Hearing Loss Disease Treatment Market Size Analysis:

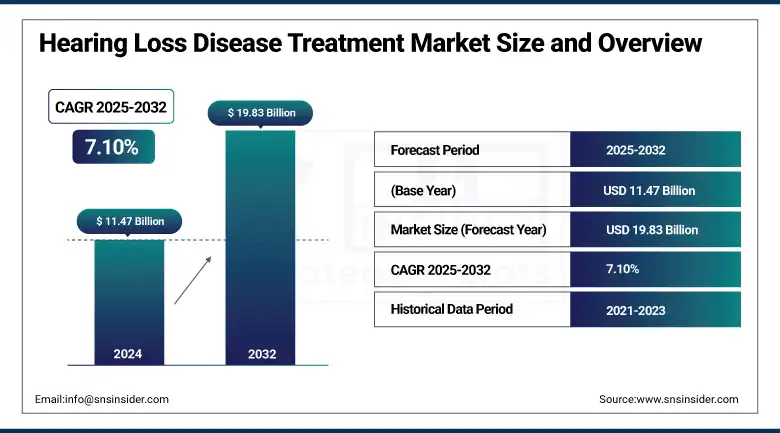

Hearing Loss Disease Treatment Market size was valued at USD 11.47 billion in 2024 and is expected to reach USD 19.83 billion by 2032, growing at a CAGR of 7.10% over the forecast period of 2025-2032.

Growing awareness of auditory health, changing demographics, and increasing hearing loss frequency all help to fuel the market expansion in the therapy for hearing loss disease.

For instance, according to the World Health Organisation (WHO), around 2.5 billion people globally, will have some degree of hearing loss by 2025 and in over 700 million would need rehabilitative treatments.

To Get more information On Hearing Loss Disease Treatment Market - Request Free Sample Report

Early screening and intervention programs are much needed at government agencies, such as the U.S. National Institute on Deafness and Other Communication Disorders (NIDCD), who estimate that about 15% of American adults have some trouble hearing. While national campaigns, such as India's NPPCD program concentrate on early identification and simplified treatment routes, regulatory bodies including the FDA are swiftly approving novel medications and technologies. These initiatives, together with growing insurance coverage and technical developments, are changing the present scene of the hearing loss treatment business.

The increasing incidence of hearing loss, especially among elderly individuals and those exposed to occupational noise, is a main factor influencing the market for the treatment of hearing loss. Due to the changing communication, cognition, and employment opportunities, the WHO estimates the yearly cost of neglected hearing loss at around USD 1 trillion globally. One in three Americans between the ages of 65 and 75 has hearing loss, according to recent NIDCD statistics. The CDC thus advises universal newborn hearing screening to boost rates of early intervention.

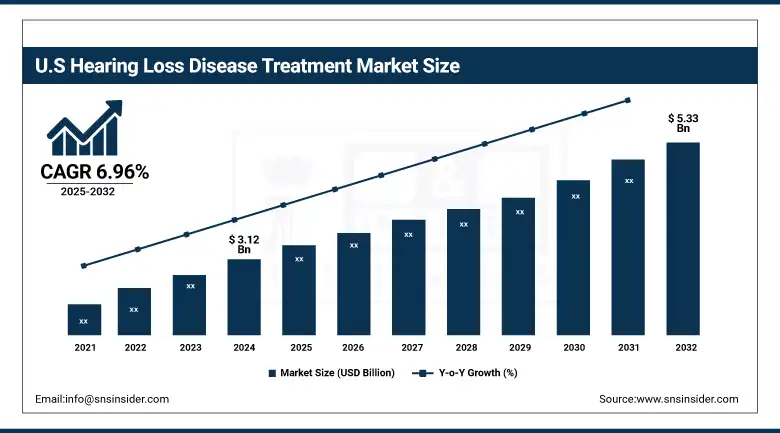

Reflecting its advanced healthcare infrastructure and acceptance of new auditory problem treatment alternatives, the U.S. hearing loss disease treatment market accounted for a significant share of the global market in 2024 with a market value of USD 3.12 billion in 2024 and is expected to reach USD 5.33 billion by 2032 with a 6.96% CAGR over the forecast period. Government-backed insurance coverage, regulatory approvals for new hearing aid market items, and significant R&D expenditure by major companies treating hearing loss disorders all help to drive this dominance.

Hearing Loss Disease Treatment Market Dynamics:

Drivers:

-

Modern Treatments and Advances in Gene Therapy are Rapidly Changing the Management of Hearing Loss Disease

During the last few years, the ways on treating hearing loss diseases are changing fundamentally on account of newer advances in gene therapy and pharmacology interventions. By 2025, estimates of the global number of people requiring rehabilitation for debilitating hearing loss range from roughly 430 million to 700 million. Researchers and business executives are thus hastening the creation of innovative ideas in response.

Particularly, gene therapy research targeted at otoferlin gene (OTOF)-related hearing loss has shown promising results in a 2025 clinical investigation; 10 out of 11 treated children showed remarkable hearing gains, with several reaching almost normal levels. Drugs such as PEDMARK, licensed by the U.S. FDA, serve to lower chemotherapy-induced hearing loss in young infants, therefore fostering pharmaceutical innovation. Tight clinical trial criteria let regulatory authorities, including the FDA and EMA, closely monitor these advancements to guarantee safety and effectiveness. These results mark a new chapter in hearing care and give promise for regenerative, individualized, and stronger therapies meant for both sensorineural and hereditary kinds of hearing loss.

Restraints:

-

High Prices and Insufficient Coverage of Insurance Strictly Limit Access to Treatments for Hearing Loss Disease

High costs and inadequate insurance coverage are still major obstacles to fair access to treatments for hearing loss, notwithstanding technical developments. Reflecting the huge financial impact of untreated cases, the World Health Organization estimates that neglected hearing loss globally has yearly expenditures of around USD 1 trillion. The great cost of assistive listening devices (ALDs) combined with little government support and insurance coverage causes the Deaf and Hard of Hearing (DHH) community to experience social isolation, educational challenges, and psychological stress. These institutional constraints highlight the indispensable necessity of government programs, targeted subsidies, and extra insurance coverage to guarantee that technological developments provide real accessibility and an improved quality of life for all impacted persons.

Two important government healthcare projects in India, the Rashtriya Swasthya Bima Yojana (RSBY) and Pradhan Mantri Jan Arogya Yojana (PMJAY), neither cover cochlear implants or hearing aids. As a result, people and their families are left to carry whole financial weight. This exclusion covers continuous needs, including follow-up audiological tests and equipment maintenance, which then help to control long-term costs.

Hearing Loss Disease Treatment Market Segmentation Analysis:

By Product

With a 90% share in 2024, the devices category controlled the hearing loss disease treatment market. Driving the leadership in this field is fast innovation in hearing restoration technologies, including artificial intelligence-powered hearing aids, wireless connection, and upgraded cochlear implant market solutions. The FDA expanded indications in November 2024 for Med-El cochlear implants, therefore allowing more adults with moderate-to-profound sensorineural hearing loss to benefit from enhanced hearing preservation technologies. Particularly for the market sectors connected to the treatment of age-associated hearing loss, these advances have made audiology devices more efficient and easily available.

The WHO predicts that hazardous listening practices expose around 1.1 billion young people to be at risk of noise-induced hearing loss, which fuels the need of rehabilitative and preventative hearing care therapies. Since they allow faster acceptance of new technology and better patient access, government reimbursement policies and regulatory harmonization also help the hearing aids market.

Driven by advancements in otoprotective drugs and regenerative hearing technologies, the drugs segment is predicted to grow at the fastest CAGR. Approved by the FDA in 2025, ORC-13661 is an investigational medication developed by the University of Washington for clinical trials aimed at protecting patients from the negative effects of aminoglycoside antibiotics damaging hearing. This marks a major advancement in the therapeutic path for hearing loss, with more late-stage trials for anti-inflammatory and gene therapies targeted at both sensorineural and conductive hearing loss therapies.

For a new anti-inflammatory medicine, SPI-101, Sound Pharmaceuticals claimed in May 2023, successful Phase 3 enrollment. Particularly in cases of unresponsive to device-based treatments and young hearing loss treatment, these advancements should address unmet needs.

Supported by strong government funding and regulatory control, the defining trend in the hearing loss disease treatment market analysis is the convergence of technology and drug-based solutions.

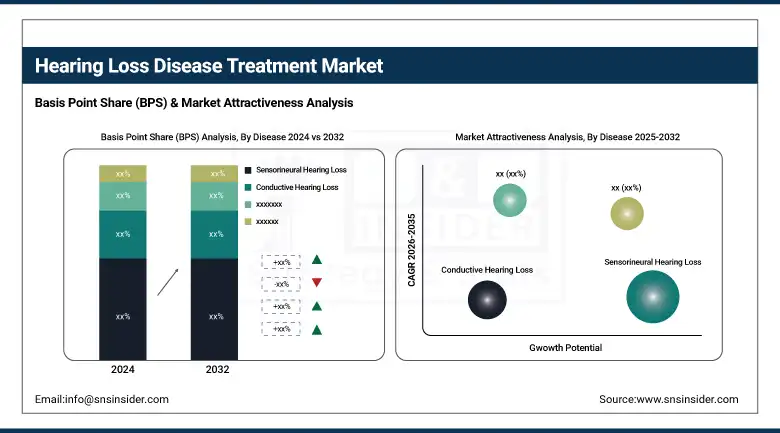

By Disease

Reflecting its great frequency and the major load sensorineural hearing loss segment dominated the market with a revenue share, 64% in 2024. With the NIDCD estimating that up to 66,000 new U.S. cases annually are caused by sudden sensorineural hearing loss, this kind of hearing loss is usually related to aging, hereditary elements, and chronic noise exposure. The majority of this group is supported by the great acceptance of novel pharmacological therapies, cochlear implants, and hearing aids.

Recent government-funded studies have focused mostly on optimizing the results of sensorineural hearing loss treatment. Underlining constant efforts to improve and validate creative auditory disorder treatment modalities, the 2025 assessment of hyperbaric oxygen therapy (HBOT) by the Washington State Health Care Authority evaluated its cost-effectiveness and efficacy for sudden sensorineural hearing loss.

The conductive hearing loss therapies segment is predicted to increase at a considerable CAGR, supported by advances in minimally invasive surgical techniques and bone-anchored hearing aids. Government initiatives focusing on early management and infection control, key causes of conductive hearing loss, are driving category expansion. For example, although U.S. officials currently promote research into creative conductive hearing loss remedies, India's NPPCD program stresses early identification and treatment of ear infections.

By End use

The hospital segment held the highest hearing loss illness treatment market share, 46% in 2024, thereby underscoring the major relevance of hospitals in offering total auditory problem therapy. Modern diagnosis tools, surgical facilities, and multidisciplinary teams including ENT specialists and audiologists competent to manage difficult circumstances and provide both device-based and pharmacological treatments equip hospitals. Government spending in national screening programs and healthcare infrastructure has improved patient outcomes by means of upgraded hospital-based hearing care services.

Particularly for cases requiring pediatric hearing loss therapy, early diagnosis and intervention resulting from the CDC's continued support of universal newborn hearing screening in the U.S. has proven quite helpful.

The rising need for specialized outpatient treatment and the rising frequency of chronic ear ailments drive otology clinics predicted to grow with the highest CAGR. Faster wait times, tailored hearing aid treatments, and more convenience than hospital settings, these offices offer. Government policies supporting outpatient treatment and the acceptance of telehealth platforms are especially aiding otology clinics to flourish in places with restricted access to hospital-based services.

Hearing Loss Disease Treatment Market Regional Analysis:

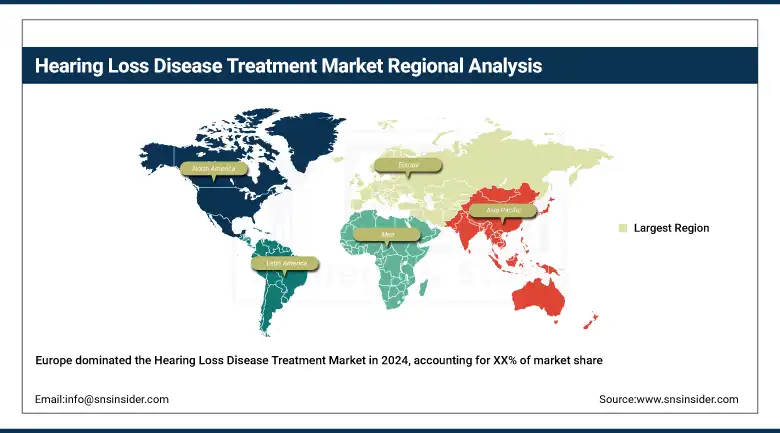

In Europe, the hearing loss disease treatment market generated a significant revenue share in 2024. Strong government funding for audiology breakthroughs, a well-developed clinical research environment, and rising acceptance of both device-based and pharmaceutical hearing loss treatments help the region’s growth. The main markets are Germany, France, and the U.K., each of which uses strong manufacturing capacity, public healthcare projects, and legislative changes to propel market development. Though otology and ambulatory clinics are becoming more popular, particularly in the care of chronic hearing loss, hospitals remain the main distribution point.

Get Customized Report as per Your Business Requirement - Enquiry Now

Rising awareness, growing healthcare expenditure, and a sizable aging population are driving the fastest hearing loss disease treatment market growth in the Asia Pacific region. Supported by government expenditures in healthcare and public health initiatives, nations such as Japan and China are seeing fast acceptance of hearing aids, cochlear implants, and regenerative hearing therapies. Online platforms and ambulatory clinics are improving patient access to hearing care treatments. Hence, Asia-Pacific is a major area for future development of the market for the treatment of hearing loss diseases.

Rising investments in healthcare infrastructure and government campaigns to promote knowledge of hearing loss are driving market expansion in the Middle East and Africa. Though the market is still smaller than in other countries, nations such as South Africa, Saudi Arabia, and the UAE are emphasizing increasing access to pharmaceutical therapies, cochlear implants, and hearing aids. Thanks to growing healthcare expenditure and growing awareness of hearing health, Latin America, led by Brazil, is seeing consistent expansion in the hearing loss treatment market.

Hearing Loss Disease Treatment Market Key Players:

The key Hearing Loss Disease Treatment Companies are Demant A/S, Spiral Therapeutics (Otonomy, Inc.), Sensorion, Novartis AG, Ws Audiology A/S, Audifon Gmbh & Co. Kg, MED-EL Medical Electronics, Sonova, Audina Hearing Instruments, Inc., Acousia Therapeutics Gmbh, and others.

Recent Developments in the Hearing Loss Disease Treatment Market:

-

The Lundbeck Foundation partnered with T&W Medical in April 2024 to purchase a minority share in its 51% controlling ownership in WS Audiology A/S, a global hearing aid manufacturer co-owned (49%) by EQT.

-

Eargo, Inc. launched two new over-the-counter hearing wellness devices, Eargo SE and Eargo, to expand its product portfolio and appeal to a larger customer base in January 2024.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 11.47 Billion |

| Market Size by 2032 | USD 19.83 Billion |

| CAGR | CAGR of 7.1% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Disease (Conductive Hearing Loss, Sensorineural Hearing Loss, and Mixed (Conductive and Sensorineural)) • By Product (Devices, and Drugs {Systemic steroids, Antiviral medication, Vasodilators, and Others}) • By End Use (Hospitals, Ambulatory clinics, and Otology clinics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Demant A/S, Spiral Therapeutics (Otonomy, Inc.), Sensorion, Novartis AG, Ws Audiology A/S, Audifon Gmbh & Co. Kg, MED-EL Medical Electronics, Sonova, Audina Hearing Instruments, Inc., Acousia Therapeutics Gmbh, and others |

Frequently Asked Questions

Ans: The Hospitals segment dominated the Hearing Loss Disease Treatment Market.

Ans: High Costs and Inadequate Insurance Coverage Severely Limit Access to Hearing Loss Disease Treatments

Ans. The CAGR of the Hearing Loss Disease Treatment Market is 7.10% during the forecast period of 2025-2032.

Ans: The North America region dominated the Hearing Loss Disease Treatment Market in 2024.

Ans. The projected market size for the Hearing Loss Disease Treatment Market is USD 19.83 billion by 2032.

Get in Touch