Hospital Outsourcing Market Report Scope & Overview:

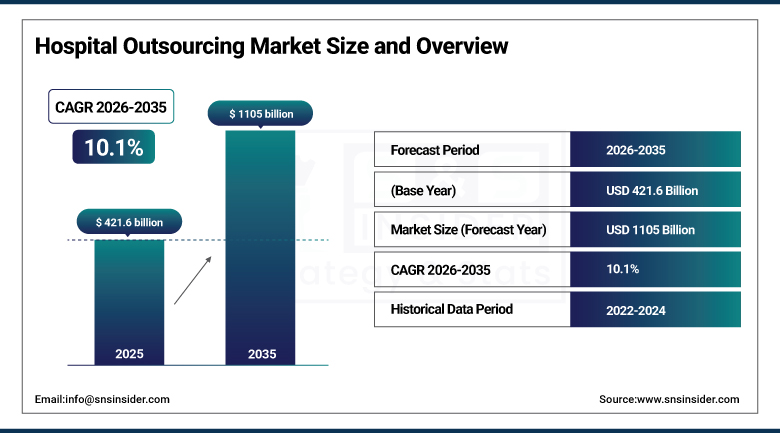

The Hospital Outsourcing Market was valued at USD 421.6 billion in 2025 and is expected to reach USD 1,105 billion by 2035, growing at a CAGR of 10.1% from 2026-2035.

The growth of the Hospital Outsourcing Market can be attributed to increasing healthcare expenditures, rising number of patients, and requirement of efficiency. Non-core activities such as information technology, billing, and facilities management are outsourced by hospitals in order to concentrate on providing treatment and improving quality while reducing operating expenses.

The American Hospital Association's 2024 report documents that hospital employment costs grew by 21% between 2019 and 2023, driven by nursing and physician shortages that required extensive use of contract labor at premium rates. The HFMA's survey of hospital CFOs found that 73% identified cost reduction through outsourcing as a priority strategic initiative for the 2024-2026 planning period.

Hospital Outsourcing Market Size and Forecast

-

Market Size in 2025: USD 421.6 Billion

-

Market Size by 2035: USD 1,105 Billion

-

CAGR: 10.1% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Hospital Outsourcing Market - Request Free Sample Report

Hospital Outsourcing Market Trends

-

AI-powered medical documentation and clinical note generation is rapidly becoming an outsourced service, with platforms like Nuance's DAX Copilot processing millions of patient encounters monthly on behalf of hospital clients.

-

Revenue cycle management outsourcing is accelerating as payer contract complexity, claim denial rates, and coding requirements all grow beyond what hospital internal billing departments can efficiently manage.

-

Pharmacy services outsourcing including specialty pharmacy management, medication therapy management, and 340B program administration is growing as drug cost management becomes a boardroom-level hospital financial priority.

-

Laboratory services outsourcing through national reference laboratories and localized regional lab networks is growing as advanced molecular diagnostics require technical expertise and equipment that small hospital labs cannot economically maintain in-house.

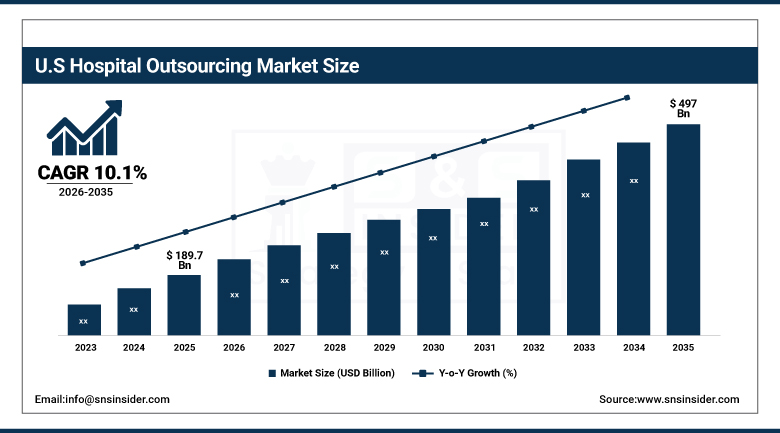

U.S. Hospital Outsourcing Market was valued at USD 189.7 billion in 2025 and is expected to reach USD 497 billion by 2035, growing at a CAGR of 10.1% from 2026-2035.

Outsourcing in the U.S. Hospital industry is due to increased costs in health care, lack of personnel, and the demand for increased efficiency. The hospitals contract with companies for provision of information technology, revenue cycle management, and clinical support services among others.

The U.S. Bureau of Labor Statistics projects registered nurse shortages will reach 194,000 positions by 2031, creating structural staffing challenges that make clinical services outsourcing increasingly attractive.

Hospital Outsourcing Market Segment Analysis

-

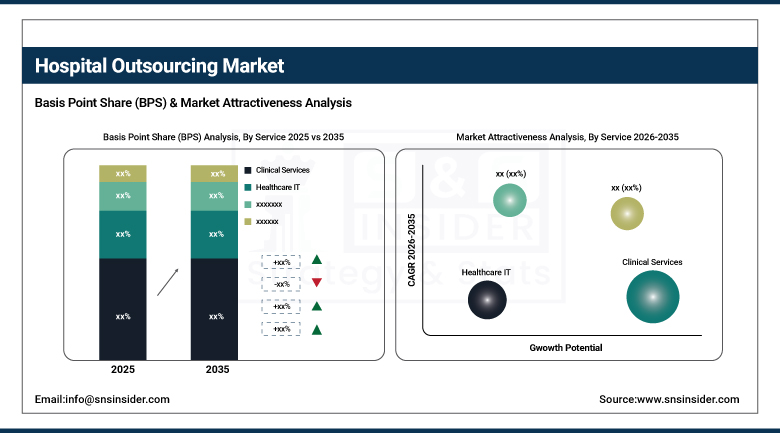

By Service, Clinical Services dominated with ~22% share in 2025; Healthcare IT growing fastest in the Hospital Outsourcing Market.

-

By Type, Private hospital segment dominated the Hospital Outsourcing Market in 2025; Public hospital segment growing with government efficiency programs.

By Service: Clinical Services dominates, Healthcare IT growing fastest

Clinical Services held approximately 22% of the Hospital Outsourcing Market in 2025 and maintained its dominant position in 2025. This reflects the outsourcing penetration of physician specialty services hospitalist programs, emergency medicine groups, anesthesiology practices, and radiology interpretation services are routinely provided by large physician management organizations rather than employed physicians at many hospitals. Envision Healthcare, TeamHealth, and USACS collectively staff emergency departments and hospitalist programs at thousands of U.S. hospitals under service contracts that give hospital operators predictable labor costs and clinical coverage without the administrative complexity of directly employing specialist physicians.

Healthcare IT is growing at the fastest service segment CAGR, driven by multiple parallel technology transformation pressures. Hospital IT departments must simultaneously manage electronic health record implementations and upgrades, cybersecurity threats that target healthcare at above-average rates, AI and automation integration, telemedicine infrastructure, and regulatory reporting systems a technical breadth that small and medium hospital IT teams cannot cover comprehensively. AI-powered medical documentation which requires natural language processing expertise, regulatory compliance understanding, and clinical workflow knowledge that general IT staff do not possess has created an entirely new outsourcing category that scarcely existed five years ago and is now among the fastest-growing hospital IT outsourcing services.

By Type: Private hospitals dominate, Public hospital outsourcing growing

Private hospitals maintained the dominant type position in the Hospital Outsourcing Market throughout 2025, reflecting both the larger share of private hospital beds in developed markets and the commercial imperative that private operators face to manage costs aggressively in competitive healthcare markets. For-profit hospital systems in the U.S. HCA Healthcare, Tenet, and Community Health Systems have historically been among the most aggressive adopters of outsourcing across all service categories, viewing external service providers as cost-efficiency tools that free capital for direct patient care investment. Private hospital operators also have the governance structures boards with commercial orientation, management incentive alignment with financial performance that support outsourcing decisions being made on pure cost-benefit analysis rather than requiring the political navigation that public sector institutional decisions often involve.

Public hospital outsourcing is growing as a share of total market revenue, driven by government healthcare system efficiency initiatives across the UK, Australia, Canada, and developing nations that are seeking to improve public hospital performance without proportional public spending increases. The UK's NHS has significantly expanded outsourcing to independent sector treatment centers for elective procedures, diagnostic services, and support services as it works to reduce record waiting lists. Australia's public hospital system has expanded outsourcing of pathology services, medical imaging, and food service management across state health systems seeking operating cost reductions. In developing markets, public hospital outsourcing of laboratory services, medical equipment maintenance, and pharmaceutical supply chain management is driven by the combination of limited public sector technical capacity and growing healthcare system investment that is pulling in private sector operators.

Hospital Outsourcing Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

United Kingdom |

28% |

|

Asia Pacific |

Australia |

30% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

50% |

North America Hospital Outsourcing Market Insights

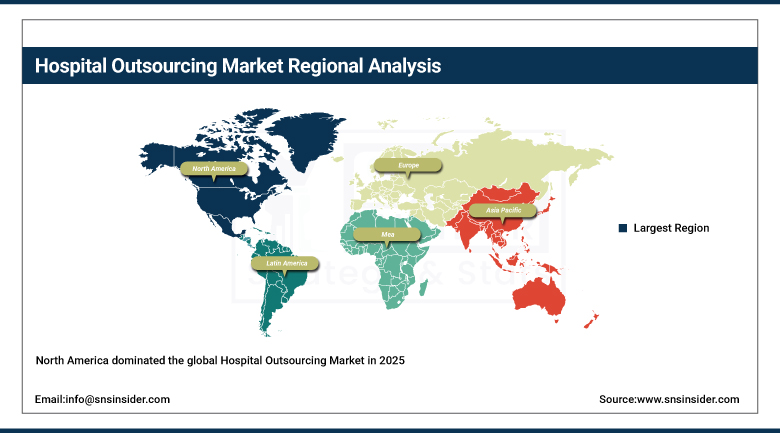

North America dominated the global Hospital Outsourcing Market in 2025 and will maintain its leadership through the forecast period, anchored by the U.S. healthcare system's deep institutional adoption of outsourcing across virtually every non-clinical function and an expanding set of clinical services. The concentration of large for-profit hospital systems that treat outsourcing as a financial management strategy sustains high-volume, long-term outsourcing contracts. The growth of private equity investment in healthcare services which typically intensifies outsourcing of non-core functions following acquisition is a structural accelerator of North American hospital outsourcing market growth. Canada's provincial health systems are also expanding outsourcing programs, particularly in imaging and laboratory services, as provinces face fiscal pressure to manage healthcare cost growth without commensurate tax revenue increases.

HFMA's 2024 member survey documents that U.S. hospitals' average revenue cycle management cost as a percentage of net revenue declined from 4.2% to 3.1% for hospitals using outsourced RCM providers compared to full in-house operations, representing a significant financial justification for RCM outsourcing adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Hospital Outsourcing Market Insights

Europe's hospital outsourcing market is characterized by the NHS's significant and growing outsourcing programs in the UK, national health system efficiency initiatives across Germany and France, and the expansion of private healthcare outsourcing in Eastern European markets where private hospital development is growing rapidly. The UK's NHS spent over GBP 10 billion on outsourced services in 2023, making it one of the world's largest single buyers of hospital outsourcing services. NHS England's Independent Sector Treatment Centre program which contracts with private providers to deliver elective surgical procedures and diagnostic services on behalf of NHS patients represents a large and strategically important hospital outsourcing model that is being expanded as NHS waiting list pressures intensify. Germany's hospital reform program, which is restructuring hospital specialization and funding, is driving consolidation and outsourcing as smaller hospitals rationalize non-core service delivery to focus on their designated clinical specialties.

Asia Pacific Hospital Outsourcing Market Insights

Asia Pacific is the fastest-growing regional Hospital Outsourcing Market, driven by rapidly expanding private hospital sectors across India, Southeast Asia, and China, government healthcare system efficiency initiatives in Australia and Japan, and the growing complexity of hospital operations as these markets adopt advanced clinical technologies. India's private hospital sector anchored by Apollo Hospitals, Fortis, and Max Healthcare represents the region's most commercially active outsourcing buyer, with environmental services, revenue cycle management, dietary services, and equipment maintenance all routinely outsourced across major private hospital networks. Australia's public hospital system has a well-developed outsourcing tradition in pathology services and medical imaging, with Healius and Sonic Healthcare providing outsourced diagnostic services to public hospitals under state health department contracts. China's healthcare reform programs are creating growing private hospital sector development that will expand hospital outsourcing demand significantly through the forecast period.

India's private hospital sector generated revenue of approximately USD 53 billion in 2023 and is growing at 15% annually, with outsourcing of non-clinical services representing an estimated 12-15% of total operating expenditure across major private hospital networks.

Middle East & Africa and Latin America Hospital Outsourcing Market Insights

The Middle East is the MEA region's dominant hospital outsourcing market, with the UAE and Saudi Arabia leading adoption through their large modern private hospital sectors and Vision 2030 healthcare system transformation programs. Dubai's Health Authority and Abu Dhabi's Department of Health have both implemented programs attracting international hospital management companies that bring outsourcing expertise alongside clinical capability. Saudi Arabia's Public Investment Fund is funding hospital development programs where international operators are contracted as management partners who bring full operational outsourcing expertise to newly constructed facilities. In Africa, hospital outsourcing is most developed in South Africa's private hospital sector — Mediclinic, Netcare, and Life Healthcare outsource laboratory, dietary, and support services extensively while public sector outsourcing in Sub-Saharan Africa is in its early stages, primarily involving laboratory diagnostic services where international organizations support government health systems. Latin America's market is dominated by Brazil and Mexico, where private hospital networks and public health system efficiency programs both drive outsourcing adoption.

Hospital Outsourcing Market Growth Drivers:

-

Healthcare cost pressure and staffing shortages driving accelerating hospital outsourcing adoption globally

The hospital outsourcing market's growth is being powered by financial pressure that is both immediate and structural. Hospital operating costs particularly labor costs have grown faster than revenue in most developed healthcare markets for the past five years, creating margin pressure that makes cost reduction a first-priority strategic imperative rather than a secondary financial management consideration. Nursing and physician shortages simultaneously make internal staffing of many functions more expensive and less reliable than outsourcing to specialist providers who can aggregate demand across multiple client hospitals and maintain more stable staffing pools. Technology complexity has added another dimension: the growing technical sophistication of healthcare IT, AI-powered clinical documentation, and cybersecurity requirements has exceeded the capability of most hospital IT departments, creating outsourcing demand for services that did not exist as categories a decade ago. Each of these cost, staffing, and technology pressures is durable and growing, sustaining outsourcing market growth that is not dependent on any single structural change to resolve.

Hospital Outsourcing Market Restraints:

-

Data security vulnerabilities and integration complexity creating significant challenges for hospital outsourcing adoption

Hospital outsourcing faces a trust challenge that is uniquely acute in healthcare: the data that must be shared with service providers includes some of the most sensitive personal information any organization possesses patient medical records, diagnoses, treatment histories, mental health records, and genomic data. The consequences of a data breach at an outsourced hospital services provider are not merely reputational and financial; they directly affect patient privacy in ways that can cause lasting harm. The 2024 Change Healthcare breach which exposed protected health information for potentially 190 million Americans through a cyberattack on a revenue cycle management outsourcing company demonstrated at scale what can go wrong when healthcare organizations outsource to providers with inadequate security infrastructure. This incident prompted significant reassessment of hospital outsourcing due diligence requirements and pushed cybersecurity qualification to the center of vendor selection processes.

Hospital Outsourcing Market Opportunities:

-

AI-powered clinical documentation and pharmacy management outsourcing creating significant hospital market growth opportunities

AI-powered clinical documentation represents the most commercially active frontier of hospital outsourcing market growth. Physician administrative burden estimated to consume 2 hours of documentation for every 1 hour of patient care is the leading driver of physician burnout and one of the most commonly cited reasons physicians leave clinical practice. Ambient AI documentation systems that listen to clinical encounters and automatically generate structured medical notes, discharge summaries, and referral letters address this burden directly, and they work most effectively as managed services where the AI platform, medical terminology optimization, regulatory compliance, and integration with the EHR are all handled by the outsourcing provider. Nuance's DAX Copilot, Augmedix, and Suki AI are competing for the largest commercial opportunity in healthcare IT outsourcing that has emerged in a generation.

Recent Developments:

-

2026: Optum Health expanded its hospital RCM outsourcing platform to integrate real-time payer policy monitoring that automatically updates coding rules and denial prevention protocols when payer coverage policies change reporting a 28% reduction in preventable denial rates for hospitals on the integrated platform versus the industry average of 9-12% denial rates for hospitals managing payer policy changes manually.

-

2025: Aramark Healthcare expanded its Environmental Services outsourcing program to include AI-powered room turnover analytics that use computer vision to verify cleaning completion, track high-touch surface disinfection compliance, and predict staffing requirements based on patient discharge patterns reducing hospital-acquired infection rates by 14% across its managed facilities.

Hospital Outsourcing Market Key Players

Some of the Hospital Outsourcing Market Companies

-

Sodexo S.A.

-

Aramark Corporation

-

Optum Inc. (UnitedHealth Group)

-

R1 RCM Inc.

-

Conifer Health Solutions

-

Parallon Business Solutions (HCA)

-

TeamHealth Holdings LLC

-

Envision Healthcare Corp.

-

ABM Industries Inc.

-

Healtheon Capital Group

-

Siemens Healthineers AG

-

GE HealthCare Technologies Inc.

-

Philips Healthcare

-

Accenture plc

-

Conduent Business Services LLC

-

ISS A/S

-

Wipro Limited

-

Cognizant Technology Solutions

-

Infosys BPM Ltd.

-

Teleradiology Solutions

Hospital Outsourcing Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 421.6 Billion |

| Market Size by 2035 | USD 1,105 Billion |

| CAGR | CAGR of 10.1% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service (Healthcare IT, Transportation Services, Clinical Services, Business Services, Others) • By Type (Public, Private) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sodexo S.A., Aramark Corporation, Optum Inc. (UnitedHealth Group), R1 RCM Inc., Conifer Health Solutions, Parallon Business Solutions (HCA), TeamHealth Holdings LLC, Envision Healthcare Corp., ABM Industries Inc., Healtheon Capital Group, Siemens Healthineers AG, GE HealthCare Technologies Inc., Philips Healthcare, Accenture plc, Conduent Business Services LLC, ISS A/S, Wipro Limited, Cognizant Technology Solutions, Infosys BPM Ltd., Teleradiology Solutions |

Frequently Asked Questions

Ans: The Private hospital segment dominated the Hospital Outsourcing Market in 2025.

Ans: North America dominated the Hospital Outsourcing Market in 2025.

Ans: Clinical Services dominated with approximately 22% share in 2025; Healthcare IT is the fastest growing service segment.

Ans: The Hospital Outsourcing Market was valued at USD 421.6 billion in 2025.

Ans: The Hospital Outsourcing Market is expected to grow at a CAGR of 10.1% from 2026 to 2035.

Get in Touch