Healthy Food Market Report Scope & Overview:

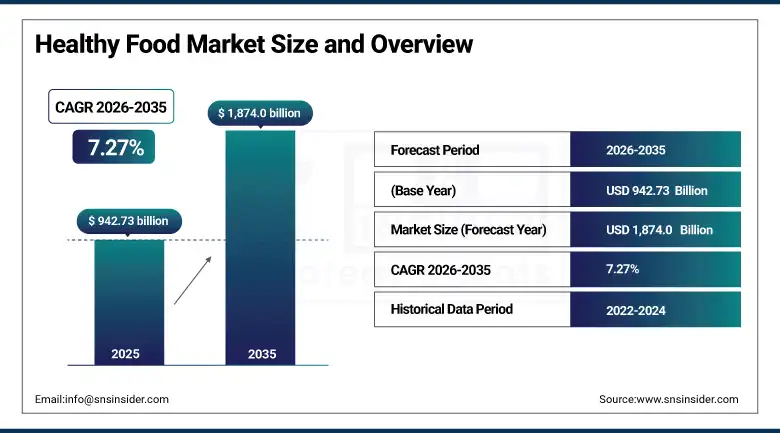

The Healthy Food Market was valued at USD 942.73 Billion in 2025 and is expected to reach USD 1,874.0 Billion by 2035, growing at a CAGR of 7.27% from 2026–2035.

Healthy food has moved from a specialist retail category to a mainstream consumer priority across developed and developing markets alike. More than 70% of global consumers checked nutrition labels during grocery shopping in 2025. 60% prioritized products labelled low-sugar, high-protein, or free from artificial ingredients. Chronic disease rates in ageing populations are turning food choices into a public health concern as much as a personal one. Functional foods, organic products, and free-from alternatives are now standard fixtures in mainstream supermarkets globally, not just in specialty health stores. The category covers a wide range of products and consumer motivations. Some buyers want help with weight management. Others need allergy-safe options. Many are seeking products that support gut health, immune function, or daily energy levels. GLP-1 weight management medication adoption is creating a new and commercially significant demand segment. Patients on these drugs need smaller, protein-rich meals that work alongside their treatment. Food brands are developing formulated products to serve this group. The commercial opportunity this creates remains largely unclaimed by established food manufacturers.

Over 70% of global consumers actively checked nutrition labels during grocery purchases in 2025. Digital health platforms and continuous glucose monitors are beginning to shape food buying decisions for a growing segment of health-motivated consumers worldwide.

Market Size and Forecast

-

Market Size in 2026E: USD 1,011.28 Billion

-

Market Size by 2035: USD 1,874.0 Billion

-

CAGR: 7.27% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Healthy Food Market - Request Free Sample Report

Healthy Food Market Trends

-

GLP-1 medication adoption is creating direct demand for food products formulated to work alongside these treatments, with patients needing protein-rich, low-volume, and nutrient-dense meals that support health outcomes during therapy.

-

Probiotic, prebiotic, and postbiotic product launches are accelerating across beverages, dairy, and snack categories as consumer awareness of the gut health connection to overall wellbeing grows rapidly.

-

Clean-label and minimally processed products are gaining market share as consumers grow increasingly skeptical of long ingredient lists and the ultra-processed food formulations that dominate conventional food aisles.

-

Protein bars, seaweed snacks, and chickpea-based crisps are gaining dedicated shelf space in mainstream grocery chains as functional snacking replaces traditional indulgent formats in consumer routines.

-

Continuous glucose monitors and personalized nutrition apps are reshaping food purchase decisions for health-focused consumers, creating new brand discovery pathways for health-positioned food companies.

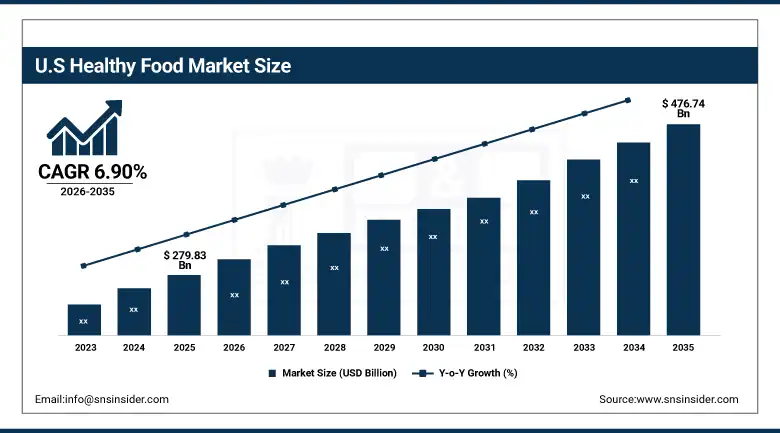

The U.S. Healthy Food Market Outlook

The U.S. Healthy Food Market was valued at approximately USD 279.83 Billion in 2025 and is expected to reach approximately USD 476.74 Billion by 2033, growing at a CAGR of 6.90%.

The United States is the most commercially developed healthy food market in the world. High per-capita food spending combined with strong consumer health awareness creates the conditions for premium products to succeed at scale. Whole Foods, Sprouts, and Trader Joe's built retail models centered on health-positioned food and helped normalize premium pricing for this category. Mainstream grocers including Kroger, Walmart, and Target have materially expanded their health and wellness food sections over the past five years. FDA health claim regulations govern what brands can communicate on packaging and reward investment in clinical evidence. Direct-to-consumer subscription food brands have built substantial businesses in the U.S. by serving health-motivated buyers who want nutrition and convenience together. Factor, Sakara Life, and Daily Harvest have each demonstrated the commercial viability of premium health food subscriptions at scale. GLP-1 medication adoption is an emerging structural demand driver still in its early commercial phase.

USDA organic food sales in the U.S. exceeded USD 67 Billion in 2024. The organic premium held firm through inflationary pressure, confirming that health-motivated consumers protect this category of spending even during periods of broader economic stress.

Healthy Food Market Segment Analysis

-

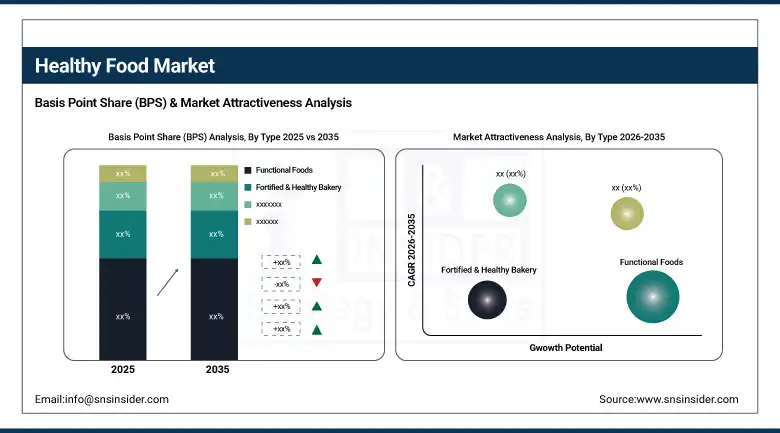

By Type, Functional Foods led the market with approximately 34.81% share in 2025; Healthy Snacks are the fastest-growing type at a CAGR of 13.50% through 2035, fueled by the shift toward nutritious convenience food options.

-

By Free Form, Gluten-Free products held approximately 36.27% share in 2025; Lactose-Free products are the fastest-growing at a CAGR of 11.69%, reflecting rapidly growing consumer awareness of lactose intolerance across previously underserved markets.

-

By Nature, Non-GMO products dominated with approximately 60.57% share in 2025; GMO products are the fastest-growing at a CAGR of 10.35% as precision fermentation and biofortification enable nutritionally superior formulations.

-

By Calorie Content, Low-Calorie products held approximately 45.38% of the market in 2025; No-Calorie products are the fastest-growing at a CAGR of 12.43%, driven by zero-sugar beverage adoption and advances in sweetener technology.

By Type, functional foods dominate, healthy snacks grow fastest

Functional foods occupied about 34.81% share of revenue in the healthy food segment in 2025. Functional foods refer to the foods with health benefits beyond their nutritional components. Probiotics, omega-3 eggs, enriched cereals, and beverages with added vitamins are the common types of functional foods. The scientific evidence for health benefits associated with these foods has been accumulating over the past 20 years. It is due to this evidence that brands have managed to command premium prices without undermining the trust in their products during economic cycles. More and more pharmaceutical and nutraceutical companies are now venturing into the domain of functional foods.

Healthy snacks account for the most rapidly growing sub-segment of the category, posting a CAGR of 13.50% until 2035. The behavioral pattern of consuming unhealthy snacks has undergone a profound change, which does not qualify as a temporary trend. Examples of emerging healthy snacks in major retail outlets include protein bars, products made of seaweeds, chickpeas, and air-popped grains. Consumers seek products that can satisfy them both nutritionally and in terms of taste. These brands grow faster than the category average, with the snack meal opportunity growing over time.

By Free Form, gluten-free dominates, lactose-free grows fastest

Gluten-free products held approximately 36.27% of free-from revenues in 2025. Consumer awareness of coeliac disease has grown significantly over the past decade. Non-coeliac gluten sensitivity is now more widely recognized as a legitimate condition affecting a meaningful proportion of the adult population. These developments together have expanded the consumer base for gluten-free products well beyond people with a medical diagnosis. Gluten-free product ranges now cover bakery, snacks, pasta, sauces, and beverages.

Lactose-free products are the fastest-growing free-from category at a CAGR of 11.69% through 2035. Approximately 65% of the global adult population has some degree of lactose intolerance. Awareness of this condition has historically been low in many markets. As that awareness grows, more consumers are seeking lactose-free versions of dairy products they would otherwise reduce or avoid. Lactase-treated milk and lactose-free cheese and yogurt lines are gaining mainstream supermarket distribution.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.6% |

|

Europe |

Germany |

23.8% |

|

Asia Pacific |

China |

43.7% |

|

Middle East & Africa |

UAE |

28.3% |

|

Latin America |

Brazil |

43.4% |

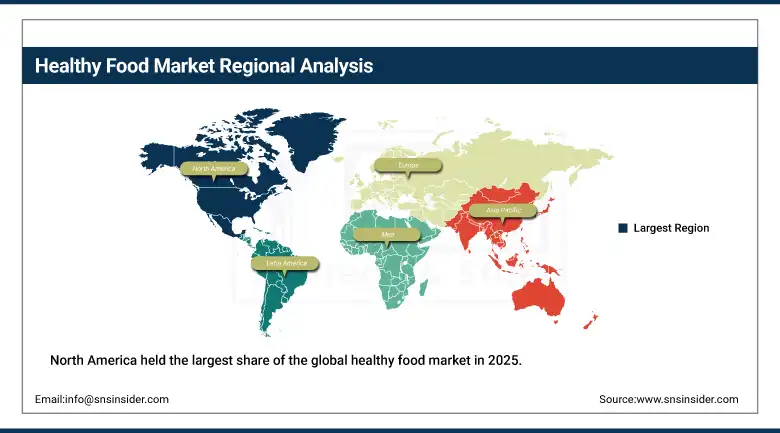

North America Healthy Food Market Insights

North America held the largest share of the global healthy food market in 2025. The United States accounts for approximately 84.6% of North American revenues. Strong consumer health awareness combined with high per-capita food expenditure sustains above-average healthy food spending across all income groups in the upper half of the distribution. The specialty retail infrastructure built around health-positioned food is more developed in the U.S. than in any other national market. Whole Foods, Sprouts, Natural Grocers, and Trader Joe's collectively serve tens of millions of health-focused shoppers every year. Mainstream grocery chains have responded to consumer health trends by expanding wellness food sections in a material way. Target, Kroger, and Walmart have all upgraded their health food assortments significantly in recent years. Online subscription healthy food brands have grown rapidly in the U.S. by offering nutrition alongside convenience. The GLP-1 medication wave is creating an emerging consumer segment that needs specifically formulated food products.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Healthy Food Market Insights

The European region is home to one of the largest and most tightly regulated healthy foods markets. Germany makes up about 23.8% of European revenue as the largest national food market in the EU. Organic and clean-label preferences are prevalent in Germany, Switzerland, and Scandinavian regions. Food labeling laws in the EU stipulate that all food items must carry accurate nutrition labeling within their packaging. Health claims by food brands in Europe are first reviewed and validated by the European Food Safety Authority before being used for commercial purposes. Such strict regulations contribute to consumer trust in the category, although this is at the expense of lengthy product launches compared to other regions. The United Kingdom, France, Netherlands, and Scandinavia have healthy foods markets that continue to experience steady growth. The highest per capita expenditure in Europe on organic food consumption takes place in Switzerland, Denmark, and Austria. Free-from food products have made it into the mainstream supermarket shelf spaces in Western Europe over the last decade. Consumers in Europe exhibit a higher willingness-to-pay premium prices for certified organic and sustainable foods compared to average global consumers.

Asia Pacific Healthy Food Market Insights

Asia Pacific represents the highest growth healthy food region. China represents about 43.7% share of Asia Pacific revenues. Fast urbanization, increasing incomes among middle class population and increased awareness about the risks associated with chronic diseases are key factors driving the demand for health-related products. Traditional cultures of functional foods in countries such as China, Japan and South Korea lead to high consumer acceptance of health foods. Countries such as India, Vietnam and Indonesia represent early adopters but are fast-growing markets. Healthy food brands are adopting premium product positions in the Asian retail environment.

MEA & Latin America Healthy Food Market Insights

The Middle East, Africa, and Latin America are growing healthy food markets at different stages of commercial development. The UAE leads MEA revenues at approximately 28.3% of the regional share. Premium healthy food retail in Dubai and Abu Dhabi serves a large, internationally mobile, health-conscious consumer population that expects global product standards. Government nutrition programmes across Gulf Cooperation Council countries are broadening dietary health awareness beyond the urban core. Brazil leads Latin American revenues at approximately 43.4%. Growing middle-class awareness of chronic disease prevention in major Brazilian cities is driving demand for organic, functional, and free-from food products.

Market Dynamics

Growth Drivers: Rising chronic disease rates, expanding consumer health awareness, and functional food innovation are the primary drivers of healthy food market growth.

Chronic disease is both a personal health concern and a public fiscal challenge. Type 2 diabetes, cardiovascular disease, and obesity together cost global healthcare systems trillions of dollars annually. Governments are responding with nutrition education and preventive health investment. Consumers are responding by changing what they buy. Both forces, one policy-driven and one consumer-driven, are creating durable structural demand for healthier food options. This demand is not cyclical. It is tied to demographic and epidemiological trends that will grow stronger over the coming decade. Functional food innovation has accelerated. Precision fermentation is enabling production of bioactive ingredients with documented health benefits at commercial scale. Brands are investing in clinical evidence to support claims that justify premium pricing. The GLP-1 medication market has created an entirely new consumer segment that needs protein-rich, low-volume, micronutrient-dense food options. No established brand has yet taken a dominant position in this segment. The commercial opportunity remains largely open to brands that move quickly with credible product development.

Restraints: Premium pricing, complex health claim regulations, and consumer skepticism about heavily processed alternatives are restraining broader healthy food market adoption.

Pricing has proven to be the biggest barrier to entry for healthy foods among price-conscious customer segments. Organic and functional foods tend to be priced 20% to 50% higher than their traditional counterparts. In regions where household incomes remain low, this premium makes it very difficult for many customers to purchase these healthy foods. Even in well-developed markets, consumers tend to spend less money on premium products when financial constraints arise. At present, the healthy food industry has not found a way to address the pricing issue in order to make these food types accessible in mass quantities among poorer consumer segments. There is increasing cynicism among consumers regarding overly processed plant-based or functional foods. There has been rising acceptance among public health experts of the idea that some alternatives may not be as healthy as the traditional food items.

Opportunities: GLP-1 companion nutrition products, personalized dietary technology integration, and emerging market income growth represent the largest near-term healthy food market opportunities.

The market of GLP-1-based obesity therapy has started generating a consumer demand for foods which can be consumed in combination with these drugs. Consumers require high protein content, low volume, and high micronutrients content foods, which help maintain health results associated with the therapy. There has not emerged any leading food brand in this market yet. The base of consumers has been growing very fast in the United States and has started its development in Europe and Asia-Pacific regions. With more and more affordable GLP-1-based medicines becoming available, the consumer potential for the segment in question will continue growing very actively. Modern personalization platforms are helping healthy foods brands find consumers. They include continuous glucose monitoring devices, microbiomes tests, and apps for nutritional coaching through artificial intelligence. Such technologies recommend food products according to the data collected from consumers. Thus, food brands, visible in such platforms, have the unique opportunity to connect with highly health-conscious and expensive consumers.

Recent Developments:

-

January 2026: Beyond Meat launched Beyond Immerse, a plant-based protein beverage targeting health-motivated consumers seeking high-protein nutrition options beyond conventional meal formats.

-

January 2026: Impossible Foods partnered with Equii to develop protein-enriched plant-based meal products using Equii's wheat protein fermentation technology, targeting the functional nutrition consumer segment.

-

May 2025: Danone acquired Kate Farms, strengthening its position in plant-based medical nutrition and general wellness food for health-focused consumer segments seeking clinical-grade nutritional products.

-

2025: Nestlé launched green tea extract-based nutraceutical products targeting metabolic health consumers across the Asia Pacific region, extending its functional food portfolio into bioactive wellness categories.

-

2025: Kellogg's expanded its Special K brand with high-protein and probiotic cereal variants, targeting health-motivated breakfast consumers across North American and European grocery markets.

Healthy Food Market Key Players are:

-

Nestlé S.A.

-

Danone S.A.

-

General Mills Inc.

-

Kellogg Company

-

PepsiCo Inc.

-

The Coca-Cola Company

-

Unilever plc

-

Conagra Brands Inc.

-

Hain Celestial Group Inc.

-

Amy's Kitchen

-

Nature's Path Foods Inc.

-

Annie's Homegrown (General Mills)

-

Whole Earth Brands Inc.

-

Simple Mills Inc.

-

Kind LLC

-

RxBar (Kellogg)

-

Perfect Snacks

-

RXBAR

-

Larabar (General Mills)

-

Boulder Brands Inc.

Healthy Food Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 942.73 Billion |

| Market Size by 2035 | USD 1,874.0 Billion |

| CAGR | CAGR of 7.27% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Functional Foods, Fortified & Healthy Bakery, Healthy Snacks, Better-For-You Foods, Beverages, Chocolates, Others) • By Free Form (Gluten-Free, Lactose-Free, Dairy-Free, Soy-Free, Nut-Free, Others) • By Nature (Non-GMO, GMO) • By Calorie Content (No-Calorie, Low-Calorie, Reduced-Calorie) • By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online, Convenience Stores, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nestlé S.A., Danone S.A., General Mills Inc., Kellogg Company, PepsiCo Inc., The Coca-Cola Company, Unilever plc, Conagra Brands Inc., Hain Celestial Group Inc., Amy's Kitchen, Nature's Path Foods Inc., Annie's Homegrown, Whole Earth Brands Inc., Simple Mills Inc., KIND LLC, RXBAR, Perfect Snacks, LÄRABAR, Boulder Brands Inc.. |

Frequently Asked Questions

North America dominated the Healthy Food Market in 2025.

Functional Foods dominated with approximately 34.81% of revenues in 2025.

Rising chronic disease prevalence and consumer health awareness are the primary drivers. GLP-1 medication adoption is creating an emerging demand segment for specifically formulated functional food products.

The Healthy Food Market was valued at USD 942.73 Billion in 2025.

The Healthy Food Market is expected to grow at a CAGR of 7.27% from 2026 to 2035.

Get in Touch