Lithium-Ion Battery Anode Market Report Scope & Overview:

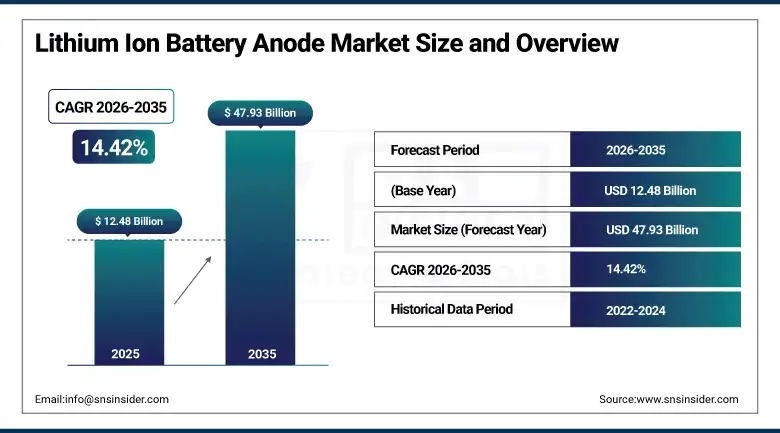

The Lithium-Ion Battery Anode Market was valued at USD 12.48 Billion in 2025 and is expected to reach USD 47.93 Billion by 2035, growing at a CAGR of 14.42% from 2025–2035.

The market for lithium-ion battery anodes is witnessing exponential growth owing to the growing use of electric vehicles and rising demand from consumer electronics and utility-grade battery storage applications. The use of anode materials is essential within lithium-ion batteries since the materials determine the energy density, cycle life, charging rate, and thermal management of the battery cell. Graphite continues to be the preferred choice of anode material in lithium-ion battery anode market due to its supply chain, cost-effectiveness, and ability to work with current manufacturing methods of lithium-ion battery cells. The rising trend of adopting silicon anodes is attributed to the need to increase the specific capacity and charging rate in next-generation batteries.

In 2024, Panasonic Holdings Corporation announced the commencement of commercial production of its next-generation silicon-enhanced graphite composite anode material at its Wakayama facility, achieving a specific capacity of 450 mAh/g compared to 360 mAh/g for conventional graphite anodes. The enhanced energy density enables Tesla's 4680 cylindrical cell programme to achieve higher range per charge cycle, directly addressing the range anxiety barrier that remains the primary consumer hesitation factor in EV adoption across North American and European markets.

Market Size and Forecast

-

Market Size in 2026E: USD 14.28Billion

-

Market Size by 2035: USD 47.93 Billion

-

CAGR: 14.42% from 2025 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Lithium Ion Battery Anode Market - Request Free Sample Report

Lithium-Ion Battery Anode Market Trends

-

Silicon-graphite composite anodes are replacing pure graphite in high-performance EV cells, offering up to 25% higher energy density with improved cycle life management through advanced binder and electrolyte formulations.

-

Synthetic graphite demand is rising as battery manufacturers seek consistent purity and electrochemical performance over natural graphite whose quality variance creates cell production yield risk.

-

Domestic anode material production investment in North America and Europe is accelerating as IRA and EU Battery Regulation local content requirements create supply chain localization incentives.

-

Hard carbon anodes for sodium-ion batteries are emerging as a complementary technology for stationary storage applications where lithium cost reduction pressure motivates alternative chemistry development.

-

Lithium titanate (LTO) anodes are gaining adoption in fast-charging commercial vehicle and grid applications where cycle life exceeding 20,000 cycles and ultra-fast charge capability outweigh the lower energy density trade-off.

U.S. Lithium-Ion Battery Anode Market Outlook

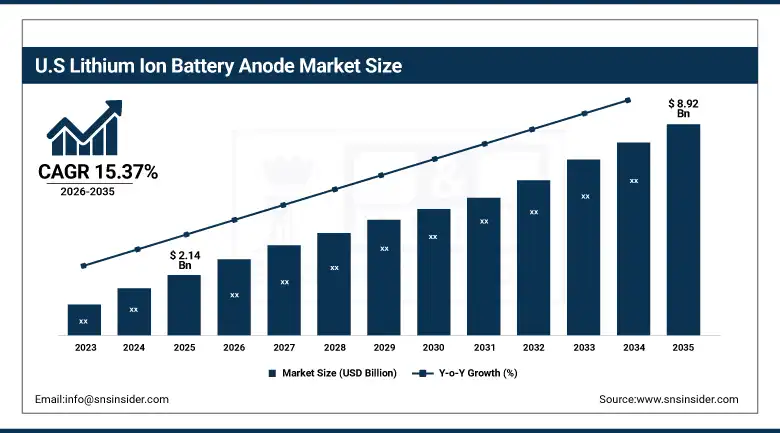

The U.S. Lithium-Ion Battery Anode Market was valued at approximately USD 2.14 Billion in 2025 and is expected to reach approximately USD 8.92 Billion by 2035, growing at a CAGR of approximately 15.37%.

The U.S. is the most strategically significant growth market for lithium-ion battery anodes outside Asia, driven by the Inflation Reduction Act's battery manufacturing tax credit creating substantial domestic cell production investment. Tesla's Nevada Gigafactory, Panasonic's Kansas facility, LG Energy Solution's Michigan and Arizona operations, and Samsung SDI's Indiana plant collectively create a domestic cell manufacturing base whose anode procurement motivates domestic supply chain development. The U.S. government's critical mineral strategy specifically identifies anode-grade graphite and silicon as priority materials whose domestic production and processing capability reduces dependence on Chinese supply that currently accounts for over 80% of global natural graphite anode material processing.

Epsilon Advanced Materials commenced construction of its first U.S. synthetic graphite anode manufacturing facility in North Carolina in 2024, targeting 50,000 metric tons of annual anode capacity to serve domestic battery cell manufacturers whose IRA domestic content requirements create preference for U.S.-sourced anode materials.

Lithium-Ion Battery Anode Market Segment Analysis

-

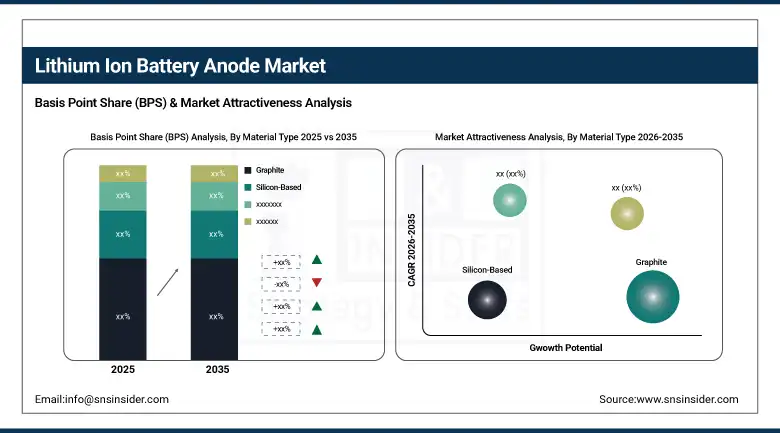

By Material Type, the Graphite segment dominated the lithium-ion battery anode market with 78.4% share in 2025, while the Silicon-Based segment is the fastest growing due to its substantially higher theoretical specific capacity of 3,579 mAh/g compared to graphite's 372 mAh/g, enabling next-generation EV cells to achieve higher energy density within the same volumetric and gravimetric constraints.

-

By Application, the Electric Vehicles segment dominated the lithium-ion battery anode market with 52.3% share in 2025, while the Energy Storage Systems segment is the fastest growing as grid-scale battery deployment for renewable energy integration creates large-format cell procurement whose anode material volume scales with utility storage capacity expansion.

-

By End-Use Industry, the Automotive segment dominated the lithium-ion battery anode market with 54.1% share in 2025, while the Power & Utilities segment is the fastest growing as energy transition investment creates grid storage capacity expansion whose lithium-ion battery procurement creates above-average anode material demand growth compounding with renewable generation capacity addition.

By Material Type, graphite dominates, silicon-based grows fastest

Graphite emerged as the material type market leader with a market share of 78.4% for the lithium-ion battery anode market in 2025. Commercial leadership of graphite is a function of its well-established nature as the standard anode material used since the commercial launch of lithium-ion batteries in the early 1990s. This can be attributed to its presence in the global supply chain in terms of its mining, either naturally sourced from mines in China, Mozambique, and Canada, or synthesized using petroleum coke and coal tar pitch. Its electrochemical stability, understood intercalation process, standard carbonate electrolyte compatibility, and cost per unit energy make it a preferred specification choice.

Silicon-based anodes are the fastest-growing material type because silicon's theoretical specific capacity of 3,579 mAh/g represents nearly ten times graphite's 372 mAh/g, creating a compelling energy density improvement pathway for EV manufacturers whose competitive differentiation increasingly depends on range per charge cycle. The commercial adoption challenge of silicon's approximately 300% volumetric expansion during lithiation, which causes particle fracture and SEI layer instability, is being progressively addressed through silicon-graphite composite formulations, nanostructured silicon designs, and advanced binder systems that constrain expansion while maintaining electrical contact integrity across thousands of charge-discharge cycles.

By Application, electric vehicles dominate, energy storage systems grow fastest

Electric vehicles retained the dominant application position with 52.3% of the lithium-ion battery anode market in 2025. The extraordinary growth of global EV production, from approximately 10 million units in 2022 to a projected 40+ million units annually by 2030, creates aggregate anode material procurement whose scale substantially exceeds any other application segment. Each EV's battery pack requiring 10-100 kg of anode material depending on vehicle segment and battery capacity creates per-unit material intensity that multiplied by EV production volume generates commercial scale that sustains the automotive application's dominant position through the vehicle electrification decade.

Energy storage systems are the fastest-growing application because global grid storage capacity additions are accelerating as renewable energy penetration creates grid stability challenges whose battery storage solution creates systematic anode material procurement. Bloomberg Nef’s projection that global grid battery storage capacity will reach 1,200 GWh by 2030 from approximately 45 GWh in 2022 creates an extraordinary volume growth trajectory whose anode material procurement compounds with EV demand to sustain above-average market growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.6% |

|

Europe |

Germany |

20.8% |

|

Asia Pacific |

China |

52.3% |

|

Middle East & Africa |

Saudi Arabia |

34.7% |

|

Latin America |

Brazil |

46.1% |

North America Lithium-Ion Battery Anode Market Insights

North America is the fastest-growing regional lithium-ion battery anode market, driven by IRA's battery manufacturing tax credit creating above-average domestic cell production investment, the U.S. critical mineral strategy prioritizing anode material supply chain localization, and Canada's natural graphite mining expansion creating regional supply. The United States accounts for approximately 84.6% of North American revenues through domestic cell manufacturing operations, federal battery material processing investment, and the commercial fleet electrification programmer’s battery procurement.

Canada contributes approximately 15.4% of North American revenues through its natural graphite mining operations in Quebec and Ontario, the growing domestic battery manufacturing investment, and the federal critical mineral strategy's processing capacity development programme.

Europe Lithium-Ion Battery Anode Market Insights

Europe is a strategically prioritized anode market where EU Battery Regulation's local content and carbon footprint requirements create domestic supply chain investment motivation, Northvolt's Swedish gigafactory, ACC's French facility, and SVOLT's German plant create regional anode procurement, and the European Battery Alliance's supply chain localization programme supports anode material processing capacity development. Germany accounts for approximately 20.8% of European revenues through its automotive OEM sector's EV programme battery procurement, the Tier 1 battery supplier's German operations, and the federal government's battery value chain investment programme.

France, Sweden, and Poland are significant secondary markets where gigafactory construction, EV production expansion, and renewable energy storage deployment create consistent anode material procurement that compounds with the European battery manufacturing scale-up.

Asia Pacific Lithium-Ion Battery Anode Market Insights

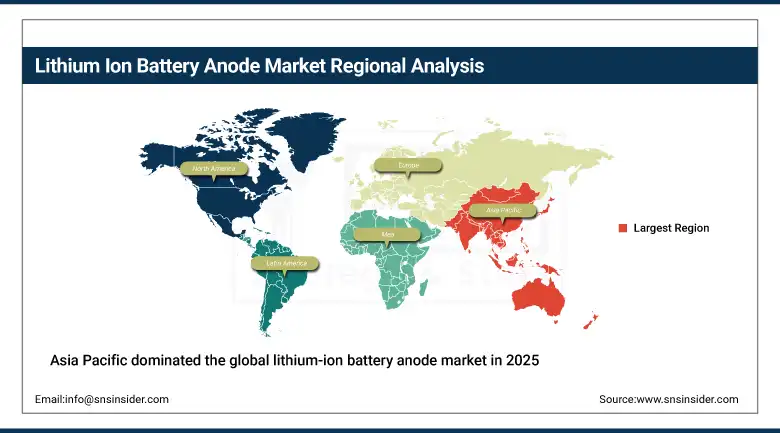

Asia Pacific dominated the global lithium-ion battery anode market in 2025 as the world's largest battery manufacturing region. China accounts for approximately 52.3% of Asia Pacific revenues through its position as the world's largest lithium-ion battery producer, with CATL, BYD, and CALB's combined annual cell production capacity exceeding 1,000 GWh creating the most commercially significant anode material procurement globally. China's integrated anode supply chain encompassing natural graphite mining, purification, and spheroidization processing, combined with synthetic graphite production from domestic petroleum coke, creates cost-competitive anode material supply that sustains Chinese cell manufacturers' global competitiveness.

Japan and South Korea are significant secondary markets where Panasonic's 4680 cell programme, Samsung SDI's premium EV cell production, and LG Energy Solution's global cell manufacturing operations create above-average anode material quality specifications whose silicon-enhanced and high-purity graphite procurement creates premium market segments.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Lithium-Ion Battery Anode Market Insights

Saudi Arabia leads MEA revenues at approximately 34.7% through its Vision 2030 battery manufacturing investment, the nascent domestic EV production programme, and the grid storage deployment for renewable energy integration in its solar capacity expansion. Brazil leads Latin American revenues at approximately 46.1% through its natural graphite mining operations, the growing domestic EV market, and the emerging battery manufacturing investment programme whose localization creates anode material procurement development.

Mozambique's natural graphite mining expansion and South Africa's battery energy storage system deployment create significant MEA secondary market contributions whose anode material production and procurement reflect the region's progressive battery value chain development.

Market Dynamics

Growth Drivers: EV adoption creating above-average anode material demand and energy storage deployment compounding procurement

Electric vehicle adoption is the lithium-ion battery anode market's most commercially significant growth driver. Each percentage point increase in global EV market penetration creates proportional anode material procurement growth whose compound trajectory generates commercial scale that sustains above-average market expansion through 2035. IEA's Net Zero scenario projecting 45% of new vehicle sales being EVs by 2030 creates a demand trajectory whose anode material component grows in direct proportion to battery capacity deployment, creating predictable long-term procurement visibility that motivates supply chain investment.

Grid-scale energy storage deployment for renewable energy integration creates anode material demand that compounds with EV procurement to sustain above-average market growth independent of any single application's trajectory. Each gigawatt-hour of grid storage capacity addition requiring approximately 500-700 metric tons of anode material creates procurement that scales with the global energy transition investment whose annual battery storage addition is projected to grow from 45 GWh in 2022 to over 500 GWh annually by 2030.

Restraints: Natural graphite supply concentration in China and silicon anode cycle life commercialization challenge

Natural graphite supply concentration creates anode market vulnerability whose China's approximately 65% share of global natural graphite mining and over 80% share of anode-grade purification processing creates geopolitical supply risk that Western battery manufacturers and governments are actively seeking to reduce through domestic production investment. Each export restriction episode or trade policy change that affects Chinese graphite supply creates battery production planning uncertainty whose commercial impact motivates supply chain diversification at above-market cost.

Silicon anode commercialization challenge creates a technical barrier whose volumetric expansion, SEI layer instability, and cycle life limitation relative to graphite requires substantial material science and cell engineering investment before widespread adoption in mainstream EV applications. Each silicon anode product launch that fails to meet automotive-grade cycle life requirements creates market confidence setback that sustains graphite's dominant position beyond the timeline that silicon's energy density advantage would otherwise motivate.

Opportunities: Domestic anode manufacturing localization and next-generation silicon-dominant anode development

Domestic anode manufacturing localization represents the most commercially transformative near-term opportunity whose IRA battery manufacturing tax credit, EU Battery Regulation local content requirement, and national critical mineral strategies create substantial investment incentive for non-Chinese anode production capacity development. Each new domestic anode manufacturing facility that achieves competitive cost structure relative to Chinese alternatives creates supply chain diversification that reduces geopolitical risk while creating commercial relationships with domestic cell manufacturers whose IRA and EU compliance requires local anode sourcing.

Next-generation silicon-dominant anode development represents a premium long-term opportunity whose successful commercialization at automotive-grade cycle life and cost creates a fundamental battery energy density step-change that sustains EV competitive differentiation. Each silicon anode breakthrough that extends cycle life while maintaining high specific capacity creates above-average commercial value relative to graphite alternatives, establishing technology leadership positions for material suppliers and cell manufacturers who successfully navigate the engineering challenge.

Recent Developments:

-

2024: Panasonic Holdings commenced commercial production of silicon-enhanced graphite composite anode material at its Wakayama facility, achieving 450 mAh/g specific capacity for Tesla's 4680 cylindrical cell programme, enabling higher energy density and extended driving range per charge cycle.

-

2024: Epsilon Advanced Materials announced construction of its first U.S. synthetic graphite anode manufacturing facility in North Carolina targeting 50,000 metric tons annual capacity to serve domestic battery cell manufacturers under IRA domestic content requirements.

-

2024: Group14 Technologies expanded its silicon carbon composite anode material production capacity in Moses Lake, Washington, supplying Porsche's high-performance EV battery programme whose ultra-fast charging requirement creates above-average silicon anode content specification.

Lithium-Ion Battery Anode Market Key Players

-

Showa Denko K.K. (Resonac)

-

Hitachi Chemical Co., Ltd.

-

Mitsubishi Chemical Corporation

-

BTR New Material Group Co., Ltd.

-

Shanshan Corporation

-

Jiangxi Zichen Technology Co., Ltd.

-

Nippon Carbon Co., Ltd.

-

Kureha Corporation

-

Epsilon Advanced Materials

-

Group14 Technologies

-

Nexeon Limited

-

Sila Nanotechnologies Inc.

-

Panasonic Holdings Corporation

-

SGL Carbon SE

-

Targray Technology International Inc.

-

Elcan Industries Inc.

-

Imerys S.A.

-

Novonix Limited

-

Superior Graphite Co.

-

Tokai Carbon Co., Ltd

Lithium-Ion Battery Anode Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.48 Billion |

| Market Size by 2035 | USD 47.93 Billion |

| CAGR | CAGR of 14.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Graphite, Silicon-Based, Lithium Titanate (LTO), Hard Carbon, Others) • By Application (Consumer Electronics, Electric Vehicles, Energy Storage Systems, Industrial, Others) • By End-Use Industry (Automotive, Electronics, Power & Utilities, Aerospace & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Showa Denko K.K. (Resonac), Hitachi Chemical Co., Ltd., Mitsubishi Chemical Corporation, BTR New Material Group Co., Ltd., Shanshan Corporation, Jiangxi Zichen Technology Co., Ltd., Nippon Carbon Co., Ltd., Kureha Corporation, Epsilon Advanced Materials, Group14 Technologies, Nexeon Limited, Sila Nanotechnologies Inc., Panasonic Holdings Corporation, SGL Carbon SE, Targray Technology International Inc., Elcan Industries Inc., Imerys S.A., Novonix Limited, Superior Graphite Co., and Tokai Carbon Co., Ltd. |

Frequently Asked Questions

The Lithium-Ion Battery Anode Market is expected to grow at a CAGR of 14.42% from 2025 to 2035.

The Lithium-Ion Battery Anode Market was valued at USD 12.48 Billion in 2025.

Accelerating electric vehicle adoption creating above-average anode material demand growth, and large-scale grid energy storage deployment compounding EV procurement to sustain above-average market expansion through 2035.

Graphite dominated the Lithium-Ion Battery Anode Market with 78.4% share in 2025, while Silicon-Based is the fastest growing segment.

Electric Vehicles dominated the Lithium-Ion Battery Anode Market with 52.3% share in 2025, while Energy Storage Systems is the fastest growing segment.

Get in Touch