High Sensitivity Information Solutions Market Report Scope & Overview:

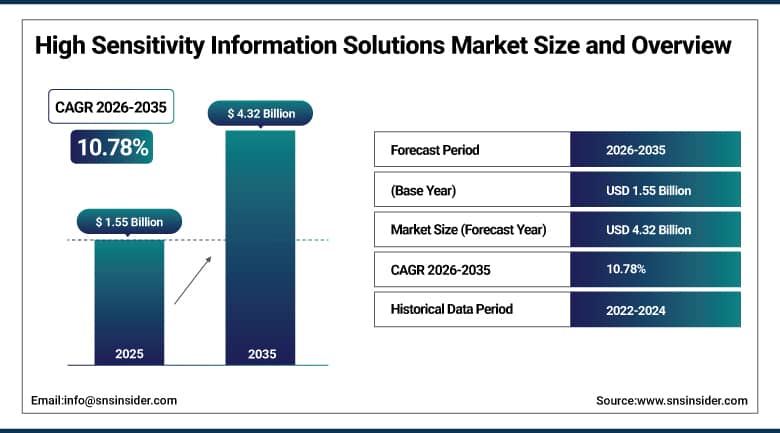

The High Sensitivity Information Solutions Market was valued at USD 1.55 billion in 2025 and is expected to reach USD 4.32 billion by 2035, growing at a CAGR of 10.78% from 2026-2035.

The High Sensitivity Information Solutions Market is witnessing growth due to rising number of cyber attacks, growing number of data breaches, and high demand for sophisticated security systems. The fast-paced adoption of digital technologies, cloud computing, and remote working policies has led to a broadened attack surface, thereby making the need for high sensitivity information solutions all the more important. Moreover, the implementation of regulatory policies like GDPR, HIPAA, and PCI DSS, among others, is also contributing towards market growth by encouraging organizations to embrace encryption, IAM, and DLP solutions.

The proliferation of cloud computing and remote work environments has further fueled demand, with 52% of organizations citing cloud-based services as driving PKI (Public Key Infrastructure) growth, followed by zero-trust strategies (50%), remote-work needs (43%), and IoT adoption (43%).

Market Size and Forecast

-

Market Size 2026E: USD1.72 Billion

-

Market Size 2035: USD 4.32 Billion

-

CAGR (2026-2035): 10.78%

-

Fastest Growing Market: Asia Pacific

-

Largest Market: North America

To Get More Information On High Sensitivity Information Solutions Market - Request Free Sample Report

High Sensitivity Information Solutions Market Trends

-

Rising need for secure handling, monitoring, and protection of sensitive data is driving the high sensitivity information solutions market.

-

Growing adoption across BFSI, government, defense, and healthcare sectors is boosting market growth.

-

Expansion of digital transformation, cloud storage, and remote working environments is fueling solution deployment.

-

Increasing focus on data privacy, compliance requirements, and risk mitigation is shaping adoption trends.

-

Advancements in encryption, identity and access management, data loss prevention, and AI-driven threat detection are enhancing security capabilities.

U.S. High Sensitivity Information Solutions Market Size Outlook

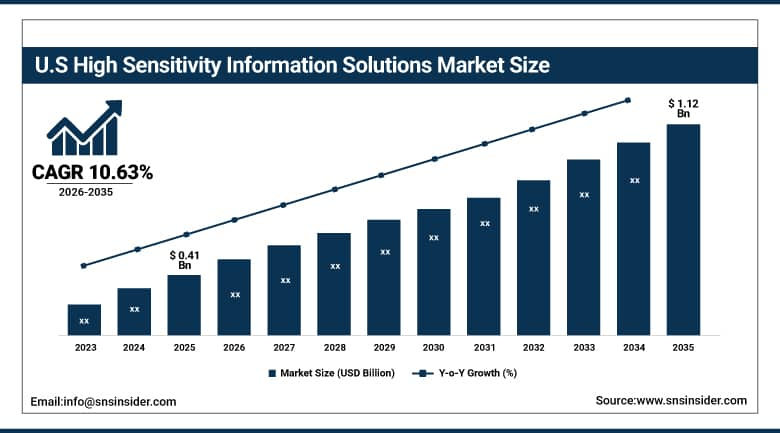

The U.S. High Sensitivity Information Solutions Market was valued at USD 0.41 billion in 2025 and is expected to reach USD 1.12 billion by 2035, growing at a CAGR of 10.63% from 2026-2035.

The U.S. High Sensitivity Information Solutions Market is experiencing growth owing to rising instances of cyber-attacks and data breaches, as well as increasing demand for cybersecurity solutions. With the fast adoption of the cloud and digitization, there are increasing opportunities for data breaches, and strict regulatory compliances such as HIPAA and CCPA further support market growth.

The U.S. Office for Civil Rights has received more than 374,000 HIPAA complaints since 2003, conducted 1,193 compliance reviews, and resolved nearly 99% of cases, demonstrating strong regulatory enforcement and effective resolution of healthcare data privacy violations.

High Sensitivity Information Solutions Market Segment Analysis

-

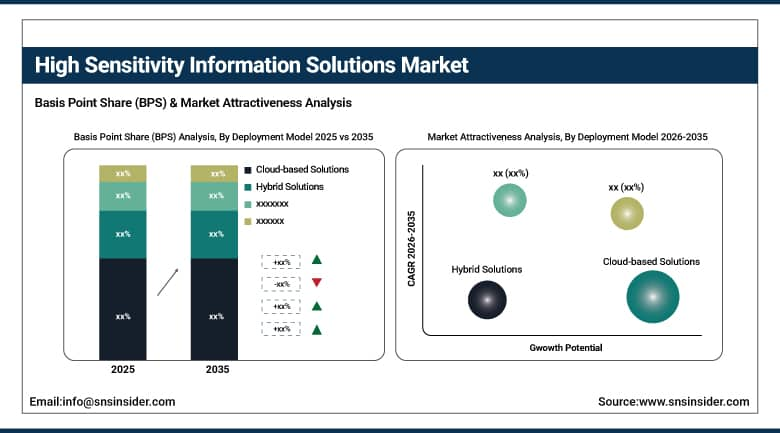

By Deployment Model, cloud-based solutions segment dominated the market in 2025 with 52% share; hybrid solutions segment is the fastest growing segment.

-

By Solution Type, identity and access management (IAM) segment dominated the high sensitivity information solutions market in 2025 with 28% share; data encryption solutions segment is the fastest growing segment.

-

By End User Industry, healthcare segment dominated the market in 2025 with 31% share; financial services segment is the fastest growing segment.

-

By Organizational Size, large enterprises segment dominated the market in 2025 with 66% share; small and medium-sized enterprises (SMES) segment is the fastest growing segment.

-

By Compliance and Regulatory Requirements, GDPR segment dominated the market in 2025 with 34% share; PCI DSS segment is the fastest growing segment.

By Deployment Model, cloud-based solutions segment dominates the market, hybrid solutions segment is the fastest growing

The cloud-based solutions segment dominated the high sensitivity information solutions market owing to its scalability, affordability, and easy deployment options. Enterprises are increasingly migrating towards cloud systems for storing their high sensitivity data in a highly secured manner while allowing them to access the same in real time. Advanced security capabilities provided by cloud systems include automation of update processes, central monitoring, and compliance management. Increased digital transformation and adoption of software as a service-based security solutions have contributed immensely to the dominance of cloud deployment in managing high sensitivity information.

The hybrid solutions segment is the fastest growing in the high sensitivity information solutions market because of the growing need for flexible and secure IT infrastructures where both on-premise systems and cloud technology can coexist. Enterprises are opting for hybrid solutions to ensure that they benefit from the advantages provided by both on-premise solutions and cloud technologies. Hybrid solution enables the enterprise to store high sensitivity data on-premises while leveraging cloud systems for scaling purposes and analytical activities. Issues related to data sovereignty and need for customized security architectures drive the adoption of hybrid solutions.

By Solution Type, identity and access management (IAM) segment dominates market, data encryption solutions segment is the fastest growing

The Identity and Access Management (IAM) segment dominated the high sensitivity information solutions market due to their importance in user access control, identity verification, and prevention of the data leak. Many organizations use IAM solutions due to the necessity to comply with various security and regulatory requirements. Besides, the increasing number of cybersecurity threats and the necessity to protect confidential information make IAM even more popular among companies.

The data encryption solutions segment is the fastest growing in the high sensitivity information solutions market because of the increasing number of data breaches, attacks, and necessary compliance requirements. Data encryption is important due to the necessity to protect sensitive data in transit and in a place from any kind of threats. With the growth of popularity of cloud-based services, telecommuting, and international operations, the need for such solutions grows. Also, due to increased legal requirements for data protection and higher attention to data privacy, many companies deploy such solutions.

By End User Industry, healthcare segment dominates the high sensitivity information solutions market, financial services segment is the fastest growing

The healthcare segment dominated the high sensitivity information solutions market owing to the crucial necessity of protecting patient information, clinical information, and electronic health record systems. The healthcare domain deals with huge amounts of confidential data, thus making it a primary target for cyberattacks. With the increased digitalization of the healthcare industry and the growing usage of electronic health records, there has been an even more urgent necessity of deploying advanced security technologies.

The financial services segment is the fastest growing in the high sensitivity information solutions market because of the increasing adoption of digital banking channels and online transactions. Financial institutions are dealing with sensitive personal and transactional data, which make them attractive targets for various cybercrimes, including phishing attacks and frauds. The growing popularity of fintech platforms and mobile banking systems increases the demand for cybersecurity and data protection solutions. Stringent regulatory compliances and rising concerns related to fraud prevention increase the use of high sensitivity information solutions in financial services.

By Organizational Size, large enterprises segment dominates the high sensitivity information solutions market, smes segment is the fastest growing

The large enterprises segment dominated the high sensitivity information solutions market owing to their huge IT infrastructure, need for large scale data processing, and budget allocation towards cybersecurity. Such firms deal with massive volumes of confidential customer, financial, and operational data that require comprehensive security systems. They also have to comply with stringent regulations that make advanced solutions in identity management and encryption mandatory. Furthermore, the earlier implementation of digital transformation initiatives and cloud strategies has also increased the importance of such comprehensive systems for them.

The SMEs segment is the fastest growing in the high sensitivity information solutions market due to increased awareness about cybersecurity threats along with increased digital adoption. The increasing incidences of cyberattacks on small and medium-sized enterprises (SMEs) have led them to invest in advanced but cost-effective security solutions. The accessibility of such solutions through cloud-based systems has added momentum to their growth. In addition to this, the increased requirement for regulatory compliance as well as growing presence of e-commerce and digital services is boosting their adoption.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

94.6% |

|

Europe |

United Kingdom |

28.7% |

|

Asia Pacific |

China |

55.9% |

|

Middle East & Africa |

UAE |

16.3% |

|

Latin America |

Brazil |

53.8% |

North America High Sensitivity Information Solutions Market Insights

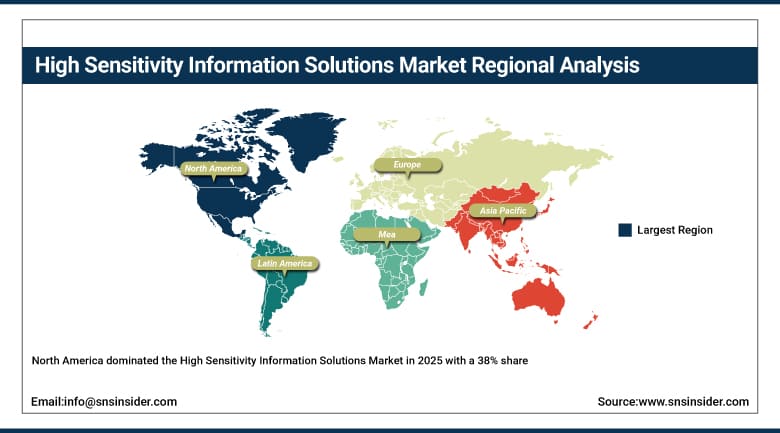

North America dominated the High Sensitivity Information Solutions Market in 2025 with a 38% share, owing to the high adoption rate of advanced cybersecurity solutions and quick digital transformations in various industry sectors. The region has a robust information technology network and hosts major cybersecurity and software vendors, which fosters continuous innovations in data security solutions. Various strict regulations such as HIPAA and CCPA and others are compelling firms to adopt secure data management solutions. Moreover, increased cyber-attacks and cloud adoption, coupled with high demand from healthcare, BFSI, and governmental segments, will drive regional dominance and growth in the future.

In North America, cybercrime remains highly significant, with the U.S. Federal Bureau of Investigation (FBI) reporting $12.5 billion in reported cybercrime losses in 2023, highlighting the scale of sensitive data exposure risks driving demand for encryption, IAM, and DLP solutions.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe High Sensitivity Information Solutions Market Insights

The European High Sensitivity Information Solutions Market growth is fueled by stringent data protection laws like GDPR and growing emphasis on cybersecurity within various industries. Companies are making substantial investments in solutions such as encryption, identity and access management, and data loss prevention services to comply with the stringent requirements and protect their sensitive information. Growing digitalization within the banking, healthcare, and government industries is contributing to the market growth. The increasing number of cyberattacks and data breaches are prompting companies to implement robust security frameworks.

EEA Supervisory Authorities have recorded over 144,000 GDPR complaints and queries, along with 89,000 data breaches. Around 63% of cases have been resolved, while 37% remain open, highlighting ongoing regulatory enforcement and data protection challenges across Europe.

Asia Pacific High Sensitivity Information Solutions Market Insights

The Asia Pacific region is projected to experience the highest growth rate in the High Sensitivity Information Solutions Market with a CAGR of 12.12% during the forecast period. This rapid growth will be fueled by fast digital transformations, greater adoption of cloud computing technology, and increasing internet usage in developing countries. Growing cyber-attacks and increasing data protection requirements will motivate organizations to adopt more advanced security solutions. Furthermore, strong growth in various sectors such as IT, BFSI, healthcare, and government will propel the market growth.

In the Asia Pacific region, rapid digitalization is increasing exposure to cyber risks. The International Telecommunication Union (ITU) reports that internet usage in Asia-Pacific exceeds 2.9 billion users, representing the largest digital population globally and significantly expanding the attack surface for sensitive data environments.

Middle East & Africa and Latin America High Sensitivity Information Solutions Market Insights

Middle East & Africa and Latin America High Sensitivity Information Solutions Market is experiencing constant growth owing to high levels of digitalization and increased realization of cybersecurity challenges. The increasing adoption of cloud services, mobile applications, and online banking platforms leads to the need for effective data protection solutions. Additionally, governments have started implementing data privacy laws to boost security levels. Nevertheless, insufficient cybersecurity facilities and budget shortages in some countries become impediments to further adoption. At the same time, the increasing level of investment in IT upgrades and cyber attacks cases favor market growth prospects.

The International Telecommunication Union (ITU) notes that Africa alone has over 600 million internet users, with rapid growth in mobile connectivity increasing exposure to data security risks and accelerating adoption of secure information management solutions.

Market Dynamics

Growth Drivers: Rising cybersecurity threats and data breach incidents driving demand for advanced protection solutions globally

The growing number and complexity of cyber attacks have been playing a major role in the rising requirement for highly sensitive information security technologies. Businesses are focusing more on securing their sensitive financial, health care, and other data as cyber attacks that compromise such information keep rising. Furthermore, with the proliferation of digital transformation initiatives, adoption of cloud technologies, and remote working models, businesses have become even more vulnerable to such cyber attacks. This is why many businesses have made investments in various technologies such as encryption, identity and access management, and data loss prevention technologies. In addition, regulatory requirements such as those provided by GDPR, HIPAA, and PCI DSS are also forcing companies to enhance their security architectures.

Restraints: High implementation and integration costs limiting adoption among small and medium-sized enterprises globally

The use of highly sensitive information protection solutions requires considerable initial spending on software, infrastructure, and qualified cybersecurity specialists. High-tech solutions, like encryption solutions, identity and access management systems, and data loss prevention solutions, require maintenance and regular upgrading, which means more costs for ownership in total. SMEs are usually limited in their budgets, preventing them from applying comprehensive security solutions. Additionally, integration of these security measures with legacy software creates an extra challenge and requires further investments. Moreover, employee training and compliance with new regulations complicate matters even further.

Opportunities: Rapid expansion of cloud computing and digital transformation creating strong demand for secure data management solutions

The rapidly growing trend of cloud computing along with digital transformation has created many lucrative opportunities for high-sensitivity information solution providers. Companies have started shifting their crucial IT processes to cloud infrastructure. Thus, there is an increased demand for security technologies that can secure highly sensitive data. The demand for IAM solutions, encryption services, and data loss prevention solutions is very high because of their scalable nature. Also, the use of hybrid clouds and multi-cloud solutions by organizations has made it imperative for companies to secure their data in more complicated ways. The need to secure data in different ways has led to innovations in the field of security as a service solutions and automated threat detection. Another area where the use of data security products is increasing is in digitalization of industries such as BFSI, healthcare, and retail.

Recent Developments:

-

2026: Microsoft expanded Azure Health Data Services, enabling hospitals to store and exchange FHIR-based clinical data securely, while adding AI-driven PHI protection layers and identity-based access controls for sensitive medical records.

-

2026: Oracle enhanced Oracle Health Data Intelligence platform, integrating generative AI with EHR workflows to secure clinical data access, automate documentation, and improve governance for sensitive patient information across hospital networks.

-

2026: Palo Alto enhanced Cortex XSIAM for healthcare, deploying automated threat detection systems specifically targeting hospital EHR networks and medical data breaches, improving response time to ransomware attacks.

-

2025: IBM expanded QRadar healthcare security analytics, deploying AI systems that detect abnormal access patterns in electronic health records and patient data systems across hybrid cloud environments.

High Sensitivity Information Solutions Market Key Players are:

-

Cerner Corporation

-

McKesson Corporation

-

Picis Clinical Solutions

-

iSOFT Group Limited

-

Allscripts Healthcare Solutions

-

CompuGroup Medical

-

Optum

-

Siemens Healthineers

-

Epic Systems

-

IBM Corporation

-

Oracle Corporation

-

Microsoft Corporation

-

Symantec (by Broadcom Inc.)

-

Thales Group

-

Dell Technologies

-

Check Point Software Technologies Ltd.

-

Trend Micro Inc.

-

Palo Alto Networks

-

CyberArk Software Ltd.

-

SailPoint Technologies

High Sensitivity Information Solutions Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.55 Billion |

| Market Size by 2035 | USD 4.32 Billion |

| CAGR | CAGR of 10.78% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution Type (Data Encryption Solutions, Access Control Management, Data Masking Tools, Identity and Access Management (IAM), Data Loss Prevention (DLP)) • By Deployment Model (On-premises Solutions, Cloud-based Solutions, Hybrid Solutions) • By End User Industry (Healthcare, Financial Services, Government and Public Sector, Retail, Education) • By Organizational Size (Small and Medium-sized Enterprises (SMEs), Large Enterprises) • By Compliance and Regulatory Requirements (General Data Protection Regulation (GDPR), Health Insurance Portability and Accountability Act (HIPAA), Payment Card Industry Data Security Standard (PCI DSS), Federal Information Security Management Act (FISMA), California Consumer Privacy Act (CCPA)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cerner Corporation, McKesson Corporation, Picis Clinical Solutions, iSOFT Group Limited, Allscripts Healthcare Solutions, CompuGroup Medical, Optum, Siemens Healthineers, Epic Systems, IBM Corporation, Oracle Corporation, Microsoft Corporation, Symantec (by Broadcom Inc.), Thales Group, Dell Technologies, Check Point Software Technologies Ltd., Trend Micro Inc., Palo Alto Networks, CyberArk Software Ltd., SailPoint Technologies |

Frequently Asked Questions

North America dominated the High Sensitivity Information Solutions Market in 2025.

The Identity and Access Management (IAM) segment dominated the High Sensitivity Information Solutions Market in 2025.

Rising cybersecurity threats and data breach incidents driving demand for advanced protection solutions globally.

The High Sensitivity Information Solutions Market was valued at USD 1.55 billion in 2025.

The High Sensitivity Information Solutions Market is expected to grow at a CAGR of 10.78% from 2026 to 2035.

Get in Touch