High-Speed Camera Market Report Scope & Overview:

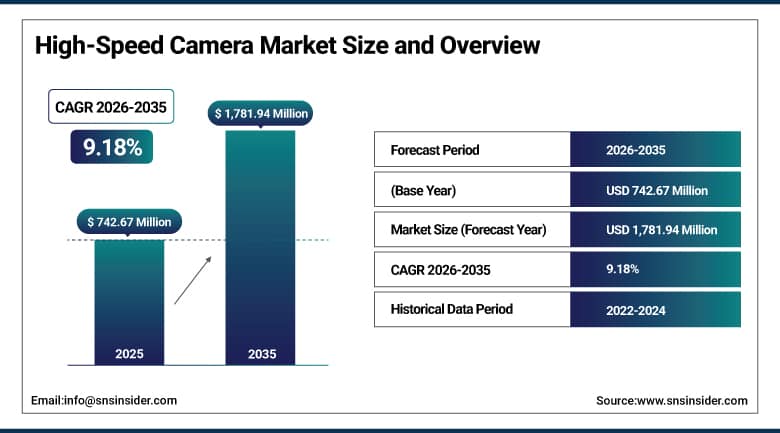

The High-Speed Camera Market was valued at USD 742.67 Million in 2025 and is expected to reach USD 1,781.94 Million by 2035, growing at a CAGR of 9.18% from 2026–2035.

The global high-speed camera market is growing at an exceptional pace. High-speed cameras are specialised imaging systems capable of capturing thousands to millions of frames per second, enabling precise visualisation and analysis of rapid events that conventional cameras cannot resolve. They are essential tools in aerospace testing, automotive crash testing, medical research, materials science, industrial quality control, sports performance analysis, and media production. The market is driven by rising adoption in automotive and aerospace testing, regulatory mandates for crash testing from NHTSA and Euro NCAP, and increasing applications in AI-driven industrial automation requiring real-time motion analysis.

In November 2024, Aconity3D enhanced its PBLM additive manufacturing process stability with Mikrotron EoSens 3.0MCX5 high-speed cameras, enabling real-time parameter analysis during metal powder bed laser melting at frame rates sufficient to capture melt pool dynamics and detect process defects during part fabrication. This innovation improves defect detection and optimises additive manufacturing for broader industrial applications, demonstrating the commercial progression of high-speed camera adoption from standalone testing instruments toward integrated real-time process monitoring systems in advanced manufacturing.

Market Size and Forecast:

-

Market Size in 2026E: USD 810.87 Million

-

Market Size by 2035: USD 1,781.94 Million

-

CAGR: 9.18% from 2026 to 2035

-

Fastest Growing Region: Europe

-

Largest Region: North America

To Get More Information On High-Speed Camera Market - Request Free Sample Report

High-Speed Camera Market Trends:

-

AI integration with high-speed cameras is enabling automated defect detection, motion tracking, and real-time event analysis, improving operational efficiency and reducing manual data review

-

Advancements in CMOS sensor technology are enhancing image quality, sensitivity, dynamic range, and resolution at higher frame rates, expanding high-speed camera applications

-

Compact and portable high-speed camera systems are increasing adoption in field-based applications such as sports analysis, accident investigation, and industrial troubleshooting

-

Growth in additive manufacturing is creating new demand for high-speed cameras used in real-time process monitoring, quality assurance, and production optimization

-

Rising investment in autonomous vehicles and ADAS technologies is driving demand for high-speed imaging systems used in testing, validation, and safety performance analysis

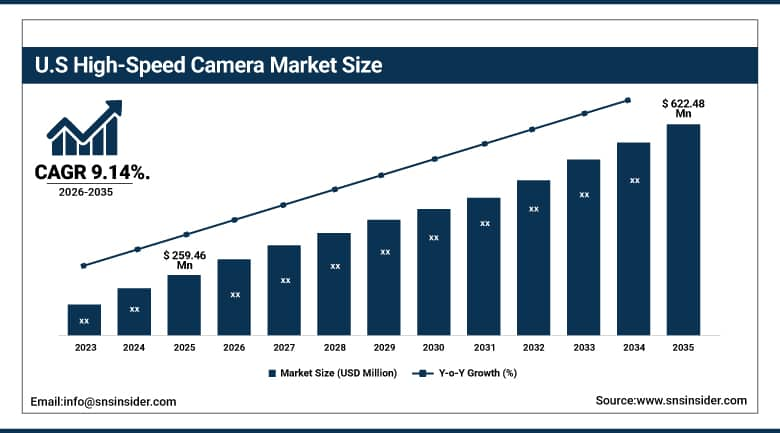

U.S. High-Speed Camera Market Outlook:

The U.S. High-Speed Camera Market was valued at approximately USD 259.46 Million in 2025 and is expected to reach approximately USD 622.48 Million by 2035, growing at a CAGR of approximately 9.14%.

The U.S. is the most commercially significant high-speed camera market within North America’s 40% global revenue dominance. Vision Research (AMETEK), Photron USA, and Phantom high-speed camera brands collectively define the commercial U.S. market. NHTSA’s crash test regulatory mandate creates structured automotive OEM and testing laboratory high-speed camera procurement whose NCAP five-star safety programme creates additional voluntary adoption motivation. NASA, DoD, and national laboratory programme’s aerospace and defence testing investment sustains above-average government procurement. Industrial automation’s expansion and AI-driven quality control adoption create growing commercial procurement.

In March 2025, Baumer expanded its sensor portfolio with OE60 and OE40 edge sensors offering precision up to 1μm and advanced connectivity, enhancing flexibility for various industrial high-speed imaging applications. The expansion reflects the commercial momentum of precision industrial imaging whose quality control, process monitoring, and automated inspection applications create growing sensor and camera procurement across discrete and process manufacturing sectors globally.

High-Speed Camera Market Segment Analysis

-

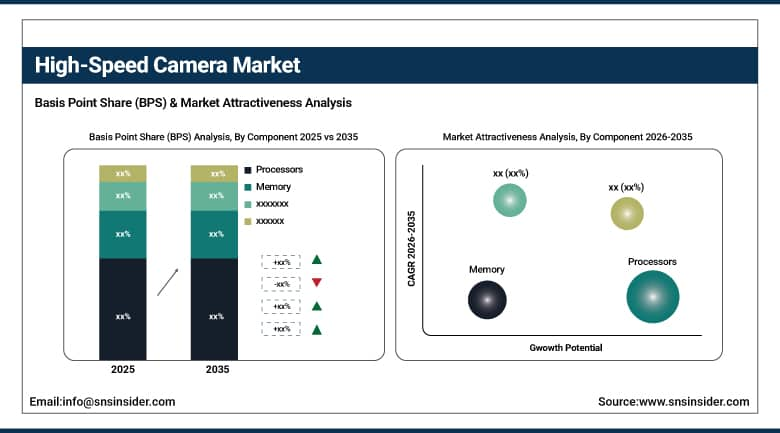

By Component, the Processors segment dominated the High-Speed Camera Market with approximately 34% share in 2025, while the Memory segment is the fastest growing segment.

-

By Frame Rate, the <10,000 FPS segment dominated the High-Speed Camera Market in 2025, while the 30,000–50,000 FPS segment is the fastest growing segment.

-

By Application, the Aerospace & Defence segment dominated the High-Speed Camera Market with 35% share in 2025, while the Healthcare & Life Sciences segment is the fastest growing segment.

By Component, processors dominate, memory grows fastest

Processors retained the dominant component position with approximately 34% of the high-speed camera market in 2025. The processor’s role as the high-speed camera’s computational core whose real-time image acquisition, pixel-level processing, compression, and data management at thousands of frames per second creates the most technically demanding component requirement in the system. High-speed camera processors must handle data rates of tens to hundreds of gigabytes per second while maintaining synchronisation accuracy at microsecond precision whose combined computational requirement defines the processor as the differentiating component whose performance capability determines the system’s maximum achievable frame rate and resolution combination.

Memory is the fastest-growing component because increasing frame rates and resolution demands require progressively larger onboard buffer storage for high-volume image data capture during record events. A 1,000-frame capture at 100,000 FPS in 4K resolution generates terabyte-scale data volumes whose temporary storage in high-speed DRAM or NAND flash buffer memory requires above-standard capacity that grows proportionally with performance specification advancement. Advancements in DRAM and NAND flash technology improving data transfer speeds sustain memory component growth that compounds with overall high-speed camera performance progression.

By Application, aerospace & defence dominates, healthcare grows fastest

Aerospace and defence retained the dominant application position with 35% of the high-speed camera market in 2025. The application’s commercial primacy reflects the non-discretionary testing requirement that aerospace safety certification and defence system performance validation create for high-speed imaging whose technical capability is the only method available for capturing events occurring at millisecond and microsecond timescales. Missile trajectory analysis, ballistics impact testing, aircraft structural response, wind tunnel flow visualisation, and combustion research each create high-speed camera procurement whose per-installation commercial value substantially exceeds consumer and industrial alternatives. Government contract funding creates predictable multi-year procurement relationships that sustain above-average aerospace and defence application revenue contribution.

Healthcare and life sciences is the fastest-growing application because biomechanics research, surgical instrument motion analysis, cardiovascular catheter dynamics, implant performance characterisation, and neuroscience motion capture are creating new medical high-speed camera adoption that compounds with biomedical research funding growth. Each new medical device development programme requiring dynamic performance testing, each clinical biomechanics laboratory, and each sports medicine facility creates high-speed camera procurement whose combined aggregate across the growing biomedical research infrastructure sustains healthcare’s fastest-growing application status.

By Frame Rate, below 10,000 FPS dominates, 30,000-50,000 FPS grows fastest

The sub-10,000 FPS frame rate category retained the dominant position in the high-speed camera market in 2025. This category’s commercial primacy reflects its position as the most commercially accessible entry point for high-speed imaging whose frame rate capability serves the majority of automotive crash testing, consumer product impact testing, industrial quality control, and sports broadcast slow-motion requirements. Automotive crash tests at 1,000-4,000 FPS, component impact tests at 5,000-8,000 FPS, and sports slow-motion capture at 1,000-5,000 FPS collectively represent the application categories whose combined procurement volume creates the sub-10,000 FPS category’s commercial dominance. The category’s competitive pricing relative to ultra-high-speed alternatives sustains its commercial accessibility across the broadest customer range.

The 30,000-50,000 FPS segment is the fastest-growing frame rate category because scientific research, advanced industrial automation, and precision sports analysis applications requiring precise fast-event imaging at frame rates beyond conventional automotive and broadcast requirements create above-average procurement growth. Combustion analysis, detonation research, high-velocity impact studies, and aerodynamic flow visualisation each require frame rates in this range whose growing research application breadth creates procurement demand that compounds with scientific funding and industrial automation investment. Sensor technology advancement making 30,000-50,000 FPS cameras progressively more accessible at commercially viable pricing sustains above-average growth in this previously ultra-premium category.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America High-Speed Camera Market Insights

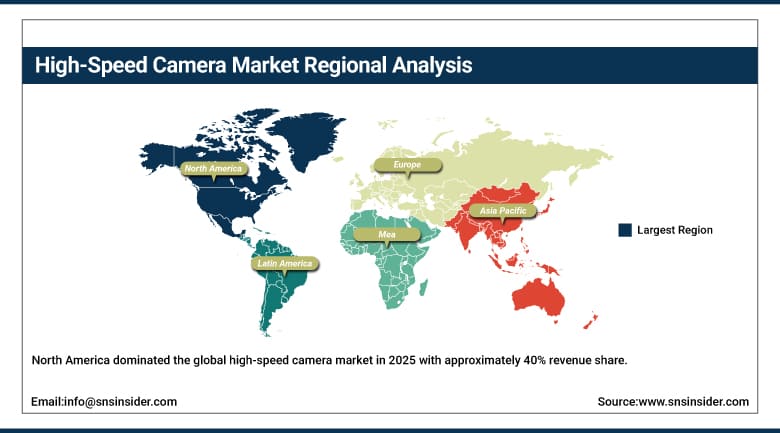

North America dominated the global high-speed camera market in 2025 with approximately 40% revenue share. The United States accounts for approximately 87.4% of North American revenues through Vision Research’s Phantom camera dominance, NASA and DoD’s aerospace and defence procurement, NHTSA’s crash test mandate creating automotive OEM high-speed imaging investment, and the automotive and aerospace testing laboratory infrastructure.

Canada contributes approximately 12.6% of North American revenues through its aerospace testing infrastructure, university research programme procurement, and the automotive manufacturing sector’s quality control investment creating consistent high-speed camera demand.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe High-Speed Camera Market Insights

Europe is the fastest-growing regional high-speed camera market, driven by Euro NCAP’s progressive crash test rating system creating automotive OEM high-speed imaging investment, the aerospace and defence sector’s testing infrastructure, and industrial automation’s above-average adoption across German and Nordic manufacturing. Germany accounts for approximately 22.3% of European revenues through its automotive OEM sector’s crash test investment, Fraunhofer Institute’s research programme procurement, and the industrial machinery sector’s quality control imaging adoption.

The United Kingdom and France are significant secondary markets where aerospace testing facilities, Formula 1 motorsport engineering’s high-speed imaging investment, and Airbus’ aerodynamic testing procurement create consistent above-average high-speed camera demand.

Asia Pacific High-Speed Camera Market Insights

Asia Pacific is a growing high-speed camera market, driven by China’s automotive industry’s crash test investment, Japan’s advanced manufacturing and robotics sector’s quality control adoption, South Korea’s electronics manufacturing inspection, and India’s growing aerospace and defence programme. China accounts for approximately 44.8% of Asia Pacific revenues through its automotive manufacturing scale, government aerospace programme’s testing infrastructure, and industrial automation investment.

Japan represents a technically sophisticated secondary market where the automotive industry’s precision engineering, the electronics manufacturing sector’s quality control, and the robotics industry’s motion analysis create consistent above-average per-unit high-speed camera specification.

MEA & Latin America High-Speed Camera Market Insights

UAE leads MEA revenues at approximately 38.4% through its aerospace and defence sector’s testing investment, the Formula 1 related motorsport engineering, and the growing manufacturing sector’s quality control adoption. Brazil leads Latin American revenues at approximately 44.2% through its automotive manufacturing sector’s crash test investment, the aerospace programme’s Embraer-related testing infrastructure, and the growing industrial automation sector.

Saudi Arabia’s defence programme and South Africa’s automotive manufacturing create significant MEA secondary markets whose high-speed camera procurement reflects the respective national industrial investment priorities.

Market Dynamics:

Growth Drivers: Automotive and aerospace regulatory testing mandates and AI-driven industrial quality control creating systematic procurement

Automotive crash test regulatory mandates are the high-speed camera market’s most commercially certain growth driver. NHTSA’s Federal Motor Vehicle Safety Standards, Euro NCAP’s five-star rating system, and NCAP programmes across Asia Pacific collectively require automotive OEM crash testing whose documentation requires high-speed imaging at frame rates sufficient to capture occupant restraint system activation, structural deformation, and intrusion measurement at time resolutions conventional cameras cannot provide. Each new vehicle programme requiring regulatory crash certification creates high-speed camera procurement whose commercial scale sustains automotive’s consistent contribution to market demand.

AI-driven industrial quality control is creating a new systematic high-speed camera adoption pathway whose integration with machine vision inspection platforms creates real-time defect detection capability that conventional imaging cannot achieve for fast-moving production line objects. Each manufacturing line that integrates high-speed camera machine vision creates procurement whose recurring consumable and service revenue compounds with the industrial automation investment pace across global manufacturing sectors. The additive manufacturing sector’s melt pool monitoring application, demonstrated by Aconity3D’s Mikrotron camera integration, creates a new application category whose adoption will compound with advanced manufacturing technology proliferation.

Restraints: High equipment cost and large data volume management complexity

High-speed camera system cost, ranging from tens of thousands to hundreds of thousands of dollars for advanced systems, creates adoption barriers in cost-sensitive research and industrial environments where the specific testing requirement frequency does not justify permanent high-speed camera ownership. Each organisation that requires occasional high-speed imaging creates rental and service bureau procurement preference over capital ownership whose cost structure creates a portion of market demand that commercial equipment ownership does not capture.

Large data volume management complexity creates post-capture workflow challenges for organisations whose IT infrastructure and analysis software capability is not sized for the terabyte-scale data volumes that extended high-frame-rate capture sessions generate. Each high-speed camera deployment that lacks adequate data storage, transfer bandwidth, and analysis software creates operational bottlenecks whose constraint on productive image capture limits the return on camera investment.

Opportunities: Medical imaging and autonomous vehicle testing creating new procurement categories

Medical high-speed imaging represents a growing premium application whose biomechanics research, surgical instrument characterisation, and implant performance testing create procurement at healthcare institutions whose research funding creates structured annual equipment budgets. Each new medical school biomechanics laboratory and each medical device company’s performance testing facility creates high-speed camera procurement whose healthcare premium pricing sustains above-market revenue per installation.

Autonomous vehicle testing and ADAS sensor validation creates growing high-speed camera demand for pedestrian detection algorithm development, LiDAR point cloud validation against high-speed visual ground truth, and crash avoidance system performance certification. Each AV development programme that requires high-speed imaging for safety system validation creates procurement that compounds with the growing number of active AV development programmes across automotive OEMs and technology companies globally.

Recent Developments:

-

2024: Aconity3D enhanced its PBLM additive manufacturing process stability in November 2024 using Mikrotron EoSens 3.0MCX5 high-speed cameras for real-time parameter analysis during metal powder bed laser melting, enabling defect detection and process optimisation in advanced industrial manufacturing.

-

2025: Baumer expanded its sensor portfolio in March 2025 with OE60 and OE40 edge sensors offering 1μm precision and advanced connectivity, enhancing flexibility for industrial high-speed imaging applications requiring sub-micron measurement accuracy.

-

2025: In February 2025, iX Cameras launched a new generation ultra-compact high-speed camera series targeting field deployment for automotive testing, sports performance analysis, and industrial quality control applications requiring portable high-frame-rate imaging capability in non-laboratory environments.

High-Speed Camera Market Key Players:

-

Vision Research Inc. (AMETEK Inc.)

-

Photron USA Inc.

-

Mikrotron GmbH

-

iX Cameras Ltd.

-

Olympus Corporation

-

Fastec Imaging Corporation

-

nac Image Technology

-

WEISSCAM GmbH

-

DEL Imaging Systems LLC

-

Baumer Group

-

Motion Capture Technologies

-

AOS Technologies AG

-

Shimadzu Corporation

-

Integrated Design Tools (IDT)

-

Revealer

-

RedLake (Integrated Design Tools)

-

Kirana (Specialised Imaging)

-

Stanford Photonics

-

Optronis GmbH

-

FMBC LLC

High-Speed Camera Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 742.67 Million |

| Market Size by 2035 | USD 1781.94 Billion |

| CAGR | CAGR of 9.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Image Sensors, Processors, Memory, Lens, Fan & Cooling, Others) • by Frame Rate (<10,000 FPS, 10,000–30,000 FPS, 30,000–50,000 FPS, >50,000 FPS) • by Application (Aerospace & Defence, Automotive & Transportation, Healthcare & Life Sciences, Media & Entertainment, Industrial Automation, Scientific Research, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Vision Research Inc. (AMETEK Inc.), Photron USA Inc., Mikrotron GmbH, iX Cameras Ltd., Olympus Corporation, Fastec Imaging Corporation, nac Image Technology, WEISSCAM GmbH, DEL Imaging Systems LLC, Baumer Group, Motion Capture Technologies, AOS Technologies AG, Shimadzu Corporation, Integrated Design Tools (IDT), Revealer, RedLake (Integrated Design Tools), Kirana (Specialised Imaging), Stanford Photonics, Optronis GmbH, FMBC LLC |

Frequently Asked Questions

The High-Speed Camera Market is expected to grow at a CAGR of 9.18% from 2026 to 2035.

The High-Speed Camera Market was valued at USD 742.67 Million in 2025.

Automotive crash test regulatory mandates from NHTSA and Euro NCAP creating systematic high-speed imaging procurement, and AI-driven industrial quality control creating new systematic adoption pathways for real-time defect detection on high-speed production lines.

Aerospace & Defence dominated the High-Speed Camera Market with 35% share in 2025, while the Healthcare & Life Sciences segment is the fastest growing.

North America dominated the High-Speed Camera Market in 2025 with approximately 40% revenue share, while Europe is the fastest-growing region.

Get in Touch