Hydrogen Electrolyzer Market Report Scope & Overview:

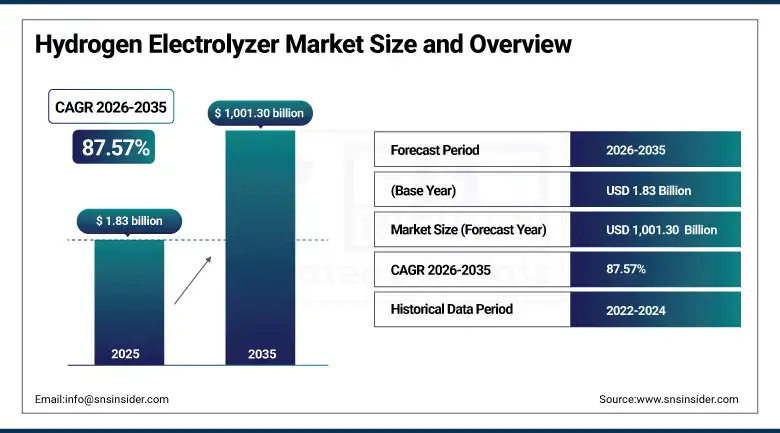

The Hydrogen Electrolyzer Market was valued at USD 1.83 billion in 2025 and is expected to reach USD 1,001.30 billion by 2035, growing at a CAGR of 87.57% from 2026–2035.

The global hydrogen electrolyzer market is at the epicenter of the clean energy transition, as the convergence of net-zero carbon commitments from over 130 national governments, falling renewable electricity costs that are progressively improving green hydrogen economics, and the recognition that large-scale green hydrogen production is essential for decarbonizing hard-to-abate industrial sectors collectively create the most consequential energy market opportunity of the coming decade. The market’s extraordinary CAGR reflects both the current early-commercial stage of the electrolyzer market and the extraordinary investment momentum that government hydrogen strategies, corporate decarbonization commitments, and venture capital energy transition investment are jointly mobilizing across the electrolyzer technology development and manufacturing scale-up programmes that are now advancing toward commercial readiness at a pace that the sector’s critics initially dismissed as unachievable. The International Energy Agency’s Net Zero by 2050 scenario projects that hydrogen will supply approximately 10% of global final energy demand by 2050, with green hydrogen produced by electrolysis accounting for the dominant and growing portion of that supply as carbon capture costs and fossil hydrogen production carbon costs converge with declining green hydrogen production economics.

Plug Power’s July 2025 commissioning of a 100 MW PEM electrolyzer plant in New York capable of producing up to 45 tons of green hydrogen daily for heavy transport and industrial decarbonization applications represents a landmark commercial-scale PEM deployment whose operational performance data will provide the real-world evidence base that is critical for convincing risk-averse industrial hydrogen off takers to sign the long-term green hydrogen supply agreements that justify the capital expenditure of subsequent gigawatt-scale electrolyzer project development.

Market Size and Forecast

-

Market size in 2026E: USD 3.44 Billion

-

Market size by 2035: USD 1,001.30 Billion

-

CAGR (2026 to 2035): 87.57%

-

Fastest growing region: Asia Pacific

-

Largest region: Europe

To Get more information On Hydrogen Electrolyzer Market - Request Free Sample Report

Hydrogen Electrolyzer Market Trends

-

Rapid scaling of PEM electrolyzer manufacturing capacity by major suppliers including Plug Power, Nel ASA, ITM Power, and Siemens Energy in response to an accelerating pipeline of utility-scale green hydrogen project final investment decisions, with electrolyzer stack component cost reduction.

-

Growing deployment of co-located renewable power and electrolyzer systems that directly pair utility-scale solar and wind generation with electrolysis capacity to produce green hydrogen at the lowest possible renewable electricity cost, eliminating grid connection costs and transmission losses.

-

Progressive development of solid oxide electrolyzer cell technology for high-temperature electrolysis applications that achieve superior electrical efficiency relative to alkaline and PEM systems.

-

Increasing adoption of electrolyzer systems for hydrogen-based long-duration energy storage applications where electrolysis converts surplus renewable electricity during periods of generation excess into hydrogen that can be stored in geological formations, above-ground pressure vessels, or converted to ammonia for seasonal energy storage.

-

Growing commercialization of anion exchange membrane electrolyzer technology that combines the material cost advantages of alkaline electrolysis with the dynamic response capability and compact architecture of PEM systems, potentially offering a third commercial electrolyzer technology pathway.

The U.S. Hydrogen Electrolyzer Market Outlook

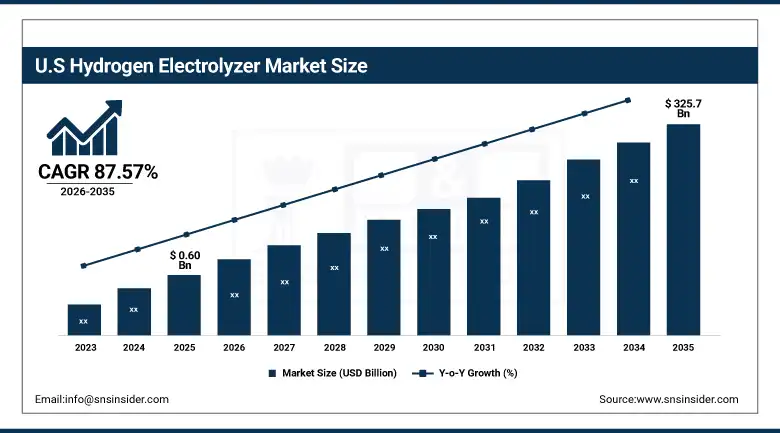

The U.S. hydrogen electrolyzer market was valued at approximately USD 0.60 billion in 2025 and is expected to reach approximately USD 325.7 billion by 2035, growing at a CAGR of 87.57% from 2026–2035.

The United States hydrogen electrolyzer market is being shaped by the Inflation Reduction Act’s extraordinary financial incentive structure, which makes the IRA’s clean hydrogen production tax credit the most commercially important policy instrument for green hydrogen economics in any national market globally, directly enabling project economics that are attracting electrolyzer project investment at a scale and pace that no other market incentive framework has achieved. The IRA hydrogen hub programme is simultaneously funding seven regional hydrogen ecosystems across the Pacific Northwest, Appalachia, the Gulf Coast, the Midwest, and New England that collectively represent the most geographically diverse and commercially scaled green hydrogen infrastructure development programme in the world, creating anchor demand for electrolyzer capacity that domestic and international electrolyzer suppliers are racing to serve through manufacturing capacity expansions and supply chain localisation investments in the United States. The petroleum refining sector’s potential transition from grey to green hydrogen production represents the single largest near-term U.S. electrolyzer demand opportunity, as the approximately 10 million tonnes of hydrogen consumed annually by U.S. refineries for hydrocracking and desulphurisation processes represents an electrolytic replacement demand whose capture at even a modest initial percentage would represent an enormous electrolyzer installation requirement.

The Department of Energy’s Hydrogen Shot initiative targeting a cost reduction of clean hydrogen production to USD 1 per kilogram within a decade is driving electrolyzer technology development investment across U.S. national laboratories, universities, and private sector R&D programmes that are collectively advancing the stack component efficiency, manufacturing yield, and operational durability improvements that must be achieved to reach the USD 1 per kilogram target and fully unlock hydrogen’s potential as a widely adopted clean energy carrier.

Hydrogen Electrolyzer Market Segment Analysis

-

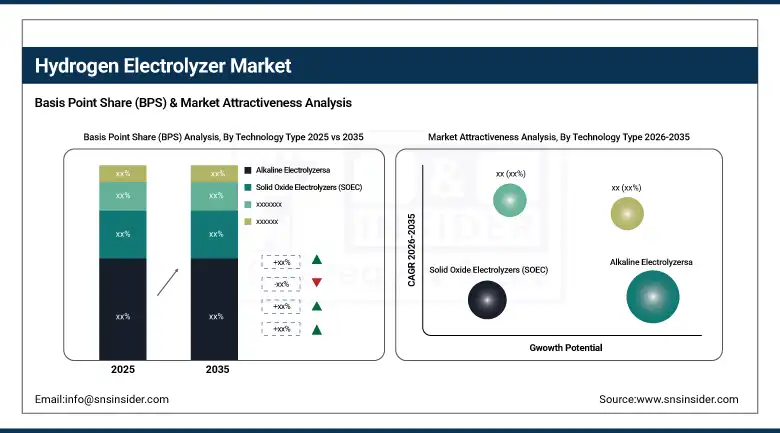

By technology type, alkaline electrolyzers dominated the hydrogen electrolyzer market with approximately 55% share in 2025; PEM electrolyzers are the fastest-growing technology at a CAGR of approximately 92%.

-

By capacity, systems above 1 MW held a significant share of the hydrogen electrolyzer market in 2025; the above 1 MW segment is simultaneously the fastest-growing.

-

By application, energy and power generation led the hydrogen electrolyzer market with approximately 38% share in 2025; transportation and mobility is the fastest-growing application at approximately 95% CAGR.

-

By end user, the utilities and energy sector held the largest share in 2025; the chemical industry is the fastest-growing end user.

By Technology Type, alkaline electrolyzer dominate, PEM grows fastest

Alkaline electrolyzer retained the dominant technology position with approximately 55% of the hydrogen electrolyzer market in 2025. The alkaline system’s fundamental commercial advantages including lower capital cost per megawatt of capacity, absence of the precious metal catalyst materials that define PEM’s most significant cost reduction challenge, and demonstrated 80,000-hour or greater operational lifetime across industrial installations provide a compelling economics case for large-scale green hydrogen projects where capital cost per kilogram of hydrogen production capacity is the dominant investment decision criterion. PEM electrolyzers are the fastest-growing technology at approximately 92% CAGR through 2035, driven by the technology’s superior alignment with the dynamic operating profiles that variable renewable power integration requires, its ability to respond rapidly to fluctuating electricity input from wind and solar sources without the operational stress that alkaline systems experience during rapid load cycling, and the compact modular architecture that simplifies containerized system deployment for projects requiring fast installation timelines and flexible capacity scaling as renewable energy and offtake capacity evolves.

By Application, energy/power generation dominate, mobility grows fastest

Energy and power generation retained the dominant application position with approximately 38% of the hydrogen electrolyzer market in 2025, reflecting the category’s role as the primary commercial context in which electrolyzer systems are currently being deployed at utility scale across the European hydrogen hub projects, offshore wind-to-hydrogen developments, and large-scale solar-to-hydrogen facilities that represent the leading edge of the green hydrogen infrastructure build-out that is attracting the majority of the sector’s investment capital.

Transportation and mobility is the fastest-growing application at approximately 95% CAGR through 2035, propelled by the deployment of hydrogen fuel cell heavy commercial vehicles, buses, trains, and maritime vessels whose green hydrogen fuel requirements are creating near-term electrolyzer demand anchored by fleet operators, port authorities, and transit agencies that are making long-term hydrogen fuel procurement commitments as part of their scope 1 emission reduction strategies.

Regional analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Hydrogen Electrolyzer Market Insights

North America is the fastest-growing regional electrolyzer market, driven primarily by the transformative commercial impact of the Inflation Reduction Act’s clean hydrogen production tax credit that is enabling green hydrogen project economics previously achievable only with extraordinary renewable electricity cost advantages, and the Department of Energy’s USD 7 billion hydrogen hub programme that is creating seven regional green hydrogen ecosystems across the country simultaneously. The United States accounts for approximately 87.4% of North American electrolyzer revenues as the region’s largest market by a substantial margin, with the concentration of IRA-incentivised project development, world-class renewable energy resources, and the political and regulatory support infrastructure that the Biden-era hydrogen strategy established and whose core economic incentive structures have been maintained through subsequent policy cycles.

Europe Hydrogen Electrolyzer Market Insights

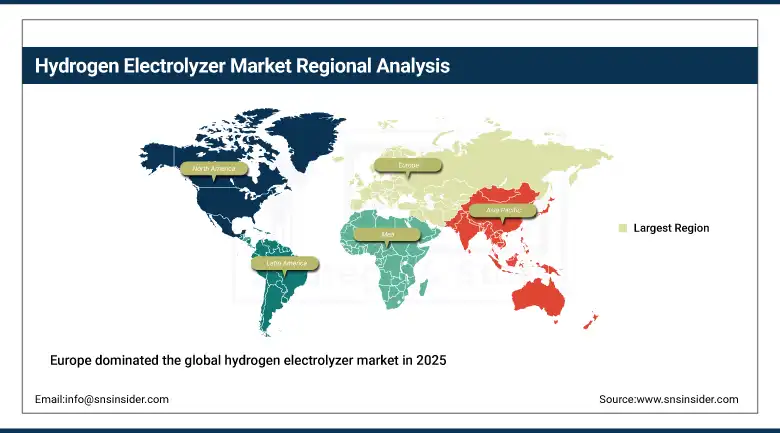

Europe dominated the global hydrogen electrolyzer market in 2025 with the largest regional share, driven by the European Union’s REPowerEU plan targeting 10 million tonnes of domestic green hydrogen production by 2030, the world’s most ambitious national hydrogen strategies across Germany, France, the Netherlands, Spain, and the UK, and the concentration of the most commercially advanced electrolyzer manufacturers globally including Nel ASA, ITM Power, John Cockerill Hydrogen, McPhy Energy, and Sunfire whose European headquarters and primary manufacturing facilities make the region the global centre of electrolyzer technology development and commercial scale-up. Germany accounts for approximately 22.3% of European electrolyzer revenues as the region’s largest national market, with a national hydrogen strategy targeting 10 GW of electrolysis capacity by 2030, major steel industry hydrogen direct reduction commitments from Thyssenkrupp and ArcelorMittal, and the world’s most developed hydrogen distribution infrastructure development programme that collectively create the most commercially active large-scale electrolyzer procurement environment in the global market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Hydrogen Electrolyzer Market Insights

Asia Pacific is the fastest-growing regional electrolyzer market by CAGR, driven by China’s extraordinary pace of electrolyzer manufacturing scale-up that has made the country the world’s largest producer of alkaline electrolyzer stacks by volume, Japan’s foundational hydrogen technology programme whose decades of fuel cell and hydrogen infrastructure investment are creating the demand infrastructure for large-scale green hydrogen deployment, South Korea’s ambitious hydrogen economy roadmap targeting hydrogen as a primary clean energy carrier across power generation, transportation, and industry, and Australia’s extraordinary green hydrogen export potential leveraging its world-class solar and wind resources and strategic geographic proximity to major Asian hydrogen import markets. China accounts for approximately 61.7% of Asia Pacific electrolyzer revenues and represents the most consequential manufacturing and deployment force in global electrolyzer markets, as Chinese electrolyzer manufacturers’ rapid capacity expansion and aggressive cost reduction targets are creating the manufacturing economics that will define global alkaline electrolyzer pricing across the forecast period and determine the competitiveness of green hydrogen relative to alternative decarbonisation pathways in the key industrial sectors that green hydrogen must penetrate to fulfil its climate contribution potential.

Latin America and MEA Hydrogen Electrolyzer Market Insights

Latin America and the Middle East and Africa are emerging but strategically significant hydrogen electrolyzer markets where extraordinary renewable energy resources, relatively low land costs, and growing regional policy frameworks for green hydrogen development are creating the conditions for large-scale green hydrogen export project development that will generate significant electrolyzer procurement demand across the forecast period. Saudi Arabia leads Middle East and Africa electrolyzer revenues at approximately 38.4% of the regional total, driven by the Kingdom’s NEOM green hydrogen project that represents one of the world’s largest planned green ammonia production facilities targeting 1.2 million tonnes per year of green ammonia from 4 GW of dedicated renewable power and 2.2 GW of electrolysis capacity, and Saudi Arabia’s broader hydrogen strategy that positions the Kingdom as a major green hydrogen exporter to European and Asian import markets as its renewable energy cost advantages enable competitive green hydrogen production economics. Brazil accounts for approximately 44.2% of Latin American electrolyzer revenues through its exceptional solar and wind resources in the northeast, government green hydrogen export ambitions, and early-stage hub project development in the Pecém and Suápe industrial complexes.

Market Dynamics

Growth drivers: Government hydrogen strategies with unprecedented financial incentives

The primary structural growth drivers for the hydrogen electrolyzer market are the convergence of government hydrogen strategies across the world’s largest economies that are deploying unprecedented financial incentive frameworks—most notably the U.S. Inflation Reduction Act’s clean hydrogen production tax credit and the European Union’s hydrogen bank auction mechanism—that are transforming green hydrogen project economics from marginal to commercially viable at the scale required to attract the private capital that the sector’s gigawatt-scale deployment ambitions demand. The relentless cost reduction trajectory of solar photovoltaic and wind power generation, which has reduced renewable electricity costs by 90% or more across the best resource locations globally over the past decade and is projected to continue declining as manufacturing scale, technology efficiency improvement, and grid infrastructure investment combine to push generation costs toward levels where green hydrogen production costs approach grey hydrogen costs without subsidy support.

Restraints: High electrolyzer capital cost relative to fossil hydrogen production

A significant restraint on the hydrogen electrolyzer market is the substantial capital cost gap between electrolytic green hydrogen production and incumbent fossil hydrogen production pathways, as steam methane reforming without carbon capture produces hydrogen at a fraction of the current cost of green hydrogen via electrolysis in most markets, creating an economic barrier that government subsidy programmes must bridge while manufacturing scale-up and technology efficiency improvement narrow the gap through the cost reduction trajectories that academic and industry analysts project but whose achievement depends on electrolyzer project pipeline conversion rates that current market conditions do not yet guarantee.

Opportunities: Industrial hydrogen demand decarbonization creating gigawatt-scale electrolyzer procurement anchor customers

The industrial hydrogen demand decarbonization opportunity represents the largest near-term electrolyzer market development catalyst, as the world’s approximately 90 million tons of annual fossil hydrogen consumption for ammonia synthesis, petroleum refining, methanol production, and direct reduction ironmaking represents a defined, large-scale, and growing electrolytic replacement demand whose capture is advancing as the production cost gap between green and fossil hydrogen narrows and as carbon pricing, regulatory mandates, and corporate scope 1 emission reduction commitments create financial incentives for industrial operators to initiate the procurement and project development processes that will translate that demand into electrolyzer orders.

Recent Developments

-

2025: Plug Power commissioned a 100 MW PEM electrolyzer plant in New York in July 2025, capable of producing up to 45 tons of green hydrogen daily, representing one of the largest single PEM electrolyzer installations in North America and providing critical real-world performance data for the heavy transport and industrial decarbonization applications that the facility’s output is targeting.

-

2025: Air Liquide and TotalEnergies announced a joint investment of over EUR 1 billion in February 2025 to develop two large-scale low-carbon hydrogen production plants in the Netherlands, including a 200 MW electrolyzer in Rotterdam and a 250 MW electrolyzer in Zeeland, representing one of the largest co-investment commitments in European green hydrogen infrastructure.

-

2025: Siemens Energy and STRABAG were contracted to build one of Europe’s largest electrolysis plants for OMV in Austria, advancing the construction of industrial-scale green hydrogen capacity for refinery decarbonization as OMV pursues its renewable energy and hydrogen transition strategy across its European refining operations.

Hydrogen Electrolyzer Market Key Players are:

-

Nel ASA

-

ITM Power plc

-

Plug Power Inc.

-

Siemens Energy AG

-

Thyssenkrupp Nucera AG

-

John Cockerill Hydrogen

-

McPhy Energy S.A.

-

Sunfire GmbH

-

Cummins Inc.

-

Enapter S.r.l.

-

Air Products and Chemicals Inc.

-

Air Liquide S.A.

-

Topsoe A/S

-

Bloom Energy Corporation

-

H2B2 Electrolysis Technologies

-

ELB Elektrolyse

-

Asahi Kasei Corporation

-

De Nora SpA

-

Verdagy Inc.

-

Electric Hydrogen Inc.

Hydrogen Electrolyzer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.04 billion |

| Market Size by 2035 | USD 88.74 Billion |

| CAGR | CAGR of 13.48% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Vehicle Type (Commercial Vehicles, Passenger Vehicles) • By Deployment Type (Cloud, On-Premise) • By Communication Technology (Cellular System, Satellite Communication, GNSS, DSRC, Others) • By Industry Vertical (Transportation & Logistics, Construction, Oil & Gas, Utilities, Healthcare, Government & Public Safety, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Samsara Inc., Geotab Inc., Verizon Connect, Trimble Inc., Omnitracs, Webfleet Solutions, Teletrac Navman, Motive, Lytx Inc., Spireon, Azuga, Fleetio, Mix Telematics, Actia Group, Masternaut, Daimler FleetBoard, Microlise Group plc, Transics International, Trackunit A/S, G7 Networks |

Frequently Asked Questions

Europe dominated the hydrogen electrolyzer market in 2025, with Germany as the leading national market within the region

Alkaline electrolyzers dominated with approximately 55% revenue share in 2025.

Government hydrogen strategies with unprecedented financial incentives, most notably the U.S. Inflation Reduction Act’s clean hydrogen production tax credit and the EU hydrogen bank mechanism, are enabling green hydrogen project economics.

The hydrogen electrolyzer market was valued at USD 1.83 billion in 2025.

The hydrogen electrolyzer market is expected to grow at a CAGR of 87.57% from 2026 to 2035.

Get in Touch