Hybrid Cloud Market Report Scope & Overview:

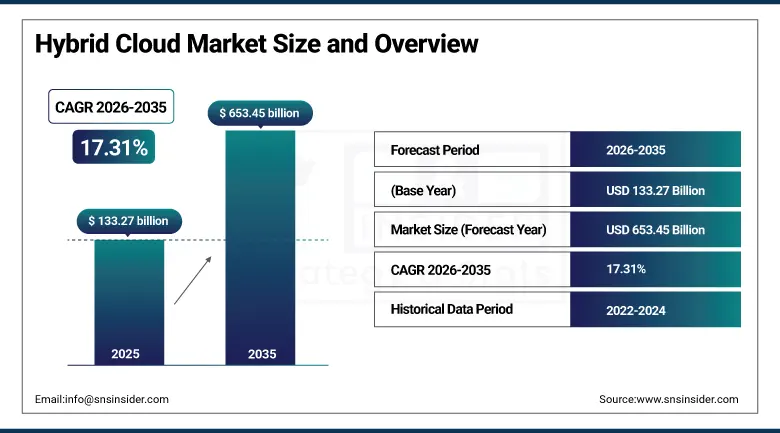

The Hybrid Cloud Market was valued at USD 133.27 Billion in 2025 and is expected to reach USD 653.45 Billion by 2035, growing at a CAGR of 17.31% from 2026–2035.

The global hybrid cloud market is growing at an exceptional pace. Hybrid cloud integrates private and public cloud environments with on-premises infrastructure, enabling organisations to optimise workloads, maintain data sovereignty, and achieve cost efficiency simultaneously. In 2024, 73% of enterprises had a hybrid cloud strategy in place, and 82% of IT leaders reported operating a hybrid model. Organisations are increasingly using hybrid architectures to run regulated workloads on private infrastructure while leveraging public cloud for scalable, non-sensitive applications. AI-driven automation, edge computing integration, and the demand for multi-cloud portability are creating new value layers that sustain commercial investment.

Microsoft expanded Azure Arc capabilities in 2024, enabling customers to deploy Azure-managed services including SQL Managed Instance across on-premises, multi-cloud, and edge environments from a single control plane. The enhancement directly addresses the enterprise requirement for unified hybrid cloud management that maintains consistent governance, compliance, and operational tooling across heterogeneous infrastructure without requiring separate management workflows for each deployment environment.

Market Size and Forecast

-

Market Size in 2026E: USD 156.36 Billion

-

Market Size by 2035: USD 653.45 Billion

-

CAGR: 17.31% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Hybrid Cloud Market - Request Free Sample Report

Hybrid Cloud Market Trends

-

AI workload integration across hybrid environments is driving demand for unified orchestration platforms that manage AI training on private GPU infrastructure while accessing public cloud inference and storage services dynamically.

-

FinOps adoption is accelerating as enterprises seek real-time visibility into hybrid cloud spending, enabling cost attribution across private and public environments and optimising resource placement based on cost and performance.

-

Container and Kubernetes adoption is enabling workload portability across hybrid environments by abstracting application deployment from underlying infrastructure, reducing vendor lock-in and enabling consistent DevOps workflows.

-

Data sovereignty and residency regulation is reinforcing hybrid cloud’s commercial rationale in the EU, India, and Southeast Asia where GDPR, DPDPA, and national data localisation requirements mandate on-premises or domestic private cloud processing for certain data categories.

-

Edge computing integration with hybrid architectures is creating distributed processing environments where time-sensitive workloads execute at the network edge while centralised analytics and management remain in private or public cloud.

U.S. Hybrid Cloud Market Outlook

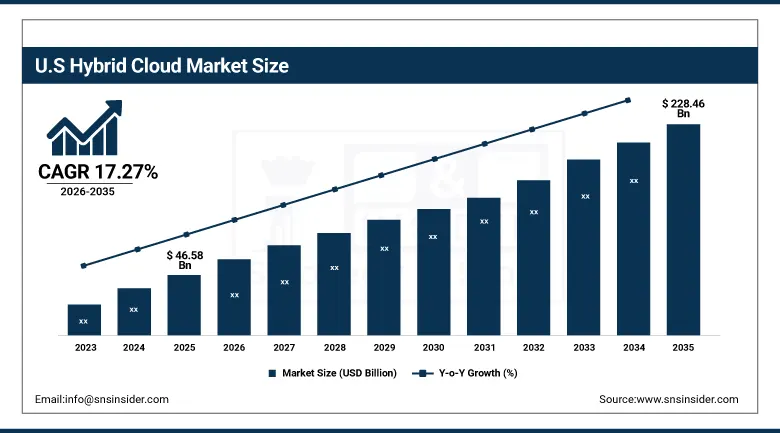

The U.S. Hybrid Cloud Market was valued at approximately USD 46.58 Billion in 2025 and is expected to reach approximately USD 228.46 Billion by 2035, growing at a CAGR of approximately 17.27%.

The U.S. is the world’s largest hybrid cloud market. AWS, Microsoft Azure, Google Cloud, and IBM together define the commercial frontier of hybrid cloud platform capability. Federal government hybrid cloud adoption under FedRAMP authorised private and hybrid cloud programmes creates substantial institutional procurement. Financial services regulators including OCC, Fed, and SEC require data residency and audit trail capabilities that hybrid cloud architectures satisfy while enabling public cloud elasticity for non-regulated workloads. The U.S. market’s commercial sophistication is visible in above-average FinOps programme maturity, Kubernetes adoption rates, and AI-hybrid workload integration deployment.

IBM launched its HashiCorp-integrated cloud portfolio in 2024 following its USD 6.4 billion acquisition, enabling enterprises to manage multi-cloud and hybrid infrastructure through a unified Terraform-based infrastructure-as-code platform. The acquisition strengthens IBM’s hybrid cloud strategy by adding a widely adopted open-source provisioning ecosystem that reduces the automation engineering investment enterprises require when orchestrating workloads across complex hybrid environments.

Hybrid Cloud Market Segment Analysis

-

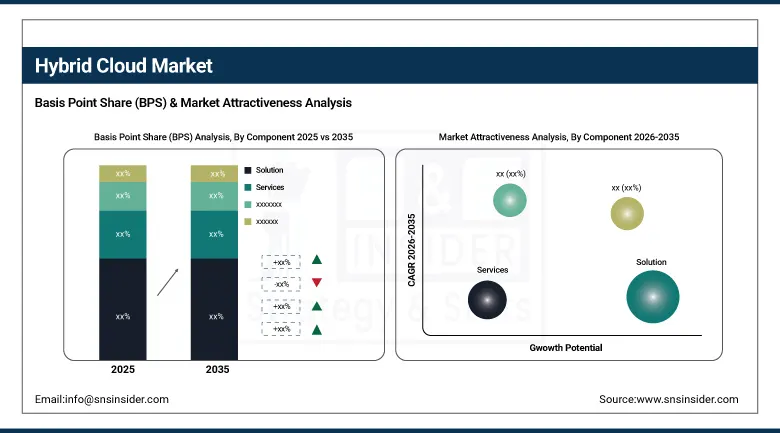

By Component, the Solution segment dominated the Hybrid Cloud Market with approximately 73.00% share in 2025, while the Services segment is the fastest growing with a CAGR of 19.55% during the forecast period.

-

By Service Model, the SaaS segment dominated the Hybrid Cloud Market with approximately 44.00% share in 2025, while the PaaS segment is the fastest growing with a CAGR of 20.10% during the forecast period.

-

By Organisation Size, the Large Enterprises segment dominated the Hybrid Cloud Market with approximately 68.50% share in 2025, while the SMEs segment is the fastest growing with a CAGR of 21.25% during the forecast period.

-

By Vertical, the BFSI segment dominated the Hybrid Cloud Market with approximately 24.00% share in 2025, while the Healthcare segment is the fastest growing with a CAGR of 20.68% during the forecast period.

By Component, solution dominates, services grow fastest

The Solution segment retained the dominant component position with approximately 73% of the hybrid cloud market in 2025. Its commercial primacy reflects the capital-intensive nature of hybrid cloud infrastructure investment. Organisations building hybrid environments procure private cloud platforms, management software, networking infrastructure, and orchestration tooling whose aggregate value substantially exceeds associated service fees. VMware, IBM, and Microsoft provide the core software-defined infrastructure platforms whose licensing and subscription revenue defines the solution segment’s commercial scale.

Services are the fastest-growing component at a CAGR of 19.55% because hybrid cloud implementation complexity exceeds the internal capability of most enterprise IT teams. Cloud migration strategy, application refactoring, security architecture, compliance framework integration, and ongoing operational optimisation each require specialist expertise that managed service providers and consulting firms supply. The widening gap between hybrid cloud adoption ambition and available internal skills creates persistent demand for external services whose scope expands with each successive hybrid infrastructure upgrade.

By Service Model, SaaS dominates, PaaS grows fastest

SaaS retained the dominant service model position with approximately 44% of the hybrid cloud market in 2025. Its commercial leadership reflects the universal enterprise adoption of cloud-based applications across CRM, ERP, collaboration, and productivity categories. Salesforce, Microsoft 365, and ServiceNow are each deployed across hybrid environments where their cloud delivery integrates with on-premises identity, data, and security infrastructure. SaaS’s commercial dominance is structural rather than cyclical—enterprise application deployment has permanently shifted toward SaaS delivery whose hybrid integration capability defines the modern enterprise architecture standard.

PaaS is the fastest-growing service model because enterprise application development is transitioning from lift-and-shift migration toward cloud-native design patterns that require platform services including managed Kubernetes, serverless functions, API management, and AI/ML development tooling. Each new cloud-native application delivered on hybrid PaaS platforms creates ongoing platform service consumption that sustains recurring revenue growth independent of initial deployment investment.

By Organisation Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant organisation size position in the hybrid cloud market in 2025. Their leadership reflects the direct correlation between organisational complexity and hybrid cloud requirement. Organisations with regulated data, legacy infrastructure, global operations, and complex security governance cannot adopt public-cloud-only strategies without creating compliance exposure that their legal and risk functions cannot accept. Hybrid cloud’s ability to satisfy these requirements while enabling public cloud economics for appropriate workloads creates precisely the value proposition that large enterprises require.

SMEs are the fastest-growing segment because the hybrid cloud market’s commercial accessibility is improving rapidly. Managed hybrid cloud services from AWS Outposts, Azure Arc, and Google Anthos are progressively reducing the engineering investment required to deploy hybrid environments. Simplified orchestration platforms, automated compliance tools, and pay-as-you-go pricing are making hybrid cloud commercially viable for organisations whose IT teams cannot sustain the dedicated hybrid infrastructure engineering capacity that earlier hybrid implementations required.

By Vertical, BFSI dominates, healthcare grows fastest

BFSI retained the dominant vertical position with approximately 24% of the hybrid cloud market in 2025. Financial services’ hybrid cloud adoption reflects the sector’s unique combination of regulatory constraints and commercial cloud economics motivation. Banks cannot move regulated customer financial data to public clouds without meeting specific data residency, audit, and security requirements that private cloud infrastructure satisfies. Simultaneously, the commercial pressure to reduce IT infrastructure cost and deploy AI analytics at scale motivates maximum public cloud adoption for non-regulated workloads where compliance constraints do not apply.

Healthcare is the fastest-growing vertical at a CAGR of 20.68% because digital health transformation is driving urgent adoption of cloud-native application delivery, AI-assisted diagnostics, and patient data platform development across hospital systems and health networks that simultaneously face strict HIPAA data sovereignty requirements. Hybrid cloud enables healthcare organisations to keep patient records and clinical data on private infrastructure while accessing public cloud AI services for imaging analysis, genomic processing, and population health analytics whose computational intensity requires elastic public cloud capacity.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Hybrid Cloud Market Insights

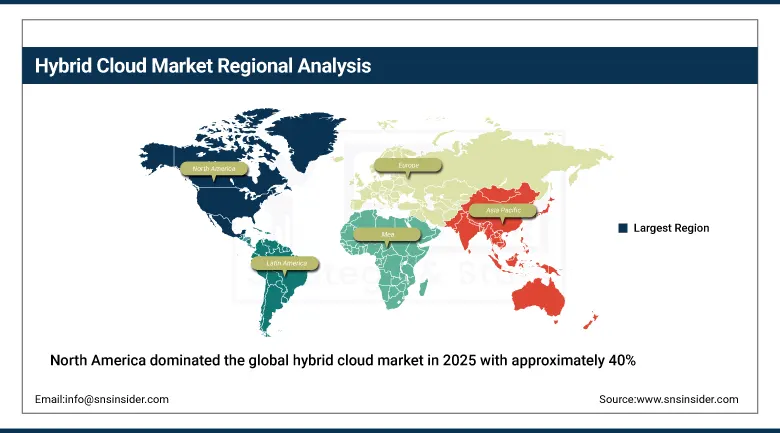

North America dominated the global hybrid cloud market in 2025 with approximately 40% of global revenues. The United States accounts for approximately 87.4% of North American revenues. AWS, Microsoft Azure, Google Cloud, and IBM are each headquartered in the U.S. and collectively define the hybrid cloud platform ecosystem. Federal government hybrid cloud investment under the Cloud Smart strategy and FedRAMP authorisation framework creates substantial institutional procurement. Enterprise BFSI and healthcare hybrid cloud adoption in the U.S. sustains the highest per-organisation cloud investment of any national market.

Canada contributes approximately 12.6% of North American revenues through its financial services sector’s hybrid cloud adoption, government digital service modernisation, and the growing technology sector whose cloud-native development practices create consistent hybrid platform demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Hybrid Cloud Market Insights

Europe is a significant hybrid cloud market where GDPR data residency requirements, EU data sovereignty investment, and the progressive implementation of the EU Cloud Rulebook create a structured regulatory environment that reinforces hybrid cloud’s commercial rationale. Germany accounts for approximately 22.3% of European revenues through its industrial enterprise’s hybrid cloud adoption for Industry 4.0 transformation, SAP’s cloud platform migration, and the federal government’s sovereign cloud investment.

The United Kingdom, France, and the Netherlands are significant secondary markets where financial services hybrid cloud, government digital transformation, and the technology sector’s cloud-native development create consistent demand. OVHcloud, Deutsche Telekom’s Open Telekom Cloud, and sovereign cloud initiatives by multiple EU member states are creating European alternatives to hyperscaler dependency that sustain hybrid investment.

Asia Pacific Hybrid Cloud Market Insights

Asia Pacific is the fastest-growing regional hybrid cloud market at a CAGR of 20.12% from 2026 to 2035, driven by rapid digital transformation across China, India, Japan, South Korea, and Southeast Asia. China accounts for approximately 44.8% of Asia Pacific revenues through Alibaba Cloud, Tencent Cloud, and Huawei Cloud’s domestic enterprise hybrid adoption and the government’s cloud-first digital economy strategy.

India represents the most commercially dynamic emerging market within Asia Pacific. The DPDPA’s data localisation requirements and the IT sector’s massive cloud adoption are simultaneously creating hybrid cloud demand. Indian enterprises across BFSI, healthcare, and manufacturing are investing in hybrid architectures that satisfy domestic data residency while enabling public cloud scalability for innovation workloads.

MEA & Latin America Hybrid Cloud Market Insights

The Middle East and Africa and Latin America are growing hybrid cloud markets where government digital transformation investment, data sovereignty regulation, and expanding enterprise cloud adoption are creating structured demand. UAE leads MEA revenues at approximately 38.4% through its smart city programmes, CBUAE cloud banking regulations, and the commercial concentration of multinational enterprise operations whose global hybrid standards require local alignment.

Brazil leads Latin American revenues at approximately 44.2% through its LGPD data protection requirements, large financial services sector’s hybrid cloud investment, and hyperscaler infrastructure expansion in São Paulo that improves domestic latency and compliance economics for Brazilian enterprise hybrid deployments.

Growth Drivers: Data sovereignty regulation reinforcing hybrid rationale and AI workload orchestration creating new hybrid value

Data sovereignty regulation is the hybrid cloud market’s most structurally reinforcing commercial driver. GDPR, HIPAA, India’s DPDPA, and national data localisation requirements across Southeast Asia collectively mandate that specific data categories remain within defined geographic or institutional boundaries. Public cloud alone cannot satisfy these requirements without creating compliance exposure. Hybrid cloud enables organisations to place regulated data on private or domestic cloud infrastructure while maximising public cloud adoption for compliant workloads, creating a regulatory rationale for hybrid adoption that strengthens with each new data protection framework enacted globally.

AI workload orchestration is creating a new commercial value layer for hybrid cloud beyond traditional flexibility and cost optimisation. AI training requires GPU infrastructure whose capital cost organisations are increasingly deploying on private or co-located infrastructure for cost control. AI inference, data preprocessing, and model serving benefit from public cloud elasticity. Hybrid orchestration platforms that seamlessly route AI workloads between private GPU clusters and public cloud inference endpoints create operational efficiency that neither purely private nor purely public cloud can achieve independently.

Restraints: Integration complexity across heterogeneous environments and skills shortage in hybrid cloud engineering

Integration complexity is the hybrid cloud market’s most persistent operational challenge. Connecting private infrastructure, multiple public clouds, and legacy on-premises systems through consistent networking, identity, and security fabric requires sustained engineering investment that most enterprise IT teams cannot sustain without specialist support. Each new cloud provider or private platform added to the hybrid environment adds integration surface whose maintenance burden compounds with architectural complexity.

The hybrid cloud engineering skills shortage creates implementation quality challenges across the market. Practitioners who combine private cloud platform expertise, public cloud certification, Kubernetes proficiency, and security architecture capability are the market’s most commercially scarce professional resource. The gap between hybrid cloud adoption ambition and available implementation expertise sustains managed service demand but limits the pace of self-managed hybrid programme development among organisations that cannot recruit or retain qualified hybrid architects.

Opportunities: Sovereign cloud hybrid investment, AI-hybrid workload management platform, and SME managed hybrid service expansion

Sovereign cloud investment represents the most commercially significant near-term opportunity created by geopolitical and regulatory momentum. European, Middle Eastern, and Southeast Asian governments are investing in national sovereign cloud infrastructure whose data sovereignty credentials enable sensitive government and critical infrastructure workloads to migrate from on-premises to sovereign hybrid cloud environments. Each national sovereign cloud programme creates a new institutional procurement channel whose scale reflects government digital transformation ambition.

AI-hybrid workload management platforms represent a premium product development direction whose value proposition addresses the specific orchestration challenges of running AI infrastructure across private GPU deployments and public cloud AI services. Platforms that provide unified cost visibility, workload placement optimisation, and model lifecycle management across hybrid AI environments create commercial value that general-purpose hybrid management tools do not deliver with equivalent specificity.

Recent Developments:

-

2024: Microsoft expanded Azure Arc capabilities in 2024, enabling deployment of Azure-managed services including SQL Managed Instance across on-premises, multi-cloud, and edge environments through a single control plane, directly addressing the enterprise requirement for consistent governance across heterogeneous hybrid infrastructure.

-

2024: IBM completed its USD 6.4 billion acquisition of HashiCorp in 2024, integrating Terraform-based infrastructure-as-code tooling into IBM’s hybrid cloud portfolio to enable enterprises to provision and manage multi-cloud and hybrid environments through a unified open-source automation platform.

-

2024: Google Cloud expanded its Distributed Cloud portfolio in 2024 with new air-gapped and connected sovereign deployment options that enable government and regulated enterprise customers to run Google Cloud services on their own infrastructure while maintaining local data sovereignty and operational control.

Hybrid Cloud Market Key Players

-

Amazon Web Services

-

Microsoft

-

IBM

-

Google Cloud

-

Hewlett Packard Enterprise

-

Oracle

-

Nutanix

-

Red Hat

-

Cisco Systems

-

Dell Technologies

-

Rackspace Technology

-

NetApp

-

Pure Storage

-

Zscaler

-

Equinix

-

Alibaba Cloud

-

Tencent Cloud

-

OVHcloud

Hybrid Cloud Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 133.27 Billion |

| Market Size by 2035 | USD 653.45 Billion |

| CAGR | CAGR of 17.31% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solution, Services) • by Service Model (IaaS, PaaS, SaaS) • by Organisation Size (Large Enterprises, SMEs) • by Vertical (BFSI, IT & Telecom, Healthcare, Retail, Manufacturing, Government, Media, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Amazon Web Services, Microsoft, IBM, Google Cloud, VMware, Hewlett Packard Enterprise, Oracle, Nutanix, Red Hat, Cisco Systems, Dell Technologies, Rackspace Technology, NetApp, Pure Storage, Zscaler, Palo Alto Networks, Equinix, Alibaba Cloud, Tencent Cloud, OVHcloud |

Frequently Asked Questions

The Hybrid Cloud Market is expected to grow at a CAGR of 17.31% from 2026 to 2035.

The Hybrid Cloud Market was valued at USD 133.27 Billion in 2025.

Data sovereignty regulation reinforcing hybrid cloud’s commercial rationale across regulated industries, AI workload orchestration creating new hybrid value layers beyond traditional flexibility, and the universal enterprise preference for architectures that balance public cloud economics with private infrastructure control.

BFSI dominated the Hybrid Cloud Market with approximately 24% share in 2023, while Healthcare is the fastest growing with a CAGR of 20.68%.

North America dominated the Hybrid Cloud Market in 2025 with approximately 40% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch