Medical Second Opinion Market Report Scope & Overview:

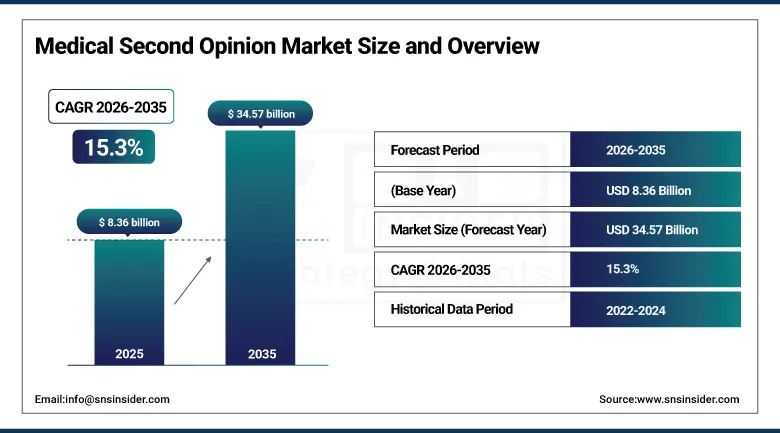

The Medical Second Opinion Market was valued at USD 8.36 Billion in 2025 and is expected to reach USD 34.57 Billion by 2035, growing at a CAGR of 15.3% from 2026–2035.

The Medical Second Opinion Market is expanding owing to an increase in cases of chronic and critical illnesses such as cancer, heart problems, and neurological diseases, among others, thus the need to confirm diagnosis and treatments. Increasing awareness among patients and their need for reliable and professional medical advice is fueling this market growth. Advances in telemedicine and digitized health platforms have improved access to specialist advice around the world. Moreover, increasing healthcare costs have prompted patients to seek second opinion on their treatments for making informed choices.

According to the World Health Organization (WHO), non-communicable diseases (NCDs) cause approximately 41 million deaths annually, accounting for around 74% of global deaths, highlighting the massive burden of chronic conditions that often require specialist evaluation and treatment validation. WHO also reports that cancer causes nearly 10 million deaths per year globally, while cardiovascular diseases account for approximately 17.9 million deaths annually, making them the leading cause of mortality worldwide.

Medical Second Opinion Market Size and Forecast

-

Market Size in 2026E: USD 9.64 Billion

-

Market Size by 2035: USD 34.57 Billion

-

CAGR: 15.3% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Medical Second Opinion Market - Request Free Sample Report

Medical Second Opinion Market Trends

-

AI-powered diagnostic review platforms are enabling faster specialist matching and automated medical record summarisation for second opinion case preparation.

-

Employer-sponsored second opinion benefits are expanding as corporations document medical cost savings and treatment plan optimisation from specialist case review programmes.

-

Oncology second opinion demand is surging as precision medicine’s treatment complexity creates patient and oncologist motivation for multidisciplinary case validation.

-

International medical tourism for second opinions is growing as cost differentials and specialist availability attract cross-border patients to academic medical centres.

-

Real-time digital pathology and radiology image transfer is enabling remote second opinion services that match the quality of in-person specialist review.

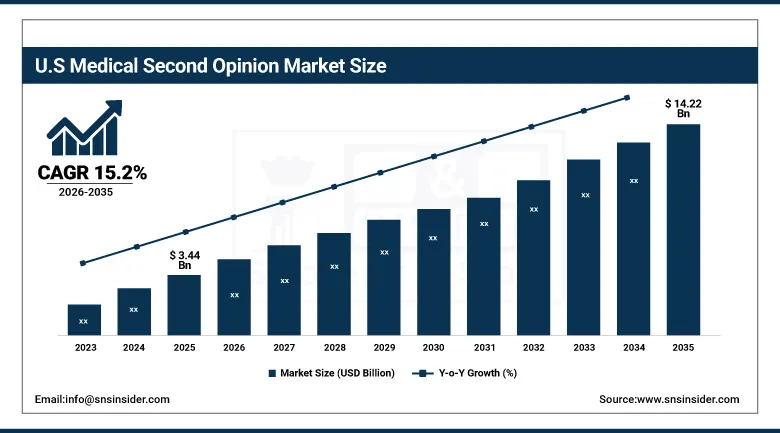

The U.S. Medical Second Opinion Market Outlook

The U.S. Medical Second Opinion Market was valued at approximately USD 3.44 Billion in 2025 and is expected to reach approximately USD 14.22 Billion by 2035, growing at a CAGR of approximately 15.2%.

The United States leads the global medical second opinion market through its high healthcare expenditure per capita, the world’s most extensive employer-sponsored health benefit ecosystem, and the concentration of world-leading academic medical centres including Cleveland Clinic, Mayo Clinic, and Johns Hopkins whose specialist reputation sustains demand for their remote and in-person second opinion programmes.

U.S. National Cancer Institute reports approximately 2 million new cancer cases annually, further reinforcing the demand for expert medical second opinions in oncology care. These factors collectively highlight the growing reliance on specialist consultation services for accurate diagnosis, treatment validation, and improved clinical decision-making.

Medical Second Opinion Market Segment Analysis

-

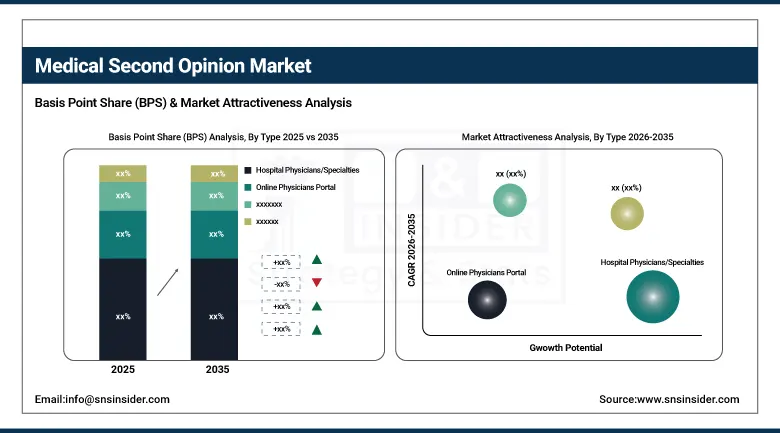

By Type, Hospital Physicians/Specialties segment dominated the Medical Second Opinion Market in 2025 with 41.6% share; Medical Second Opinion Companies segment is the fastest growing segment.

-

By Source of Service, In-House segment dominated the market in 2025 with 57.8% share; Outsourced segment is the fastest growing segment.

-

By Application, Cancer segment dominated the market in 2025 with 38.4% share; Neurological Disorders segment is the fastest growing segment.

By Type, hospital physicians and specialty doctors dominate the market, while medical second opinion companies are the fastest-growing segment

Hospital physicians and specialty doctors dominated the Medical Second Opinion Market due to the high clinical skills, interaction with patients, and established relationships of hospital physicians and specialty doctors. Patients feel more confident when dealing with in-hospital physicians since they have all necessary information about patients' health status. This makes the process of diagnosis much easier because these specialists can use all their knowledge gained from working in various disciplines. They also provide better coordination and sound clinical judgment.

Medical second opinion companies are the fastest-growing segment owing to the increasing number of digital healthcare solutions and higher preference of remote consultations among the specialists. These organizations facilitate easy contact between patients and the best healthcare providers around the world. This trend is facilitated by increased awareness of different types of diseases, growth of telemedicine services, and wider availability of internet. Patients show more interest in using these services because of convenience and privacy.

By Source of Service, in-house segment dominates the medical second opinion market, while outsourced services is the fastest-growing segment

The in-house segment dominated the Medical Second Opinion Market due to the tendency of patients who opt to get an in-house second opinion as it allows doctors to work together within a hospital setting and makes communication easier between general practitioners and specialists. It allows for the provision of coordinated care, proper medical documentation, and faster clinical decision-making process. Moreover, it allows for easy access to state-of-the-art diagnostic equipment.

Outsourced services are the fastest-growing segment due to the increase in demand for flexible and technology-based medical consultation methods. The demand for expert medical opinions from other specialists has been growing among patients and medical professionals, especially in complex cases. Outsourcing allows people to access specialists from around the world while at the same time reducing costs and turnaround time. Growth in telemedicine technology is expected to fuel its expansion even further.

By Application, cancer dominates the medical second opinion market, while neurological disorders is the fastest-growing segment

Cancer dominated the Medical Second Opinion Market owing to the increased prevalence of the disease and complexity associated with its diagnosis and treatment. Seeking expert opinions is common amongst cancer patients in order to have confirmation about their diagnoses, get information regarding more advanced treatments available, and enhance chances of living longer after the condition. Cancer is considered to require multidisciplinary opinions from experts, thus boosting growth in demand in the market.

Neurological disorders are the fastest-growing segment because of the rising incidence rate of several neurological diseases such as Alzheimer's, Parkinson's, and epilepsy. Besides, the complexity of neurological diseases and the scarcity of specialized neurologists in certain regions contribute to the need for patients to seek second opinions from other experts. Increased awareness regarding benefits of early diagnoses and development in neuro-imaging techniques are also contributing to the growth in the segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

India |

34.2% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

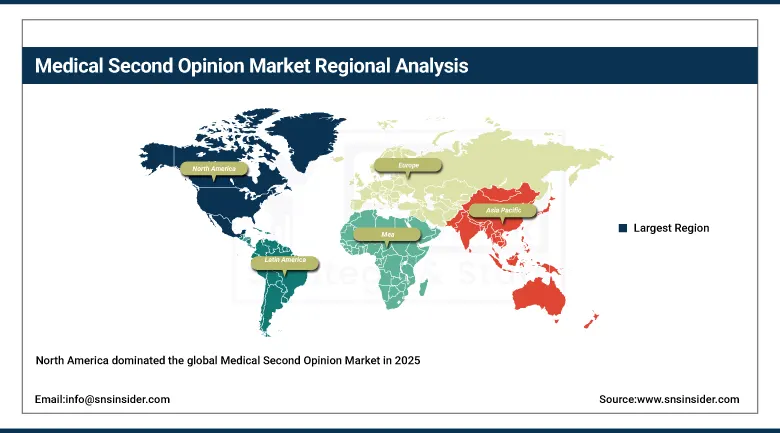

North America Medical Second Opinion Market Insights

North America dominated the global Medical Second Opinion Market in 2025, driven by the world’s most extensive employer-sponsored health benefits ecosystem and the concentration of academic medical centres whose specialist reputation creates global demand for their second opinion programmes. The United States accounts for approximately 82.5% of North American revenues through Teladoc Health’s Expert Medical Opinion, Included Health’s Grand Rounds platform, and 2nd.MD’s specialist consultation service, which together serve the majority of Fortune 500 employer-sponsored second opinion benefit programmes.

According to the U.S. Centers for Disease Control and Prevention (CDC), an estimated 60 percent of adults within the United States have a minimum of one chronic condition, which increases the necessity for a specialist consultation to diagnose their medical conditions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Medical Second Opinion Market Insights

Europe is a significant medical second opinion market where universal healthcare systems’ specialist referral delays, cross-border patient mobility rights under EU directive 2011/24/EU enabling reimbursed treatment in other member states, and the concentration of world-class academic medical centres collectively create structural second opinion demand. Germany accounts for approximately 22.4% of European revenues through its large private supplementary health insurance sector’s second opinion coverage, the Charité and Heidelberg University Hospital’s international patient second opinion programmes, and the high healthcare expenditure per capita that sustains premium specialist consultation services.

According to Eurostat, around 21% of the European Union population is aged 65 or older, a demographic trend that significantly increases the prevalence of chronic conditions and the need for specialist medical evaluations and second opinions.

Additionally, the World Health Organization (WHO) Europe reports that chronic diseases account for over 80% of deaths in the region, underscoring the heavy disease burden and sustained demand for accurate diagnosis, treatment validation, and expert clinical decision-making. These factors continue to drive the adoption of medical second opinion services across Europe.

Asia Pacific Medical Second Opinion Market Insights

Asia Pacific is the fastest-growing regional medical second opinion market, driven by the region’s rapidly expanding middle class seeking quality healthcare validation, medical tourism’s established infrastructure for international specialist consultation, and growing insurance coverage for specialist second opinion services. India accounts for approximately 34.2% of Asia Pacific revenues through its large medical tourism sector attracting international patients for second opinions at Apollo Hospitals, Fortis Healthcare, and Manipal Hospitals, and the domestic specialist consultation market serving a population increasingly aware of diagnostic error risk.

China’s growing private health insurance sector’s specialist consultation benefits, Japan’s digital health platform investment in second opinion services, and South Korea’s internationally recognised oncology and cardiac surgery centres’ second opinion programmes collectively sustain Asia Pacific’s fastest-growing regional trajectory. Southeast Asian markets including Thailand and Singapore contribute premium regional demand through established international hospital second opinion infrastructure serving both domestic and international patients.

MEA & Latin America Medical Second Opinion Market Insights

The UAE leads MEA revenues at approximately 22.8% through its world-class healthcare infrastructure, the Dubai and Abu Dhabi Departments of Health’s telemedicine regulation enabling digital specialist consultations, and the large expatriate population’s health insurance coverage including specialist second opinion benefits. Saudi Arabia contributes growing regional demand through Vision 2030 healthcare quality investment and the government’s health insurance expansion creating reimbursement-supported second opinion access.

According to the World Health Organization (WHO) Eastern Mediterranean Region (EMRO), non-communicable diseases account for more than 70% of all deaths in the region, highlighting a substantial burden of chronic conditions that require long-term management and specialist evaluation.

Brazil leads Latin American revenues at approximately 43.8% through its large private health insurance sector’s growing specialist consultation benefit adoption, the academic medical centre infrastructure at Hospital das Clínicas and Sirio-Libanes Hospital offering structured second opinion programmes, and growing healthcare consumerism among Brazil’s expanding middle class. Mexico and Colombia contribute growing secondary market demand through their private insurance sectors’ specialist benefit development and the medical tourism infrastructure serving both domestic and international second opinion seekers.

Pan American Health Organization (PAHO) reports that chronic diseases are responsible for approximately 75% of deaths in Latin America, further emphasizing the widespread impact of non-communicable diseases. These high disease burdens across regions continue to drive the need for medical second opinions to support accurate diagnosis, treatment validation, and improved patient outcomes.

Market Dynamics

Growth Drivers: Rising healthcare consumerism and digital platform accessibility eliminating geographic barriers to specialist second opinion consultation

The medical second opinion market’s exceptional growth rate is driven by the structural alignment of three simultaneously advancing forces: rising patient health literacy creating demand for diagnostic validation, digital health platforms eliminating geographic and logistical barriers to specialist access, and employer and insurer recognition that specialist second opinion services generate measurable medical cost savings through avoided unnecessary procedures and optimised treatment selection.

The documented 40% prevalence of significant diagnosis or treatment modification following specialist second opinion review across complex medical conditions creates compelling clinical and financial motivation that sustains demand independent of economic cycles. Each unnecessary surgery avoided, chemotherapy regimen optimised for correct tumour subtype, or rare disease correctly identified at first specialist review generates medical cost savings that substantially exceed the second opinion consultation fee.

Restraints: Insurance reimbursement gaps and physician resistance creating adoption barriers for formal second opinion programmes in standard clinical practice

Inconsistent insurance reimbursement coverage for second opinion consultations across health plans, payer types, and jurisdictions creates financial barrier uncertainty that suppresses patient utilisation of second opinion services whose out-of-pocket cost without reimbursement may be prohibitive for income constrained patients.

Primary physician resistance to second opinion seeking, where some clinicians interpret patient pursuit of specialist review as a confidence vote of no confidence in their clinical judgment, creates a communication barrier that suppresses second opinion utilisation in patient populations whose deference to physician authority limits assertive healthcare advocacy. The administrative burden of medical record compilation, imaging file transfer, and specialist scheduling coordination creates a utilisation friction that self-directed patients without institutional second opinion service support find discouraging relative to accepting the original diagnosis.

Opportunities: AI-powered proactive second opinion identification and emerging market medical tourism infrastructure creating high-growth commercial frontiers

AI-powered clinical decision support systems that identify high-risk diagnoses with elevated specialist modification rates from electronic health record data and proactively offer patients access to specialist second opinion review represent the most commercially transformative capability advancement in the medical second opinion market. Each employer health plan or insurance programme that deploys proactive AI identification of second opinion candidates expands service utilisation from the 1 to 3% self-selecting utilisation typical of voluntary benefit programmes toward the 15 to 25% utilisation achievable through proactive outreach to clinically appropriate cases. Emerging market medical tourism infrastructure investment creating internationally accredited hospitals in India, Thailand, Malaysia, and the UAE with specialist second opinion programme development creates a growing commercial infrastructure serving both domestic and international second opinion demand.

Recent Developments:

-

2025: Included Health integrated AI-powered clinical decision support within its Grand Rounds expert medical opinion platform, enabling proactive identification of employer health plan members with diagnoses showing high specialist modification rates for targeted outreach to expand second opinion programme utilisation.

-

2024: Teladoc Health expanded its Expert Medical Opinion service to cover 450 medical conditions across 11 specialties, providing employer-sponsored health plan members with board-certified specialist review through fully digital record submission and video consultation for complex diagnosis validation.

-

2024: Cleveland Clinic launched an enhanced MyConsult Remote Second Medical Opinion digital platform with AI-assisted case routing that automatically matches submitted cases to the highest-appropriate specialty panel based on diagnosis category, imaging modality, and clinical complexity indicators.

Medical Second Opinion Market Key Players are:

-

Teladoc Health Inc.

-

Included Health Inc.

-

2nd.MD Inc.

-

WorldCare International Inc.

-

AXA Health / AXA Global Healthcare

-

Cleveland Clinic

-

Mayo Clinic

-

Johns Hopkins Medicine International

-

Cigna Healthcare

-

Optum

-

PinnacleCare International LLC

-

HCA Healthcare

-

MDLIVE Inc.

-

Alight Solutions

-

MORE Health Inc.

-

Sun Life Health Navigator

-

Accolade Inc.

-

Medisense Healthcare Solutions Pvt. Ltd.

-

Global Second Opinion

-

Second Opinion International

Medical Second Opinion Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.36 Billion |

| Market Size by 2035 | USD 34.57 Billion |

| CAGR | CAGR of 15.3% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hospital Physicians/Specialties, Online Physicians Portal, Medical Second Opinion Companies, Health Insurance Companies) • By Source of Service (Outsourced, In-House) • By Application (Cancer, Cardiac Disorders, Neurological Disorders, Diabetes, Respiratory Disorders, Orthopaedic Disorders, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Teladoc Health Inc., Included Health Inc., 2nd.MD Inc., WorldCare International Inc., AXA Health / AXA Global Healthcare, Cleveland Clinic, Mayo Clinic, Johns Hopkins Medicine International, Cigna Healthcare, Optum, PinnacleCare International LLC, HCA Healthcare, MDLIVE Inc., Alight Solutions, MORE Health Inc., Sun Life Health Navigator, Accolade Inc., Medisense Healthcare Solutions Pvt. Ltd., Global Second Opinion, Second Opinion International |

Frequently Asked Questions

The Medical Second Opinion Market is expected to grow at a CAGR of 15.3% from 2026 to 2035.

The Medical Second Opinion Market was valued at USD 8.36 Billion in 2025.

Rising healthcare consumerism demanding diagnostic validation, digital platform accessibility eliminating geographic barriers to specialist consultation, employer-sponsored benefit adoption generating measurable medical cost savings, and growing oncology treatment complexity creating specialist case review demand are the primary growth factors.

The Cancer segment dominated the Medical Second Opinion Market with the largest share in 2025 through oncology’s treatment complexity and the documented high rate of diagnosis or treatment modification following specialist review.

North America dominated the Medical Second Opinion Market in 2025 through its world-leading employer health benefit ecosystem, academic medical centre concentration, and digital second opinion platform development.

Get in Touch