Healthcare Finance Solutions Market Report Scope & Overview:

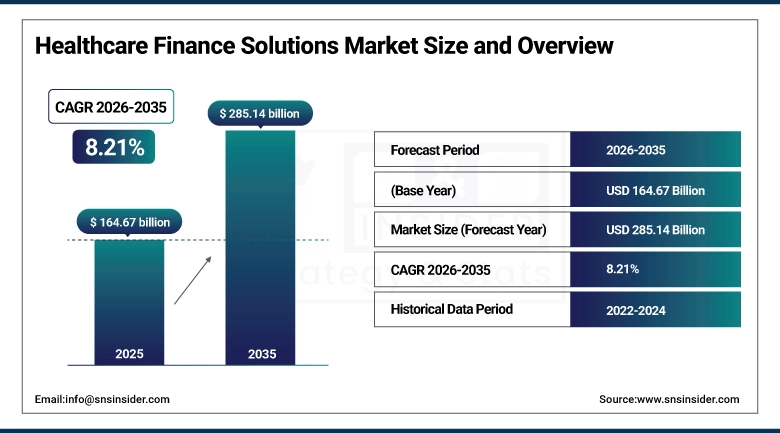

The Healthcare Finance Solutions Market size was valued at USD 164.67 billion in 2025 and is expected to reach USD 285.14 billion by 2035, at a CAGR of 8.21% during the forecast period 2026-2035.

The global healthcare finance solutions market is gaining momentum as healthcare providers, hospital groups, and outpatient facilities increasingly use structured finance instruments as a source of funding for capital-intensive purchases of medical equipment, facility expansions, and technology upgrades. The market growth can be attributed to the increased demand for diagnostic and imaging equipment finance, equipment leasing trends in physician practices and outpatient facilities, and the strategic drive towards value-based care, which forces healthcare providers to upgrade old medical equipment without exhausting capital funds. Working capital finance, project finance solutions, and corporate lending are gaining momentum in hospitals and healthcare organizations worldwide due to the constrained reimbursement environment and rising operational costs, which force healthcare providers to seek alternative, non-dilutive sources of funding. Cloud-based healthcare financial solutions, artificial intelligence-based credit assessment tools, and healthcare lending platforms are also contributing to the growth momentum of this market, which is expected to continue in the future.

For instance, in February 2024, a survey by the Healthcare Financial Management Association (HFMA) revealed that 61% of U.S. hospital CFOs increased their reliance on third-party equipment and technology financing in 2023, citing capital preservation and balance sheet flexibility as primary motivations.

Healthcare Finance Solutions Market Size and Forecast:

-

Market Size in 2025: USD 164.67 billion

-

Market Size by 2035: USD 285.14 billion

-

CAGR: 8.21% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Healthcare Finance Solutions Market - Request Free Sample Report

Healthcare Finance Solutions Market Trends

-

Rising adoption of equipment and technology finance structures by hospitals and outpatient surgery centers to fund MRI, CT, and robotic surgical systems without capital expenditure strain.

-

Expansion of working capital finance products tailored to independent physician practices, urgent care clinics, and skilled nursing facilities operating under thin operating margins.

-

Integration of AI-powered underwriting and digital loan origination platforms by healthcare finance providers to accelerate credit decisions and reduce administrative friction.

-

Growing popularity of operating lease and fair market value lease structures for diagnostic laboratory and IT equipment with short technological refresh cycles.

-

Increased demand for project finance solutions to support greenfield hospital construction, outpatient imaging center development, and specialty care facility upgrades in emerging markets.

-

Strategic collaborations between medical equipment manufacturers and captive finance companies to offer bundled procurement and financing packages directly to end-user facilities.

-

Regulatory evolution around healthcare lending disclosures, fair lending compliance, and ESG-linked financing structures is reshaping product design across corporate lending portfolios.

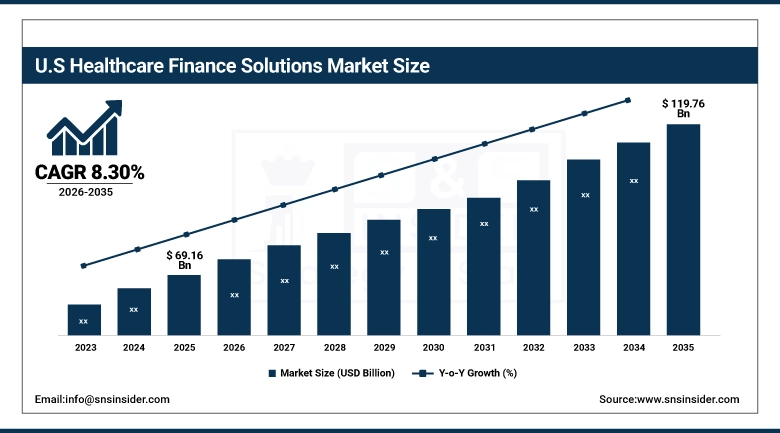

The U.S. market for Healthcare Finance Solutions is estimated to be worth USD 69.16 billion in 2025 and is projected to grow to USD 119.76 billion by 2035, with a CAGR of 8.30% during 2026-2035. The U.S. market holds the largest share of the global market for healthcare finance solutions. This is due to the scale and sophistication of its system of delivering healthcare services, capital expenditures per facility for advanced diagnostic and surgical equipment, and an established base of specialist lenders for healthcare, captive finance companies of health care providers, and bank healthcare divisions. Rural hospital capital access via federal programs, widespread utilization of section 179 tax deductions for equipment leasing and financing, and rising demand for financing of outpatient facilities contribute to sustained high growth in this market.

Healthcare Finance Solutions Market Growth Drivers:

-

Rising Capital Expenditure Demand Across Healthcare Facilities is Driving the Healthcare Finance Solutions Market Growth

The constant increase in capital expenditure needs in hospitals, health systems, and outpatient facilities represents the most compelling growth factor for the healthcare finance solutions market. The average cost for implementing a 3T MRI machine exceeds USD 3 million, and robotic surgical platforms exceed USD 2 million for a single implementation, making equipment finance a business imperative rather than a business option for healthcare organizations. As these organizations contend with workforce cost inflation, declining reimbursement rates, and growing patient volumes, equipment leases, operating lines of credit, and project finance solutions enable healthcare organizations to implement mission-critical medical technologies without impacting their cash flow or creditworthiness.

For instance, in August 2024, DLL Group reported a 17% year-over-year increase in healthcare equipment financing originations in North America, driven by demand from outpatient imaging centers and outpatient surgery centers investing in next-generation diagnostic systems.

Healthcare Finance Solutions Market Restraints:

-

Stringent Credit Underwriting Standards and Reimbursement Uncertainty are Hampering the Healthcare Finance Solutions Market Growth

Credit risks associated with revenue volatility of healthcare providers, payer mix degradation, and unpredictable changes in federal and state reimbursement policies act as major impediments to the deployment of healthcare finance solutions. Small physician practices, independent urgent care centers, and rural skilled nursing centers face higher funding costs or denial of credit due to a lack of collateral, inconsistent documentation of cash flows, and high leverage ratios. The lenders of healthcare assets face higher default risks due to reimbursement reforms and hence charge premiums, making it less affordable and limiting the market penetration of such solutions to underserved healthcare markets.

Healthcare Finance Solutions Market Opportunities:

-

Digital Lending Platforms and Embedded Finance Models Create Significant Growth Opportunities for the Healthcare Finance Solutions Market

The convergence of financial technology with healthcare procurement workflows is generating transformative opportunities for market expansion. Embedded finance models that integrate loan origination, credit decisioning, and contract execution directly into medical equipment procurement portals and group purchasing organization platforms are shortening financing cycle times from weeks to hours. AI-driven risk scoring that incorporates electronic health record revenue data, payer mix analytics, and real-time claims benchmarks enables lenders to extend credit to previously underserved provider segments with greater confidence. These innovations are expected to unlock substantial demand from pharmacies, diagnostic laboratories, and outpatient clinics that historically relied on traditional bank financing with longer approval timelines.

For instance, in November 2024, Oxford Finance announced the launch of a digital healthcare lending portal that reduced average loan processing time by 43% for small to mid-sized outpatient clinics, expanding access to working capital finance for facilities with annual revenues below USD 10 million.

Healthcare Finance Solutions Market Segment Analysis

-

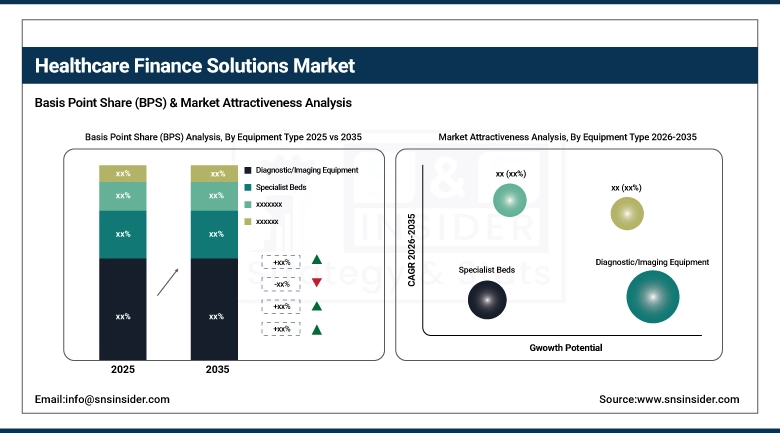

By equipment type, the diagnostic/imaging equipment segment held the largest share of approximately 36.14% in 2025, while the IT equipment segment is expected to register the highest CAGR of 9.47% through 2035.

-

By facility type, the hospitals and health systems segment dominated the market with a share of around 46.83% in 2025, while the outpatient surgery centers segment is expected to grow at the fastest CAGR of 9.12% through 2035.

-

By services, the equipment and technology finance segment led the market with approximately 43.27% revenue share in 2025, while the working capital finance segment is anticipated to register the highest CAGR of 8.94% through 2035.

By Equipment Type, Diagnostic/Imaging Equipment Leads While IT Equipment Registers Fastest Growth

The diagnostic and imaging equipment segment had the maximum revenue share of around 36.14% in 2025. This shows the capital-intensive nature of CT scanners, MRI machines, PET scanners, ultrasound machines, and interventional radiology equipment, which require structured finance to address the procurement costs of multi-million-dollar equipment. The long asset life and high collateral values make the diagnostic and imaging equipment segment a favorite among healthcare lenders and lessors. On the other hand, the IT equipment segment is expected to grow at the fastest CAGR of 9.47% from 2026 to 2035. This is mainly because of the increasing investments in electronic health records systems, cybersecurity solutions, telehealth devices, and clinical decision support systems. The short technology refresh cycle and bundling of hardware and software make the IT equipment segment attractive for captive financiers and specialty lenders of healthcare IT equipment.

By Facility Type, Hospitals and Health Systems Lead While Outpatient Surgery Centers Register Fastest Growth

Facilities and health systems dominated the market segment of the largest size, contributing to approximately 46.83% of the market revenue in 2025, owing to their large-scale capital budgets, multi-equipment procurement models, and existing relationships with healthcare finance providers for project finance and corporate lending. The wide range of funding requirements of acute care facilities, including equipment installed in the surgical suites and patient monitoring and decontamination systems, ensures consistent origination. The outpatient surgery centers segment is expected to record the highest CAGR of 9.12% over the forecast period of 2035. The segment is benefiting from the continued trend of shifting high acuity procedures from inpatient to outpatient settings. The increasing physician ownership of outpatient surgery centers, along with payer incentives favoring lower-cost care locations, is fueling capital investment in robotic surgery and imaging equipment.

By Services, Equipment and Technology Finance Leads While Working Capital Finance Registers Fastest Growth

The equipment and technology finance segment maintained its highest market revenue share of 43.27% in 2025, driven by the primary need for healthcare finance solutions, which is to help healthcare providers acquire diagnostic, surgical, and IT equipment through lease and loan arrangements that provide liquidity. The extensive range of medical equipment types that need structured finance arrangements will continue to support this segment’s market leadership. The working capital finance segment is also expected to experience the highest CAGR of 8.94% between 2026 and 2035, driven by healthcare providers' increased need for revolving credit facilities, accounts receivable financing, and lines of credit arrangements that help them manage cash flow gaps between reimbursements, staffing costs, and supply chain procurements. The financial pressure faced by independent physician practices, pharmacies, and urgent care clinics will also contribute to the market for this segment.

Healthcare Finance Solutions Market Regional Highlights:

North America Healthcare Finance Solutions Market Insights:

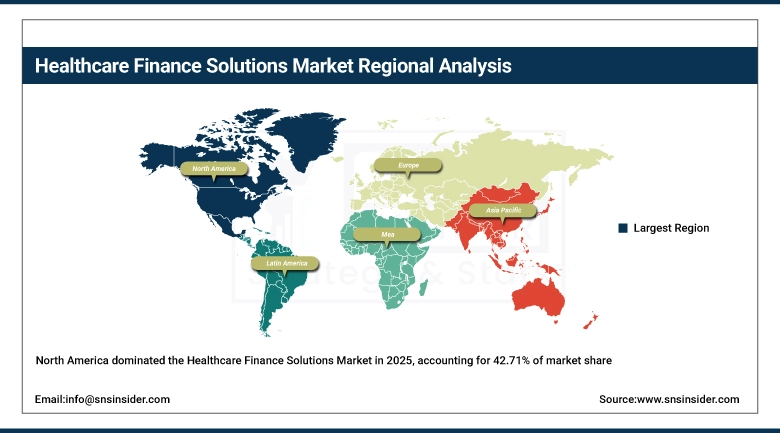

North America accounted for the highest share of over 42.71% in the healthcare finance solutions market in 2025 due to the well-established healthcare lending ecosystem in the region. The high density of acute care hospitals and specialty outpatient facilities in the region also contributed to the dominance of the regional market. The well-established secondary markets for healthcare equipment collateral in the region also helped the regional market to hold a high share in the global market. The presence of a well-established base of captive finance subsidiaries operated by global medical device manufacturers also helped the regional market to hold a high share in the global market for healthcare finance solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Healthcare Finance Solutions Market Insights:

Asia Pacific is the fastest-growing segment in the healthcare finance solutions market with a CAGR of 10.24%, driven by huge-scale investments made by the government in hospital infrastructure development, the high growth rate of private healthcare networks in China, India, and Southeast Asia, and the increased popularity of equipment leasing models adopted by newly developed diagnostic laboratory chains and outpatient imaging centers. Increasing healthcare demand among the growing middle-class population, coupled with increased insurance penetration and the arrival of global captive finance companies in the market, are broadening the scope of the market. Infra finance initiatives for greenfield hospital development in emerging ASEAN markets have created a high demand for finance solutions for hospital projects and corporate loans for regional healthcare players.

Europe Healthcare Finance Solutions Market Insights:

Europe accounts for the second-largest market share of the global healthcare finance solutions market, fueled by the continued modernization of public hospital infrastructure through health information technology programs, the increasing popularity of private funding schemes for NHS trusts and public hospital capital projects in the UK, and the expanding need for medical equipment and diagnostic device financings in Germany, France, and the Nordic countries. The pan-European healthcare investment drives, a favorable sovereign credit environment helping public health system operators minimize capital costs, and a strengthening market for sale leaseback financings of existing medical equipment assets are helping sustain growth within the combined Western and Eastern European markets.

Latin America (LATAM) and Middle East & Africa (MEA) Healthcare Finance Solutions Market Insights:

In Latin America and the Middle East and Africa, expanding private hospital networks, increasing foreign direct investment in healthcare infrastructure, and government-backed health facility modernization programs are driving adoption of healthcare finance solutions. The growing availability of USD-denominated and local currency healthcare lending products, combined with multilateral development bank participation in healthcare project finance structures, is improving capital access for providers in Brazil, Mexico, UAE, and Saudi Arabia. Mobile-first financial platforms offering streamlined equipment finance origination are supporting market penetration in regions where traditional banking relationships have historically limited provider access to structured healthcare lending.

Healthcare Finance Solutions Market Competitive Landscape:

DLL Group (De Lage Landen) (est. 1969) is a global asset-based financing company with a specialized healthcare division that provides equipment leasing, working capital, and vendor finance programs to hospitals, outpatient facilities, and physician practices across more than 30 countries. Its deep integration with medical equipment manufacturer distribution channels and proprietary credit assessment tools for healthcare providers make it a dominant force in global healthcare equipment finance origination.

-

In January 2025, DLL Group expanded its healthcare vendor finance platform in the Asia Pacific region, launching dedicated financing programs for diagnostic imaging and surgical robotics equipment providers in Australia, Japan, and Singapore to support regional facility modernization initiatives.

Oxford Finance LLC (est. 1981) is a specialty finance firm focused exclusively on the life sciences and healthcare sectors, providing senior secured loans, growth capital, and working capital solutions to hospitals, outpatient surgery centers, and healthcare services companies across North America. Its healthcare-specific underwriting expertise and flexible capital structures are key competitive differentiators.

-

In September 2024, Oxford Finance closed a USD 1.2 billion healthcare lending fund targeting growth capital and acquisition financing for outpatient clinic operators and urgent care networks, expanding its portfolio focus beyond early-stage life sciences clients.

Key Equipment Finance (est. 1923, healthcare division) is a major U.S. commercial bank-affiliated equipment finance company offering healthcare-specific leasing, loan, and municipal finance solutions to hospitals, physician practices, skilled nursing facilities, and diagnostic laboratories. Its extensive product suite spanning operating leases, finance leases, and equipment lines of credit positions it among the top U.S. healthcare finance providers by origination volume.

-

In March 2025, Key Equipment Finance introduced an AI-powered healthcare equipment financing portal that enables same-day credit decisions for transactions up to USD 2 million, significantly accelerating the origination process for outpatient imaging centers and ambulatory surgery centers.

Healthcare Finance Solutions Market Key Players:

-

DLL Group (De Lage Landen)

-

Oxford Finance LLC

-

Key Equipment Finance

-

Siemens Financial Services

-

GE HealthCare Financial Services

-

Philips Capital

-

Bank of America Practice Solutions

-

U.S. Bancorp Equipment Finance

-

Truist Equipment Finance

-

Ares Capital Corporation

-

CIT Healthcare Finance (First Citizens Bank)

-

Stryker Finance Solutions

-

Medtronic Financial Services

-

Cardinal Health Financial Solutions

-

McKesson Capital Solutions

-

Ally Healthcare Finance

-

Marlin Business Services

-

Healthcare Capital LLC

-

Provident Healthcare Partners

-

Mitsubishi HC Capital (Healthcare Division)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 164.67 Billion |

| Market Size by 2035 | USD 285.14 Billion |

| CAGR | CAGR of 8.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Equipment Type (Diagnostic/Imaging Equipment, Specialist Beds, Surgical Instruments, Decontamination Equipment, IT Equipment) • By Facility Type (Hospitals & Health Systems, Outpatient Imaging Centres, Outpatient Surgery Centres, Physician Practices & Outpatient Clinics, Diagnostic Laboratories, Urgent Care Clinics, Skilled Nursing Facilities, Pharmacies, Other Healthcare Providers) • By Services (Equipment and Technology Finance, Working Capital Finance, Project Finance Solutions, Corporate Lending) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | DLL Group (De Lage Landen), Oxford Finance LLC, Key Equipment Finance, Siemens Financial Services, GE HealthCare Financial Services, Philips Capital, Bank of America Practice Solutions, U.S. Bancorp Equipment Finance, Truist Equipment Finance, Ares Capital Corporation, CIT Healthcare Finance (First Citizens Bank), Stryker Finance Solutions, Medtronic Financial Services, Cardinal Health Financial Solutions, McKesson Capital Solutions, Ally Healthcare Finance, Marlin Business Services, Healthcare Capital LLC, Provident Healthcare Partners, Mitsubishi HC Capital (Healthcare Division) |

Frequently Asked Questions

Ans: The Healthcare Finance Solutions Market was valued at USD 164.67 billion in 2025.

Ans: The Healthcare Finance Solutions Market is expected to reach USD 285.14 billion by 2035.

Ans: The Healthcare Finance Solutions Market is projected to grow at a CAGR of 8.21% from 2026 to 2035.

Ans: In the Healthcare Finance Solutions Market, the equipment and technology finance segment held the largest share at 43.27% in 2025.

Ans: North America leads the Healthcare Finance Solutions Market with a 42.71% revenue share in 2025.

Get in Touch