Dermal Fillers Market Report Scope & Overview:

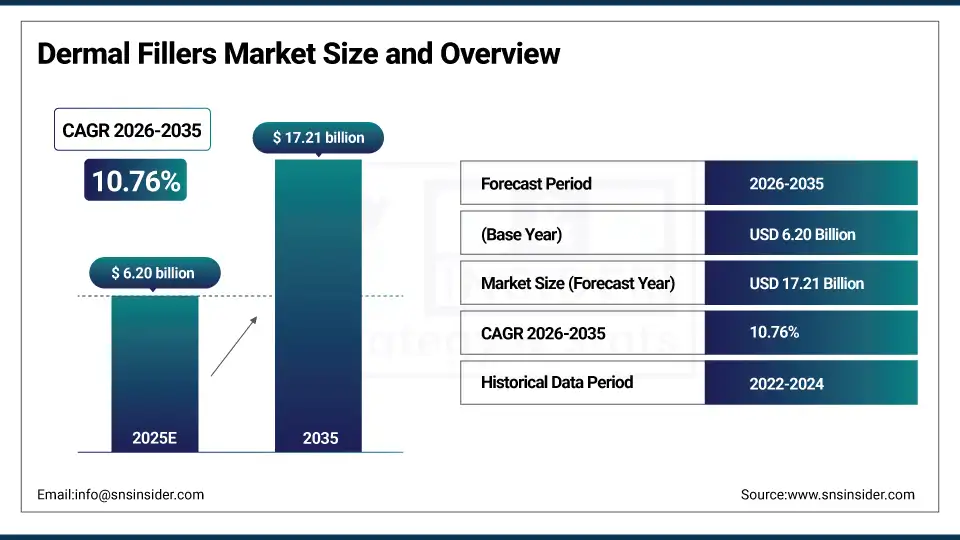

The Dermal Fillers Market size is estimated at USD 6.20 billion in 2025 and is expected to reach USD 17.21 billion by 2035, growing at a CAGR of 10.76% over the forecast period of 2026-2035.

The global dermal fillers market trend is a growing demand for minimally invasive aesthetic procedures such as wrinkle correction treatments, lip enhancement services, and facial volume restoration. The growth of the market is driven by increasing aging population demographics, rising disposable incomes in emerging economies, and growing social media influence on beauty standards. This trend is also driven by a growing adoption of advanced hyaluronic acid formulations and the growing focus on natural-looking aesthetic outcomes as healthcare providers become more focused on patient satisfaction and are more willing to invest in innovative injectable technologies, resulting in growth in the domestic and international market for biodegradable and non-biodegradable dermal filler products.

For instance, in March 2024, growing awareness and improved aesthetic treatment accessibility drove a 24% increase in dermal filler procedure volumes for medical aesthetic clinics globally, boosting non-surgical facial rejuvenation and cosmetic enhancement adoption.

Dermal Fillers Market Size and Forecast:

-

Market Size in 2025: USD 6.20 billion

-

Market Size by 2035: USD 17.21 billion

-

CAGR: 10.76% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Dermal Fillers Market - Request Free Sample Report

Dermal Fillers Market Trends

-

Dermal filler solutions are being adopted because patients demand safe anti-aging treatments, natural-looking facial enhancement, and quick recovery procedures with minimal downtime.

-

Customized aesthetic treatment protocols based on facial anatomy, skin type, and individual aging patterns to improve cosmetic outcomes of facial rejuvenation.

-

The development of longer-lasting formulations, cross-linked hyaluronic acid technologies, and combination aesthetic treatments to improve the patient satisfaction and reduce repeat visit frequency.

-

Advanced injection techniques, precision cannula systems, and 3D facial assessment tools are all available to ensure optimal product placement and natural aesthetic results.

-

Increased demand for physician training programs, certification courses and standardized injection protocols to help treatment safety and aesthetic outcome consistency.

-

Collaboration between aesthetic device manufacturers, dermatology practices and medical spas to develop innovative dermal filler products and improve treatment delivery standards.

-

FDA, EMA and international regulatory bodies promoting standards for product safety, clinical efficacy testing, adverse event monitoring, and practitioner qualification requirements.

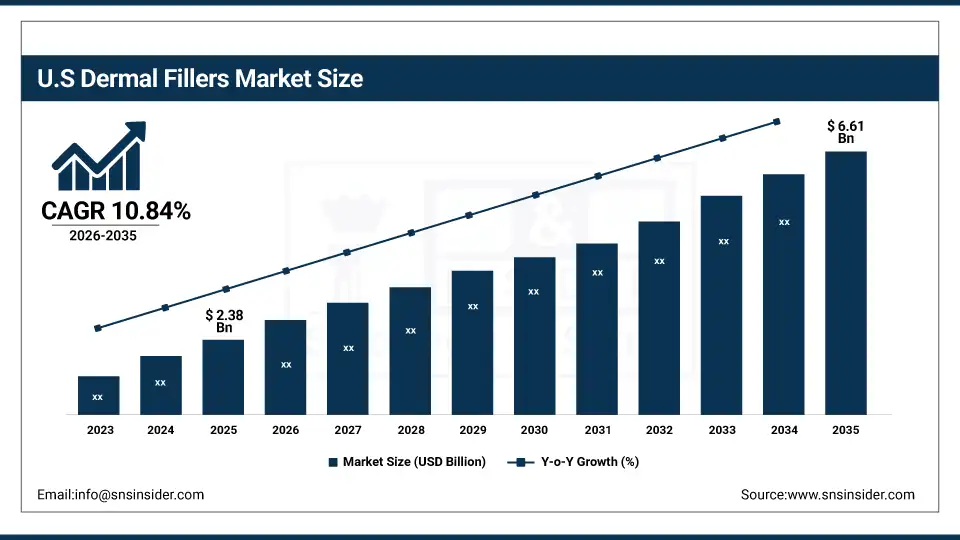

The U.S. Dermal Fillers Market is estimated at USD 2.38 billion in 2025 and is expected to reach USD 6.61 billion by 2035, growing at a CAGR of 10.84% from 2026-2035. The United States represents the largest market for dermal fillers, primarily driven by the well-established aesthetic medicine industry, high consumer spending on cosmetic procedures, and advanced medical spa infrastructure. Strong social media influence, celebrity endorsement of aesthetic treatments and increased aesthetic practitioner expertise help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the regulatory approval efficiency and swift adoption of innovative hyaluronic acid and biodegradable dermal filler solutions.

Dermal Fillers Market Growth Drivers:

-

Rising Aging Population and Anti-Aging Treatment Demand is Driving the Dermal Fillers Market Growth

Rising aging population and anti-aging treatment demand take the center stage as a growth driver for the dermal fillers market share, and are driven by the increasing geriatric demographic seeking facial rejuvenation, growing acceptance of cosmetic procedures across age groups, and heightened awareness of minimally invasive aesthetic options for wrinkle reduction and volume restoration. These solutions for facial aesthetic enhancement and age-related skin concern management are driving the base of the market, the penetration of biodegradable & long-lasting markets, and adding to the overall market share globally.

For instance, in June 2024, hyaluronic acid-based and biodegradable dermal filler products accounted for ~71% of the total global aesthetic injectable treatment investments, reflecting growing patient preference and expanding market share.

Dermal Fillers Market Restraints:

-

High Treatment Costs and Adverse Event Concerns are Hampering the Dermal Fillers Market Growth

High treatment costs & adverse event concerns of dermal filler procedures also restrict the dermal fillers market growth, as a large number of potential patients face affordability barriers for premium aesthetic treatments and remain cautious about complications such as nodule formation, vascular occlusion, or allergic reactions. This might lead to treatment hesitation, limited market penetration in price-sensitive regions, and reduced repeat procedure rates for aesthetic practices. As a result, patient access suffers, and market growth is stunted in regions where disposable incomes are limited and medical aesthetic insurance coverage is unavailable.

Dermal Fillers Market Opportunities:

-

Emerging Markets Expansion and Male Aesthetic Treatment Growth Drive Future Growth Opportunities for the Dermal Fillers Market

The opportunity in the emerging markets expansion and male aesthetic treatment growth in dermal fillers market is in the form of untapped geographic regions with rising middle-class populations, increasing male grooming trends, and growing acceptance of cosmetic procedures among men. These solutions provide for expanded patient demographics, diversified treatment applications, and new revenue streams for aesthetic practitioners. Through enhanced market accessibility, targeted marketing campaigns, and specialized treatment protocols, particularly in areas with developing aesthetic medicine infrastructure, these opportunities may improve industry revenues, decrease geographic market concentration, and expand the market.

For instance, in April 2024, international aesthetic societies reported that 32% of dermal filler procedures were performed on male patients globally, highlighting rising demographic diversification and increasing demand for gender-specific aesthetic treatment protocols.

Dermal Fillers Market Segment Analysis

-

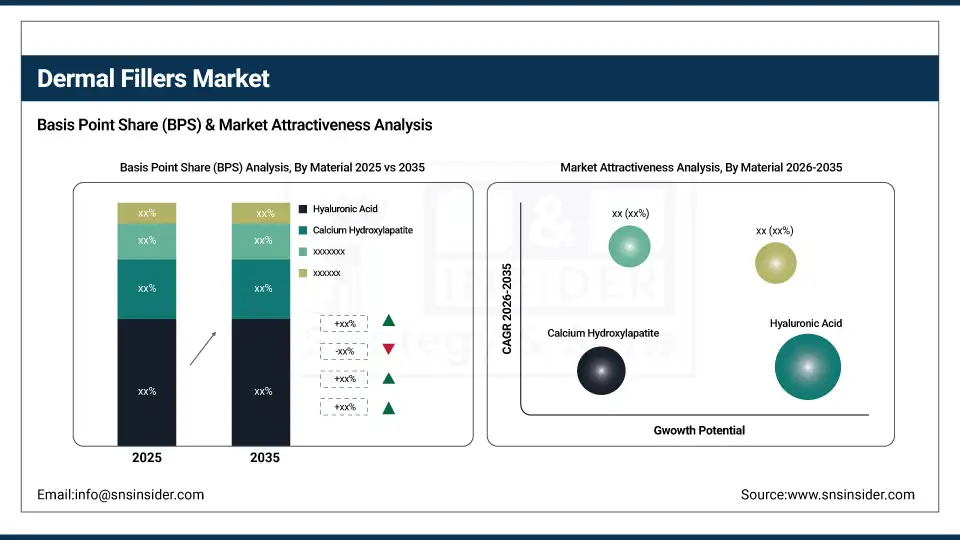

By material, hyaluronic acid held the largest share of around 67.42% in 2025E, and the poly-L-lactic acid segment is expected to register the highest growth with a CAGR of 11.34%.

-

By product, the biodegradable segment dominated the market with approximately 73.18% share in 2025E, while the non-biodegradable is expected to register the highest growth with a CAGR of 11.12%.

-

By end-user, specialty & dermatology clinics accounted for the leading share of nearly 54.28% in 2025E, and is expected to register the highest growth with a CAGR of 10.98%.

By Material, Hyaluronic Acid Leads the Market, While Poly-L-lactic Acid Registers Fastest Growth

The hyaluronic acid segment accounted for the highest revenue share of approximately 67.42% in 2025, owing to excellent biocompatibility with human tissue, natural presence in skin composition, and reversibility through hyaluronidase enzyme administration. Emerging trends, including increasing development of cross-linked formulations with extended duration and regulatory preference for naturally derived substances. In comparison, the poly-L-lactic acid segment is anticipated to achieve the highest CAGR of nearly 11.34% during the 2026–2035 period, driven by the increasing demand for collagen-stimulating treatments, longer-lasting aesthetic results, and gradual natural-looking volumization effects. Drivers include rising adoption for deep facial volume restoration, the preference for biostimulatory filler mechanisms.

By Product, the Biodegradable Segment dominates, while the Non-Biodegradable Segment Shows Rapid Growth

By 2025, the biodegradable segment contributed the largest revenue share of 73.18% due to superior safety profiles, natural metabolic absorption processes and regulatory approval advantages. Growing adoption of temporary filler solutions coupled with patient preference for reversible treatments, practitioners are increasingly recommending biodegradable dermal filler options. The non-biodegradable segment is projected to grow at the highest CAGR of about 11.12% between 2026 and 2035 due to the growing need for permanent facial contouring solutions and long-term cost-effectiveness advantages. Some of the reasons include better value proposition for patients seeking lasting results, reduced treatment frequency requirements, and specific patient populations' preference for semi-permanent aesthetic enhancement options.

By End-user, Specialty & Dermatology Clinics Lead, and Register Fastest Growth

The specialty & dermatology clinics segment accounted for the largest share of the dermal fillers market with about 54.28%, owing to their specialized aesthetic expertise, dedicated cosmetic treatment facilities, and established patient trust for facial rejuvenation procedures. Reasons driving the specialty clinic segment include increasing patient preference for board-certified practitioners and comprehensive aesthetic consultation services. In addition, it is slated to grow at the fastest rate with a CAGR of around 10.98% throughout the forecast period of 2026–2035, as dermatology clinics and medical spas seek advanced injectable product portfolios, combination aesthetic treatment protocols, and enhanced patient experience capabilities. Increased focus on personalized treatment plans and result documentation contribute to their adoption, while improved patient retention rates and treatment outcome satisfaction drive continued investment.

Dermal Fillers Market Regional Highlights:

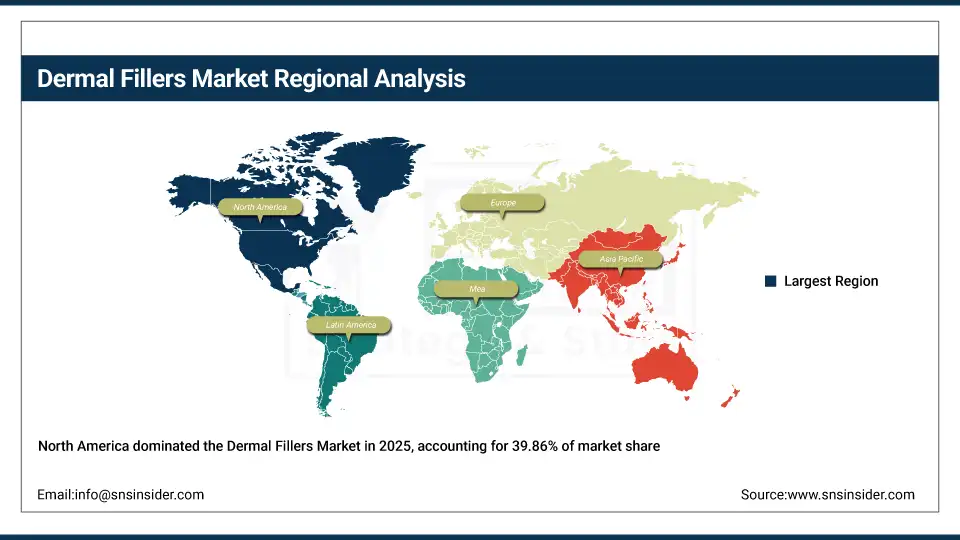

North America Dermal Fillers Market Insights:

North America held the largest revenue share of over 39.86% in 2025 of the dermal fillers market due to an established aesthetic medicine industry, high consumer awareness regarding cosmetic enhancement options, and increased practitioner expertise in advanced injection techniques. Drivers include ubiquitous social media influence on beauty standards, an advanced medical spa network, growing aesthetic treatment normalization and greater acceptance of preventative anti-aging interventions stemming from changing cultural attitudes. At the same time, various FDA product approvals, medical aesthetics innovation and enormous investments in aesthetic technology from device manufacturers and clinic operators are anchoring dermal filler products and services in the market, and ensuring multibillion dollar revenues around the world.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Dermal Fillers Market Insights:

Asia Pacific is the fastest-growing segment in the dermal fillers market with a CAGR of 12.24%, as the awareness about aesthetic procedures, rising medical tourism destinations, and beauty standard evolution in developing nations is growing. Factors including rapid urbanization, expanding middle-class population with aesthetic treatment affordability, and growing adoption of Western beauty trends are stimulating the market growth. Korean beauty influence and Chinese aesthetic market expansion have been instrumental in improving procedure accessibility, especially in metropolitan urban settings. International aesthetic brand presence and domestic manufacturing development also help in advancing treatment availability and product affordability. Increase in demand in Asia Pacific region owing to rising disposable incomes against historical spending levels and growing accessibility and acceptance of minimally invasive cosmetic procedures.

Europe Dermal Fillers Market Insights:

The dermal fillers market in Europe is the second-dominating region after North America on account of an increase in the adoption of minimally invasive aesthetic treatments, robust product safety regulations including CE marking requirements, and increasing aesthetic awareness initiatives across healthcare systems. Rising implementation of standardized injection training programs, advanced aesthetic practitioner certification, favorable reimbursement policies for reconstructive applications, and cross-border aesthetic tourism are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Dermal Fillers Market Insights:

In Latin America, and Middle East & Africa, the growing aesthetic treatment acceptance and increase in medical tourism infrastructure with disposable income growth support the dermal fillers market growth. The rising popularity of Brazilian aesthetic expertise and Middle Eastern luxury medical spa development, along with international product availability, will aid aesthetic procedure accessibility and treatment adoption. The increasing urban population and improving practitioner training standards in these regions are continuing to encourage market growth.

Dermal Fillers Market Competitive Landscape:

Allergan Aesthetics (AbbVie Inc.) (est. 1950) is a leading global pharmaceutical company that focuses on medical aesthetics, neuroscience, and eye care therapeutic areas. It uses its comprehensive product portfolio and extensive clinical research capabilities to produce cutting-edge dermal filler technology with proven safety and efficacy profiles.

-

In February 2025, it expanded its Juvéderm dermal filler line with next-generation hyaluronic acid formulations featuring enhanced cross-linking technology, aiming to improve treatment longevity and natural aesthetic outcomes across its global aesthetic practitioner network.

Galderma S.A. (est. 1981) is a well-known global dermatology company focused on prescription medications, aesthetic injectable solutions, and dermatological skincare products. It invests in innovative hyaluronic acid technologies and comprehensive aesthetic training platforms with the hopes of revolutionizing facial rejuvenation with safe, effective, and physician-administered dermal filler solutions.

-

In May 2024, launched an enhanced Restylane dermal filler portfolio featuring advanced NASHA gel technology and precision injection systems across European and North American markets, enhancing treatment versatility, patient comfort, and aesthetic outcome predictability.

Merz Pharma GmbH & Co. KGaA (est. 1908) is a leading specialty pharmaceutical company in the fields of aesthetic medicine, neurotoxin therapy, and consumer healthcare. The company's dermal filler product portfolio focuses on unique hyaluronic acid compositions and specialized volumizing formulations, and features a strong commitment to clinical evidence generation and continuous product innovation to complement the strong market presence in both physician practices and medical spa settings.

-

In September 2024, introduced advanced Belotero dermal filler variants with proprietary cohesive polydensified matrix technology for superficial wrinkle treatment, strengthening product differentiation capabilities and expanding adoption among aesthetic dermatologists and plastic surgeons.

Dermal Fillers Market Key Players:

-

Allergan Aesthetics (AbbVie Inc.)

-

Galderma S.A.

-

Merz Pharma GmbH & Co. KGaA

-

Sinclair Pharma (Huadong Medicine)

-

Revance Therapeutics, Inc.

-

Teoxane Laboratories

-

Prollenium Medical Technologies

-

Suneva Medical, Inc.

-

Integra LifeSciences Corporation

-

BioPlus Co., Ltd.

-

Laboratories Vivacy

-

Croma-Pharma GmbH

-

IMEIK Technology Development Co., Ltd.

-

Genoss Co., Ltd.

-

Hugel, Inc.

-

Aesthetic Dermal, Inc.

-

Anika Therapeutics, Inc.

-

Laboratoires Filorga

-

Bioxis Pharmaceuticals

-

Bohus BioTech AB

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | US$ 6.20 Billion |

| Market Size by 2035 | US$ 17.21 Billion |

| CAGR | CAGR of 10.76% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Hyaluronic Acid, Calcium Hydroxylapatite, Poly-L-lactic Acid, PMMA (Poly (Methyl Methacrylate)), Fat Fillers, Others) • By Product (Biodegradable, Non-Biodegradable) • By Application (Scar Treatment, Wrinkle Correction Treatment, Lip Enhancement, Restoration of Volume/Fullness, Others) • By End-user (Specialty & Dermatology Clinics, Hospitals & Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Allergan Aesthetics (AbbVie Inc.), Galderma S.A., Merz Pharma GmbH & Co. KGaA, Sinclair Pharma (Huadong Medicine), Revance Therapeutics, Inc., Teoxane Laboratories, Prollenium Medical Technologies, Suneva Medical, Inc., Integra LifeSciences Corporation, BioPlus Co., Ltd., Laboratories Vivacy, Croma-Pharma GmbH, IMEIK Technology Development Co., Ltd., Genoss Co., Ltd., Hugel, Inc., Aesthetic Dermal, Inc., Anika Therapeutics, Inc., Laboratoires Filorga, Bioxis Pharmaceuticals, Bohus BioTech AB |

Frequently Asked Questions

The Dermal Fillers Market is expected to grow at a CAGR of 10.76% over the forecast period.

The Dermal Fillers Market size was USD 6.20 billion in 2025 and is expected to reach USD 17.21 billion by 2035.

Rising Aging Population and Anti-Aging Treatment Demand is Driving the Dermal Fillers Market Growth.

The Hyaluronic Acid segment dominated the Dermal Fillers Market by material in 2025.

North America dominated the Dermal Fillers Market in 2025.

Get in Touch