Healthcare Revenue Cycle Management Market Report Scope & Overview:

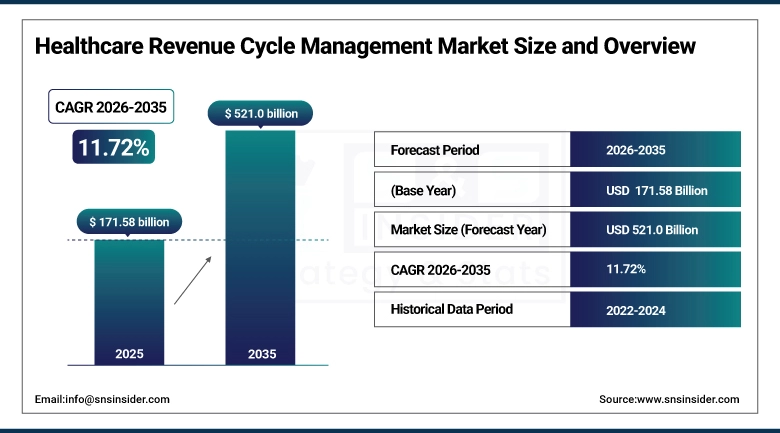

The Healthcare Revenue Cycle Management Market was estimated at USD 171.58 Billion in 2025 and is expected to reach USD 521.0 Billion by 2035 and grow at a CAGR of 11.72% over the forecast period of 2026-2035.

Factors influencing the adoption of revenue cycle management solutions in the healthcare industry include high healthcare costs, complicated billing procedures, and an increase in the number of patients. Digital health solutions, automation, and the use of AI for coding are contributing towards efficiency and lower claims denials. Regulations and value-based care initiatives are key drivers as well.

The Healthcare Financial Management Association (HFMA) reports that U.S. hospitals collectively spend approximately USD 1.2 billion annually on billing and collections administrative costs. The American Hospital Association estimates that claim denials cost U.S. hospitals over USD 262 billion annually in lost revenue, rework costs, and administrative overhead the single largest category of preventable revenue loss in U.S. healthcare.

Market Size and Forecast:

-

Market Size in 2025: USD 171.58 Billion

-

Market Size by 2035: USD 521.0 Billion

-

CAGR: 11.72% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Healthcare Revenue Cycle Management Market - Request Free Sample Report

Healthcare Revenue Cycle Management Market Trends:

-

AI-powered claim scrubbing and denial prediction are reducing first-pass claim rejection rates by identifying coding errors, medical necessity gaps, and authorization failures before claim submission.

-

Value-based care payment model complexity is driving healthcare organizations to invest in RCM platforms capable of tracking bundled payment performance and documenting quality metrics that determine reimbursement levels.

-

Patient financial engagement platforms with digital payment options, payment plans, cost transparency tools, and eligibility estimates are improving patient payment collection rates in high-deductible health plan environments.

-

Interoperability mandates under the 21st Century Cures Act are improving clinical data access for RCM purposes, enabling more accurate and timely charge capture from electronic health record documentation.

-

Remote patient monitoring and telehealth service billing complexity is creating new RCM requirements as virtual care delivery creates billing scenarios that legacy systems were not designed to handle.

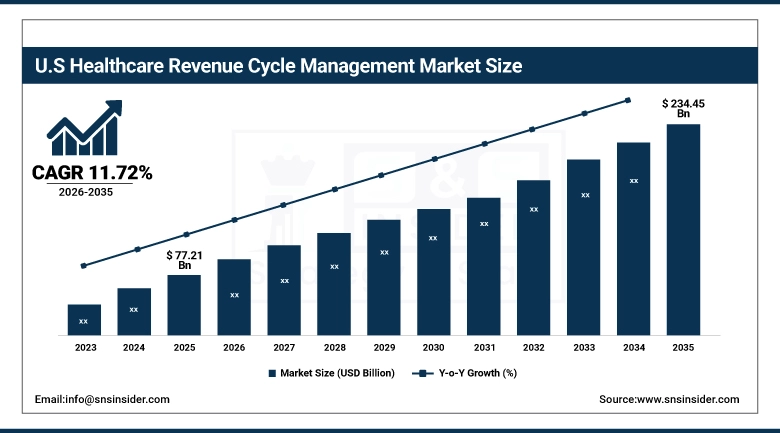

The U.S. Healthcare Revenue Cycle Management Market was valued at USD 77.21 billion in 2025 and is expected to reach USD 234.45 billion by 2035, growing at a CAGR of 11.72% from 2026-2035.

The market for healthcare revenue cycle management in the United States is supported by complicated billing systems, high expenses in healthcare, and stringent regulatory standards. Automation, artificial intelligence-based coding, and value-based care models are boosting efficiency and minimizing claim denials in healthcare.

The Centers for Medicare & Medicaid Services (CMS) 2024 physician fee schedule updates included over 400 new billing codes for digital health, remote monitoring, and behavioral health services, increasing coding complexity that drives demand for advanced RCM software. The HHS Office of Inspector General reported that improper Medicare payments exceeded USD 40 billion in fiscal 2023, reinforcing compliance-driven RCM investment across the industry.

Healthcare Revenue Cycle Management Market Segment Analysis:

-

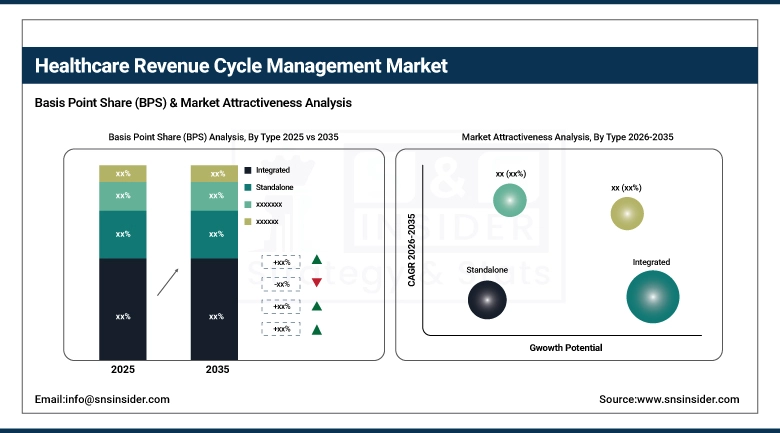

By Type, Integrated solutions dominated with ~56.2% share in 2025; Standalone solutions serving specialized single-function needs.

-

By Deployment, Cloud deployment growing fastest; On-Premise maintained in large health systems with established IT infrastructure.

-

By Component, Software dominated the Healthcare RCM Market in 2025; Services growing rapidly with RCM outsourcing adoption.

-

By Function, Claims & Denial Management growing fastest; Appointment Scheduling maintaining large installed base.

By Type, Integrated solutions dominate the Healthcare RCM Market, growing with value-based care adoption

The segment for integrated RCM software solutions was estimated at 56.2% in 2025 and is likely to remain dominant throughout the forecast period. The primary factor behind the popularity of integrated RCM software solutions is that they allow for smooth integration of all revenue cycle operations. They help in creating a single platform for tasks like billing, coding, claim processing, and patient engagement. Due to the rising popularity of value-based care delivery models, there is a high demand for real-time financial analysis. In such situations, the need for integrated platforms becomes significant for healthcare organizations that require visibility across functional areas to ensure clinical and financial success.

The RCMS that work in standalone applications address those companies that have clinical applications but need an RCMS that provides specific functions related to claim scrubbing, denials, patient payments, and/or coding. This type of software targets different clients such as physicians, specialists, and outpatient facilities that need a certain RCM function without needing a whole new system. Some companies include Waystar, Optum360, and R1 RCM that provide standalone RCMS which cater to this particular segment and can be easily embedded into their existing EHRs through HL7/FHIR API.

By Deployment, Cloud deployment growing fastest; On-Premise retained by large health systems

The cloud section of the Healthcare Revenue Cycle Management industry is projected to witness the highest growth rate in terms of scalability, affordability, and seamless integration. Healthcare organizations increasingly depend on cloud solutions due to their capacity to enable data availability, remote management of their systems, and improved system integration. In addition, they provide enhanced analytics to automate processes and facilitate updates according to evolving reimbursement methods. However, the adoption of software solutions through premises continues to dominate the Healthcare Revenue Cycle Management industry due to the existing infrastructure of leading healthcare organizations.

By Component, Software dominates while services expand with outsourcing adoption

Software became the key segment within the Healthcare Revenue Cycle Management Market in 2025 due to the vital role of software in such aspects as billing, coding, claims, and payment management. Software helps to ensure that all problems are solved by eliminating potential errors, addressing compliance issues, and optimizing revenue generation with help of analytics and artificial intelligence technology. By contrast, the services market segment experiences considerable growth due to the development of trends related to outsourcing RCM procedures.

By Function, Claims & Denial Management growing fastest; Appointment Scheduling widely adopted

The area where growth has been identified to occur the fastest in the HRCM market is claims & denial management because of increasing complexity of claims, payer requirements, and preventing revenue leakage. Claims and denial management solutions include automated and predictive capabilities that help identify errors, reduce denials, and improve the speed of receiving payments. In contrast, the area with a large installed base is appointment scheduling since appointment scheduling is a basic function in the revenue cycle management process that includes patient management and billing.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

India |

35% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

50% |

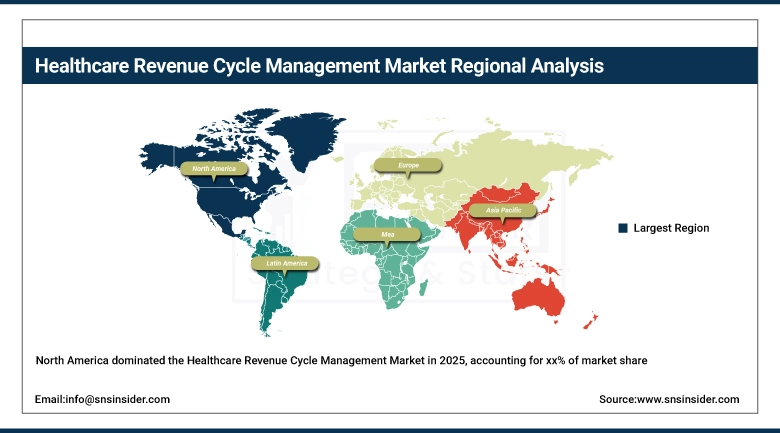

North America Healthcare Revenue Cycle Management Market Insights

The North American region held the top spot in terms of revenue contribution in the global Healthcare RCM Market in 2025, supported by its unique payer environment, higher per-capita healthcare spending, and mature healthcare information technology vendors' landscape. In the U.S., the deployment of RCM technologies is encouraged by the complex payer environment, Meaningful Use programs promoting widespread adoption of EHRs, and the move towards a value-based reimbursement model, which necessitates better financial performance monitoring. The development of AI-driven coding automation, real-time eligibility verification, and predictive denial management strategies is most prevalent in the North American market, especially in the U.S., where the financial implications of effective RCM practices are greater than elsewhere.

The American Medical Association's 2023 Prior Authorization Physician Survey found that physicians complete an average of 43 prior authorization requests per physician per week, each requiring RCM system support. The Centers for Medicare & Medicaid Services reports that Medicare paid over USD 900 billion to healthcare providers in fiscal 2023, creating an enormous transaction volume that RCM systems must process with high accuracy and timeliness.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Healthcare Revenue Cycle Management Market Insights

Europe Healthcare RCM Market is fueled by the presence of robust regulations, universal healthcare policies, and rising trends in digital health care in countries like Germany, France, and the United Kingdom. The region is experiencing an increased need for effective billing, coding, and cost management due to high healthcare expenses and aging populations. The development of digital records by governments and the introduction of regulations is driving the use of RCM processes. The NHS is taking steps towards digitalization, resulting in more efficient operations and better management of payments.

Asia Pacific Healthcare RCM Market Insights

Asia-Pacific is the most rapidly expanding market for Healthcare Revenue Cycle Management, propelled by the increasing investment in healthcare infrastructure in countries such as China, India, Japan, and Southeast Asia; the increasing number of citizens being covered under health insurance schemes; and increasing usage of Electronic Health Records (EHR), which contain the clinical documentation data processed through RCM software. The Indian government’s Ayushman Bharat health insurance scheme covering over 500 million citizens belonging to the poor segment of society has resulted in an elaborate reimbursement scheme within the government hospitals that necessitates a robust claims management process.

India's Ayushman Bharat-Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) program processes over 25 million claims annually, creating one of the world's largest government health insurance claims management programs requiring sophisticated RCM infrastructure. Japan's Ministry of Health, Labour and Welfare mandates electronic claims submission for all hospital billing, creating nationwide digital RCM infrastructure that supports advanced analytics deployment.

Middle East & Africa and Latin America Healthcare RCM Market Insights

Healthcare RCM in the Middle East & Africa and Latin America is maturing due to investments being made in the healthcare infrastructure in countries such as Brazil, South Africa, and UAE. Countries have been focusing on digitization of their healthcare systems and improving hospitals' capabilities; thus, there is a need for improved billing and claim management solutions. In the Middle East, more mandatory health insurance programs, along with an active private healthcare sector, is boosting adoption of RCM processes. Latin America's healthcare market is experiencing growth in terms of more private healthcare providers and complex reimbursement models.

Healthcare Revenue Cycle Management Market Growth Drivers:

-

Rising healthcare billing complexity and AI-driven automation creating sustained global healthcare RCM market growth

Growth in the RCM industry results from the convergence of growing administration complexity and growing capabilities of AI automation technologies. Increasing healthcare reimbursement complexity will not reduce as value-based care approaches become prevalent, along with other reimbursement strategies such as bundle payment programs that involve quality-based incentives. Prior authorization requirements have been expanding to cover an increased number of services, on average, the typical physician in the US completes about 43 prior authorization requests per week. AI automation represents the industry response in terms of machine learning solutions to predict claim denial risk ahead of time, NLP to extract billing information from clinical documents, and robotic process automation to take care of repetitive activities such as data entry and claims inquiry. Each increase in the first-pass claims acceptance rate results in millions of saved dollars for financially strained healthcare organizations.

Healthcare Financial Management Association research documents that healthcare organizations using AI-powered RCM technology report 25-35% reduction in claim denial rates and 15-20% improvement in days in accounts receivable compared to organizations relying on manual RCM processes. McKinsey estimates that automating healthcare administrative processes including RCM could save the U.S. healthcare system USD 265 billion annually.

Healthcare Revenue Cycle Management Market Restraints:

-

Complex regulatory compliance requirements and high implementation costs limiting healthcare RCM adoption among smaller providers

Healthcare RCM technology implementation is complex and expensive in ways that create meaningful adoption barriers for smaller healthcare providers. HIPAA compliance, state-level billing regulations, payer-specific claim submission requirements, and the ongoing regulatory changes that accompany healthcare reform each impose compliance requirements that RCM systems must incorporate and maintain continuously. For rural hospitals, small physician practices, and community health centers operating with limited IT staff and capital budgets, the cost and complexity of advanced RCM system implementation including data migration, staff training, workflow redesign, and ongoing system maintenance can exceed available resources. RCM outsourcing has emerged as the primary mechanism through which smaller providers access advanced RCM capability without internal technology investment, but outsourcing economics themselves require minimum volume thresholds that very small practices do not meet.

Healthcare Revenue Cycle Management Market Opportunities:

-

Autonomous AI coding and value-based care analytics creating transformative healthcare RCM growth opportunities globally

Autonomous coding where AI generates ICD-10 diagnosis codes and CPT procedure codes directly from clinical documentation without human coder involvement represents the most commercially significant near-term RCM innovation opportunity. Medical coding currently requires armies of credentialed coders who are expensive to employ, slow to scale, and inconsistent across individuals. AI coding systems that achieve accuracy comparable to experienced human coders can process documentation faster, at lower cost, and with consistency that human coders cannot match at volume. Companies including 3M Health Information Systems, Optum360, and Nuance are advancing autonomous coding products toward the commercial deployment scale that would transform healthcare administrative staffing economics. Value-based care analytics providing real-time visibility into quality performance, cost-per-episode economics, and attributed patient outcomes represent a premium RCM segment that health systems running value-based contracts are actively seeking and willing to pay premium prices for.

Recent Developments:

-

2025: Waystar launched its AI-powered Claim Intelligence platform with real-time claim denial prediction that analyzes 200+ variables per claim before submission to identify likely denial reasons and recommend corrections, reporting average first-pass acceptance rate improvement from 89% to 96% across early commercial implementations at regional health system customers.

-

2025: Oracle Health expanded its Revenue Management Cloud capabilities with integrated AI-assisted prior authorization management that automatically submits authorization requests, tracks payer responses, and escalates denials to clinical staff through the EHR workflow, targeting the reduction of physician prior authorization burden documented at 43+ requests per physician per week.

-

2026: R1 RCM announced full commercial deployment of its AI Advantage autonomous medical coding platform across 15 health system clients, achieving 95%+ coding accuracy on emergency medicine and outpatient evaluation and management service lines without human coder review, generating documented coding department labor cost reductions of 40-60% at fully deployed installations.

Healthcare Revenue Cycle Management Market Key Players:

-

Cerner Corporation (Oracle Health)

-

Optum (UnitedHealth Group)

-

Waystar Health Inc.

-

Nthrive Inc.

-

GE Healthcare

-

Greenway Health LLC

-

AdvancedMD Inc.

-

Kareo Inc. (Tebra)

-

Athenahealth Inc.

-

Change Healthcare (Optum)

-

3M Health Information Systems

-

Nuance Communications (Microsoft)

-

McKesson Corporation

-

SSI Group LLC

-

MedAssets (Vizient)

-

Allscripts Healthcare Solutions

-

Meditech

Healthcare Revenue Cycle Management Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 171.58 Billion |

| Market Size by 2035 | USD 521.0 Billion |

| CAGR | CAGR of 11.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Standalone, Integrated) • By Deployment (Cloud, On-Premise) • By Component (Software, Service) • By Function (Appointment Scheduling, Claims & Denial Management, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | R1 RCM Inc., Cerner Corporation (Oracle Health), Epic Systems Corporation, Optum (UnitedHealth Group), Waystar Health Inc., Conifer Health Solutions, Nthrive Inc., GE Healthcare, Greenway Health LLC, AdvancedMD Inc., Kareo Inc. (Tebra), Athenahealth Inc., Change Healthcare (Optum), 3M Health Information Systems, Nuance Communications (Microsoft), McKesson Corporation, SSI Group LLC, MedAssets (Vizient), Allscripts Healthcare Solutions, Meditech |

Frequently Asked Questions

Ans: The Services segment is growing rapidly driven by widespread RCM outsourcing adoption across healthcare organizations.

Ans: North America dominated the Healthcare Revenue Cycle Management Market in 2025.

Ans: The Integrated solutions segment dominated the Healthcare RCM Market with approximately 56.2% share in 2025.

Ans: The Healthcare Revenue Cycle Management Market was valued at USD 171.58 billion in 2025.

Ans: The Healthcare Revenue Cycle Management Market is expected to grow at a CAGR of 11.72% from 2026 to 2035.

Get in Touch