide initiatives for early diagnosis and prevention, including rising uptake of PrEP. Favorable reimbursement policies through Medicaid and private insurers further boost accessibility, while a focus on ending the HIV epidemic by 2030 accelerates funding and public-private collaborations.

Market Dynamics

Drivers

-

Increased Focus on Long-Acting Antiretroviral Therapies Enhances Patient Adherence and Drives the HIV Drugs Market Forward

The emergence of long-acting antiretroviral therapies (ARTs) has significantly transformed the landscape of HIV treatment. Unlike traditional regimens that require daily oral dosing, long-acting injectable or implant-based solutions reduce the frequency of medication administration to once every month or even every two months. This development is crucial in improving patient adherence, minimizing the risk of drug resistance, and enhancing treatment outcomes. Companies such as ViiV Healthcare and Johnson & Johnson have pioneered this segment with drugs like Cabotegravir and Rilpivirine-based treatments. These innovations address a critical gap in HIV therapy treatment fatigue and non-compliance—especially among vulnerable populations such as the homeless, youth, and those suffering from mental health issues. Moreover, clinical studies in the United States funded by the National Institutes of Health (NIH) have demonstrated better viral suppression with long-acting therapies. As regulatory bodies like the U.S. Food and Drug Administration (FDA) continue to expedite the approval of these treatments, market penetration is expected to increase substantially. The convenience and privacy offered by these solutions also help reduce social stigma. Additionally, long-acting ARTs are proving effective in pre-exposure prophylaxis (PrEP), opening a dual-use advantage. As a result, the demand for long-acting therapies is not just reshaping clinical practice but also establishing a strong revenue-generating frontier, making it one of the key growth drivers in the evolving HIV drugs market.

Restraints

-

Persistent Socioeconomic Disparities in the United States Limit Access to Advanced HIV Drugs and Hamper Market Growth

Despite advancements in treatment, significant socioeconomic disparities in the United States continue to limit access to HIV medications, particularly among low-income, uninsured, and minority populations. Although public health programs like Medicaid and Ryan White HIV/AIDS Program aim to provide coverage, many patients still face financial barriers such as high co-pays, transportation costs, and inconsistent insurance coverage. These challenges are even more pronounced in Southern U.S. states, which have the highest HIV incidence rates but often the weakest public health infrastructures. The uneven expansion of Medicaid under the Affordable Care Act has also led to access gaps, with individuals in non-expansion states facing greater difficulty in obtaining antiretroviral therapy. Language barriers, fear of stigma, and lack of education further deter consistent treatment adherence. These factors not only prevent optimal health outcomes but also limit the market potential for pharmaceutical companies aiming to reach broader populations. In essence, while technological advancements continue, these social determinants of health pose a major restraint on the overall growth of the HIV drugs market.

Opportunities

-

Growing Integration of Telehealth Services for HIV Care Creates New Avenues for Drug Access and Market Penetration

The growing integration of telehealth in HIV care has opened new opportunities for expanding access to medications and improving patient management. Especially after the COVID-19 pandemic, telemedicine platforms in the United States have enabled remote diagnosis, counseling, and prescription renewals, reducing logistical and stigma-related barriers. Federally qualified health centers and private telehealth services now offer virtual consultations for PrEP, antiretroviral therapy, and routine viral load monitoring. This shift is particularly beneficial for patients in rural or underserved areas, where specialist access is limited. Moreover, partnerships between digital health platforms and pharmaceutical companies are streamlining patient engagement, adherence tracking, and drug delivery through mail-order pharmacies. Companies like Nurx and PlushCare have already collaborated with leading drug manufacturers to offer home-based HIV care. This trend not only boosts patient convenience and adherence but also opens a scalable channel for pharmaceutical companies to increase drug penetration. As digital health gains further regulatory backing, its role in HIV drug distribution is expected to expand significantly.

Challenge

-

Managing Comorbidities in Aging HIV Patient Populations Increases Treatment Complexity and Drug Interaction Risks

With the advent of effective antiretroviral therapy, individuals living with HIV are living longer, leading to an aging patient population. However, this longevity brings with it a new set of challenges managing age-related comorbidities such as cardiovascular disease, diabetes, and renal impairment alongside HIV. Older patients often take multiple medications, increasing the risk of drug-drug interactions and adverse effects. For instance, protease inhibitors used in HIV treatment can affect lipid metabolism, potentially exacerbating cardiovascular risks. Furthermore, the liver and kidney functions decline with age, affecting how drugs are metabolized and excreted. Pharmaceutical companies must account for these physiological changes when formulating treatments, which often leads to a narrower therapeutic window and a higher rate of therapy modification. Clinicians are also challenged with balancing HIV suppression while minimizing side effects and ensuring compliance. This multifactorial complexity significantly raises the bar for both drug development and real-world treatment management, presenting a formidable challenge in the evolving HIV drugs market.

Segmental Analysis

By Drug Class

In 2023, Combination HIV Medicines dominated the global human immunodeficiency virus drugs market with a 42.6% market share, owing to their increased effectiveness, improved adherence rates, and patient-friendly dosing regimens. These therapies combine two or more antiretroviral agents in a single tablet, which significantly simplifies treatment for people living with human immunodeficiency virus. According to the U.S. Department of Health and Human Services (HHS), combination drugs are recommended as the first-line treatment in antiretroviral therapy due to their ability to reduce pill burden and improve compliance. Notable examples include Gilead Sciences’ Biktarvy and ViiV Healthcare’s Dovato, both of which are widely adopted globally for their clinical efficacy and minimal side effects. Additionally, the World Health Organization (WHO) guidelines emphasize the importance of fixed-dose combinations for streamlining treatment in low- and middle-income countries. The growing preference for these combinations, supported by clinical guidelines and government-backed procurement programs like the President's Emergency Plan for AIDS Relief (PEPFAR), has contributed significantly to the segment’s leading position in 2023.

By Distribution Channel

In 2023, Hospital Pharmacies led the global human immunodeficiency virus drugs market with a substantial 48.3% market share, primarily due to the increasing reliance on specialized care and immediate drug accessibility within hospital settings. Hospital pharmacies play a pivotal role in dispensing antiretroviral therapy, particularly for newly diagnosed patients or those with comorbidities that require tailored regimens and monitoring. According to data from the Centers for Disease Control and Prevention (CDC), many hospitals, especially in urban regions of the United States, are designated centers for the initial diagnosis and management of human immunodeficiency virus, ensuring that patients receive comprehensive treatment and counseling under one roof. Moreover, public health initiatives and institutional procurement mechanisms such as bulk purchasing through health departments and national health systems often prioritize hospitals as key drug distribution nodes. This segment also benefits from strategic collaborations between pharmaceutical manufacturers and healthcare institutions to deliver high-cost combination therapies in a controlled and monitored environment, ensuring proper adherence and reducing the risk of resistance development, thus cementing its dominant status in 2023.

Regional Analysis

North America emerged as the leading regional market for human immunodeficiency virus drugs in 2023, accounting for approximately 53.1% of the global market share, driven by advanced healthcare infrastructure, high treatment coverage, and strong government backing for antiretroviral programs. The United States, in particular, played a central role, supported by initiatives like the Ending the HIV Epidemic plan launched by the U.S. Department of Health and Human Services, which aims to reduce new human immunodeficiency virus infections by 90% by 2030. This federal strategy includes widespread testing, pre-exposure prophylaxis (PrEP) availability, and comprehensive antiretroviral therapy coverage through public healthcare programs like Medicaid and Medicare. Additionally, the presence of major pharmaceutical players such as Gilead Sciences and ViiV Healthcare ensures rapid development, approval, and distribution of innovative therapies like long-acting injectables and single-tablet regimens. Canada also contributes to the region’s dominance with its national human immunodeficiency virus drug programs and public reimbursement policies that ensure wide access. Together, these policy-driven measures, combined with strong pharmaceutical R&D ecosystems and awareness campaigns, have positioned North America at the forefront of the global human immunodeficiency virus drug market.

Moreover, the Asia Pacific region emerged as the fastest growing in the global human immunodeficiency virus drugs market, with a substantial growth rate from 2024 to 2032, driven by rising disease prevalence, expanding healthcare access, and supportive governmental interventions. Countries like India, China, and Thailand are at the forefront of this growth due to their large patient populations and increasing public health efforts to improve diagnosis and treatment. For example, India’s National AIDS Control Organization (NACO) has been actively expanding its antiretroviral therapy centers and providing free treatment, supported by international organizations such as UNAIDS and the Global Fund. Meanwhile, China’s Healthy China 2030 initiative is promoting widespread testing and early treatment, aiming to achieve the United Nations' 95-95-95 goals. Additionally, pharmaceutical companies in the region are ramping up local production of generic antiretroviral drugs, significantly improving affordability and access. In Southeast Asia, collaborations with global health agencies have led to improved awareness and treatment uptake, especially in vulnerable populations. These combined efforts, along with increased investments in healthcare infrastructure and digital health platforms for treatment adherence, are propelling the rapid expansion of the human immunodeficiency virus drugs market across Asia Pacific.

Do You Need any Customization Research on HIV Drugs Market - Enquire Now

Key Players

-

AbbVie Inc. (Lopinavir/Ritonavir, Aluvia, Kaletra)

-

Aurobindo Pharma Ltd. (Efavirenz, Tenofovir Disoproxil Fumarate, Lamivudine)

-

Cipla Ltd. (Trioday, Viraday, Tenvir)

-

Dr. Reddy's Laboratories Ltd. (Efavirenz, Tenofovir, Lamivudine)

-

Emcure Pharmaceuticals Pvt. Ltd. (Zidovudine, Lamivudine, Atazanavir)

-

Gilead Sciences, Inc. (Biktarvy, Truvada, Descovy)

-

Glenmark Pharmaceuticals Ltd. (Lamivudine, Tenofovir, Efavirenz)

-

Hetero Drugs Ltd. (Tenofovir, Efavirenz, Lamivudine)

-

Johnson & Johnson (Janssen Pharmaceuticals) (Prezista, Symtuza, Edurant)

-

Lupin Limited (Lamivudine, Zidovudine, Efavirenz)

-

Merck & Co., Inc. (Isentress, Delstrigo, Pifeltro)

-

Mylan N.V. (now part of Viatris) (Tenofovir, Lamivudine, Efavirenz)

-

Natco Pharma Ltd. (Efavirenz, Tenofovir, Lamivudine)

-

Sun Pharmaceutical Industries Ltd. (Lamivudine, Tenofovir, Efavirenz)

-

Teva Pharmaceutical Industries Ltd. (Efavirenz, Zidovudine, Lamivudine)

-

Torrent Pharmaceuticals Ltd. (Efavirenz, Tenofovir, Lamivudine)

-

ViiV Healthcare (Triumeq, Dovato, Tivicay)

-

Zydus Lifesciences Ltd. (formerly Cadila Healthcare) (Zidovudine, Lamivudine, Efavirenz)

-

Alkem Laboratories Ltd. (Lamivudine, Tenofovir, Efavirenz)

Recent Developments

-

March 2025: Early clinical trials of new long-acting HIV drugs, including lenacapavir, showed promising results. These advancements indicated a shift towards more effective and convenient HIV treatment and prevention methods, potentially improving adherence and outcomes for individuals living with or at risk of HIV.

-

February 2025: Gilead Sciences announced that the U.S. Food and Drug Administration (FDA) accepted their New Drug Application for lenacapavir as a biannual injectable for HIV prevention under Priority Review. This step brought the drug closer to potential approval and availability for individuals at risk of HIV in the United States.

-

January 2025: The United Nations reported that lenacapavir has shown exceptional promise in both HIV prevention and treatment. The report underscored the importance of making this biannual injectable drug accessible and affordable, particularly in low- and middle-income countries, to effectively combat the global HIV epidemic.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 32.34 Billion |

| Market Size by 2032 | USD 50.32 Billion |

| CAGR | CAGR of 5.04% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Drug Class (Integrase Inhibitors, Nucleoside Reverse Transcriptase Inhibitors (NRTIs), Non-Nucleoside Reverse Transcriptase Inhibitors (NNRTIs), Combination HIV Medicines, Others) •By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Gilead Sciences, Inc., ViiV Healthcare, GlaxoSmithKline plc (via ViiV Healthcare), Merck & Co., Inc., Johnson & Johnson (Janssen Pharmaceuticals), AbbVie Inc., Cipla Ltd., Mylan N.V. (now part of Viatris), Hetero Drugs Ltd., Emcure Pharmaceuticals Pvt. Ltd. and other key players |

Frequently Asked Questions

Asia Pacific is emerging as the fastest-growing region in the HIV Drugs Market.

Combination HIV medicines accounted for 42.6% of the HIV Drugs Market in 2023.

The HIV Drugs Market is projected to grow at a CAGR of 5.04% during the forecast period.

The HIV Drugs Market is expected to reach USD 50.32 Billion by 2032.

The HIV Drugs Market was valued at USD 32.34 Billion in 2023.

Get in Touch